KBND - Global Macro Outlook - Fourth Quarter 2023

2023-10-18 05:35:00 ET

Summary

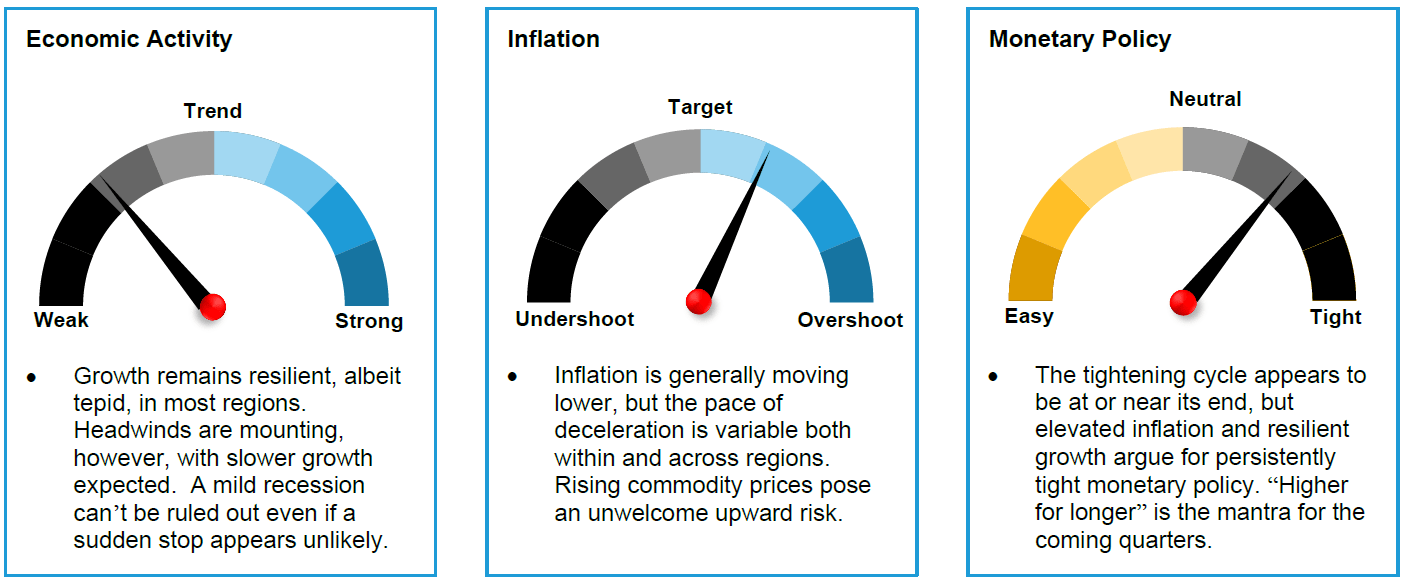

- Years of aggressive monetary conditions have begun to bite, and global central banks appear near the end of their respective tightening cycles.

- Growth in Europe was weaker than the US, since households there had comparatively smaller savings to navigate high inflation.

- Emerging markets have been relatively resilient, with record-level remittances a contributing factor. China’s growth continues to disappoint, primarily due to a longer-term secular slowdown, and we expect further policy easing as a result.

- We now believe the Fed, as well as the Bank of England and European Central Bank, will hold rates for several quarters before undertaking a gradual easing cycle.

- Investors should be optimistic, but watchful of events that could change the picture in the coming quarters.

By Eric Winograd, Adriaan du Toit, Katrina Butt, Armando Armenta, Markus Schneider

The Macro Picture

Last quarter we highlighted the resilience of the global economy, which continued to expand despite a series of shocks this year. Its resilience held largely intact during the third quarter as well, though not uniformly. With global central banks raising borrowing rates significantly over the past few years, tighter monetary conditions have begun to bite—a trend we expect will continue in the coming months and perhaps even accelerate if the recent rise in longer- dated interest rates continues.

Central banks are aware of this, and the Federal Reserve (Fed), the Bank of England ((BOE)) and the European Central Bank (ECB) signaled that they are at or very near the end of their respective tightening cycles. Emerging-market ((EM)) central banks are, as they have been throughout this cycle, ahead of their developed-market ((DM)) peers and some have already begun to cut rates.

The slowdown we anticipate looks manageable at this stage; indeed, it actually looks desirable. Inflation has fallen, but it isn’t yet conclusively headed back to target - we expect it will be several more quarters before inflation is back to normal levels. Slower growth is a necessary precondition for full inflation convergence. As a result, we don’t believe that slower growth should alarm investors or will alarm policymakers. It isn’t until inflation is much lower that DM central banks will be ready to ease conditions and support growth. This means that despite the resilience of the global economy to date, we forecast a protracted period of below-trend growth through 2024 and likely beyond.

