TOYOF - GM: Tesla's Dominance Is More Than Priced In

2023-07-06 19:15:00 ET

Summary

- General Motors has experienced a decade of underperformance and now sports a 17% earnings yield.

- CEO Mary Barra's EV and autonomous drive aspirations are hitting speed bumps thanks to competition from Tesla. Cruise appears to be losing the battle.

- Investors have fled to Tesla at a 1.3% earnings yield, but GM is arguably the better investment.

- With a detailed analysis of profit margins, the chip shortage, and recession risk, I estimate long-term returns of 11% per annum.

CEO Mary Barra - Criticisms And Praise

I recently listened to GM's 2023 annual meeting , and one disgruntled shareholder went on a long speech about the downfall of GM. He pointed out that General Motors ( GM ) and Ford ( F ) once had a terrific market share in the United States, but now foreign companies like Hyundai ( HYMTF ), Toyota ( TM ), and Honda ( HMC ) have all but taken that away.

However, GM is not going down without a fight. According to Cox Automotive , it recently took back the "sales crown" from Toyota, seeing its U.S. market share jump from 13.2% in Q4 2021 to 17.2% in Q4 2022.

Here's how GM's U.S. sales have trended over the past five years:

GM's U.S. Sales In Units (Cox Automotive)

Still, at the annual meeting, the disgruntled shareholder went on to call for more management accountability. GM hasn't exactly been a top performer in the S&P 500:

Asked at the annual meeting how she would increase shareholder value, CEO Mary Barra said:

"So when we focus on EV [Electric vehicles], AD [Autonomous drive], and connectivity, we think there's tremendous growth potential for General Motors. That's what we're working hard to execute, and I think that will drive creation of shareholder value."

