AUY - Gold And Silver Development Optionality Plays (Part 2 Small Caps)

Summary

- A list of gold and silver developers with large resources.

- Estimated valuations for each company on the list.

- Company descriptions from the GSD (GoldStockData) database.

- Optionality plays are one way to identify a good risk-reward opportunity.

- If gold and silver prices rise, then companies that have large resources in the ground become more valuable.

Introduction

An optionality play is a company that has a large amount of gold/silver in the ground that has never been developed into a mine. Ideally, you want to find large deposits that are highly undervalued compared to a company's FD (fully diluted) market cap.

To avoid confusion, my list uses AUEQ (gold equivalent). I am using the current spot price and the number of AUEQ ounces a company has in the ground (Note that I have made AUEQ estimates for some companies, and I could be wrong). Then I compare that value to their FD market cap.

I am also estimating the in-situ value. In-situ is another term for how much AUEQ they have in the ground. For in-situ, I am using 10% of the deposit's AUEQ value. Plus, I am using $100 AUEQ per oz for a second valuation.

There are many factors that skew the valuations of companies, so this is only meant to be a starting point for you to do your own DD. For instance, my AUEQ estimates can be off and will change in the future. The location of the projects and the quality of the management teams impact the value. And there are many other factors that come into play to value a company. One huge one is the ability to finance a project. If a company can't finance the capex, then its valuation can languish.

I've always liked to find good optionality plays, especially for companies that could find more gold/silver through additional exploration. If you can buy AUEQ ounces in the ground for low valuations, then there is a good chance those ounces could be worth more in the future if gold/silver prices rise. Plus, as a company de-risks a project using a PEA, PFS, DFS, and permitting, the value of a company tends to rise.

While I like finding undervalued optionality plays, the risk level is quite high. In fact, you have to treat these as speculation bets and expect to lose money. In fact, I am underwater on quite a few of the stocks on this list. They might do well in the long term if gold/silver prices rise, but I might end up losing money on most of my optionality plays. That said, the potential for big returns is real. If gold/silver prices take off, there are not that many undeveloped projects with large resources. Demand for them should be significant.

