USMC - Global Asset Allocation Viewpoints Q4 2023 - The Last Mile

2023-10-18 12:30:00 ET

Summary

- The global outlook is being troubled by rising rates, oil prices and the U.S. dollar, resulting in investor risk aversion.

- Spiking bond yields are challenging the equity market’s soft landing assumption. With limited prospect of an upgrade to earnings expectations, equity market returns are likely to be muted.

- Higher for longer may extend the bond sell-off, but a modest economic downturn means credit spreads can remain fairly tight.

- REITs may remain under pressure, while commodities’ strong performance may be sustained.

Key themes for 4Q 2023

- Global growth is facing a number of headwinds.

The global outlook is being troubled by rising rates, oil prices and the U.S. dollar, resulting in investor risk aversion. The U.S. faces a consumer-led downturn, although corporate balance sheet strength should ensure it is only mild. - Inflation is decelerating, albeit slowly, and will end the year above target.

Global inflation continues to recede, but deep economic slowdowns will be required to reach global central bank inflation targets. Higher oil prices, if sustained, also threaten to undermine anchored inflation expectations. - Global monetary tightening cycles are nearing the end, but rate cuts are not imminent.

As long as economic growth remains above trend, inflation may resurge, forcing continued caution amongst policymakers and delaying policy rate cuts. - Equities face limited upside as a 2024 soft landing is already priced in.

Spiking bond yields are challenging the equity market’s soft landing assumption. With limited prospect of an upgrade to earnings expectations, equity market returns are likely to be muted - particularly until bond yields peak. - The global bond sell-off is disruptive but adds much-needed income to fixed income.

A nuanced approach is required in fixed income. Higher for longer may extend the bond sell-off, but a modest economic downturn means credit spreads can remain fairly tight. Bonds now generate meaningful portfolio income. - Alternatives provide important diversification against traditional equities and fixed income.

Until bond yields peak, REITs may remain under pressure. Commodities’ strong performance may be sustained. While the less-bearish economic outlook suggests infrastructure exposure is less crucial, inflation mitigation is still required.

Investment themes

Central bank tightening: The last mile

The inflation shock has dissipated significantly, mainly due to the renormalization of supply chains, but has also been helped along by higher policy rates. Inflation remains above central bank targets. However, as a deep economic downturn would likely be required to hit the bullseye, policymakers presumably believe the growth-inflation trade-off is not worth the extra mile of tightening. As such, policy rates are probably close to their peak.

That said, central bankers must remain alert to bubbling price pressures. As long as growth stays above trend, there will be a risk of inflation resurgence. So, while rate hikes are largely complete, rate cuts are not imminent. Policy loosening will only be initiated once economic growth has slowed - hopefully to just below trend, but likely into negative territory.

Short, shallow U.S. downturn

The unique support provided by policymakers during the pandemic enabled households and corporations to firm up the health of their balance sheets. They each entered 2023 with reduced interest rate sensitivity, prompting resiliency in the face of aggressive monetary tightening. But these measures have essentially acted to delay the downturn, not cancel it.

Indeed, the various fiscal support structures for households are now winding down. By early 2024, many consumers will be exposed to the full burden of higher rates. Companies, however, will remain insulated until late 2024, when the corporate debt maturity wall becomes more pressing.

Consumer spending will likely begin to weaken soon, but with still-strong corporate spending offsetting the impact, the forecasted downturn will be limited to just two quarters of modestly negative growth, with only a slight increase in unemployment - a soft recession.

Bonds are back

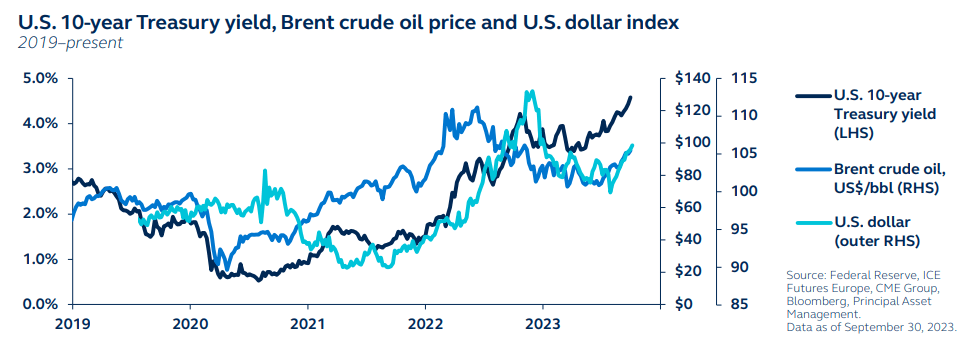

Central banks' reinforcement of the higher-for-longer narrative is clearly behind much of the recent upward spike in global bond yields. Yet there are additional forces at play that suggest bond yields will settle at a permanently higher level.

The U.S. fiscal deficit, already colossal, is projected to balloon in coming years, resulting in large-scale Treasury issuance, both now and in the future. And with the Bank of Japan's eventual move away from ultra-easy monetary policy drawing incremental demand away from U.S. Treasurys, the U.S. government will need to offer a higher interest rate on its bonds to attract buyers.

Higher rates imply greater volatility and lower long-term growth. But for investors, higher rates also indicate that bonds can finally be more than just a diversification tool - the "income" is back in fixed income.

Consider the potential risks

Resurgent inflation: If economic growth fails to slow, it risks igniting a resurgence in price pressures. Central banks would have to respond by resuming policy tightening, tipping economies into deep downturns. Even worse, if growth slows but rising energy prices result in a de-anchoring of inflation expectations, central banks would still need to respond to the stagflationary environment by hiking rates further.

Financial market stress: Previous bond bear markets have ended in financial turmoil. And when combined with rising oil prices and a strengthening U.S. dollar, there is an elevated risk of significant casualties across the global financial system. If bond yields continue to rise relentlessly, something will eventually break.

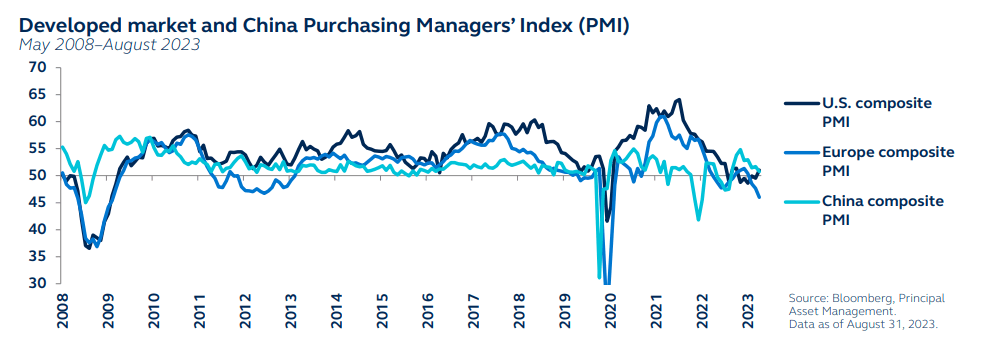

Global economy: Starting to feel the heat

The post-pandemic recovery is starting to ebb as global storm clouds gather. China’s economic story has disappointed as the property sector weighs heavily on consumption. Proactive and meaningful policy support is required if the economy is to hit the 5% growth target. Europe is heading for stagnation, weakened by China’s economic struggles and ECB monetary tightening. And while U.S. growth has exceeded expectations, with consumption headwinds building, growth is poised to decelerate. The convergence of rising interest rates, soaring oil prices, and a strengthening U.S. dollar has created a concerning scenario. Bond vigilantes have reacted to the prolonged period of higher interest rates, while supply cuts in the oil market have put upward pressure on prices. Additionally, the Fed's more hawkish stance compared to other central banks has bolstered the U.S. dollar's value. Collectively, these factors pose a risk to global economic growth, increase the likelihood of inflation, and threaten financial stress. Although there are a few positive aspects in the global economy, such as Japan's recovery from a prolonged period of lackluster growth and India's impressive growth trajectory, the global economic outlook remains weak.

The global outlook looks troubled as rising rates, oil prices and the U.S. dollar threaten to exacerbate economic slowdowns.

{kind=link}

{kind=link}

U.S. economy: After Beyoncé and Taylor Swift

The U.S. economy experienced significant strength in the third quarter of 2023, largely attributed to exceptional consumer spending on special entertainment events like the Beyoncé and Taylor Swift concert tours. However, with challenges beginning to mount for consumers, it is likely that 3Q 2023 marked the pinnacle of this growth.