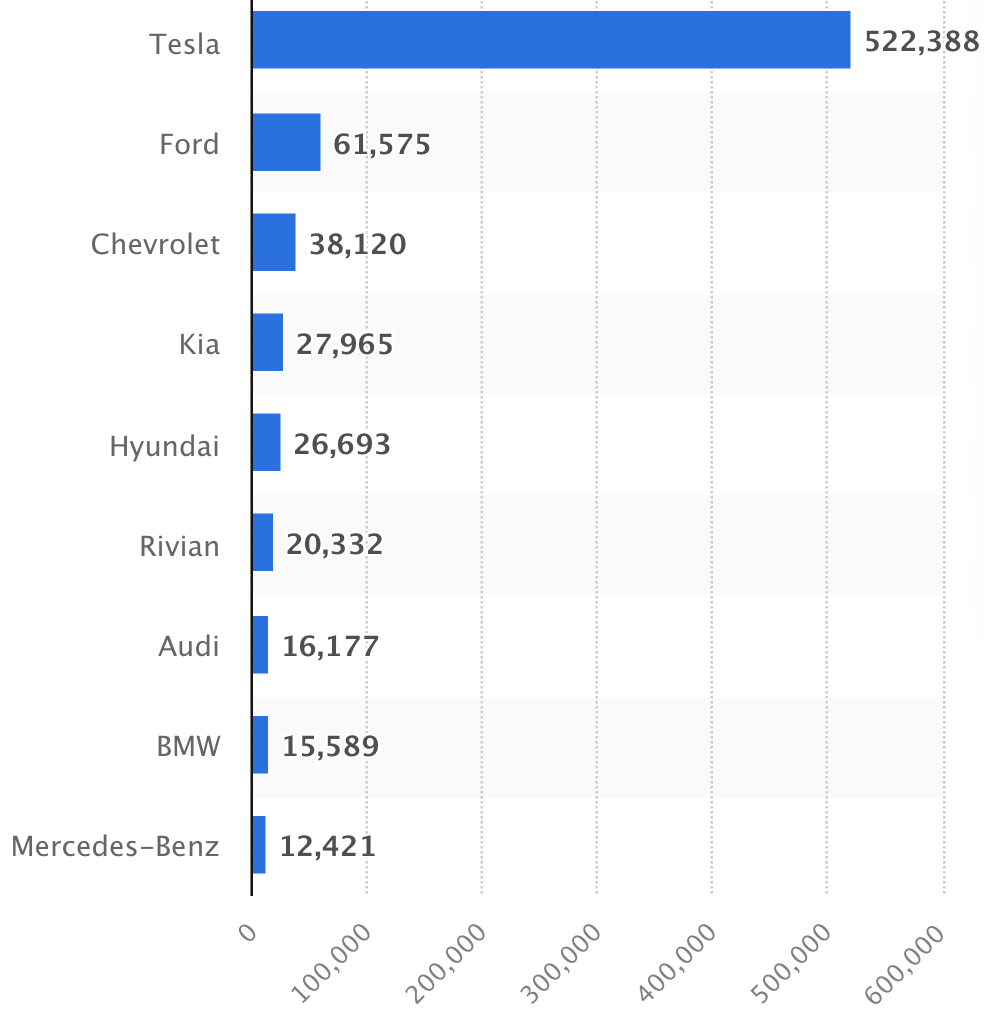

Mary has been CEO of GM since 2014, and this strategy just hasn't worked. The company plans to go all electric by 2035, but GM isn't top-of-mind when it comes to electric vehicles, and in my opinion it may never be. GM's Chevrolet brand came in 3rd in 2022 electric vehicles sold:

{kind=link}

GM's futuristic plans under Mary Barra may have worked, if not for Tesla. Tesla came along and is crushing GM in EV's.

Still, CEO Mary Barra has done some good things since taking over in 2014. For one, she has reduced GM's share count, meaning your per-share ownership has gone up:

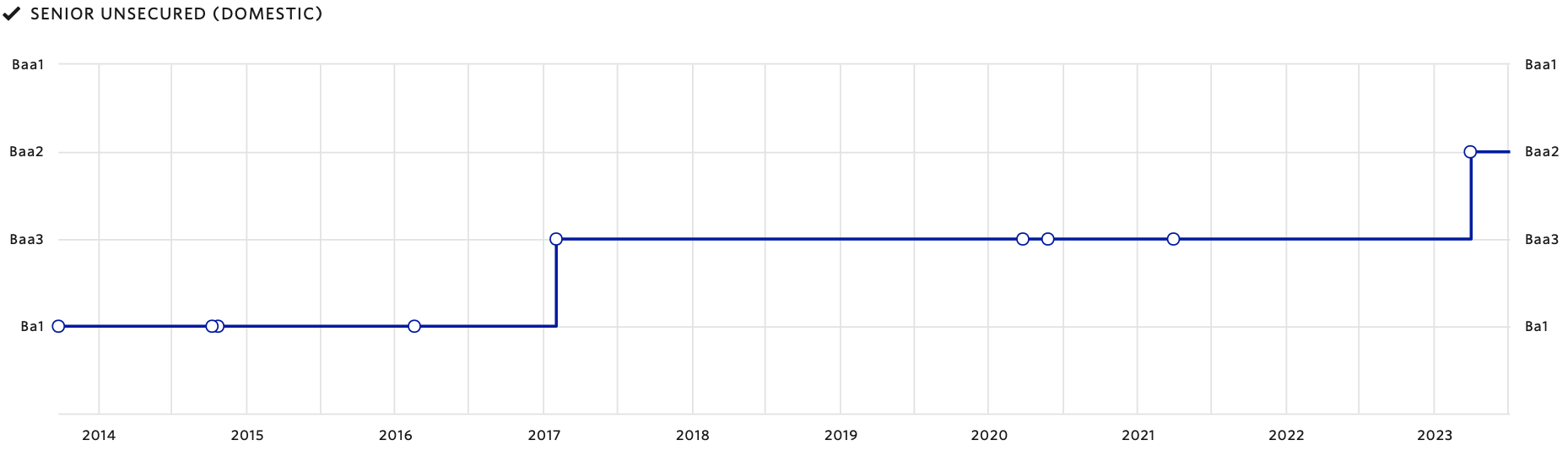

Second, she has improved the company's credit rating from high-end junk bond (Ba1), to low-end investment grade (Baa2):

{kind=link}

Looking at GM's debt to equity, the company is in a stronger position than Ford, but has more leverage than Toyota and Honda:

Earnings By Segment 2022

Here's GM's operating income by segment for 2022 :

| Segment: |

| Billions USD |

| GM North America |

| $12.99 B |

| GM International |

| $1.14 B |

| Corporate |

| ($1.85 B) |

| Cruise |

| ($1.89 B) |

| GM Financial |

| $4.08 B |

| Total |

| $14.47 B |

Cruise - Autonomous Drive

GM has been losing larger and larger sums on its Cruise business. This is the company's autonomous drive arm. Still, this exciting new segment has economic value. GM's Aimee Ridella said :

"GM will make Super Cruise hands-free driver assistance technology available on 22 vehicles by the end of 2023."

This adds value to GM's products, so long as consumers see self-driving as a desirable feature.

