GIC - Global Industrial Company: Stepping Back A Bit

2023-08-07 13:02:19 ET

Summary

- Global Industrial Company reported Q2 revenue and profits that exceeded expectations.

- Earnings per share fell short of last year but beat analysts' estimates, resulting in net income of $21.5 million.

- Other profitability metrics were mixed, with operating cash flow increasing but EBITDA falling slightly.

- Even in light of these results, shares look closer to fair value after having risen and after incorporating recent valuation data.

On August 1st, the management team at Global Industrial Company ( GIC ) announced financial results covering the second quarter of the company's 2023 fiscal year. The value-added industrial distributor reported revenue and profits that exceeded analysts' expectations. Relative to how the company performed last year, the picture wasn't great, but it was better than it could have been. In my view, the performance achieved by management, combined with how shares of the enterprise are priced at the moment, both on an absolute basis and relative to similar firms, demonstrates that the company is doing well. But given the uptick in price and a higher valuation than before, I believe that moving it back down to a 'hold' makes sense right now.

Gauging recent performance

In early March of this year, I ended up upgrading my rating on Global Industrial Company from a 'hold' to a 'buy' after seeing the stock plummet 18.5% at a time when the S&P 500 had risen 4.1%. This drop took the company from being fairly valued to being somewhat undervalued. Of course, the downturn that shares experienced were not necessarily unwarranted. The company had been exhibiting weakness on both its top and bottom lines leading up to that point. But even a company that is experiencing fundamental weakness can still make for an attractive prospect if the price is right. Since upgrading the company, things have gone well, but not as well as I would have hoped. Shares have seen an upside of 16.1% at a time when the S&P 500 has gone up 10.5%. So I consider this a solid win for now.

