GSAT - Globalstar: Still A Long Way To Go

2023-03-30 15:29:36 ET

Summary

- Globalstar must prove it has the ability to fulfill its open orders in the first quarter of 2023.

- Globalstar plans on spending an additional $250 million in CapEx for the full year 2023, which could put enormous pressure on the bottom line.

- Some important profitability metrics are dismal, underscoring areas Globalstar must significantly improve in to perform well.

Globalstar, Inc. ( GSAT ), which provides mobile satellite services around the world, has been struggling for some time, as supply chain constraints, heaving spending, and big losses have kept the share price of the company down, even as it pushes to regain momentum and grow revenue and improve its bottom line.

Globalstar stock has been volatile over the last couple of years, even since it started its upward run in early January 2021, when it soared from approximately $0.33 per share on January 4, 2021, to almost $3.00 per share on February 8, 2021.

After the big move, it has traded in a range of about $0.90 per share to just under $3.00 per share - being rejected a couple of times when it approached that level, and afterwards plummeting to the above-mentioned $0.90 per share level.

The lack of visibility from supply chain constraints, rising costs, increasing expenditures, and uncertainty concerning the macroeconomic situation, have continued to weigh on the company.

While it appears to have regained momentum on the revenue side of things from the improvement of its supply chain and being able to fulfill more of its open orders, at the same time the company expects to increase CapEx in 2023 by another $250.00 million or so, which will almost certainly result in more losses.

In this article, we'll look at some of its recent numbers, the impact of its supply chain on its performance, key metrics that point to ongoing weakness, and what the future holds for the company in the current market environment.

{kind=link}

Some of the numbers

Globalstar's revenue in the fourth quarter of 2022 was $41.31 million, up 19.8 percent year-over-year, beating by $2.56 million . Revenue for full year 2022 was $149.00 million, compared to revenue of $124.3 million for full year 2021.

The major catalysts behind revenue growth were service revenue and revenue from subscriber equipment sales. Revenue from subscriber equipment sales was up 8 percent year-over-year, while commercial IoT equipment revenue was up 100 percent.

Guidance for full year 2023 revenue is for it to be in a range of $185.00 million to $230.00 million.

As supply constraints continue to ease, the company has been able to fulfill many of its open orders; that should be a catalyst going forward, not only because of the open orders being fulfilled but also because of the ability of the company to fulfill a growing number of new orders. That appears to be confirmed with its SPOT equipment revenue as well, which was down $1.5 million in the fourth quarter of 2022 but is expected to rebound in the first quarter of 2023, based upon the company returning to regular production levels.

Service revenue in the fourth quarter jumped 22 percent year-over-year, primarily from its wholesale capacity services contract. Sequentially, it climbed $7.3 million from the start of its Phase 1 service and work related to the construction of new satellites. Revenue from its legacy services was down 7 percent sequentially.

Revenue from its commercial IoT service was up 14 percent sequentially, partially from the increase in net subscribers and higher ARPU. The company said the number of new gross activations was up over 50 percent in the reporting period.

Adjusted EBITDA in the fourth quarter of 2022 was $18.3 million, up 48 percent from adjusted EBITDA of $12.4 million in the fourth quarter of 2021.

Net loss for full year 2022 was -$(257.00) million, or -$(0.14) per diluted share, compared to a net loss of -$(113.00) million, or -$(0.06) per diluted share for full year 2021.

At the end of calendar 2022, the company held cash and cash equivalents of $32.1 million, compared to cash and cash equivalents of $14.3 million at the end of calendar 2021.

The combination of total debt and outstanding vendor financing was $191.9 million at the end of calendar 2022, compared to $237.9 million at the end of calendar 2021.