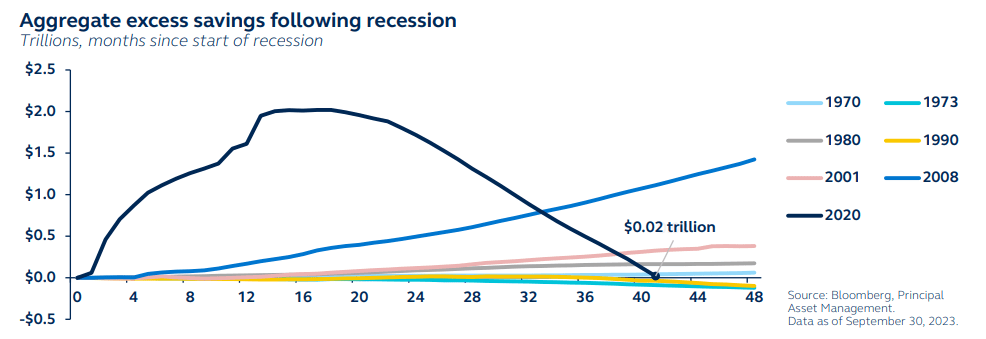

- The significant excess savings cushion, which both fuelled consumer spending and helped prevent a build-up in household indebtedness, has been run down. Assuming the recent pace of drawdown persists, excess household savings will be exhausted within the next few months.

- Various pandemic-related fiscal support measures, such as the resumption of student loan repayments, which according to estimates, will cost U.S. consumers around $18 billion per month, are ending.

While fiscal support and excess savings have shielded consumers from tighter monetary policy, by early 2024, many households will be exposed to the full burden of higher rates.

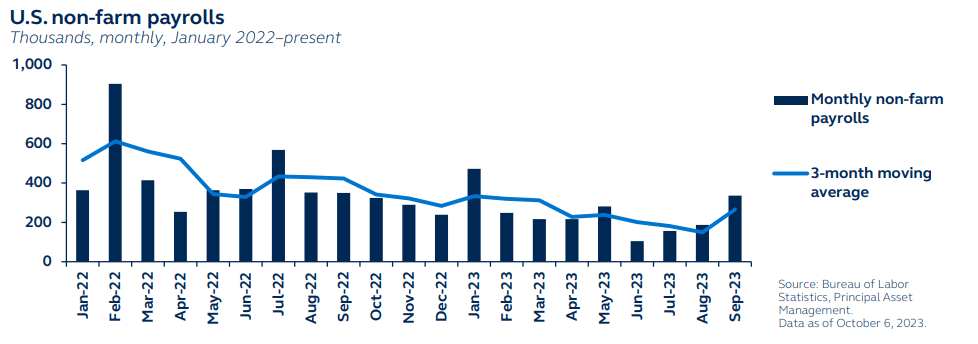

Labor market softness is also likely to weigh on households. Cracks are starting to show, with monthly payrolls numbers steadily trending downwards. A negative jobs growth number could be in the pipeline within the next few months.

Fading excess savings and expiring fiscal support imply that consumers will soon be exposed to the full burden of higher policy rates.

{kind=link}

{kind=link}

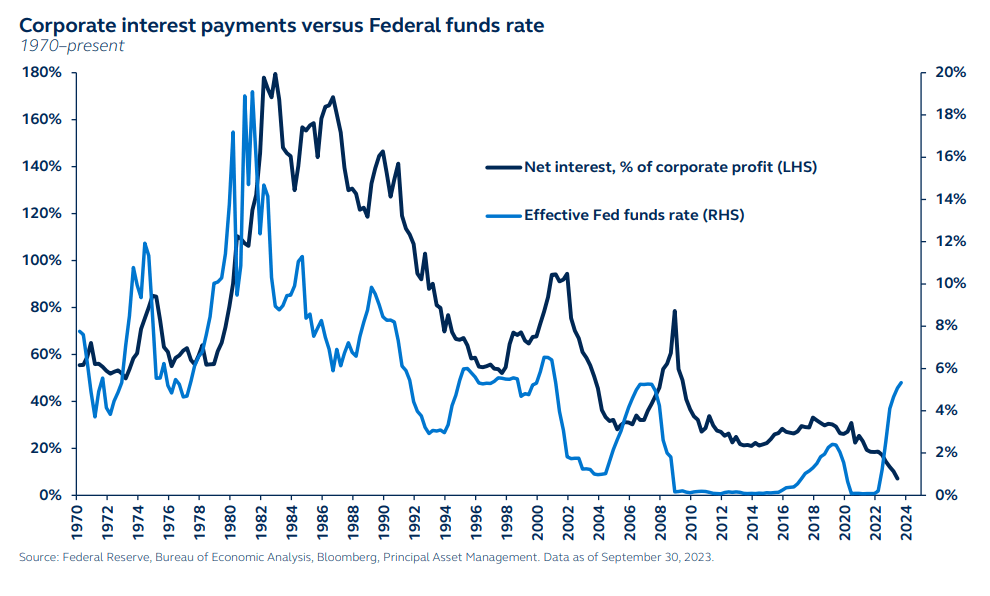

Powell pillow: Insulating the economy from rate hikes

Fed policy acts with "long and variable lags." Today, these lags appear to be extended even longer than usual.

A record corporate debt binge during 2020 and 2021, in response to the Fed’s emergency corporate debt buying facilities, allowed companies to raise significant liquidity, shore up their balance sheets and lock in record low interest rates. As a result, corporate interest burdens have fallen to the lowest levels seen in over 50 years, even as policy rates have risen to their highest level since 2001. If many firms had to refinance their debt next year, the increased cost of servicing that debt could result in severe economic stress. However, the corporate debt maturity wall will remain relatively unchallenging through 2024, so companies will likely continue to be cushioned from higher interest rates. While consumer spending is expected to weaken soon, the impact on economic activity will be somewhat offset by strong corporate spending. As a result, the forecasted economic downturn is expected to be a short and shallow, “soft” recession, extending two quarters, resulting in just a 0.4% drop in economic output, and limiting the rise in the unemployment rate to around 4%.

Companies will remain cushioned from higher rates next year, offsetting consumer weakness, and resulting in only a short and shallow U.S. recession.

{kind=link}

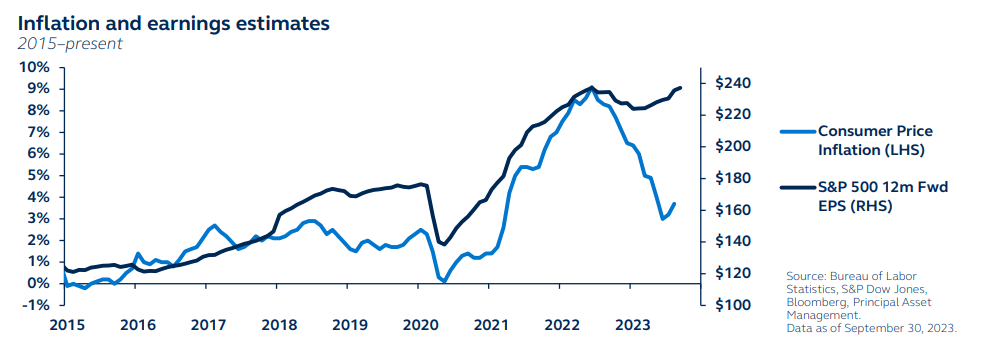

Inflation: In need of a little growth slowdown

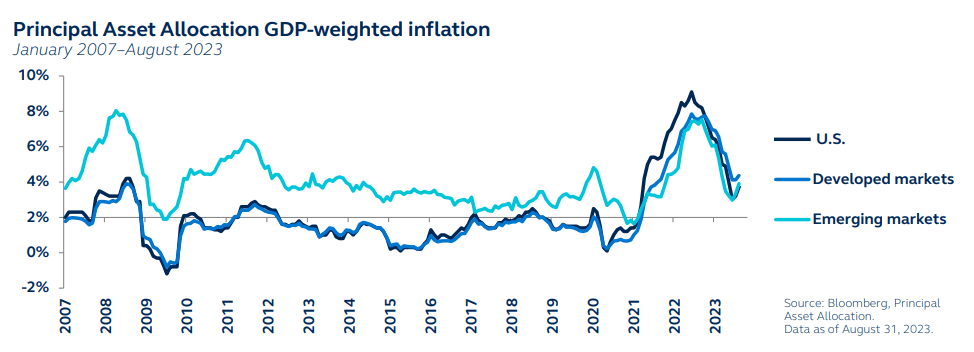

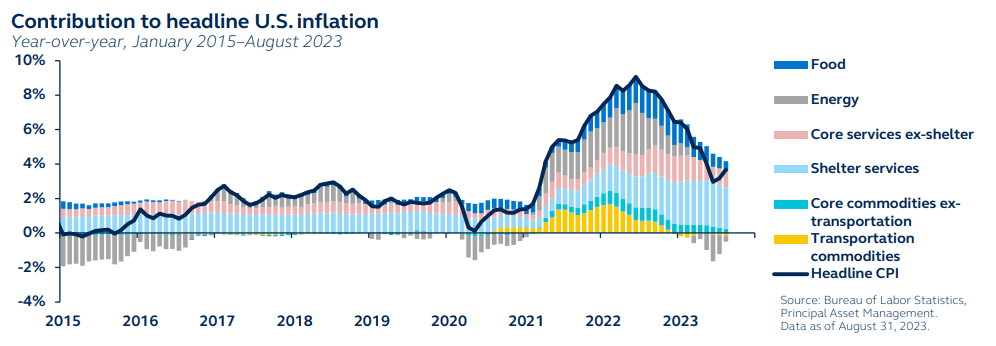

Global economies have made significant headway in reducing inflation. Much of the improvement has been focused on core commodity inflation, where supply chain normalization has helped moderate price pressures.