{kind=link}

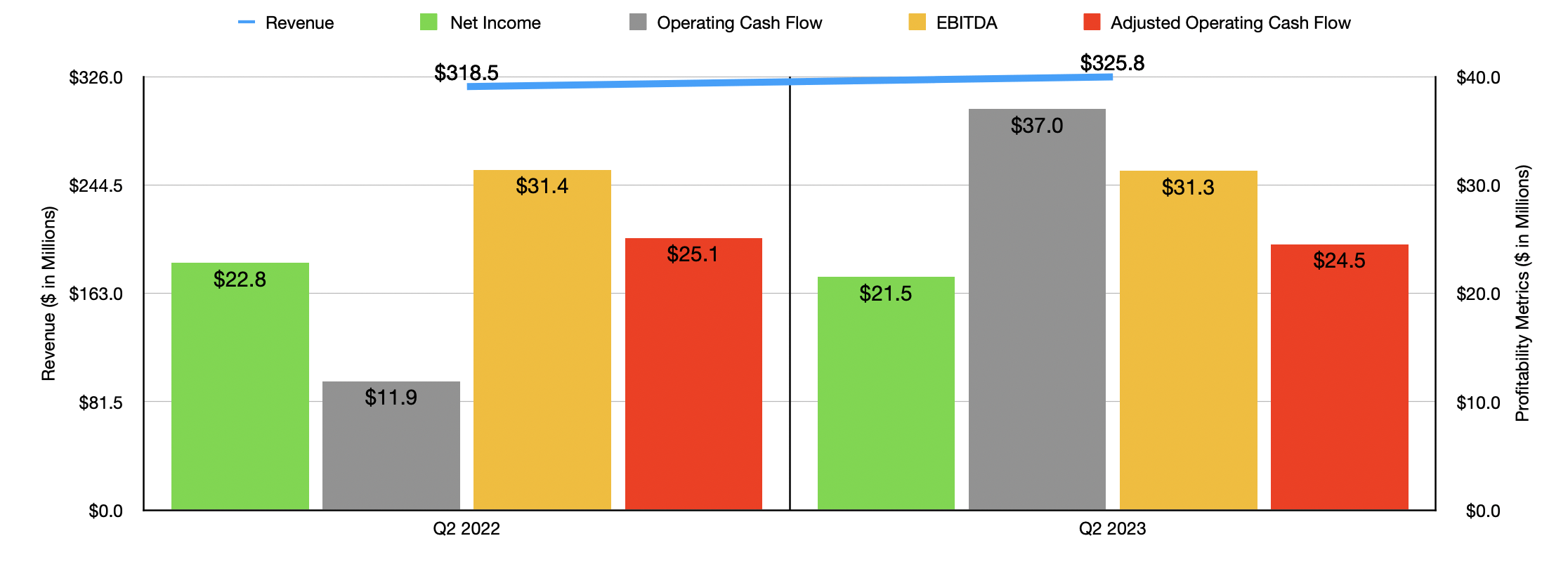

Fast forward to today, and we are now able to digest the most recent financial performance that management reported. This covers the second quarter of the company's 2023 fiscal year. According to management, revenue came in at $325.8 million. That represents an increase of 2.3% over the $318.5 million the firm reported one year earlier. In addition, it also exceeded analysts' forecasts to the tune of $24.4 million. The increase in revenue, according to management, was driven pretty much entirely by the firm's acquisition of Indoff. Without this factored in, revenue would have actually declined by 5.2%. Although product volume shipped decreased, a bigger factor appears to have been price deflation. This should actually excite a lot of market watchers since this indicates that the inflationary pressures that led to high interest rates might be in the early stages of a reversal.

On the bottom line, the picture was somewhat mixed. Earnings per share came in at $0.56. While this fell short of the $0.59 per share that the company reported in the second quarter of 2022, it was $0.14 per share above what analysts thought it would be. This resulted in a net income of $21.5 million compared to the $22.8 million reported at the same time last year. Even though the company benefited from a rise in revenue, the firm's gross profit margin shrank from 35.5% to 34.7%. This decline, management said, largely reflected the aforementioned acquisition's lower gross margin profile. Had it not been for this purchase, the company's gross profit margin actually would have increased modestly to 35.7%. And that would have been largely the result of a change in sales mix.

