GWRS - Global Water Resources: Strong Financial Performance With Expanding Profit Margins But Unfavorable Valuation

2024-01-02 23:52:38 ET

Summary

- Global Water Resources reported solid Q3 results, with a significant increase in revenues and improved profit margins.

- The water services segment outperformed, driven by an increased client base in the Phoenix metropolitan area.

- The company has a consistent dividend payout and is expected to achieve higher revenues and EPS in FY23.

- It is trading at a forward GAAP P/E multiple of 40.25x, which I think doesn't provide a favorable risk-reward profile.

Investment Thesis

Global Water Resources, Inc. ( GWRS ) is a water resource management company headquartered in Phoenix, Arizona. In this thesis, I will analyze its third-quarter results along with its future growth prospects. I will also be analyzing its valuation at the current price level and the upside potential in its stock price. It experienced a significant increase in revenues and an improvement in profit margins. However, its valuation at the current price level doesn't provide a favorable risk-reward profile, and hence, I assign a hold rating for GWRS.

Company Overview

GWRS focuses on providing sustainable water solutions to residential, commercial, and industrial customers. It operates in the water, wastewater, and recycled water sectors, ensuring the efficient and responsible use of water resources. Its business can be segregated into two segments: Water Utility Services and Wastewater and Recycled Water Services. The majority of its operations are located in the city of Phoenix and Tucson.

{kind=link}

Q3 FY2023 Result

GWRS reported solid third-quarter results, beating the market revenue and EPS expectations by 9.26% and 37.5%, respectively. The water services segment proved to be the outperformer, with a significant 29.5% growth in revenues. As per my analysis, the increased client base in the Phoenix metropolitan area primarily drove the revenues. The acquisition of Farmers Water Co. , completed in February 2023, also contributed to the revenues, and the company managed to take over the operations effectively.

It reported total revenues of $14.5 million , up 22.2% compared to $11.9 million in the same quarter last year. The primary revenue drive was the water services segment, with a 29.5% increase in revenues to $7.5 million, up from $5.8 million in the corresponding quarter of the previous year. I believe the water services segment could continue to outperform in the coming quarters, given the increase in the client base and higher demand from the residential sector. Phoenix's housing market has seen some improvement compared to 2022, and the interest rates cut in 2024 could further improve the situation, eventually resulting in higher demand for water services. The wastewater and recycled water services segment saw an increase of 7% in revenues at $6.5 million, compared to $6.07 million in the same quarter last year. I believe the company has managed to improve its water recycling efficiency, and with an increase in the active water connections from the industrial sector, the water recycling revenues will witness significant growth. The net income for the quarter stood at $2.63 million, up a massive 56.5% compared to $1.68 million in Q3 FY22. This brings the diluted EPS for the quarter to $0.11, bringing the net income margin to 18.1%, up from 14.1%. The increased revenues and controlled operational expenses resulted in improved net income margins.

{kind=link}

As of December 28, it declared a monthly dividend of $0.0251 , representing a 1.2% increase from the previous month's dividend payout of $0.0248. I would like to highlight that the company has been consistent with its dividend payout and, in the past ten years, never missed a single month of dividend payout, even during COVID-19. The current dividend brings the forward annual dividend yield to 2.31%.

Now, let us have a look at its balance sheet. As of September 30, 2023, it reported cash and cash equivalent of $5.28 million against long-term debt of $103.2 million. I believe the high debt liability has resulted in increased interest expenses for the company, putting a dent in its profit margin. However, I think the company has managed its debt efficiently, and the amount of debt has seen a slight reduction over the past few quarters. The company's current financial performance has helped it navigate its debt obligation effectively.

Overall, the company managed to outperform on multiple parameters, including revenue growth and improved profit margins. The consistent dividend payout reflects its commitment to returning the profits to the investors. The management has not provided any future guidance, but the market estimates the FY23 revenues in the range of $50.5-$52.5 million, reflecting a 17% increase compared to FY22 revenues of $44.7 million. I believe the company should be able to achieve the higher end of this estimate given the improved Pheonix housing market and consistent growth in active water connections. The FY23 EPS is estimated to be $0.33, compared to FY22 EPS of $0.24. It should not face any challenge in achieving the EPS targets given that in the past nine, it has recorded EPS of $0.28 and is in line to achieve the estimated targets.

Competitive Analysis

{kind=link}

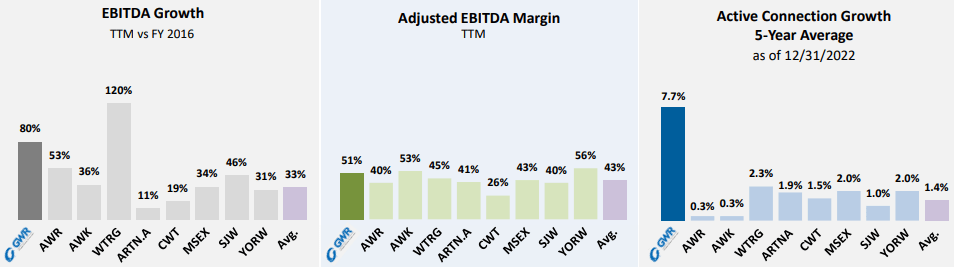

GWRS is currently trading at a share price of $12.96, a decline of 1.44% in the past year. It has a market cap of $316 million. It has managed to outperform most of its competitors with respect to EBITDA and water connections growth, as we can see in the chart above. But when it comes to valuation, I believe it is highly overvalued compared to its peers. It is trading at a forward GAAP P/E multiple of 40.25x, compared to its peer's ARTNA and YORW P/E multiple of 25.43x and 24.3x. GWRS has performed strong financially and is expected to do so in the coming quarters, but the current valuation leaves very narrow room for an upside in the stock price. Investors can wait for a 10-15% correction in the stock price and then think of buying on the dips, but initiating a fresh buying position at the current price level is not advisable.

Conclusion

The company is on the right growth track, experiencing growth in the active water connections, and at the same time, it has managed to improve its profit margins. The consistent dividend payout is a big positive for the investors. FY24 is expected to be favorable for the company, with a recovery in the housing sector and expected interest rate cuts. It is trading at a forward GAAP P/E multiple of 40.25x, which I think doesn't provide a favorable risk-reward profile. Considering all these factors, I assign a Hold rating for GWRS.

For further details see:

Global Water Resources: Strong Financial Performance With Expanding Profit Margins But Unfavorable Valuation