GLNG - Golar And The FLNG Market: Risky But Cheap And Without Much Competition

2023-04-24 17:16:36 ET

Summary

- Golar focuses on floating liquefaction of natural gas.

- If Golar is successfully recognized for its safe, reliable, and profitable operations, and builds new FLNG infrastructure opportunities, stock demand will likely grow.

- I assumed that FLNG projects could provide a viable economic solution for gas reserves that cannot be converted to LNG due to technical, geographic, and economic constraints.

- It is worth noting that the standardized FLNG design can be reused for new opportunities after a field is produced.

Golar LNG Limited ( GLNG ) is reshaping its business model to focus almost exclusively on the FLNG market. With new projects, new assets recently acquired, and a lot of cash in hand, like other analysts, I am expecting a significant increase in FCF from 2023. It is also worth noting that Golar believes that it is the only player in the market, which will likely offer a significant advantage over new entrants. Even considering risks from lower demand of LNG, declining value of vessels, or lack of sufficient capital, in my view, the stock remains quite undervalued.

Golar

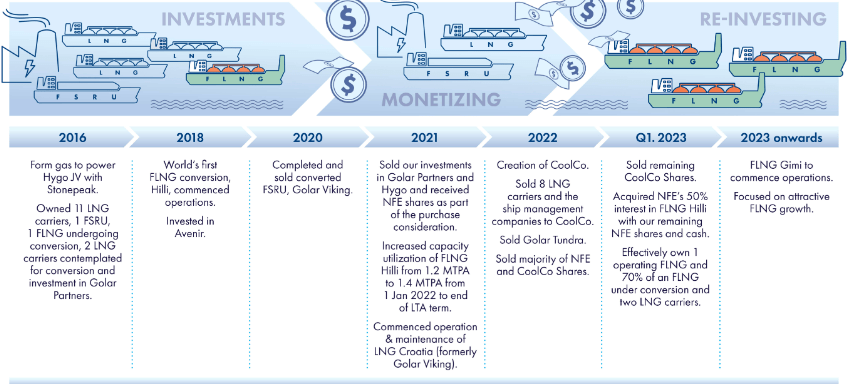

The company is currently going through a transformation period, moving from the shipment of liquefied natural gas and the management of combined cycle gas-fired power plants to a focus on floating liquefaction of natural gas. Notice in the chart below the changing process and the fact that FLNG Gimi is expected to commence operations in 2023.