{kind=link}

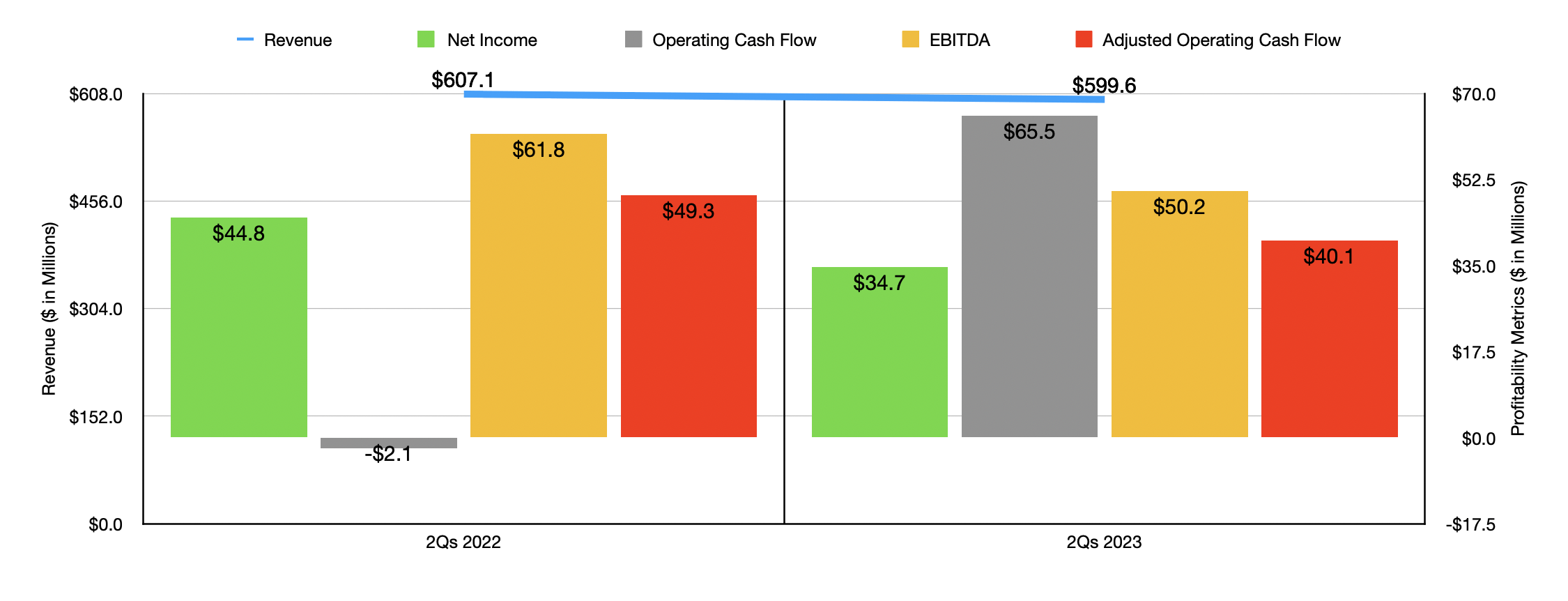

Other profitability metrics for the company were mixed as well for the quarter. Operating cash flow, for instance, more than tripled from $11.9 million to $37 million. As great as this looks, the picture does change if we adjust for changes in working capital, doing this, we actually would have seen a decline from $25.1 million to $24.5 million. Meanwhile, EBITDA for the company fell from $31.4 million to $31.3 million. What's really fascinating about these quarterly results is that they mark an improvement over what the company reported in the first quarter. In the chart above, for instance, you can see financial results for the entirety of the first half of 2023 relative to the same time last year. Even with revenue up in the second quarter, sales in the first half of the year combined were lower than they were in 2022. Profits and cash flows were also meaningfully lower, so most of that pain must have come from the first quarter on its own.

Unfortunately at this time, we don't have much insight into what the 2023 fiscal year in its entirety will look like. In the investor call that management had following the release of earnings, the top brass stated that they expect continued variability throughout this year due to things like seasonality and having to work through higher-cost inventories. In the third quarter of this year, these issues, combined with the Indoff acquisition, should result in the company's consolidated gross margin declining on a year-over-year basis. But unfortunately, we don't know to what extent this will take place.