Evidence of an impending slowdown is weakest in the US, where growth may have accelerated over the summer, supported by robust consumer spending. Still, we believe that tighter credit conditions, a gradually normalizing labor market and diminished stockpiles of household savings suggest that the next few quarters are unlikely to be as strong as the last few. Seeing strong growth over the summer, the Fed seems the most likely among central banks to raise rates in the fourth quarter, though we don’t expect it. Rising and persistently high energy prices are potentially a complicating variable that would both delay inflation convergence and impede consumer spending. We forecast the Fed to stay on hold for several quarters before undertaking a gradual easing cycle; it would take a large shock that pushed the economy onto a more negative trajectory to lead to earlier or more aggressive rate cuts than that.

Europe’s economic performance was weaker than the US over the summer. European households have had a comparatively smaller savings cushion to rely on during this high-inflationary period, and the cost-of-living crisis has felt more severe in Europe as a result. We anticipate a sharp fall in inflation in Europe in the coming months, as the impact of last year’s massive rise in energy costs falls out of the annual calculation. But it will take some time before underlying inflationary pressures are truly normalized and, as in the US, rising energy prices could further complicate the picture. In the meantime, we expect the ECB and the BOE to follow a Fed-like policy path: watchful waiting for several quarters followed by an eventual pivot to rate cuts.

The remaining clear exception among major economies is China, where disappointing growth has prodded policymakers into easing conditions, even as other major economies tightened. We believe that additional easing is likely, but investors shouldn’t become overly optimistic as a result. China is in the midst of a long-term secular slowdown. So, we view easing there as designed to manage the downside risks around that long-term path rather than an effort to return China’s economy to its previous more rapid growth trajectory. China remains a large, relatively fast- growing economy. Yet its transition from an infrastructure- and trade-driven force to one more focused on domestic consumption means that it will no longer provide the positive impulse to the global economy that many have come to expect.

The combination of slower growth in the developed world and a long-term persistent slowdown in China are both significant headwinds to EM economies. Absent a growth engine from their larger brethren, externally exposed EM economies are struggling to find traction. As a result, EM central banks are likely to remain ahead of DM central banks in cutting interest rates. While this might soften the blow from a more downbeat global environment, the overall EM outlook remains challenging.