{kind=link}

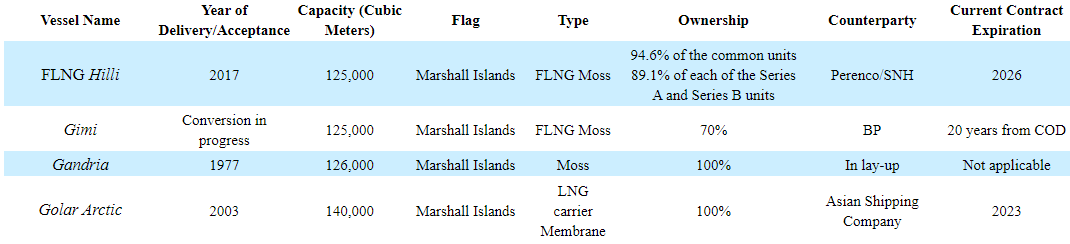

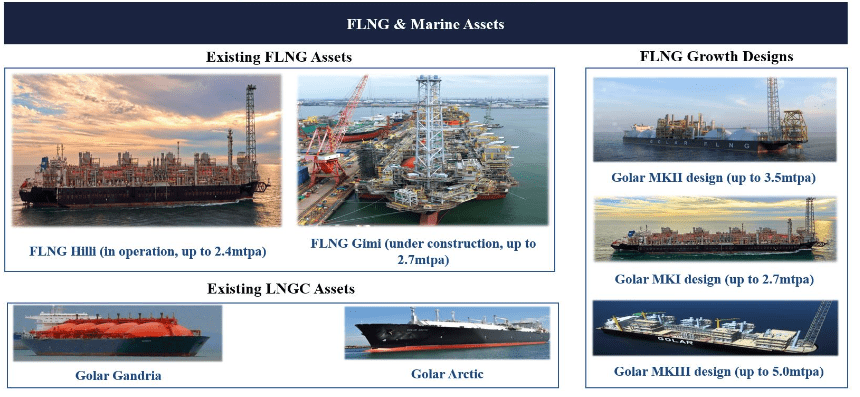

More in particular, among other operations, the company focuses on reconditioning of LNG ships and converting them into FLNG. In addition to the transportation of LNG, Golar currently reports ownership interest in 4 ships, the FLNG Hilli, Gimi, Gandria, and Arctic Golar.

{kind=link}

{kind=link}

Golar focuses on the design, ownership, and operation of marine infrastructures that enable the liquefaction, regasification, storage, and discharge of LNG safely. I believe that Golar is a good read considering that natural gas will likely play a key role in providing cleaner energy in the future. In my view, if Golar is successfully recognized for its safe, reliable, and profitable operations, and builds new FLNG infrastructure opportunities, stock demand will likely grow.

Beneficial Market Expectations, Which Include FCF Growth And Growing EBITDA

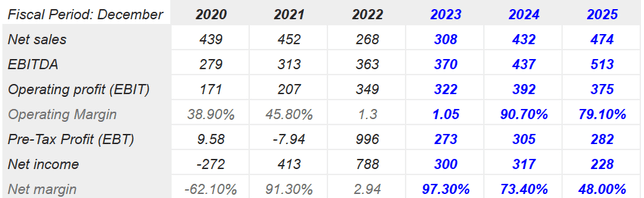

I believe that the expectations of other financial analysts are worth mentioning because they are quite beneficial. 2025 net sales would stand at $474 million with 2025 operating margin of 79% and net margin of 48%. Also, with 2025 FCF of $361 million and 2025 EPS of $2.12, I believe that the financials of Golar LNG will get better in the coming years.

{kind=link}

The financial ratios also indicate some level of undervaluation in my view. 2023 EV/EBITDA would stand at close to 7.12x with an EV/ FCF of 15.7x and a 2023 price to book close to 0.81x.

{kind=link}

Balance Sheet: More Cash In Hand And Less Total Debt Than In 2021

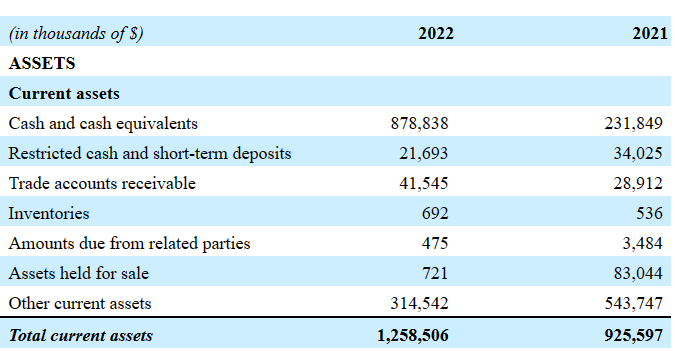

As of December 31, 2022, cash and cash equivalents stood at $878 million, significantly higher than the amount of cash reported in 2021. The sale of interests and shares in 2022 was remarkable.

During 2022, we sold 13.3 million of our NFE Shares for net consideration of $625.6 million, reducing our holdings to 5.3 million NFE Shares as of December 31, 2022. Source: 20-FIn 2022, we sold eight modern tri-fuel diesel electric ("TFDE") LNG carriers and the LNG carriers' commercial and technical management companies to CoolCo for a net consideration of $218.2 million cash and $127.1 million of CoolCo shares and recognized a loss on disposal of $10.1 million. Source: 20-F

Also, with restricted cash and short-term deposits of $21 million, trade accounts receivable $41 million, and other current assets of $314 million, total current assets were equal to $1.258 billion.