Yet, particularly in the U.S, economic resiliency has fostered continued stickiness in the core services segment. Without a meaningful economic slowdown, which would serve to rebalance tight labor markets and reduce core services price pressures, inflation is likely to remain above central bank targets. A short, shallow downturn implies that U.S. inflation is set to settle at around 2.5% - a nagging headache for policymakers.

Upside risks to inflation are also emerging. Shipping costs are showing some volatility and slightly threaten the downward trend in core commodities prices. In addition, the recent resurgence in oil prices has already driven up headline inflation.

Central banks will likely look through these developments in the near term. Yet, it is worth noting that, if sustained, higher energy prices can work their way into core inflation and inflation expectations over time. As such, central banks will need to remain alert to inflation risks.

DM central banks have made encouraging disinflation progress. Yet, the final shift lower towards central bank targets would require a meaningful economic slowdown.

{kind=link}

{kind=link}

Central banks: Higher for longer

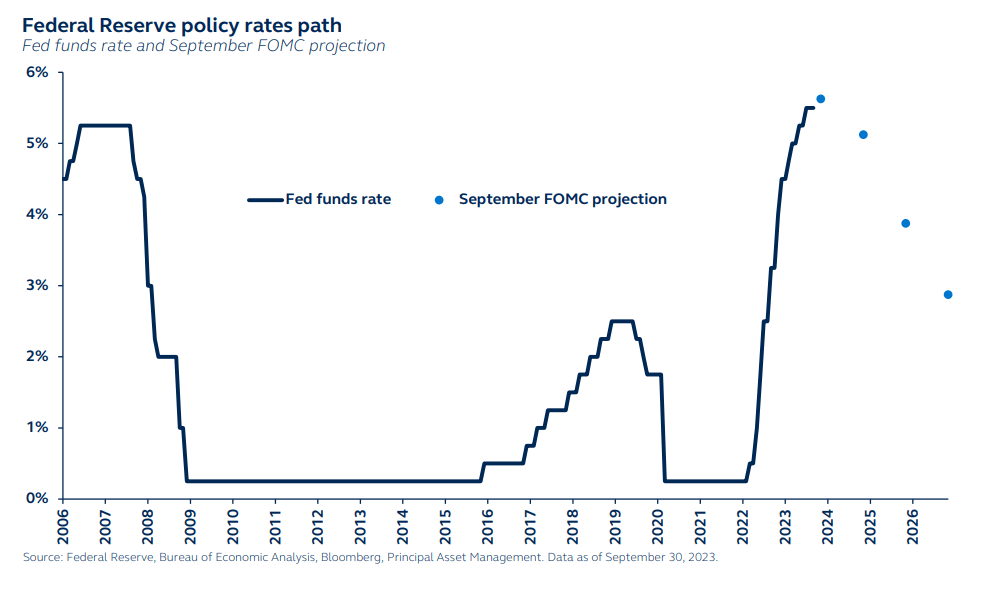

Central banks are nearing the end of one of the most aggressive global monetary tightening cycles in history.

Yet, while a peak in Fed rates will close the chapter on a key discomfort that has plagued markets and investors since late 2022, it does not necessarily open the door to imminent rate cuts. As long as economic growth remains above trend, there will be a risk that inflation picks up again, forcing continued caution amongst policymakers.

Inflation doesn’t necessarily need to fall all the way to 2% before the Fed loosens policy, but they will need to be confident that inflation is heading downward. Gradual rate cuts will begin only once the labor market shows clear signs of weakness, not before the end of 2Q 2024. Risks are, however, tilted to the upside. If economic growth continues to ignore tighter monetary conditions and remains strong, renewed inflation risks would trigger additional rate hikes - and an even-higher-for-even-longer narrative.

While most other developed market central banks are also nearing the end of their tightening cycles, the Bank of Japan is only gradually drifting towards a tighter policy stance, and across emerging markets, decelerating inflation has already permitted some central banks to start cutting rates.

Fed policy rates have likely peaked, but rate cuts will not come until mid-2024 once the labor market shows evident signs of weakness.

{kind=link}

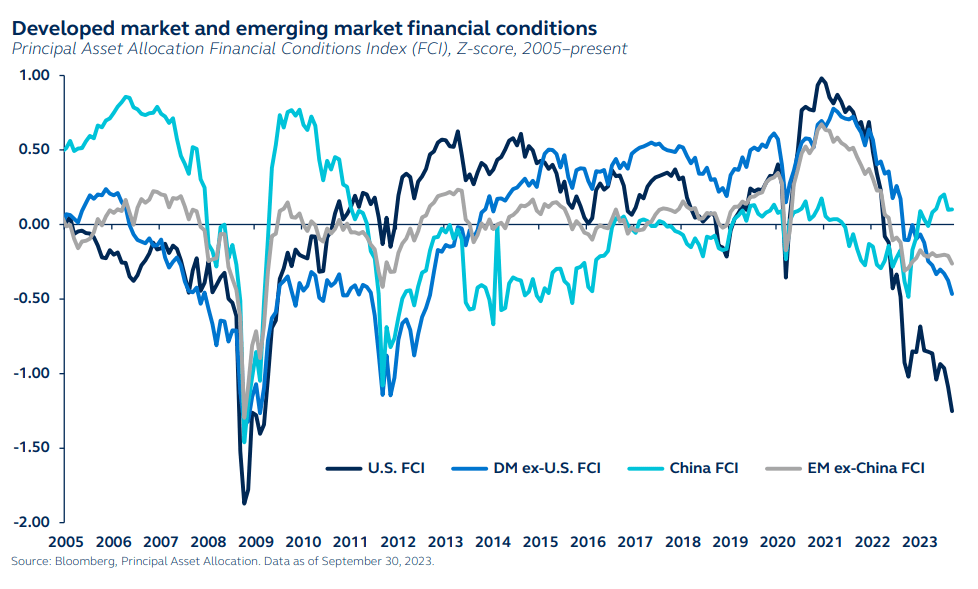

Financial conditions: Disorder and directionless markets

Global financial conditions tightened further in 3Q as the U.S. dollar continued to strengthen and investors finally took heed of developed market central banks’ hawkish messages. Global bonds sold off sharply, taking U.S. Treasury yields to their highest levels since the Great Financial Crisis. At the same time, equity markets fell as investors grew concerned about a prolonged high interest rate environment. Conditions would have tightened even further had it not been for continued resilience in credit markets.

By contrast, financial conditions in China and the broader emerging markets remained relatively loose, in line with the general easing of monetary policy in those regions.

Financial conditions will tighten even further if bond yields creep higher in 4Q. In the less likely scenario where bond yields continue to spike, at some stage, tightening financial conditions would threaten financial stress.

Until bond yields peak, potentially only once it becomes apparent that the Fed’s tightening cycle has ended, risk assets will be subject to continued investor caution and elevated volatility. A temporary period of disorderly, directionless markets is likely, and diversification will be key.

If financial conditions continue to tighten, they will extend the current period of disorderly markets.