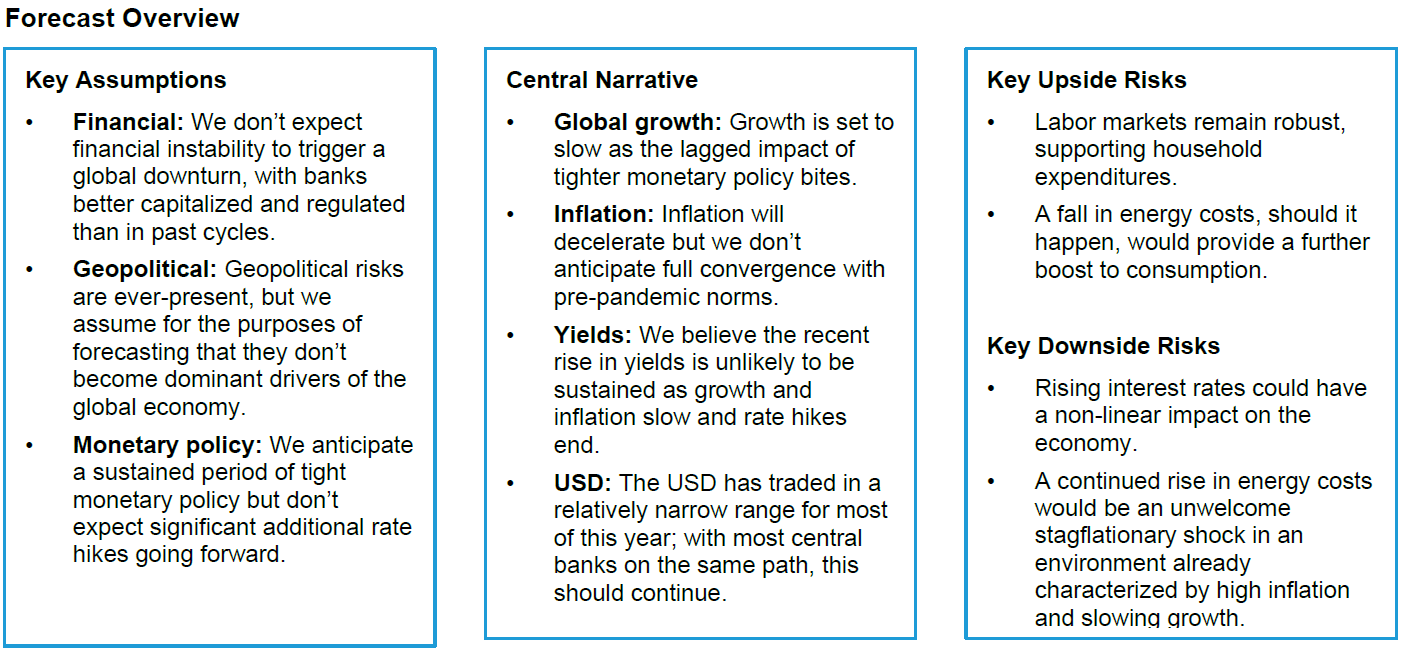

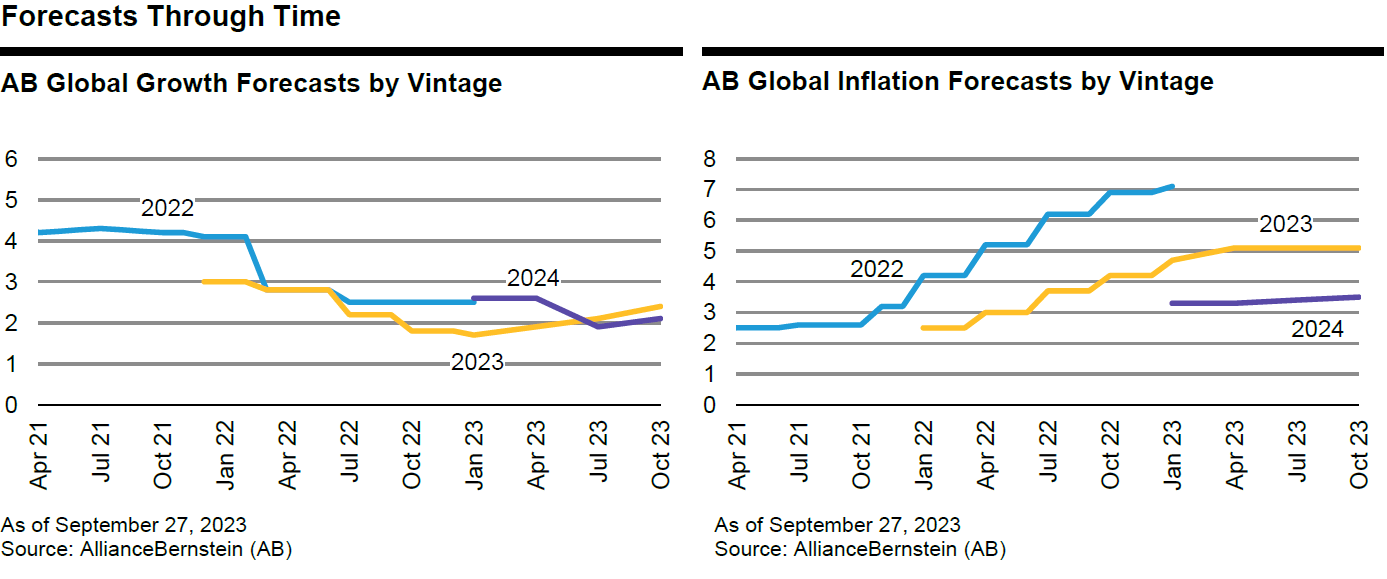

Our base case is for a gradual, manageable slowdown in the global economy accompanied by an equally gradual slide in inflation - albeit one that we expect will stop short of pre-pandemic levels. In most respects, today’s base case is the upside scenario we painted one year ago - things have gone very well indeed to this point. Given that, we’d be remiss not to acknowledge the risks around our expectations. With policy rates high and growth set to slow, the global economy’s vulnerability to shocks has likely increased. While past shocks have been comfortably absorbed, future shocks may prove not so easy to manage. A busy global political calendar, persistent geopolitical tensions and a variety of unknown unknowns ahead could become problematic, injecting a downside skew to the balance of probabilities around our base case. Investors often hear that past performance is no guarantee of future results, and the same is true in economics. Investors should be optimistic that the next few quarters will be reasonably good, but also watchful of events that could change the picture.

The Global Cycle for 4Q:2023

{kind=link}

Global Forecast

{kind=link}

{kind=link}

{kind=link}

US

{kind=link}

- The US economy appears to have accelerated over the summer, supported by robust consumer spending. Recreational and leisure activity in particular is likely to be strong: Taylor Swift’s summer tour is only one example of the willingness of consumers to spend their income and continue to draw down savings.