{kind=link}

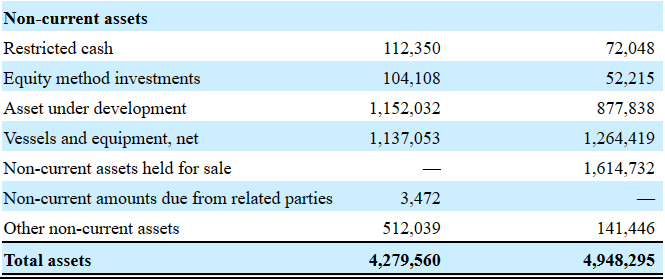

The non-current amount of assets included restricted cash of $112 million, equity method investments worth $104 million, and assets under development of $1.152 billion. Besides, with vessels and equipment of $1.137 billion, total assets were equal to $4.279 billion. The asset/liability ratio stands at more than 2x, so I believe that the balance sheet looks quite solid.

{kind=link}

Liabilities: Golar LNG Recently Reported Less Long Term And Short Term Debt

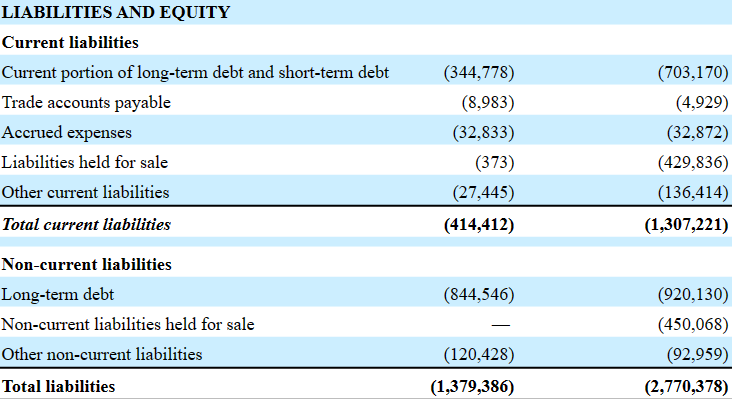

Considering the recent increase in the interest rates, I believe that management was smart in 2022. The company reduced its current amount of debt and long-term debt. Hence, Golar is a bit less exposed to increases in the interest rates.

As of December 31, 2022, current portion of long-term debt and short-term debt stood at $345 million with trade accounts payable of $9 million, accrued expenses close to $33 million, and total current liabilities worth $415 million. Besides, with long-term debt of $845 million and other non-current liabilities worth $121 million, total liabilities were equal to $1380 million.

{kind=link}

Assumptions Made In My DCF Model And Cash Flow Projections

Under my DCF model , I assumed that Golar will successfully offer low-cost and fast delivery solutions to monetize locked gas reserves. Besides, I assumed that FLNG projects could provide a viable economic solution for gas reserves that cannot be converted to LNG due to technical, geographic, and economic constraints. It is worth noting that the standardized FLNG design can be reused for new opportunities after a field is produced. In addition, the design offers a cost-effective alternative to traditional land-based projects.

Besides, I believe that the fact that Golar appears to be the only player offering FLNG as a service to gas resource owners will likely enhance the cash flow statement. I am assuming that the price of some of these services could be elevated because Golar does not seem to have a lot of competition.

Our liquefaction solution places liquefaction technology on board an existing LNG carrier using a low-cost execution model resulting in a vessel conversion to a fully-commissioned FLNG lead time of approximately three to four years. We are currently the only proven company to deliver FLNG as a service to gas resource owners. Source: 20-F

In my view, the current amount of cash in hand and the current reorganization strategy will likely bring the attention of investors. If Golar continues to sell non-core assets as well as acquire assets that offer substantial growing FCF projections, we may see demand for the stock. As a result, if the cost of capital declines, we may see increases in the intrinsic valuation of each share.

Among the equity interests that appear promising, in my view, there is growing exposure to FLNG Hilli's existing contract, which may increase the CFO per share.

