GSAT - Globalstar: Balancing Satellite Capex And Growth

2023-11-09 14:49:50 ET

Summary

- Globalstar, Inc. is a Mobile Satellite Services provider with a global subscriber base of about 773 thousand customers.

- The company has secured an exclusive IP licensing agreement with XCOM Labs to enhance its technological capabilities and expand its market reach.

- Globalstar has entered into a $64M agreement with SpaceX to launch satellites into low Earth orbit in 2025, with Apple reimbursing 95% of the launch costs.

- I think GSAT's valuation appears excessive due to its CAPEX and uncertain EBIT margins despite its promising revenue growth.

- GSAT's potential hinges on maintaining revenue growth and managing operating expenses. Yet this remains unproven, so I rate it a "hold" for now.

Globalstar, Inc. ( GSAT ) is a satellite telecommunications provider offering critical communications solutions. GSAT has recently renewed its leadership with the appointment of Dr. Paul Jacobs. Additionally, GSAT has signed exclusive agreements with XCOM Labs, is collaborating with SpaceX, and Apple is investing in its infrastructure. One of GSAT's most promising aspects is that it's building a satellite fleet that should become invaluable over time as its capacity becomes fully used. However, I rate GSAT a "hold" because of its capital-intensive nature for satellite acquisition, substantial operating expenses, and maintenance capex, which significantly limit GSAT's otherwise promising revenue growth.

Business Overview

Globalstar is a Mobile Satellite Services ((MSS)) provider catering to many industries with a global subscriber base of about 773 thousand customers as of September 2023. GSAT delivers critical communication solutions, particularly in remote or poorly served regions lacking traditional telecommunication infrastructure. Their offerings include voice and data communication services via satellites and ground stations, two-way communication devices like the GSP-1600 and GSP-1700 phones, the SPOT product line for location messaging, and Commercial IoT devices for remote data tracking and telematics. In 2022, they introduced the Realm Enablement Suite , a set of technologies and services for the advanced tracking and management of assets through satellite communication, offering reliable and optimized data processing and transmission capabilities.

Moreover, GSAT also secured an exclusive IP licensing agreement with XCOM Labs in August 2023, gaining access to cutting-edge wireless spectrum technologies to enhance its technological capabilities and expand its market reach. This move will bolster their services for private network customers with critical connectivity needs. Additionally, regarding GSAT's Infrastructure, the company maintains a network of Low Earth Orbit ((LEO)) satellites, predominantly second-generation, offering enhanced lifespan and capacity. They are expanding this fleet, committed to acquiring up to 26 new satellites by 2025, ensuring the continuity of their MSS.

GSAT's Strategic Profile, Alliances, and Leadership Revamp

GSAT has appointed Dr. Paul Jacobs, founder of XCOM Labs and former CEO of Qualcomm, as its CEO. Jacobs' appointment is poised to leverage his vast experience from his tenure at Qualcomm, where he oversaw significant revenue growth and market capitalization increase. Alongside Jacobs, Matt Grob and other XCOM technologists have joined GSAT to propel innovation. A licensing agreement gives GSAT exclusive rights to XCOM's technologies like the XCOMP coordinated multipoint radio system, which benefits complex wireless environments.

Dr. Paul Jacobs is now in charge of GSAT's future. (GSTA's LinkedIn page.)

GSAT aims to integrate XCOM's advanced wireless technologies with its satellite and terrestrial assets, enhancing its commercial offerings in areas like private network services and small devices for satellite connectivity. The deal involves GSAT issuing approximately 60 million shares of common stock to XCOM for the licensing fee and related costs. The collaboration with XCOM is expected to significantly advance GSAT's growth by leveraging both companies' combined expertise and technologies.

GSAT also capitalizes on its worldwide radio frequency spectrum allocation, authorized by the ITU, enabling the cost-effective global deployment of its services. They hold authorization to provide broadband services over 11.5 MHz of their licensed 2.4 GHz MSS spectrum. Their spectrum is integrated into the handset and infrastructure ecosystems, with Band 53 for LTE and n53 for 5G applications. Technologies from Qualcomm and Nokia have already adopted the company's spectrum. Qualcomm's support for Band n53 in its Snapdragon X65 modem-RF would enable wider device compatibility with GSAT's spectrum.