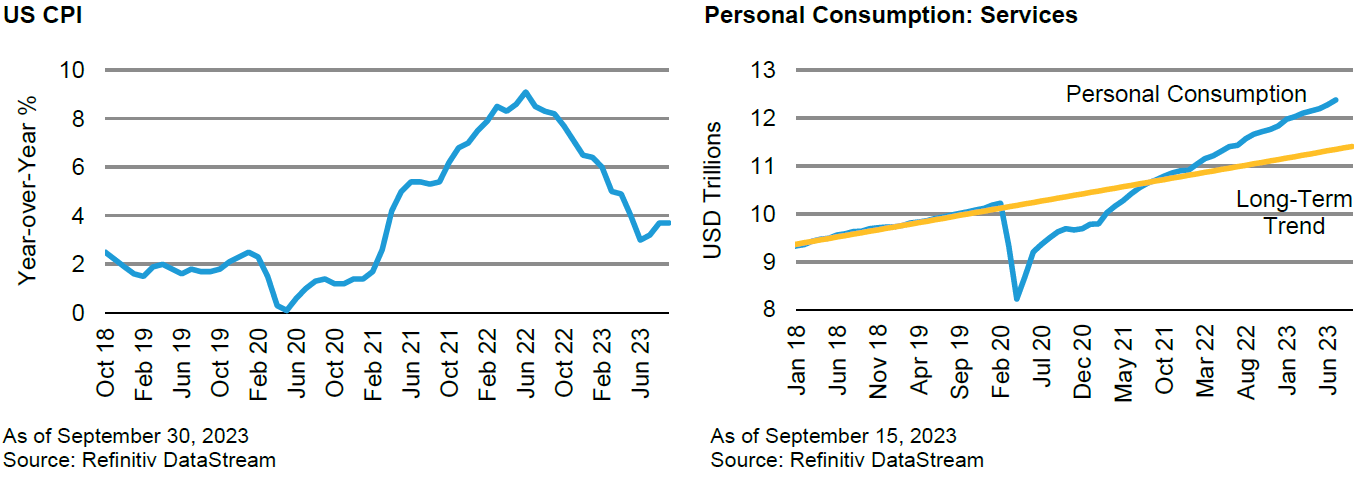

- US consumers also benefited from falling inflation, which had the effect of boosting real incomes. This has likely come to an end, however, at least for the near term: pushing inflation from 9% to just under 4% is a massive boost; future declines in price pressures are necessarily smaller and less impactful.

- The persistent strength of the labor market, combined with savings accumulated during the COVID-19 pandemic, has allowed households to smooth their consumption even during high inflation. There are early signs that the labor market is coming off the boil, if not necessarily cooling down significantly, and much of the excess savings has been spent.

- As we noted last quarter, the Fed’s focus is now on how long rates will remain high rather than how high rates will go. We agree with that focus: the persistence of higher rates is more economically significant than whether there is or isn’t an additional rate hike or two. With the economy on track for a soft landing, we expect rates to stay elevated for several quarters.

Risk Factors

- The recent rise in energy prices, and the concomitant rise in longer-dated interest rates, will slow growth and keep inflation elevated if they persist. A stagflationary shock when inflation is already too high, and growth set to slow would be unwelcome.

- The political cycle is an ever-present risk that will only increase as the US moves deeper into the 2024 election cycle. Our base case does not include a meaningful impact from politics on the near-term outlook. But should an economic shock occur, it is worth asking whether Washington would be able to respond in a timely fashion, given the political climate.

Overview

The US economy once again defied expectations in the third quarter, accelerating when most had expected slower growth. Again, the explanation comes down to the consumer: with the labor market staying strong, households reached deep into their wallets and kept spending. While it’s tempting to attribute this to the frenzy around the Taylor Swift and Beyoncé North American concert tours, that would be an oversimplification. History teaches that when American households have money, they spend it. Savings rates declines to very low levels suggest that households are optimistic about their income and haven’t felt the need to spend less.

While we’re hesitant to bet against the US consumer, we believe that the fundamentals that have supported spending are set to change direction. The labor market is, without question, strong, but forward-looking indicators suggest that it is beginning to come off the boil. Household spending power benefited from the sharp fall in inflation from more than 9% to the current 3.7%. This won’t be repeated: there simply isn’t room for inflation to fall by anything like this magnitude going forward.

Gasoline prices are also rising again, which will keep inflation sticky and take a bite out of household finances. Nothing suggests that a crisis is imminent. Indeed, a soft landing is the most likely scenario, based on the evidence. But a soft landing is still a landing: we believe that it will take a few quarters of below-trend growth to bring inflation back down to the Fed’s target. With more than 5% of interest-rate hikes in the pipeline, we believe this is the most likely outcome in the coming quarters. If inflation can be brought to heel without a recession ensuing, that would be an extraordinary outcome by historical standards. It isn’t guaranteed yet, and the economy is becoming more vulnerable to shocks as the cycle matures, but it’s worth pausing to acknowledge that today’s base case is yesterday’s upside scenario.

{kind=link}

China

{kind=link}

Outlook

- China remains a source of concern for investors as a combination of disappointing growth and worry about private sector defaults, particularly in the property sector, raise the possibility of a more negative outcome.