The acquisition of NFE's equity interest in the Common Units which closed on March 15, 2023 is expected to increase our share of the cash flow generation from FLNG Hilli's existing contract ending in July 2026. Source: 20-F

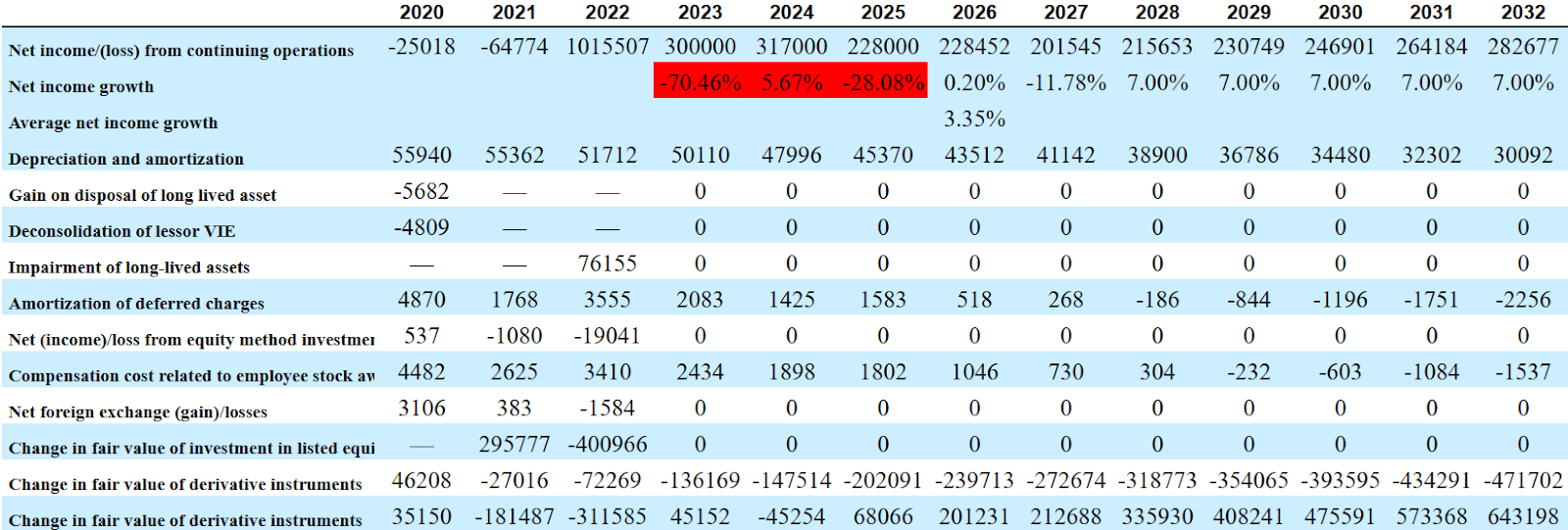

In order to run my DCF model, I used figures close to the net income forecasts for 2023, 2024, and 2025 from other market analysts . Besides, I used an average net income growth close to 3.35%, which is close to the LNG market growth expected from 2022 to 2029. I believe that my figures are significantly more conservative than that of other analysts out there.

{kind=link}

LNG Market to reach USD 593.35 Mn at a growth rate of 5.10% CAGR over the forecast period (2022-2029). Source: LNG Market to reach USD 593.35 Mn .

For the calculation of the free cash flow, I assumed a decrease in capital expenditures, which is included in the expectations of most analysts. It is also worth noting that capital expenditures appear to be decreasing from the year 2015.