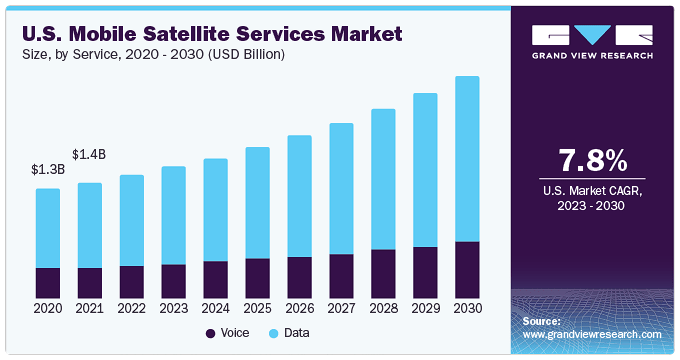

GSAT's sector is expected to grow at a 7.8% CAGR. (Grand View Research)

{kind=link}

I believe GSAT's licensed part of the 2.4 GHz spectrum is a valuable asset because the exclusive right to operate in this band allows it to offer unique services in the market. These services include terrestrial broadband services in the same spectrum used for satellite communications, standardization of devices for terrestrial and satellite connectivity, secure networks in remote locations, and integration into the cellular ecosystem for satellite-augmented LTE and 5G services. These services are more reliable because they are not reliant solely on unlicensed spectrum bands, which could be prone to congestion and interference.

In another positive news , Globalstar has entered into a $64M agreement with SpaceX to launch satellites into low Earth orbit in 2025, replacing their current constellation. Apple, referred to as a "partner" in the filing, reimburses 95% of the launch costs and has already provided $252M to Globalstar for satellite services, particularly for the Emergency SOS feature on iPhone 14 Pro and Pro Max models. This feature allows users without cellular coverage to send messages by connecting to Globalstar's satellites. Apple plans to invest $450M in U.S. infrastructure, mostly benefitting Globalstar.

Valuation Analysis

From a valuation perspective, I think it's worth understanding GSAT as a company with voice and data services, devices, IoT applications, and SPOT messages. These offerings form GSAT's revenues, divided into 1) Service Revenue and 2) Subscriber Equipment Sales. Interestingly, Service Revenues are GSAT's "growth" segment, which has increased 61.1% YoY using the latest quarterly figures .

Source: GSAT's latest 10-Q.

For this, the company has to invest heavily in acquiring satellites. In fact, for the nine months that ended in September 2023, GSAT used $110.2 million in satellite procurement alone. Naturally, this is likely a one-time, nonrecurring type of CAPEX. And it should yield revenues for years to come, as PPE often does because it involves lumpy cash outlays that are recovered over time as the assets are used and depreciated. This complicates the analysis of GSAT at this point because we have no real data yet of how potentially profitable it can be on EBIT terms, nor do we know how often it will have to replace its satellites.

Nevertheless, a simpler and easier-to-understand valuation approach is likely through a multiple. In GSAT's case, we don't know how profitable its EBIT margins can be because it's still growing its revenues and finding how much it can extract from its satellites annually. Still, we do have peer data , and with those figures, the average EBIT margin is approximately 10.1%. This, coupled with analyst's estimates for GSAT's revenues, give us an idea of how profitable GSAT can be and how much revenue it can have after developing its potential. For context, analysts forecast $226.1 million and $246.6 million in revenues for 2023 and 2024, respectively. With this information, I've outlined a path for GSAT's EBIT over the coming years until 2027. Then, using those figures, we can perform a multiples-based valuation using GSAT's sector's EV/EBIT ratio .

Author's elaboration.

However, as you can see, clearly assuming a leveling off of revenues will not be enough to justify GSAT's current valuation of $2.55 billion. In fact, if you look at its multiples, it signals overvalue. Yet, such a huge valuation disparity is often not a mistake. The market sees something in GSAT that's valuable. Often, regular telecom companies are valuable simply due to their strategic assets. Likewise, GSAT's satellite fleet is undoubtedly valuable, regardless of GSAT's capital structure or profitability. So, for the sake of argument, let's assume more aggressive growth figures. After all, GSAT recently increased its revenues by 52.2% YoY , and while analysts currently expect tamer growth into 2024, it could be that GSAT surprises to the upside. So, I'll simply use the current 52.2% YoY growth rate and repeat my valuation approach.