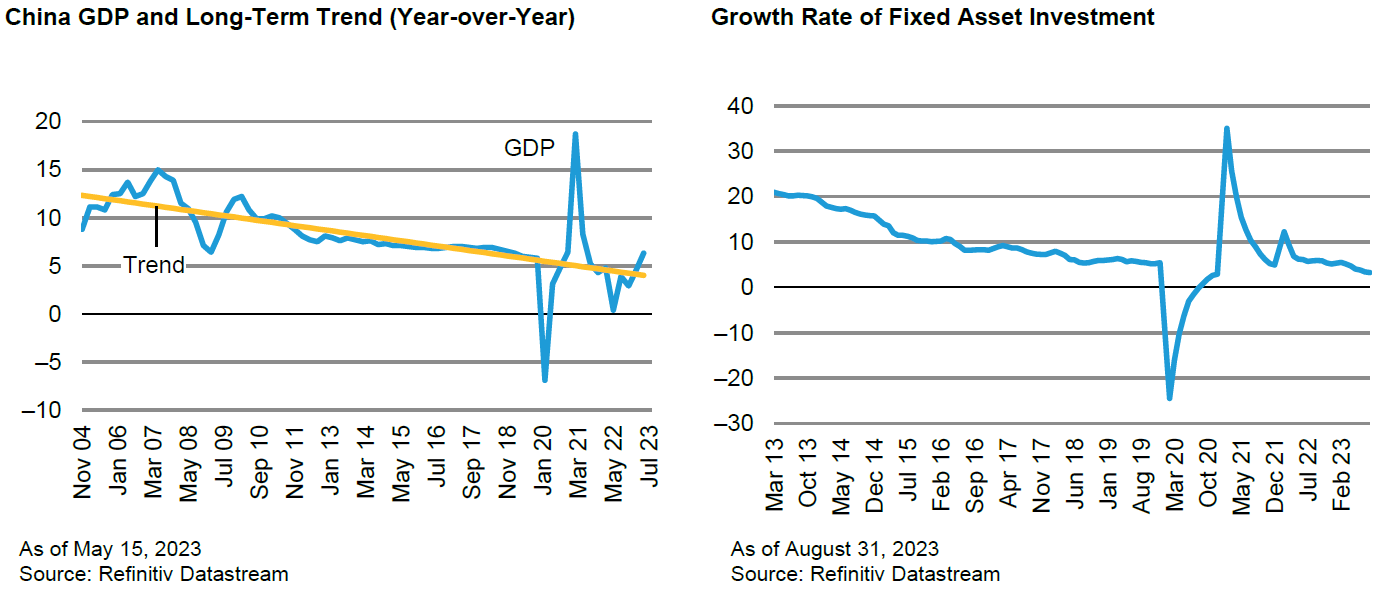

- Policymakers have taken steps to stabilize the situation, and data from late last quarter suggests that those steps have had a positive impact. But we believe that policy measures are designed primarily to limit downside risks to growth rather than an effort to push GDP onto a more rapid trajectory. China is going to slow for several years to come.

- Not only is China slowing, but its economy is in transition away from an infrastructure and heavy industry-driven growth model and toward a more consumer-focused one. This means that the pull China exerts on the global economy is going to diminish over time, even in periods when China’s growth picture looks stronger.

Risk Factors

- China’s financial markets remain opaque, with non-bank lenders in particular a source of potential weakness. Many local investors have put their money with entities that don’t have an explicit government guarantee and that have used property development projects to provide investment returns. With the property sector struggling, many trust vehicles could fall into distress, impacting financial markets and individuals. In an environment where generating domestic demand is already a challenge, defaulting on obligations to investors could be very disruptive.

Overview

We think some of the policy easing measures taken this year have been effective at stabilizing growth. Stabilization is not the same as acceleration, of course, and we don’t expect a meaningful acceleration in coming quarters. That simply isn’t the policy objective. Instead, China remains in the midst of long-term transition from focusing on building infrastructure to domestic consumption. That necessarily means a period of slower growth and a diminished impact on the global economy.

Transitional periods are always uncomfortable and risky, and this one is no different. The primary risk is that many private investment products sold in China are unlikely to be able to fulfill their obligations in a slower-growth environment. The question for policymakers is whether to step in and provide support, which would be economically beneficial but cause moral hazard, or to let some products fail, which would hurt domestic consumption and could lead to social unrest. We expect decisions to be made case by case, but our general expectation is that policymakers will be able to manage through this period without a crisis ensuing. That doesn’t mean that all is well, and growth is inevitably going to continue to slow for years.

{kind=link}

Euro Area

{kind=link}

Overview

The third quarter finally saw signs that inflation in the euro area has begun to wane. It has been a long time coming, to say the least, and the evidence of deceleration has come with economic cost. Growth has slowed noticeably and seems unlikely to bounce back in the near term. With the ECB policy rate at a record high and lenders pulling back, persistently slower growth seems the most likely outcome.