{kind=link}

Equities

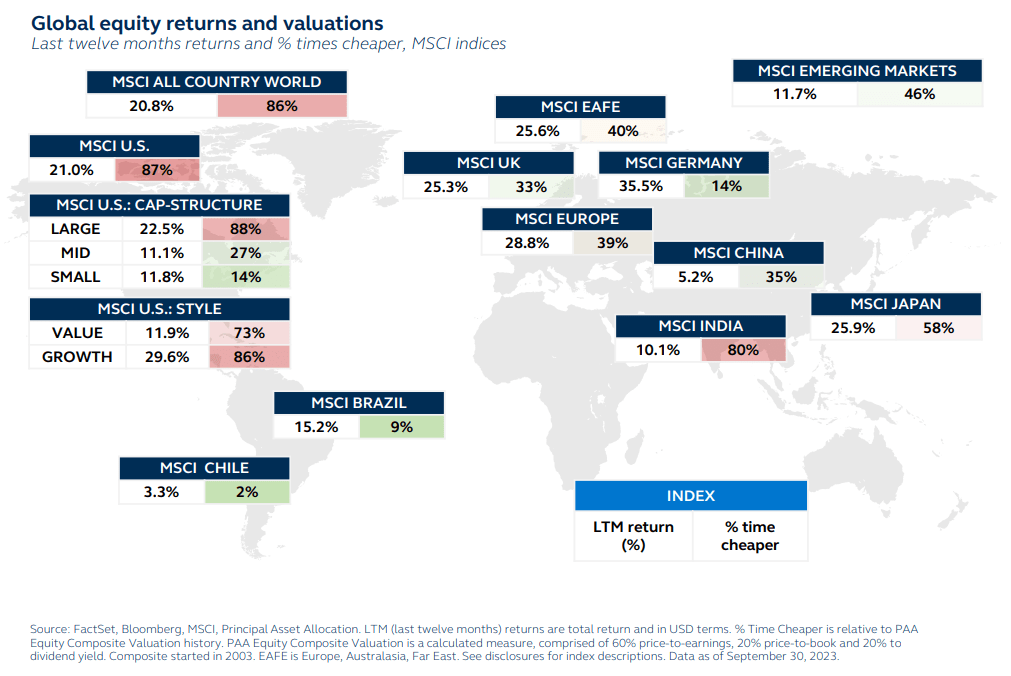

Global equity valuations remain stretched

Despite a strong earnings season, global equities lost momentum in 3Q, with most major markets posting mildly negative quarterly returns. Equities in Europe and China continued to underperform, weighed down by economic headwinds. U.S. and Japan equities were initially supported by their resilient economic activity. Still, hawkish Fed commentary and spiking bond yields in September presented significant headwinds, with the bond sell-off particularly impacting richly valued mega caps.

The broad market pullback meant global valuations became slightly more attractive in 3Q. U.S. large-cap and growth remained the most expensive markets, while small- and midcap valuations remained appealing. Japan's valuations moved back towards their historical medians, while Europe cheapened to below its historical median. Within Europe, Germany has become very undervalued on a historical basis.

EM valuations are still slightly cheaper than the historical median, but regional divergence remains significant. India's valuations are stretched and have been cheaper 80% of the time. By contrast, Latin America still looks attractive, with Brazil and Chile having been cheaper only 9% and 2% of the time, respectively.

Global equity retreated, but valuations remained stretched. The U.S. remains the most expensive market globally, while Latin America has rarely been cheaper.

{kind=link}

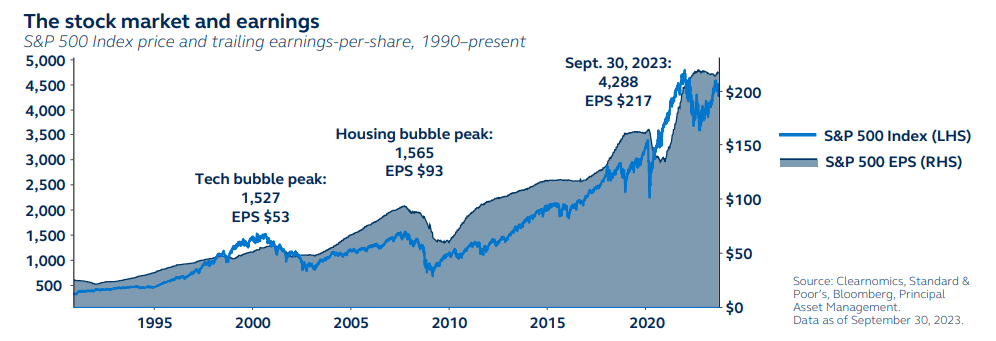

U.S. equities: A soft landing is already priced in

After soaring in the first half of the year, U.S. equities struggled in 3Q. Early in the quarter, equities had performed well as strong reported earnings prompted upward revisions of 2024 earnings growth forecasts and firmed up soft landing expectations. Yet, the significant bond sell-off has challenged both stretched valuations and constructive macro views, resulting in a market pullback.

The 2024 earnings growth outlook is now vulnerable to downward revisions:

- Softening labor markets and eroding excess savings risk curbing consumer demand, a key driver of earnings resiliency.

- Embedded in today’s double-digit 2024 earnings growth expectation is a margin expansion, initially padded by high inflation, but that now faces headwinds as price pressures ease and wage demand plays catch-up.

With limited prospect of an upgrade to earnings expectations, equity market returns will likely be muted - particularly until bond yields peak. Once clear signs of earnings or economic slowdown emerge in late 2023 or even early 2024, equity markets may, at that point, come under renewed pressure.

U.S. equities have already realized soft landing expectations but may be range-bound until clearer signs of economic slowdown emerge.

{kind=link}

{kind=link}

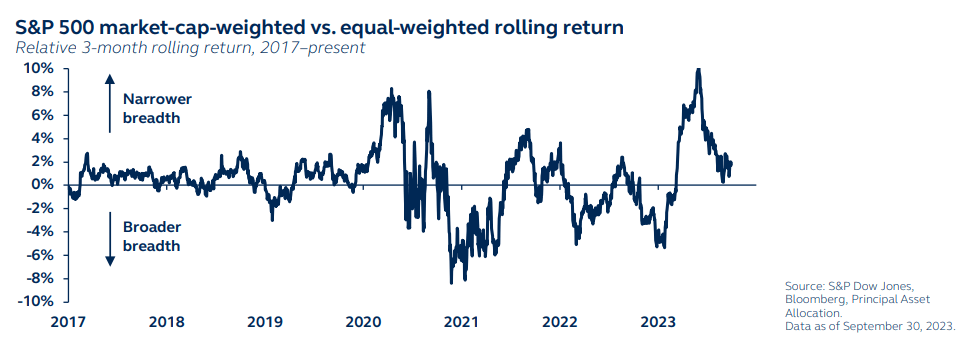

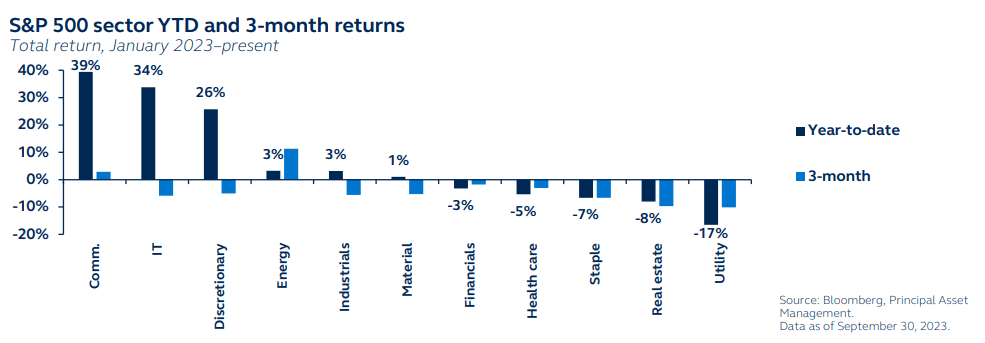

U.S. market leadership: Still a breadth story

The S&P 500’s rally broadened in July as growing hopes of a soft landing encouraged investors to increase their positioning outside the expensively valued tech universe. However, market leadership re-narrowed as 3Q progressed, as tentative signs of labor market softness emerged and PMI activity surveys weakened.

Indeed, other than energy, which has benefitted from the renewed run-up in oil prices, cyclical sectors primarily traded sideways in 3Q, albeit stronger than defensive sectors. Communications, information technology and consumer discretionary remain the top performers year-to-date - artificial intelligence remains the key theme for U.S. equities.

For market breadth to broaden out and stir another bull run, cyclicals need to play catch-up. Consumer demand must defy its various headwinds, and manufacturing activity must stage a strong recovery.

As an economic slowdown emerges in early 2024, broad defensives may deliver stronger performance. Energy stands to continue gaining from elevated oil prices. In addition, while higher bond yields are currently challenging tech companies, the uncertain environment requires strong balance sheets, cash flow, and pricing power - factors that the largest tech companies have plenty of.

Equity market breadth likely to remain narrowly concentrated as the soft landing narrative is challenged.