Source: S&P

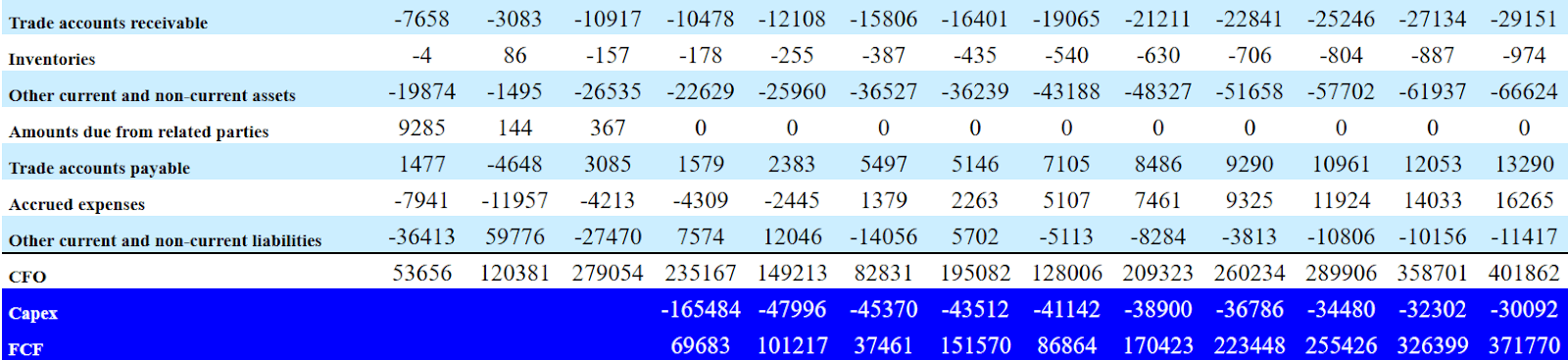

With regards to the expected decrease in capex, it is also worth noting that capital expenditure commitments may lower from 2026 to 2027, which may have a beneficial impact on future free cash flow.

{kind=link}

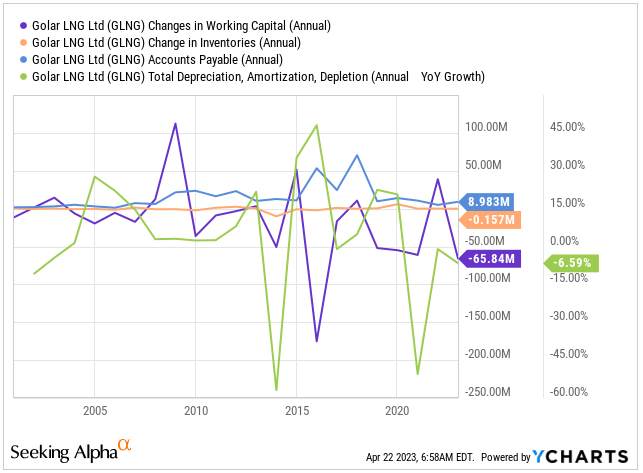

In order to design future cash flow expectations, I had a look at previous changes in working capital, changes in inventories, changes in accounts payable, and D&A. In my view, my numbers are quite conservative since I did not use very different ratios as compared to what Golar reported in the past.

{kind=link}

My numbers included 2032 net income from continuing operations of $282 million, 2032 depreciation and amortization of $30 million, amortization of deferred charges of -$3 million, change in fair value of derivative instruments of $-472 million, and change in fair value of derivative instruments close to $643 million.

{kind=link}

Besides, with 2032 trade accounts receivable close to -$30 million, changes in inventories of around -$1 million, other current and noncurrent assets close to -$67 million, and trade accounts payable of $13 million, I obtained 2032 CFO close to $401 million. Besides, with capital expenditures of -$31 million, free cash flow would stand at $371 million.