We believe policy rates are at their peak, which is good news, and both interest-rate hikes and the reduction of the ECB’s balance sheet have been accomplished without causing undue stress on the European periphery. Indeed, it is the “core” of Europe that has underperformed in economic terms, with Germany especially struggling. The country’s linkages to a slowing China have combined with the broader economic environment to make the German economy among Europe’s weakest.

The absence of peripheral stress means that policymakers have been able to pursue a traditional tightening cycle. This is welcome news for Europe’s forward outlook as a whole, since peripheral stability across the business cycle is a necessary precondition for effective policy and sustainable economic performance over time.

UK

{kind=link}

Overview

As in the euro area, inflation finally seems to have started its march lower in the UK. We believe there’s more to come: the sharp increase in energy costs last year will drop out of the annual calculation in the coming months, and inflation will fall sharply as a result. As it does, we believe that the BOE will not feel compelled to raise rates further, though that outcome can’t yet be ruled out conclusively.

The cost of the inflation fight is slower growth. As is the case elsewhere, we anticipate a sustained period of below-trend growth as tighter monetary policy works its way through the economy. Because the UK’s inflation spike was higher and the resulting cost-of- living crisis more severe, the UK seems most likely of the major economies to suffer a recession in the coming quarters. Best evidence suggests, however, that it would be a relatively mild one by historical standards.

Japan

{kind=link}

Overview

Japan’s economy continues to progress toward sustainably higher inflation, and policymakers continue to accommodate that process. The BOJ has tweaked yield-curve control and opened the door to rate hikes but doesn’t appear to feel urgency to move more rapidly. Meantime, the yen remains very weak, which should boost growth and contribute to higher inflation over the medium term.

Emerging Markets

{kind=link}

Outlook

- We still expect growth in EM to rise to trend while DM growth is projected to fall further below trend in 2024.

- If the disinflationary trend is disrupted and monetary easing curtailed/delayed, then EM growth could also dip below trend.

Risk Factors

- Higher energy prices pose upside risks to inflation and downside risks to growth.

- The strong dollar and high core yields could continue to limit flows into EM and weigh on the EM growth trajectory.

Overview

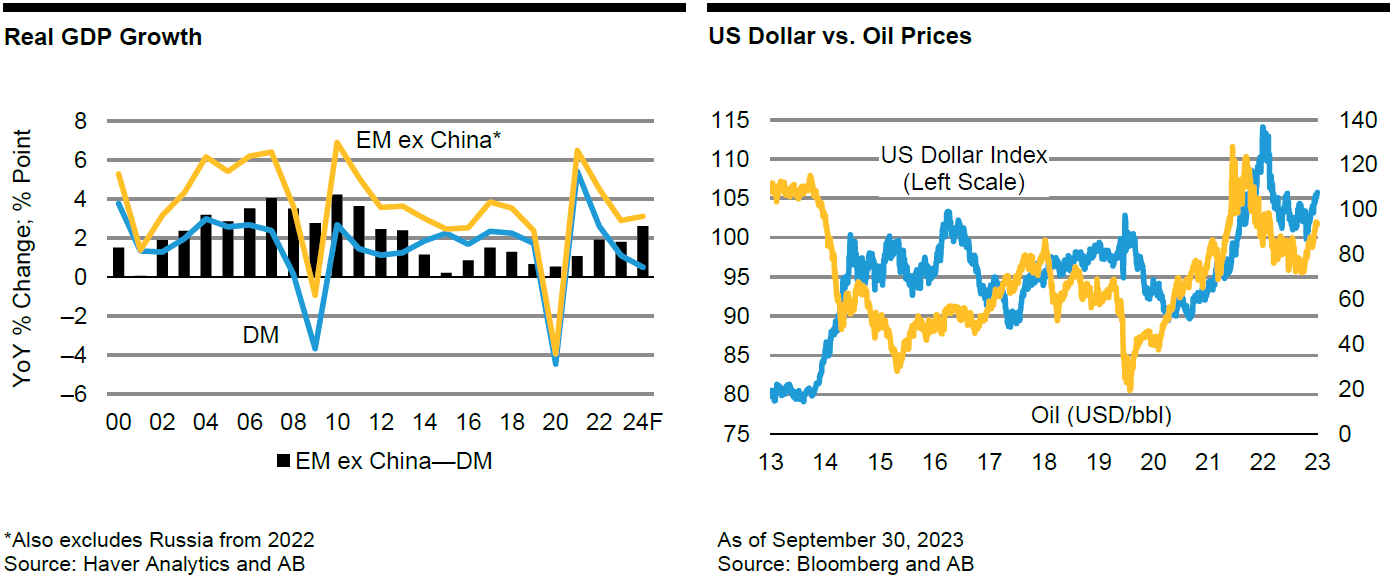

EM economic activity has been relatively resilient year to date. The remarkable resilience of the US economy has certainly counterbalanced the fading growth impulses from China and Europe. But US economic strength supports the US dollar too, and that’s generally negative for EM countries over the medium term. One supportive factor for EM over the past few years has been remittances, which rose to a record US$647 billion in 2022—three times official development assistance according to the IMF. Another positive has been the relative resilience of EM currencies due to EM central banks taking the lead in raising interest rates. Both supportive factors are, however, losing momentum. Persistent US-dollar strength could increasingly weigh on the EM trajectory over the next few quarters.