{kind=link}

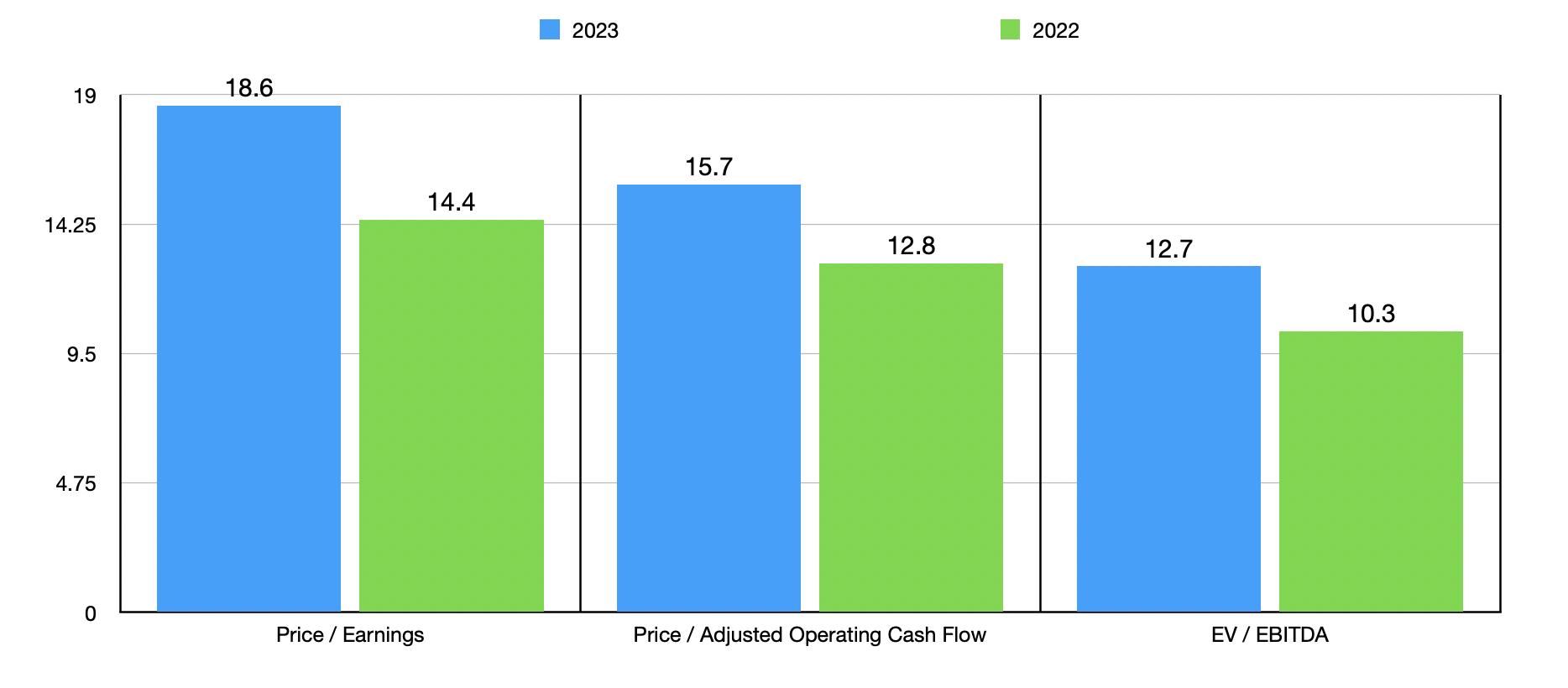

If we simply annualize the results experienced so far for the year, we would expect a net income of $60.5 million. Adjusted operating cash flow would be $71.6 million, while EBITDA would come in at $88.6 million. Using these figures, we can easily value the company as shown in the chart above. As you can see, the stock does look more expensive on a forward basis than if we were to use the results from the 2022 fiscal year. But on the whole, I would say that it's not so pricey as to eliminate any upside. Meanwhile, in the table below, I decided to compare the company to five similar firms. Using both the price-to-earnings approach and the EV-to-EBITDA approach, I found that three of the five companies were cheaper than our prospect. Meanwhile, using the price-to-operating cash flow approach, only one of the companies ended up being cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Global Industrial Company |

| 18.6 |

| 15.7 |

| 12.7 |

| Titan Machinery ( TITN ) |

| 6.3 |

| 64.9 |

| 6.7 |

| MRC Global ( MRC ) |

| 13.8 |

| 97.5 |

| 8.4 |

| BlueLinx Holdings ( BXC ) |

| 4.5 |

| 1.6 |

| 2.6 |

| Transcat ( TRNS ) |

| 64.6 |

| 40.8 |

| 26.3 |

| Alta Equipment Group ( ALTG ) |

| 60.7 |

| 43.5 |

| 8.5 |

Takeaway

Operationally speaking, it's clear to me that Global Industrial Company exceeded expectations and is doing quite well considering the economic environment it's dealing with. I will say that the weakening that has continued into the present day and that looks set to continue makes the company look less appealing than when I wrote about it previously. This, combined with the appreciation that shares experienced since I last wrote about the company, makes me feel as though downgrading the company to a 'hold' makes sense at this time.

For further details see:

Global Industrial Company: Stepping Back A Bit