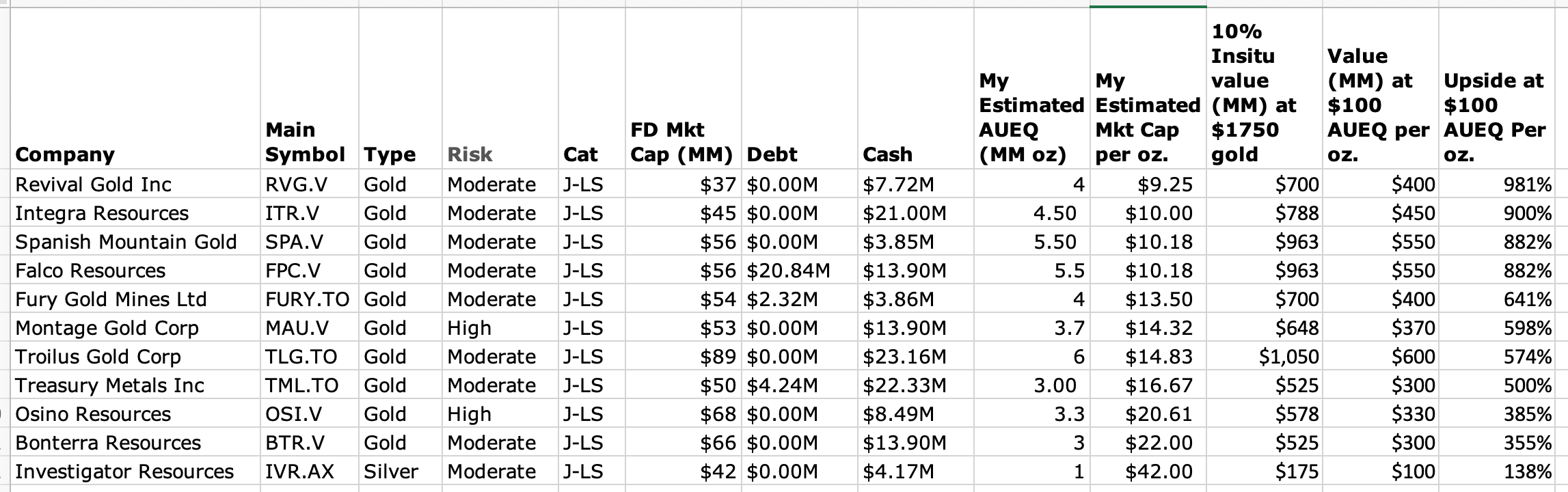

Development Optionality Plays (Small Caps)

(Sorted by Upside at $100 AUEQ Per oz.) (Click on the image for better detail).

{kind=link}

This list includes development companies that trade in North America and Australia. The Main Symbol is the exchange where they are based. V is the Canadian Venture in Toronto. AX is Australia. TO is Toronto. CN is the smaller exchange in Vancouver. Those without a suffix trade in New York.

The Risk column is somewhat of a misnomer. There are no moderate risk mining stocks. Consider High to mean very high and Moderate to be somewhat high.

The Cat column is for the category. J-LS stands for Late Stage Development. JS-NP stands for near-term producer. These are companies that are building their first mine. A near-term producer is within one year of production.

FD Mkt Cap ((MM)) stands for fully diluted market cap in the millions of dollars.

My Estimated AUEQ (MM oz) is my estimated gold equivalent in millions of ounces.

My Estimated Mkt Cap per oz is a calculation of the current FD market cap divided by the AUEQ ounces.

10% in-situ value ((MM)) at $1750 gold is a calculated value of the number of AUEQ ounces multiplied by $1750. This column is 10% of that total.

Value ((MM)) at $100 AUEQ per oz is a calculation using the number of AUEQ ounces and multiplying that by $100.

Upside at 10% in-situ is a calculation that compares the FD market cap to the 10% in-situ value.

Upside at $100 AUEQ Per oz is a calculation that compares the FD market cap to the value in the $100 AUEQ per oz column.

Okay, let me list each stock on the list in the same order as the list above. I will include the company description from the GSD database. Some of these descriptions are not recent, so keep that in mind. This list is only a starting point for you to do your own DD (Due Diligence).

Revival Gold

{kind=link}

Revival Gold ( RVLGF ) is developing an open pit project in Idaho. Their Arnett - Beartrack project has 3 million oz (1 gpt). They are targeting restarting the mine in 2025, with a construction decision in 2023. They recently completed a PEA with a capex of $100 million to produce 72,000 oz annually. A PFS is due in Q4 2022, along with an updated resource.

About 800,000 oz (phase 1) of their 3 million oz have low recovery rate average of 60% (it probably will improve). The remaining ozs have a high recovery rate at 94%. Cash costs are around $800 to $850 per oz. The economics aren't great, with an after-tax IRR at 25% at $1550 gold. By 2024, I would expect gold above $1500, so the economics should be fine.

It is a large property (12,000 acres) with exploration potential. Recently, that had a drill hole of 45 meters at 2.3 gpt. So, this mine should increase in size.

Management owns 11% and is motivated to build these two projects. I think they will become a 72,000 oz producer with all-in costs around $1350 per oz. That could make them a $500 million company at higher gold prices if they reach 1.5 million oz of reserves and gold prices take off. For this reason, it's not a bad speculation stock.

The red flags are the timeline until production (2025), dilution to finance development and the capex, and low recovery rates for the first 800,000 oz. Also, they will need to pay Yamana Gold ( AUY ) about $20 million in 2024 ($6 per resource oz). I expect Yamana to accept shares instead of cash. On a positive note, I think they have a good management team with a good plan, and they have enough insiders to avoid a takeover.

They think this will grow to 4 million oz and 200,000 oz of production. They seem ripe to be taken out by a major. That's my concern. Projects this big and this cheap nearly always get taken out.

Their plan is to be a producer in 2025:

We currently have about 850,000 ounces of the 3 million ounces of resource in the first phase heap leach restart plan. The assumed recovery from this material is currently 60% as discussed below.