{kind=link}

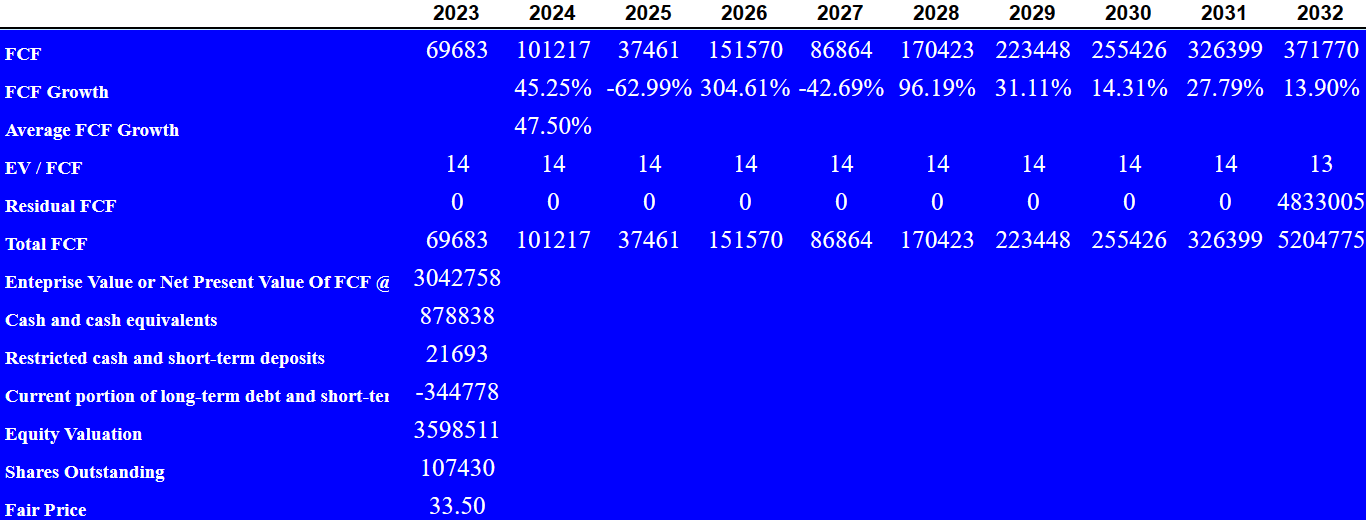

Considering a conservative EV/FCF of 13x, I obtained a residual FCF of $4.833 billion, which, with a WACC of 9%, implied an enterprise value of $3.042 billion. If we also include cash and cash equivalents of $878 million, restricted cash and short-term deposits of $21 million, and current portion of long-term debt and short-term debt close to -$345 million, the equity valuation would stand at $3.598 billion. Finally, the fair price would stand at close to $33 per share.

{kind=link}

Risks

The company is subject to various risks including the inability to obtain new financing, exposure to volatility in interest rates, operating agreements, and financial restrictions in financing agreements.

Lack of adequate financing or lack of interest from investors could lead to increasing cost of capital, which could diminish the fair value of the stock. The company may decide that some future projects may not be profitable, and may invest less, which I believe the market may not appreciate.

Risks related to business operations include non-compliance by contractual counterparties, increased labor costs, unavailability of skilled workers, or cyberattacks. Besides, I believe that fluctuations in vessel values could be quite detrimental for Golar. Too many vessels in the market or any other complication may lower the price, which may bring the book value of Golar down. As a result, I believe that some investors may dump their shares.

Finally, I believe that a decrease in the LNG demand or changes in laws and regulations with respect to the industry could deteriorate future FCF expectations. If Golar has to invest more capex to make the same amount of free cash flow, and has to respect new regulations, I believe that demand for the stock would lower.

My Takeaway

Golar LNG is currently under a reorganization period, which includes the sale of a significant number of LNG carriers and other equity interests related to investment in FLNG operations. Considering the number of players in this market, low-cost operations, and fast-delivery solutions, in my view, Golar could become quite an appealing stock in the coming years. With new cash flow coming from the FLNG Gimi in 2023 and a significant amount of cash in hand, I believe that we could receive beneficial news in the coming years in terms of new profitable investments and cash flow enhancements. Overall, the company appears to be well positioned to capitalize on the FLNG market. I believe that risks associated with its business model and the possible entry of competitors in the market are factors that must be considered by investors, but the stock, in my view, remains undervalued.

For further details see:

Golar And The FLNG Market: Risky, But Cheap, And Without Much Competition