{kind=link}

{kind=link}

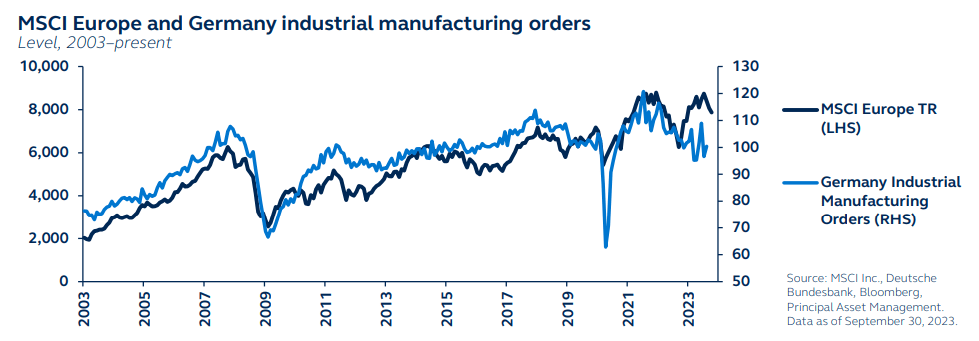

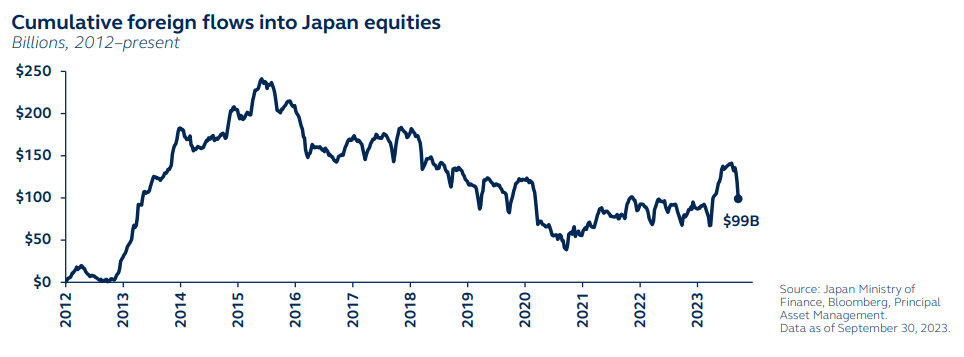

Europe and Japan: Desynchronization in action

The macro themes between Europe and Japan continue to diverge. Europe’s economic outlook is flirting with recession, yet earnings revisions have held up reasonably well, suggesting some downside may be ahead. Europe’s policy outlook will likely also weigh on European earnings as the ECB is set to maintain policy rates at elevated levels even as the economy stagnates. Yet, investors should keep a close eye on China’s outlook as any improvement would suggest some upside for European equities.

In contrast, Japan’s economy has continued to strengthen, but without the high inflation and imbalances that have burdened other DM economies in recent years. Japan’s desynchronization from other developed markets provides an attractive opportunity for diversification.

This desynchronization also means that, while the broader DM space faces the higher-for-longer policy rates narrative, the Bank of Japan has maintained ultra-easy monetary policy. This has led to significant yen weakness, which, in turn, has supported corporate earnings. Although the BoJ has signaled a potential exit from negative interest rates in the coming months, the rate differential between Japan and other DMs will likely remain significant.

An economic slowdown and sticky inflation are weighing on investor sentiment toward Europe, while reflation and easy monetary policy are supporting Japanese equities.

{kind=link}

{kind=link}

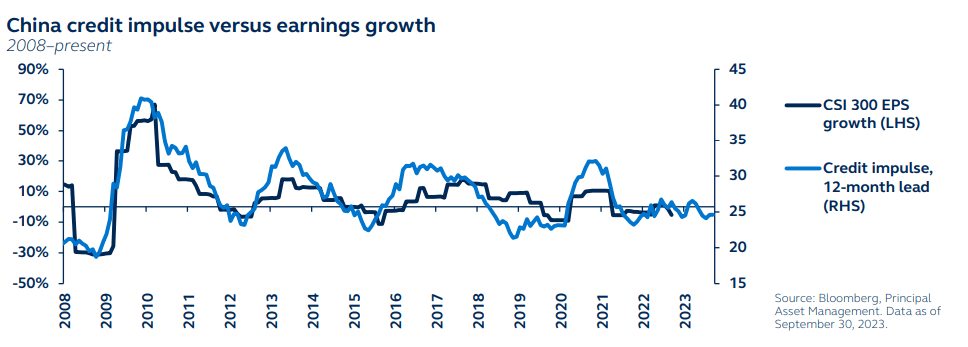

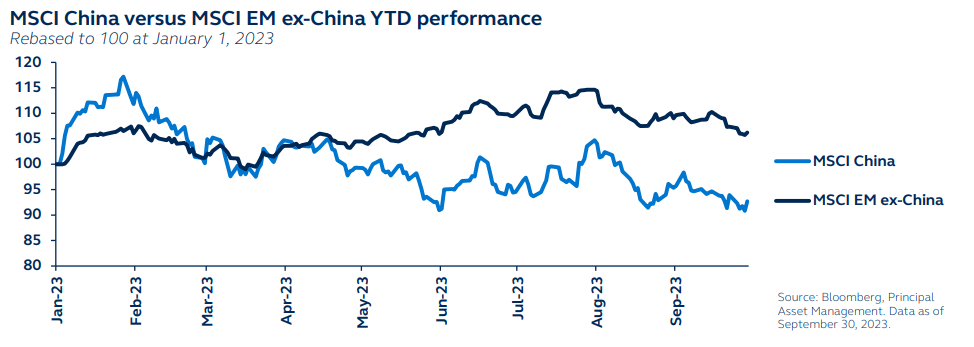

Looking at EM equities through a non-China lens

China’s economy continues to disappoint with pervasive pessimism in household and private sectors, as well as debt problems, preventing recovery. With much of the weakness tracing back to the malfunctioning property sector, policymakers have responded by cutting rates and easing property curbs. However, stimulative policies continue to fall short of expectations, and the credit impulse diminished relative to previous policy easing cycles. Without adequate action from policymakers, investor enthusiasm for investment in China will likely remain subdued.

While investors remain skeptical about China’s outlook, that does not necessarily have to darken the broader EM outlook. Years of underperformance have reduced China’s weight in broader emerging markets, and there are some clear cyclical and secular opportunities across other parts of EM:

- Geopolitical concerns have driven fund flows to destinations of supply chain relocation, such as Mexico.

- Favorable domestic policies have led to improved economic outlooks in countries such as Brazil and India.

- Attractive valuations imply more upside potential, particularly in Latin America.

While disappointing economic activity has prompted more policy stimulus in China, investors remained sceptical. Positives within EM ex-China may compensate the China risk.

{kind=link}

{kind=link}

Fixed income

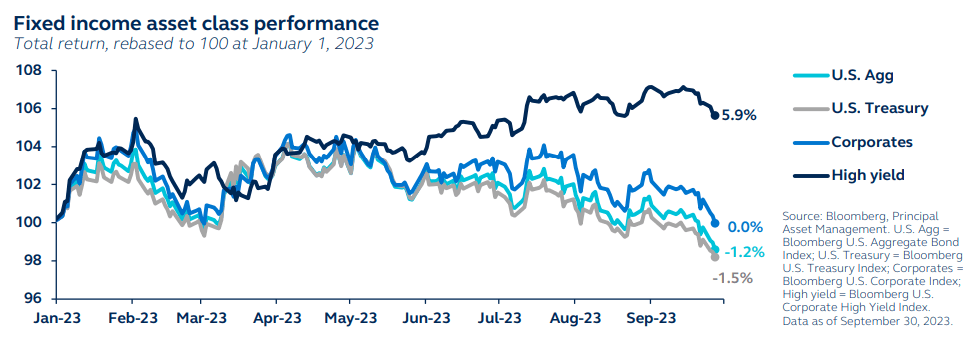

Fixed income: Finally, some meat to eat

While 2023 has been a better year for bonds after last year's bear market, the higher-for-longer narrative, which led to sharply rising interest rates during 3Q, has acted as a significant headwind.

U.S. Treasurys have delivered -1.5% returns this year, down from a peak return of 4.2% in early April. Corporate bond returns have also receded in recent months, but they have outperformed U.S. Treasurys, as continued economic resilience has driven a further tightening in spreads. High yield bonds have even hung onto most of their gains so far this year.

The outlook for a U.S. economic slowdown in 2024 suggests that, eventually, U.S. Treasurys should deliver strong positive returns, while rising defaults may lead to stress in the lower-quality segments of the credit market. However, as clear signs of economic weakness may not be evident until early 2024, government bond yields may drift slightly higher in the near term, and credit is likely to continue outperforming.

The bigger picture is that bonds can now generate more portfolio income than at any other time over the past 15 years. With investors today earning a higher yield on sovereign and high-grade corporate bonds than on equities, fixed income is finally more than just a diversification tool.

Current economic resilience is raising yields but offers valuable opportunities in bonds. Credit should continue to outperform until clear signs of economic weakness become evident.