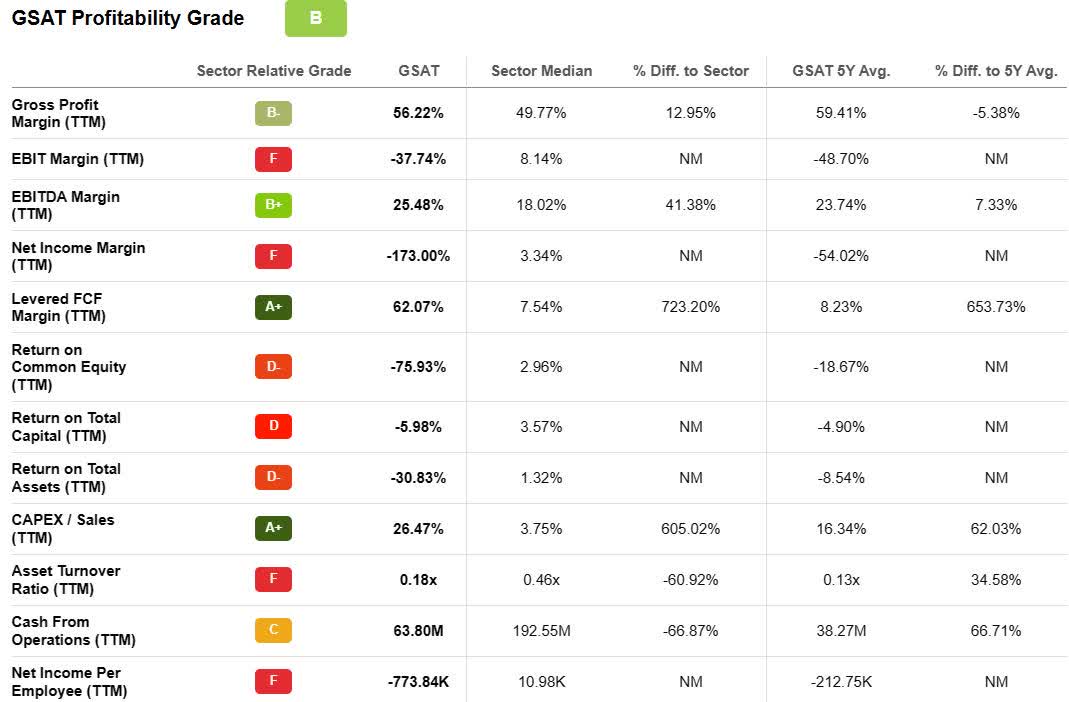

Profitability

Even though the Quant grade for Globalstar, Inc. in relationship to profitability is a "B," I consider it elevated because the key metrics I'm looking at are vastly underperforming the sector median, while other less important metrics are allowing it to look stronger than it appears to be.

For example, gross profit margin is 56.22 percent, up almost 13 percent over the sector median of 49.77 percent. It's similar with EBITDA margin, which comes in at 25.48 percent, up 41.38 percent from the sector median of 18.02 percent.

On the other hand, the most important metric in regard to profitability, in my opinion, is net income margin, and in that metric GSAT is dismal, with net income margin ((TTM)) of -(173.00) percent, compared to the sector median of 3.34 percent.

Other weak but important metrics are return on equity, which was -(75.93) percent, compared to the sector median of 2.96 percent; return on capital, which was -(5.98) percent, compared to the sector median of 3.57 percent; and return on assets, which was -(30.83) percent, compared to the sector median of 1.32 percent.

Cash from operations was $63.80 million, compared to the sector median of $192.55 million, down 66.87 percent.

{kind=link}

Concerning valuation, important metrics, there are also significantly underperforming the sector median. Price/Sales ((TTM)), for example, was 13.58, far above the sector median of 1.28, up by 963.72 percent. Price/Sales ((FWD)) was 9.92, compared to the sector median of 1.21, up 720.42 percent.

Even though GSAT has been able to boost revenue at a modest pace, it has done so at huge losses. That is likely to continue as management stated in its earnings report that it's going to spend approximately $250 million CapEx for full year 2023.

In order to improve its financial structure, the company entered into an agreement with Värde Partners for the sale of $200.00 million in aggregate principal amount of 13 percent Senior Notes due in 2029. The primary purpose will be to pay down the remaining $148.00 million under its facility agreement.

Ongoing supply chain issues

For some time, supply chain constraints have been a significant issue for GSAT, which has had a meaningful impact on subscriber equipment sales. Overall sales from that segment are down from $17.83 million for full year 2021 to $16.44 million in full year 2022.

The significance there is if the company's equipment sales are declining, it means subscription sales will also drop. While that appears to be improving in the fourth quarter of 2022, and management believes much of it will be alleviated in the first quarter of 2023, I think it has had an impact on how investors view the company.

There's that, but also the lack of clarity and visibility on how much supply chain constraints will be relieved going forward. It's one thing to make the assertion, it's another to have the issue resolved.

When there's uncertainty concerning the performance of a company associated with issues outside of its control, it makes investors uneasy, which may be one reason why the share price hasn't found any sustainable momentum over the last couple of years.

If the company proves it can fulfill the bulk of its remaining open orders, it would probably go a long way toward improving how investors view the stock. After all, announcing orders and wins that are perceived to be difficult to fulfill, aren't really wins at all - at least in the near term.

In relationship to fixed costs, this is also an issue, and when considering it also has a higher costs of components and shipping, it puts further downward pressure on the bottom line, as evidenced by the increase in total operating expenses in full year 2022 to $370.00 million, compared to $190.00 million in full year 2021.

The increase in expenses isn't only from supply chain constraints, but it has been putting further pressure on expenses and the bottom line over the last year or so.

Conclusion

There are several things that must happen with Globalstar, Inc. before it has the type of tailwinds needed to drive more interest from investors, including confirmed clarity concerning its supply chain, increasing revenue without devastating its bottom line, significantly improving its net income margin, and turning things around in its return on equity, capital, and assets.

It has shown it can on revenue and EBITDA growth, but it vastly underperforms in the important profitability metrics as measured against the sector median.

With the large increase in CapEx guided for in 2023, it suggests to me that Globalstar, Inc. has to spend an enormous amount of money to grow its top line. That said, it continues to struggle in regard to losses, and based upon management guidance, it looks like it may have to spend a lot more to move the needle to the point it starts to scale enough to take more expenses out of its operations.

The first thing that needs to be confirmed is that its supply chain is, for the most part, fixed, and the company can fulfill its open orders in the near term.

We'll also need to see how expected revenue growth has an impact on the bottom line of the company over the next year or so, as GSAT could come under pressure if it finds itself needing to raise a lot more capital to maintain and continue operations, while improving momentum.

Taken together, I want to see where Globalstar, Inc.'s net loss is at in the quarters ahead after it boosts its spending. I need to see if revenue scale is starting to improve the bottom line.

Even though its share price is almost exactly half of what it was on November 1, 2022, Globalstar, Inc. could easily fall further if its losses continue to mount.

For further details see:

Globalstar: Still A Long Way To Go