Author's elaboration.

Nevertheless, even with such aggressive growth assumptions, the implied fair value for GSAT is still well below its current market cap. For context, the aggressive assumptions in the model above still imply a fair value of $1.44 billion for GSAT, which, compared to the current market cap of $2.55, implies a 43.7% downside potential. This means the shares would be fairly valued (according to this valuation approach) at $0.77.

Naturally, this would imply a significantly bearish outlook for GSAT at these levels. As previously discussed, I believe the intrinsic strategic value of GSAT's assets could somewhat offset this assessment. Furthermore, it's reasonable to assume GSAT may have considerable unused capacity, which could enable a significant expansion of its subscriber base with notably higher EBIT margins. After all, GSAT is just starting to grow its revenues after years of substantial CAPEX investments. Thus, such potential growth, coupled with the possibly progressive improvements in GSAT's technology and increased market penetration due to the growing popularity of its services, could theoretically result in revenues and EBIT margins that outpace the figures in my previous model.

Conclusion and Closing Thoughts

Overall, GSAT is a mixed bag as an investment. On the one hand, the company is improving its technology, committing substantial CAPEX, and creating vital infrastructure that could become strategically invaluable. After all, GSAT's utility across various applications is evident. Its uses, ranging from IoT to personal devices, are undeniable. Moreover, these applications are consistent revenue generators because they rely on GSAT's satellite network. Also, the recent leadership changes and exciting partnerships like the ones with XCOM and Apple are all promising. But on the other hand, we can't simply ignore GSAT's capital-intensive nature that requires hefty CAPEX for acquiring satellites and their maintenance.

Moreover, I truly believe that the operating costs required for GSAT's specialized and advanced business can't be brushed aside. To illustrate this, consider GSAT's CAPEX to purchase new satellites, totaling roughly $110.2 million YTD in 2023. Then, compare that figure against GSAT's expected revenues in 2023 of approximately $226.1 million. And this figure doesn't even include GSAT's maintenance CAPEX, which historically has been between $30 to $50 million. It also doesn't include the company's operating expenses, which I estimate to range between $200 million and $425 million based on 2022 and 2023 figures. Significant costs and expenses must be exceeded significantly to produce enough profitability to justify GSAT's current valuation. So, I think GSAT's main investment rationale at this point hinges on 1) maintaining its recent explosive revenue growth and 2) the assumption that CAPEX and operating expenses will remain relatively fixed and not scale with revenue. Both assumptions remain to be seen, in my opinion.

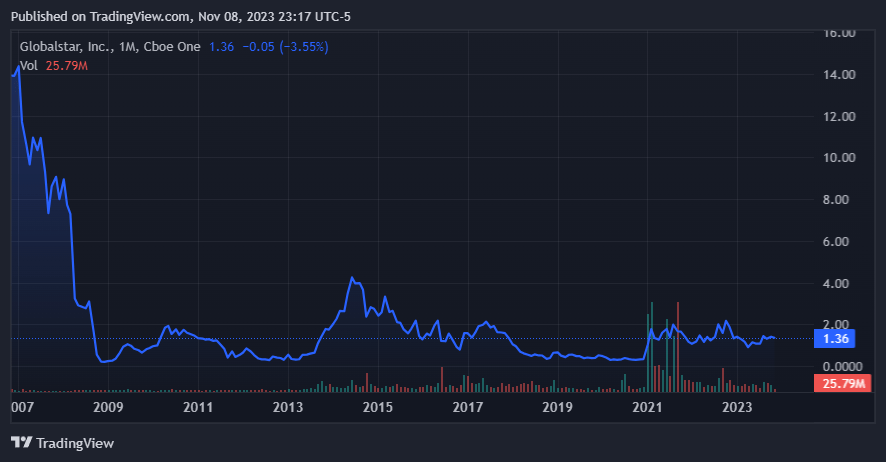

GSAT stock has been disappointing since its inception. (TradingView)

{kind=link}

So, as a whole, I think that, for the time being, a "hold" rating for GSAT seems more reasonable. This balances GSAT's recent revenue growth against its capital-intensive nature and significant OpEx. However, I think a good entry price (if it occurs) would be $0.77, which would still depend on aggressive revenue forecasts but would be easier to justify based on the current data.

For further details see:

Globalstar: Balancing Satellite Capex And Growth