{kind=link}

{kind=link}

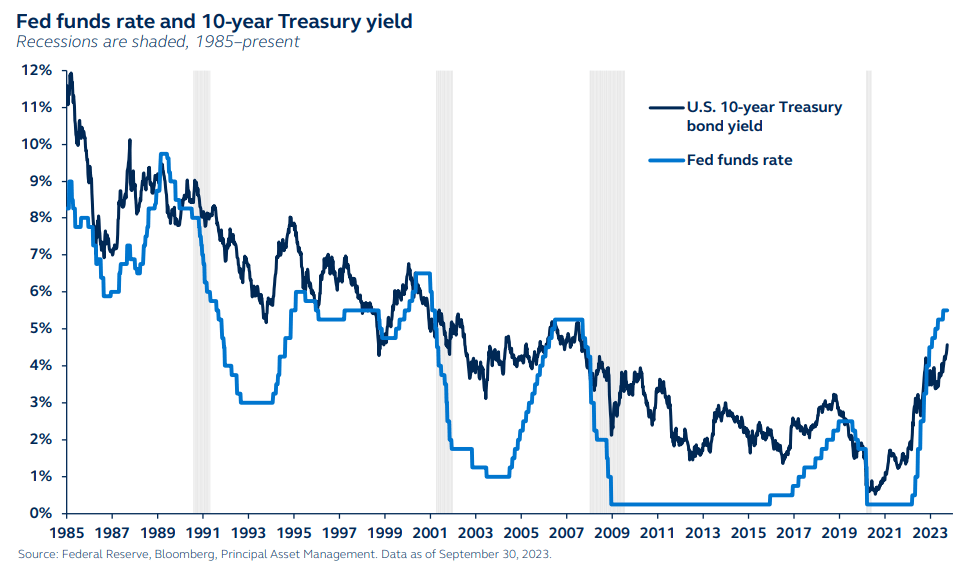

U.S. Treasurys: An uphill struggle

The relentless higher for longer-driven bond sell-off has reached a new milestone. 10-year U.S. Treasury yields hit 4.57% at the end of Q3, the highest level since 2007, up 130 basis points since the regional bank crisis earlier this year.

The move higher in yields is quite extreme. However, while bonds do look better priced, they are not yet convincingly cheap, given the validity of the higher-for-longer narrative. There are also strong technical aspects to the sell-off which are yet to be exhausted:

- The U.S. Treasury’s higher government borrowing estimates have led to a substantial increase in Treasury issuance.

- The Federal Reserve is reducing its balance sheet

- Forthcoming shifts in the Bank of Japan’s yield curve control policies also pose additional upside risk to Treasury yields.

Macro volatility is rising, and Treasury yields may rise further in the short term. Over the medium-term horizon, however, against a backdrop of slowing growth, Treasury yields should revert lower, albeit likely to settle at a higher level than has been custom for the past 15 years. In the meantime, and until that slowdown is realized, investors should maintain a neutral exposure, locking in the sizeable income opportunities but avoiding potential capital losses.

Despite the sharp move higher in yields, rising macro volatility and technical factors imply that near-term duration risks remain. A neutral Treasury positioning is warranted.

{kind=link}

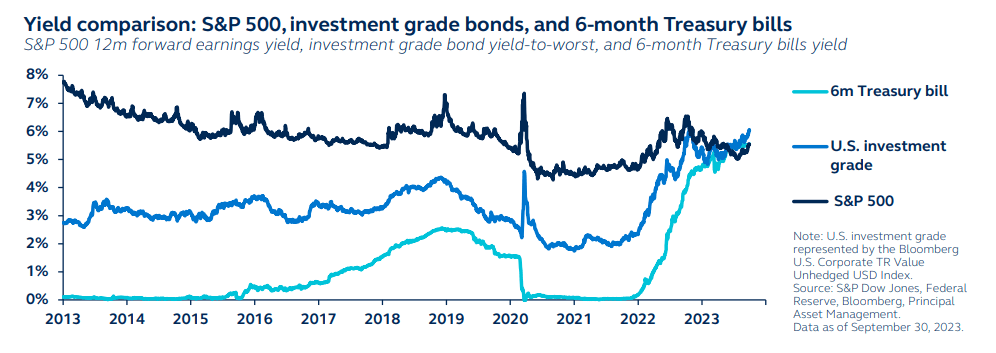

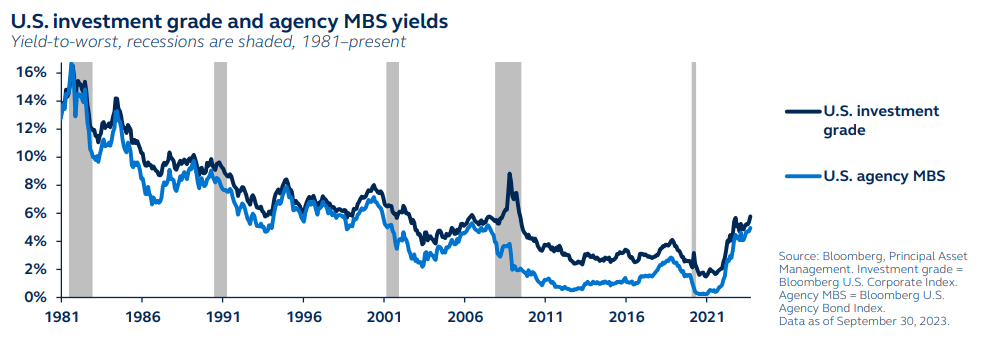

High-quality credit remains favorable ahead of slowdown

Investment-grade credit performed solidly in 3Q as economic resiliency, and its read-through to the Fed policy path, drove up yields but compressed spreads. At these levels, spreads cannot be considered cheap. However, until economic data begins to visibly slow in early 2024, default risk should remain low and risk appetite robust, supporting current spread levels.

There is also a strong income argument for investment-grade credit. After the recent bond sell-off, investment-grade yields have risen to their highest level since the Great Financial Crisis. Similarly, agency MBS yields have increased and also offer attractive income. In addition, agency MBS credit holds investor appeal given that prepayment risks should be muted given the higher-for-longer interest rate backdrop.

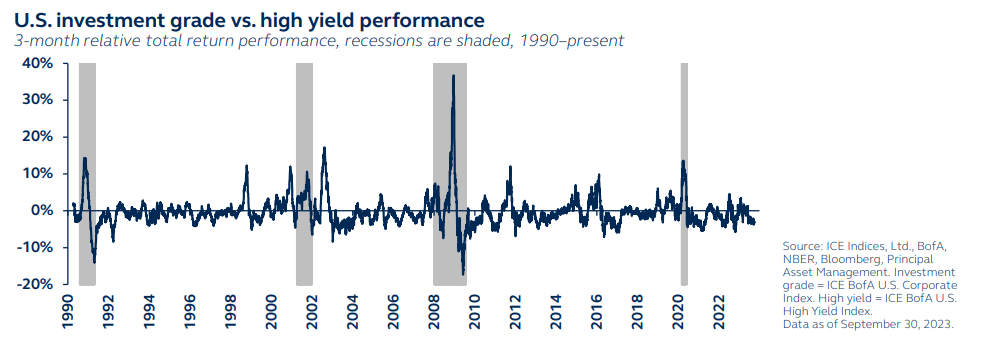

Across the credit spectrum, high-quality bonds underperformed low-quality bonds during 3Q. However, such underperformance is unlikely to be sustained for a prolonged period. While credit markets appear to be inattentive to the risks of an economic downturn, historically, high-quality credits outperform during even milder economic downturns, with relative total returns over shorter periods favoring U.S. investment-grade over high yield issues.

Higher-quality fixed income assets should outperform in an economic downturn, benefitting from tighter spreads and greater stability.

{kind=link}

{kind=link}

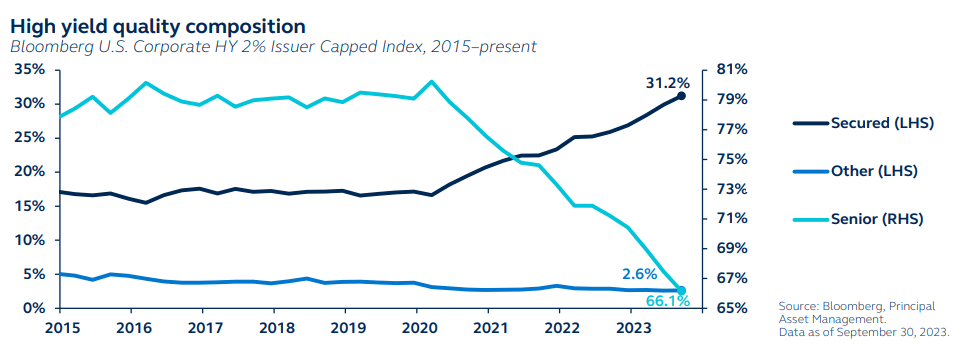

High yield: Carry income and higher quality

High yield bonds were again a bright spot in 3Q. Spreads continued to tighten, closing in on a 17-month low, reflecting economic resilience and growing soft-landing optimism for the U.S. economy. Additionally, the asset classes shorter duration has been beneficial during the recent bond sell-off.