The balance of about 2.15 million ounces is mill material with an assumed 94% recovery (see Section 13.2.4.7 of the Beartrack-Arnett TR available here ).

We are guiding to the completion of a PFS and a restart decision on the first phase heap leach by the end of 2022. At that point, we will determine whether to proceed with the first phase heap leach (with its relatively short re-permitting and construction timelines and low capex) or pursue a more ambitious (albeit longer timeline) leach + mill scenario.

In the case, where we simply go with the restart of heap leach operations, we would submit NEPA documentation and could be in a position to commence construction in 2024. Construction is expected to take about a year. This scenario does not preclude a potential mill phase down the road.

5/16/2022: Updated resource to 4 million oz.

9/5/2022: PFS delayed until H2 2023. Ouch. Construction is not likely until 2024.

Integra Resources

{kind=link}

Integra Resources ( ITRG ) is advancing the DeLamar project in Idaho. It is a 4 million oz resource (including silver), although it is low grade (.7 gpt). The good news is that it is economic, with about a 40% after-tax IRR at $1300 gold. The capex is $160 million to produce 120,000 oz annually (gold equivalent including silver). I would expect that total to rise a bit, perhaps to 200,000 oz. Cash costs will be around $800 per oz for gold equivalent. The mine won't get built until around 2026.

They are cashed up and are working on permitting and the PFS. The bad news is that insiders only own about 20% and can't prevent a takeover. They are even giving guidance that they are a takeover target. My expectation is that a mid-tier producer will take them out after it is permitted and it is de-risked (2023 to 2025). It's a past producing mine, so permitting should not be a problem. The PFS is due in 2022. I would expect permitting to require 2-3 more years. They are giving guidance for permitting to be completed in 2024. That means first pour in 2026. Ouch. That is a long wait.

If it had higher insiders, then I would like it a lot better. But, as a speculation stock, the downside appears to be limited. It could easily double in value as it gets closer to production. They are drilling 4 areas (DeLamar, Florida Mountain, War Eagle, Blacksheep) and could easily add more gold to their resources. I'm surprised it hasn't been taken out yet. This looks like a 5 million oz resource, which means potentially 300,000 oz of production. That's a $2 billion valuation at $2500 gold, when they could be taken out today for $220 million.

This is an excellent project in a good location. The problem is they will likely sell before they get to first pour, which is about 4 years away. So, investing and expecting a 5-bagger is a stretch. The more likely outcome is a 2-3 bagger.

Spanish Mountain Gold

{kind=link}

Spanish Mountain Gold ( SPAZF ) has a large open-pit gold project in Canada (British Columbia). In 2021, they released a pre-feasibility, which increased the capex to $460 million, decreased cash costs to $550 (for the first 10 years), and decreased their after-tax IRR to around 15% at $1,300 gold. This project looks attractive at $1,700 or higher gold prices.

A feasibility study should be completed in 2022. Permitting will require 2-3 additional years after the feasibility is completed. So that means no production until 2026 or 2027. It has a high capex for only 150,000 oz. of production, which makes it more difficult to finance. However, at $1,700 gold, the payback can be faster, making financing possible. They have an FD market cap of only $50 million, with future reserves valued at $12.50 per oz. As long as gold prices remain strong, the only risk to shareholders is if they sell the project for a small premium (losing our upside opportunity).

A takeover is a possibility because shareholders are unlikely to turn down a good offer (they never seem to). I think that a potential takeover is part of the reason the stock is so cheap. Investors are not interested in a small return for a high-risk stock. This mine will be built in two or three phases, ramping up to full production. They have 4.7 million oz. of M&I resources, plus significant exploration potential. The main pit is still open in all directions, and the nearby Phoenix zone has been drilled and appears to have a 3 km strike. Phase one only targets 2 million oz.

This is at least a 5 million oz. mine and quite possibly larger. That means they will likely be ramping up to 250,000 oz of annual production. The grade will drop, and cash costs will rise as they expand production, but the leverage is huge at higher gold prices.