The problem is GM is reportedly losing to Tesla ( TSLA ). Tesla's Elon Musk is known for attracting talented engineers to work with him. He recently claimed to have attracted the most integral engineer at Open AI's ChatGPT. According to Topspeed.com , Tesla is winning the autonomous driving race because of its "AI-powered cameras and machine learning." Still, neither Cruise nor Tesla's Autopilot can drive fully unassisted, yet. And even if they could, would you trust them with your life? Personally, I like my cars driven by me, myself, and I. GM and Tesla have only achieved level 2 autonomy. And in an extremely competitive field, the real winner thus far has been Mercedes-Benz ( MBGAF )( MBGYY ), who recently reach level 3 autonomy in the U.S.

An Overweight Bet On North America

In order for GM to outperform global auto companies, you're probably going to need the Canadian and U.S. dollar to remain strong. This is because GM makes 90% of its automotive revenues in North America. Historically , the current level of U.S. dollar strength hasn't lasted long. So I think this lack of international exposure will be a drag on GM.

At the same time, I think we will see a mild to moderate recession in the U.S. and a more severe recession in Canada as higher interest rates restrict consumer spending. The Federal Reserve is pushing the economy in this direction to cool inflation, and the Fed usually gets what it wants.

Profit Margins Are Falling

Meanwhile, profit margins are neither stretched nor depressed, but they are falling:

I concluded at the end of 2022 that luxury automaker's margins would fall as the economy cools, and that has mostly been the case, although EV subsidies are helping:

Margins on GM's luxury vehicles, for example, the Cadillac line-up, could fall further if we enter a recession.

The Chip Shortage Is Likely Over

On the bullish side, sales are rising as the chip shortage comes to an end:

So you have rising sales offsetting declining margins. This is typical supply and demand. You see, in 2021 and 2022, we had tons of demand, but auto companies couldn't fill that demand because they didn't have enough chips (A key component). As the supply of chips increases, auto companies now have more inventory to sell. But, these sales are typically coming in at a lower price.

I don't see the chip shortage coming back anytime soon. In fact, I see potential over-investment by TSMC ( TSM ), Samsung ( SSNLF ), and Intel ( INTC ) all at the same time. Others have corroborated my thesis here, citing the U.S. CHIPS act and slowing demand globally. As the economy cools, I see lagging demand and growing supply (Outside of generative AI). GM has secured its chip supply, partnering with GlobalFoundries.

Long-term Returns

GM has a normalized PE ratio of just 6.7x. In the decade ahead, I project total returns of 11% per annum:

| Normalized EPS |

| $5.85 |

| Assumed Dividend |

| $1.52 |

| Compound Annual Growth Rate |

| 3.5% |

| Year 10 EPS |

| $8.25 |

| Terminal Multiple |

| 9.5x |

| Year 10 Price Target |

| $78.5 |

| Annualized Returns ( Dividends Reinvested ) |

| 11% |

Note: This is a base-case scenario estimate. I have assumed GM will soon return to its pre-2020 dividend amount of $1.52 per share, which would be well covered by normalized earnings. My normalized EPS number was derived from looking at GM's average profit margin and return on assets over the past 10 years, then applying those averages to current sales and assets. The low growth rate can be attributed to my view on the company's competitive position.

To corroborate this bullish thesis, I would say that GM's rarely been this cheap on a price to tangible book basis:

And, GM is selling for less than 10x its average earnings over the past 10 years . Everything in investing is price dependent. Looking at the valuations, I think GM should handily outperform TSLA:

To reach GM's 17% earnings yield, Tesla would have to grow its $3.75 of EPS at 15% per annum for more than 18 years. This is an extreme valuation gap.

Meanwhile, GM's consolidated free cash flows are strong:

{kind=link}

In Conclusion

General Motors has experienced a decade of underperformance. Mary Barra's futuristic plan involving autonomous drive and electric vehicles may have played out better if not for Tesla and Elon Musk. Still, GM's stock is very cheap at 6.7x normalized earnings. Everyone has, rightfully so, picked Tesla to be the winner, but the market has forgotten that everything in investing is price dependent. Legendary investor Sir John Templeton once told Bill Miller:

There are only two types of investors, those who are outlook and trend investors and those who are price and value investors. 90% of people are outlook and trend investors.

Because the outlook and trend investors have fled to overvalued names, GM now trades at a deep value level. Meanwhile, the chip shortage appears to be coming to an end, which has spiked GM's sales (And market share in the United States). Short-term risks include a looming recession in North America. Still, trading a such a large discount to the S&P 500, I have GM outperforming from here. My rating: "Buy."

Until next time, happy investing!

For further details see:

GM: Tesla's Dominance Is More Than Priced In