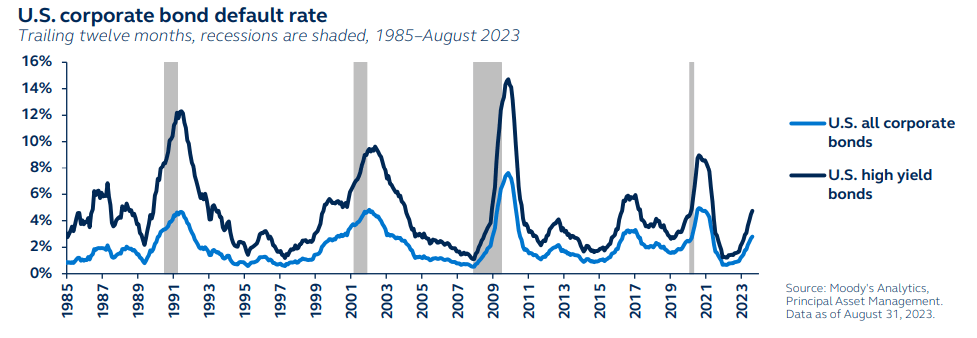

Once the economy starts to slow, high yield will likely come under some pressure. Although default rates have continued to rise, having doubled year-to-date, they appear manageable and are only slightly above their historical average.

Indeed, high yield is much healthier today than in the past:

- Economic resilience suggests that future defaults could be lower than typically expected heading into a slowdown.

- The credit quality of the high yield index today is well above historical norms - supportive of favorable recovery rates in the event of defaults.

- Immediate refinancing pressure remains low. However, the maturity wall will face rollover risks into 2024-2025.

High yield should remain resilient during the upcoming downturn and still maintains a substantial carry advantage for income-seeking investors. Therefore, despite tight spreads, high yield bonds provide an adequate yield buffer against spread widening, even as an economic downturn draws closer.

Stronger high yield credit quality is mitigating the typical risks associated with an approaching economic slowdown.

{kind=link}

{kind=link}

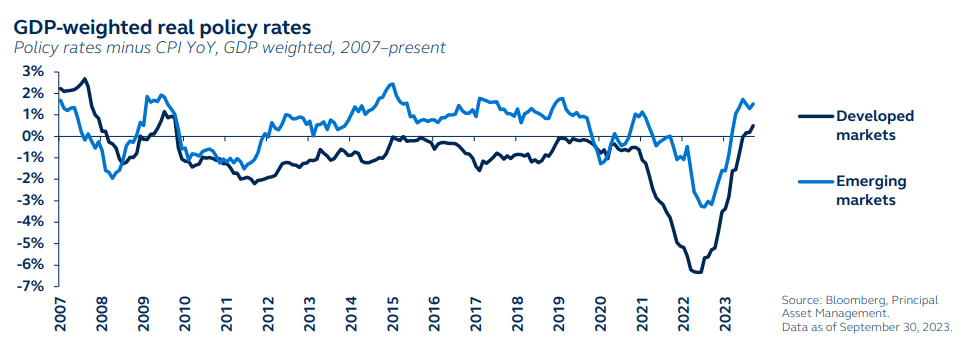

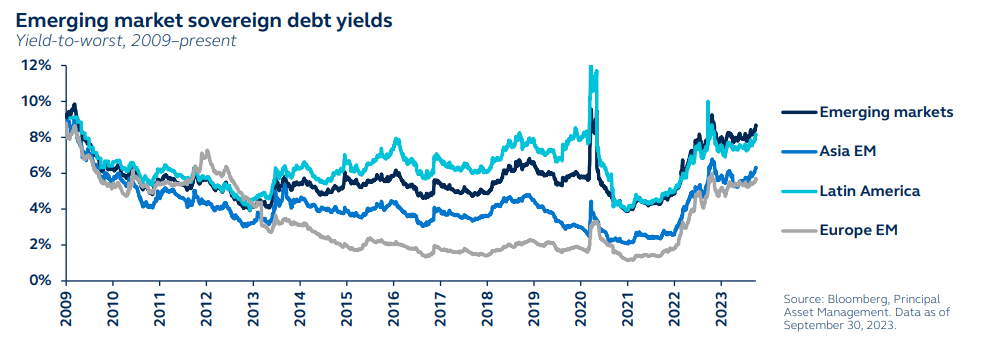

EM debt: Improved outlook but with lingering risks

Given the pro-cyclical nature of emerging market debt ((EMD)), the asset class can see weak performance during economic downturns and tighter credit. However, there are positive catalysts for EMD in the current macro environment.

Despite an expected U.S. slowdown, desynchronized economic cycles suggest EMD may weather this relatively unscathed. Certain regions exhibit favorable energy trade balances, ample FX reserves, political stability, and manageable external debts. These are important and supportive distinctions from the past.

Some emerging market central banks hiked rates before their developed market peers, helping to rein in inflation sooner. As a result, some EMs are now able to lower their policy rates, thereby creating better investment opportunities in local currency bonds. In fact, GDP-weighted real policy rates in EM are higher and falling, while DM rates are still rising. With EMD yields currently at heightened levels, investors can potentially benefit from both capital gains and substantial income.

Decelerating global inflation, slowing U.S. growth, and the Fed possibly ending its campaign of rate hikes should limit U.S. dollar upside - all supportive for emerging market debt.

Of course, risks to EMD remain. A deep liquidity crisis or severe U.S. recession could significantly challenge EMD.

Emerging market debt could escape a U.S. slowdown mostly unscathed. Faster inflation normalization in EM is allowing their central banks to start loosening policy interest rates.

{kind=link}

{kind=link}

Alternatives

Commodities: Unclear demand vs. geopolitics

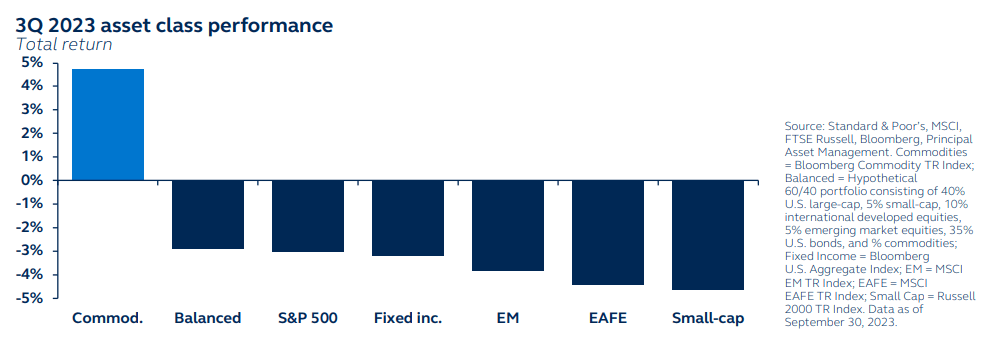

Commodities were the stand-out performers in 3Q, a sharp reversal from its weak performance in the first half of the year. Within the commodity complex, the gains were largely driven by the repricing in oil prices due to OPEC supply cuts and record oil demand.

Near-term dynamics for commodities are unclear. While the looming global growth headwinds suggest demand should slow in the coming quarters, China’s demand for commodities has defied its domestic economic downtrend. If strong demand from China is maintained, there may be only a slight softening in broad global commodity consumption next year. On the supply side, while Saudia Arabia and its OPEC+ partners are likely to extend recent cuts, that will be at least partially offset by increased U.S. oil supply. Ultimately, the mix of uncertain geopolitics, coupled with conflicting demand trends, makes for an uncertain environment.

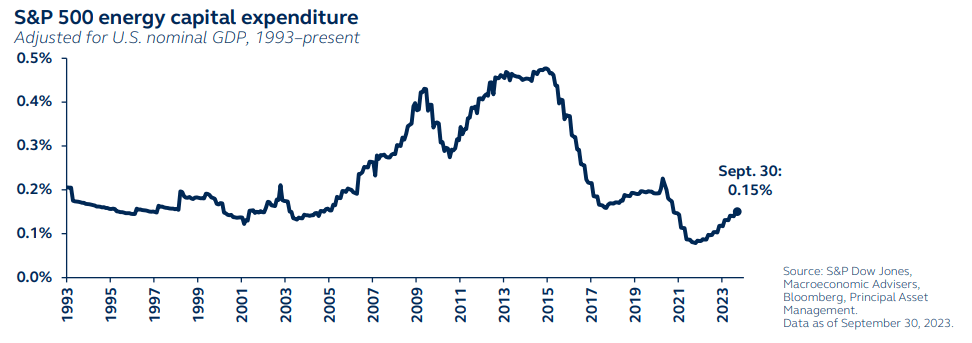

The long-term outlook, however, remains more constructive. Limited capital expenditure in fossil fuels capacity in recent years implies that commodities will likely remain in a long-term state of structural supply deficits that will support commodity prices.

While the near-term commodity outlook is unclear, structural supply deficits mean that long-term trends are clearer and more constructive.