Management owns 20% of the shares, and I think they have other insiders. Otherwise, someone would have bought the mine already at this cheap price. Usually, highly undervalued projects like this get taken out by larger companies. Especially, once they get de-risked.

One red flag is more dilution for funding the feasibility study and permitting, plus financing the large capex. Dilution should reduce returns significantly. I have my doubts this is still a 10 bagger. The key is how long it will take to permit the project. Once it is permitted, it will rocket higher, as long as gold prices are above $1800.

Falco Resources

{kind=link}

Falco Resources ( FPRGF ) has a large gold project in Quebec on 175,000 acres. The Horne mine is a 5 million oz deposit at 1.4 gpt, with significant amounts of copper (260 million lbs) and zinc (1.2 billion lbs) for offsets. Revenue is projected at about 70% gold, 18% zinc, and 12% copper. Cash costs are projected to be under $500 per oz because of offsets. Cash costs are dependent on zinc and copper.

The project will also produce 1.5 million oz of silver annually. They sold their silver for $180 million to Osisko Royalty. They will have to produce the silver at a loss, which will reduce their all-in costs. They will get paid 20% of the silver spot price at a maximum of $6 per oz. When you do the math of how much Osisko will make off this loan if silver prices exceed $50, it becomes a very ugly deal. 25 million oz x $50 is more than $1 billion. What will be the silver price from 2025 to 2040?

The capex is larger than I would like at $850 million. That will be difficult to finance. They have $180 million from the silver stream loan, but the rest won't be easy to obtain. The after-tax IRR is only 15% at $1300 gold because of the high capex. They plan to produce 220,000 oz of gold annually for 15 years. That's not really enough for the capex.

Production at Horne stopped in 1976, but it still has significant infrastructure and should be easy to permit. They expect to complete permitting in 2022 and begin construction in 2023. The CEO is a proven mine builder and operator. What I like about this stock is their potential to find another mine on their 175,000 acres in a gold district that has produced 19 million oz in 14 mines. It's usually the second mine where you make your big returns.

There are a few red flags. First, they are a takeover target. I would expect a major to buy them out before first pour. Second, financing the capex needed to build the mine won't be easy to obtain with the low IRR. Banks might demand hedging and a gold stream. Third, potential share dilution to finance the mine. Fourth, their FD market cap valuation is only $85 million. What don't investors like? Management appears to be capable, although the silver streaming deal is noxious. Perhaps investors don't like the long wait until first pour or the high capex.

It's likely they will get taken out before first pour. These highly undervalued projects are nearly always taken out. However, they have enough insiders to prevent that, although Osisko Development currently owns about 25% of the company fully diluted. Perhaps they have eyes on the project?

Fury Gold

{kind=link}

Fury Gold Mines ( FURY ) was created in October 2020 from the merger between Auryn Resources and Eastmain Resources. The combination creates the potential to develop three projects that have over 3.3 million oz (7 gpt), plus exploration opportunities (likely to grow to at least 5 million oz). They are calling themselves an exploration company, but I don't believe them. It reminds me of First Mining Gold, which acquired several advanced projects. Eventually, they picked one to develop because the market would not give them any value.

The red flag is that none of their projects is advanced, and all three need to be permitted. This will take about 4-5 years to become a producer. That is a long wait and will require a lot of share dilution. But, in the long term, the upside is significant. In fact, all three of their projects are worth their current market cap. So, you are basically getting two projects for free.

I expect them to find at least 5 million oz. With an FD market cap of $79 million, their gold in the ground is valued at $16 per oz. That makes them an excelled leverage play, even if they continue as an exploration company. They plan to drill aggressively in 2021 and probably will select which project to develop. Until then, we will not have guidance for a timeline to production. All three projects are in good locations in Canada, although Committee Bay is in cold Nunavut.

Committee Bay has 1.2 million oz (7 gpt), Homestake Ridge in British Columbia has 1 million oz (7 gpt), and Eau Claire in Ontario has 1.2 million oz (7 gpt). I would expect them to build Eau Claire first, but that is just a guess. Eau Claire has a PEA to produce 80,000 oz annually with a $140 million capex. In 2020, they released a PEA for Homestake Ridge. It has an $88 million capex to produce 45,000 oz per year. The IRR isn't great, at around 20% at $1300 gold, but I expect it to get built. The cash costs are low at around $500 to $600 per oz. If they can extend the mine life, then the IRR looks much better.