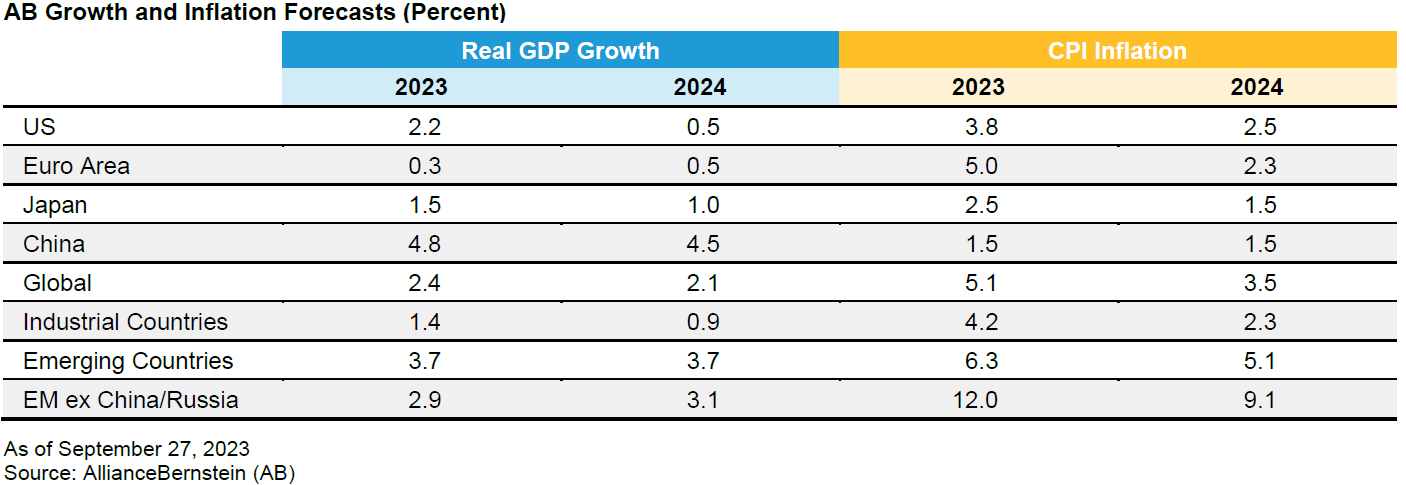

We still expect growth in EM (excluding China and Russia) to rise to trend in 2024, while DM growth is projected to fall further below trend (see first chart below). The projected divergence in EM and DM growth makes for a precarious backdrop for EM asset prices. And the combination of a strong US dollar and high oil prices skews the balance of risks to the downside. The upward shift in oil prices is more supply- than demand-driven, so central banks will generally look through the first-round effect. But elevated inflation levels through this cycle and fragile inflation expectations make it riskier for EM central banks to cut rates in the face of a supply shock, especially if the US dollar is on the front foot (see second chart below).

Higher oil/energy prices pose upside risks to inflation and downside risks to growth. The current divergence between oil prices (higher) and certain soft commodity prices (lower) is not sustainable, in our view. Two other factors to monitor are rising Pacific Ocean water temperatures which could give rise to El Niño, and the impact of the suspension of the Black Sea Grain Initiative. But we think it’s ultimately the oil price trajectory that could disrupt food price and headline disinflation. We still expect disinflation in EM and DM over the next few quarters, but the trend is likely to slow and target-friendly inflation could be delayed further. Slower disinflation and rising risks (US-dollar strength and high oil prices) could keep policy rates higher for longer. EM’s trend-like growth forecast is premised on their ability to lead the interest rate cutting cycle (after building credible rate buffers during the hiking cycle). If the disinflationary trend is disrupted and monetary easing curtailed/delayed, then EM growth could also dip below trend.

The higher-for-longer interest-rate narrative and a strong dollar are negative for capital flows into EM. China has seen significant portfolio outflows for multiple quarters as growth surprised to the downside. But portfolio flows to the rest of EM have been disappointing too. Also under pressure is foreign direct investment in EM excluding China, which slowed meaningfully over the past year or so. The strong dollar and high core yields could continue to limit flows into EM in the near term. Continued global economic divergences (growth and policy rates) are likely to keep EM in a state of flux into year-end.