{kind=link}

{kind=link}

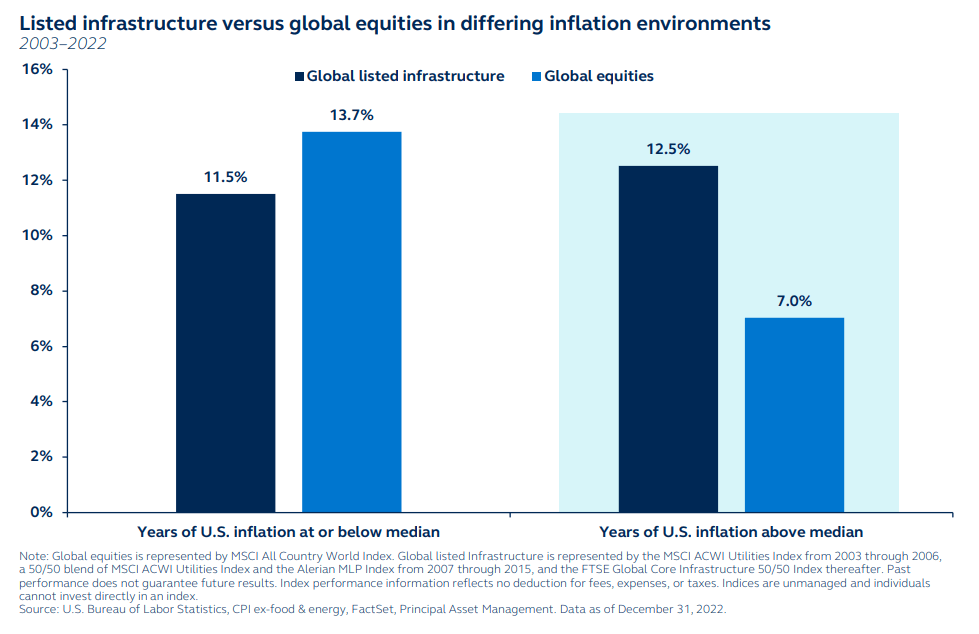

Infrastructure: Down but not out

After a sustained period of outperformance, the economic environment has become slightly less constructive for listed infrastructure.

Typically, the most opportune environment for infrastructure is when inflation is sticky and rising. By contrast, infrastructure may not outperform global equities if the U.S. economy experiences a mild downturn and inflation continues to soften.

Continued economic resilience has meant that, although an economic downturn is expected, it is projected to be only short and shallow. This less bearish economic outlook and its equity beta suggest that infrastructure may perform broadly in line with global equities, thereby deserving a neutral position. An inflation resurgence is a continued threat, and, as a result, infrastructure’s inflation mitigation properties are still required in a portfolio.

In addition, infrastructure investments can offer more stability within a well-diversified portfolio, typically having predictable cash flows associated with the long-lived assets. They also provide exposure to the global theme of decarbonization, which presents a multi-decade tailwind for utilities and renewable infrastructure companies.

While the economic backdrop is no longer as constructive for infrastructure, its predictable cash flows will be important.

{kind=link}

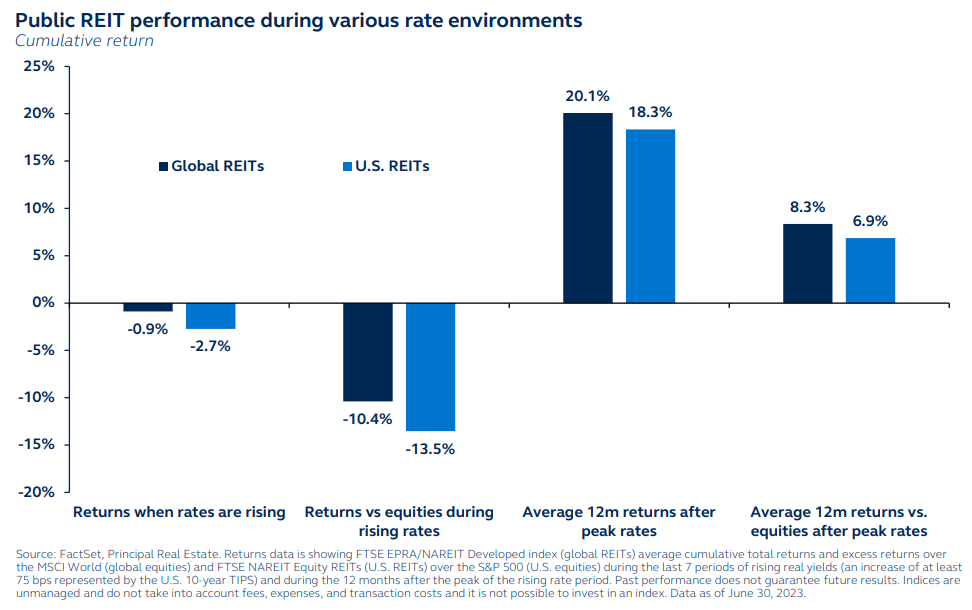

REITs: The punches keep rolling

REITs have faced headwinds for the past 18 months and continue to be challenged, most recently by the sharp bond sell-off as hawkish central bank rhetoric prompted a reconsideration of the interest rate outlook.

The likelihood of a credit crunch triggered by a banking crisis has further compounded the challenges faced by the real estate industry this year. With strict lending regulations and limited capital, the sector may continue to experience difficulties until the underlying issues are resolved. Until then, sluggish real estate transaction markets, pressure on capital values in the private market, and higher loan default risk for over leveraged properties are likely.

As a result of these various factors, the REITs market is deeply discounted and, once rates have peaked, will likely present a compelling opportunity. Indeed, peaking or falling yields have historically been the catalyst for strong REIT market performance as investors typically look to rotate to longer duration, defensive assets.

Office REITs remain the weak spot. Yet, investors should note that traditional office space accounts for only 3% of the overall U.S. REIT market and 6% of the global market. As such, office exposure itself should not deter investors.

REITs have been challenged by the bond sell-off and are now deeply discounted. Once yields have peaked, REITS should offer a compelling opportunity.

{kind=link}

Investment implications

Diversified asset allocation: Shifting to neutral as market uncertainties grow

Equities

Our equities positioning shifts to neutral. Markets have already seen a pullback and, provided the bond yield selloff is almost over, should settle into a flat range until macro weakness becomes apparent later this year or early 2024. Within U.S. equities, large-cap valuations remain stretched. However, we retain a preference for large- over small-cap, given the increasing need for quality, large balance sheets and pricing power, as well as the secular AI trend. Our exposure to ex-U.S. developed markets drops to underweight as concerns about European growth overwhelm our strong optimism for Japan. By contrast, we increased our exposure to emerging markets to a very slight overweight. China’s recovery continues to disappoint, but other EM markets are demonstrating strong valuations, strong fundamentals, or both.

Fixed income

Our fixed income positioning also shifts to neutral, mainly driven by our more cautious view on Treasurys. Although peak Fed rates and slowing growth should ultimately prompt a rally, other technical and secular forces are at work and suggest some potential further upside. We prefer credit over sovereigns, but within credit, we prefer high-quality over low-quality. As such, while investment grade remains at an overweight, high yield continues to sit at neutral. Local currency emerging market debt remains at an overweight as central bank rate cuts should enhance returns - but we acknowledge that the potent combination of spiking U.S. Treasury yields and further dollar strength would dull the outlook.

Alternatives

Alternatives remain at a neutral weighting. Commodities and natural resources move to neutral as the outlook for oil prices remains fairly constructive in light of supply cuts. The more resilient economic backdrop prompts a reduction in our long-held overweight exposure to infrastructure, although the still sticky inflation environment implies inflation protection is still required. REITs valuations have improved significantly, suggesting upside if and when central bank rates peak, and economic growth slows. Yet, until global bonds hit a ceiling, we keep REITs at a neutral. Alternatives continue to play a vital diversification role, particularly against elevated macro volatility.

Alternatives asset class include commodities, natural resources, infrastructure, REITs, and hedge funds. Allocations across the investment outlook can be proportionately adjusted so magnitudes across categories do not have to net to neutral. Data as of September 30, 2023.

| Equities Reduce risk appetite and focus on U.S. large-cap and quality factor. |

| Position toward certainty • Exposure to quality within equities can potentially offer risk mitigation during pullbacks. • Attractive international valuations suggest opportunities outside the U.S. • U.S. large-cap offers stronger geographical revenue exposure and more attractive valuations. |

| How to implement • Large-cap U.S. strategies • Quality-biased active managers • Well-diversified and active international managers |

| Fixed income Increase exposure to high-quality credit. |

| High-quality, core fixed income and total return positioning • Core fixed income to hide out in as recession risk rises. • Increasing duration bias across the asset class. • Emerging market debt may offer total return potential with central bank easing. • High yield maintains a substantial carry advantage for income-seeking investors. |

| How to implement • IG credit heavy core fixed income • Agency MBS strategies • Active emerging market debt |

| Alternatives Pursue less correlated real asset exposures. |

| Real assets • Real return-focused strategies gain attractiveness when nominal growth slows. • Infrastructure offers more stable cash flows with potentially attractive yield. • Real assets can help mitigate inflation risk. |

| How to implement • Diversified real asset strategies (infrastructure, natural resources) • Private real estate markets |

For further details see:

Global Asset Allocation Viewpoints, Q4 2023 - The Last Mile