{kind=link}

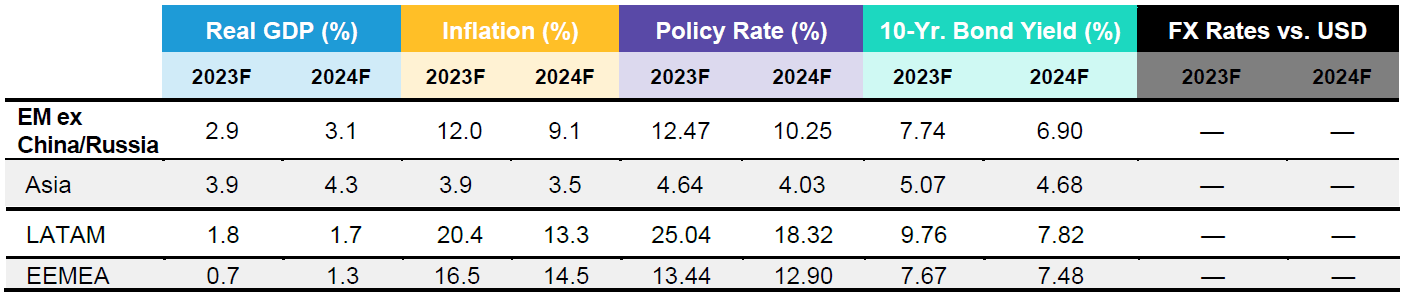

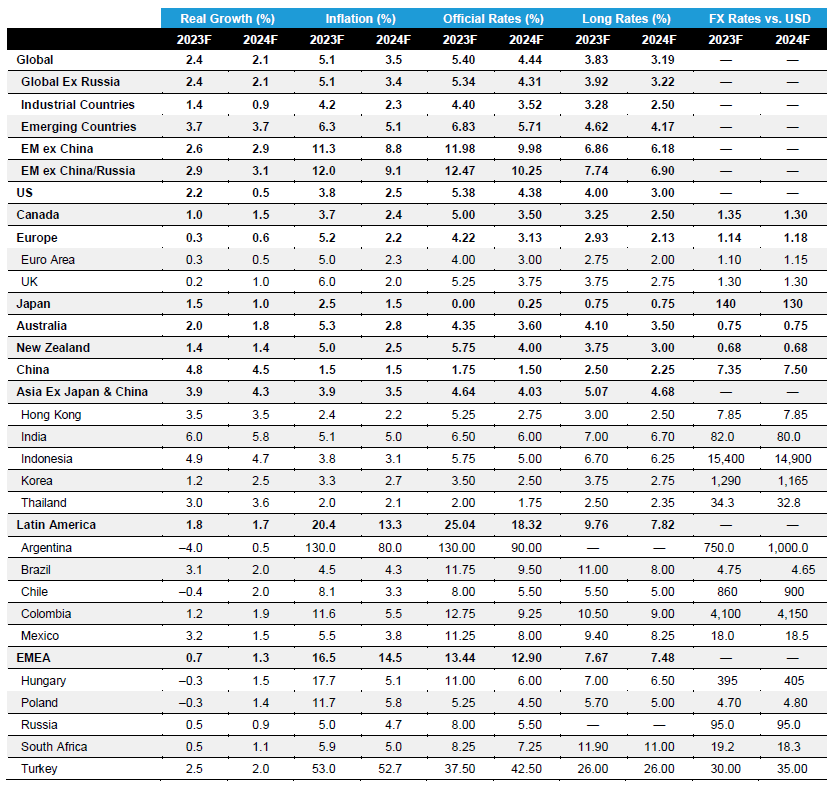

Forecast Table

{kind=link}

Growth and inflation forecasts are calendar-year averages except US GDP, which is forecast as 4Q/4Q. Interest-rate and FX rates are year-end forecasts.

Long rates are 10-year yields unless otherwise indicated.

The long rates aggregate excludes Argentina and Russia; Argentina is not forecast due to distortions in the local financial market; Russia is not forecast because the local market is inaccessible to foreign investors.

Real growth aggregates represent 29 country forecasts, not all of which are shown.

Investment Risks to Consider

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Past performance does not guarantee future results.

Important Information

Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor's personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB

L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorized and regulated in the UK by the Financial Conduct Authority (FCA -Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as "wholesale clients," as defined in the Corporations Act 2001 (Cth of Australia) and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited, a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Important Note for UK and EU Readers : For Professional Client or Investment Professional use only. Not for inspection by distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

www.alliancebernstein.com

© 2023 AllianceBernstein L.P.

UMF-430917-2023-09-29 ICN20231479

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Macro Outlook - Fourth Quarter 2023