Committee Bay is in Nunavut, so I would expect that project to come last. If they build all three projects, production should be around 200,000 to 250,000 oz. But that would take at least 8 years, and perhaps longer. It's probably better to value it as a potential 150,000 oz producer within 6 years. This could also be viewed as an exploration/optionality play, because all three projects should grow in size.

They are in a difficult position because their strategy is not clarified. They want to be valued as an exploration company with 3.3 million ozs of high-grade gold in the ground and growing. However, the market won't give them that valuation. They think if they grow their resources to 5 million that their market cap will jump to $1 billion, but it won't. They will come to realize that they need to show a path to production. For this reason, investors aren't excited about this stock. My guess is that they will eventually sell one of their three projects and use the money to develop the other two.

12/6/2021: Sold their Homestake property to Dolly Varden for $50 million CAD, including $5 million in cash and the remainder in Dolly Varden shares.

Montage Gold

{kind=link}

Montage Gold ( MAUTF ) is advancing a large open-pit project ((KONE)) in West Africa (Cote d'Ivoire). The project is on 350,000 acres and is already a 4 million oz deposit. It has various grades (.9 gpt to .5 gpt), so they will mine the high-grade portion first, with higher production for the first 3 years.

They released a PEA this year to produce an average of 200,000 oz a year, with cash costs at $850 per oz. The Capex is high at $490 million. That might not be easy to finance and is probably the reason it has a low FD market cap of $57 million.

They are cashed up with about $14 million and plan to complete a feasibility study in Q1 2022 and permitting in Q2 2022. They could be ready to begin construction next year, which is amazing considering this is a relatively new company and new discovery.

They have a solid management team that came from Red Back Mining. They know how to build and operate mines. Everything looks pretty solid. They want to build this mine as fast as they can, with first pour around 2023. They also have two other either exploration properties: Korokaha (250,000 acres) and Bobosso (175,000 acres).

There is a lot to like about this company. I really don't see any red flags other than the high capex. Insiders own 45%, including 31% by Orca Gold. It's not likely they will sell before first pour. A 200,000 oz producer is worth at least $1 billion with a large economic resource.

Troilus Gold

{kind=link}

Troilus Gold ( CHXMF ) is developing a large open pit mine (Troilus) in Quebec. The deposit is around 7 million oz (.7 gpt). However, about half of the resources are low-grade underground and might not be economic. The open pit is around 3.5 million oz. It relies on copper and silver offsets for its economics. The low grade is the reason for its low valuation, and the timeline until production (2025).

They released a PEA in 2020. The capex is $333 million to produce 250,000 annually for 10+ years (open pit). All-in costs per oz (breakeven) will be about $1,300 per oz. The after-tax IRR is low at about 15% at $1,300 gold. They probably will need $1,600 gold to finance the capex. A pre-feasibility study will be out in 2022, and a feasibility study is also scheduled for 2022. EIS permitting in Quebec takes 12 to 36 months. My guess is that it will be completed by 2024. Hopefully, sometime in 2023, they will be ready to make a construction decision.

The mine is still growing in size and is a large property (250,000 acres). They have been drilling aggressively, and that will continue for several years. I expect production to increase over time. The only red flags are the need for high gold prices to build and operate the mine, the wait for first pour, share dilution, and being a takeout target. With an FD market cap of $172 million, it is cheap versus its upside potential.

Treasury Metals

{kind=link}

Treasury Metals ( TSRMF ) is advancing a gold project (Goliath) in Ontario, Canada. It is both an open pit and an underground project. It has two main deposits (Goliath and Goldlund). Their combined resources are around 3 million oz, and they are likely to find more. I am only valuing them as a 100,000 oz producer, which is conservative. Production will begin at around 88,000 oz in 2025.

The capex is $233 million, with $700 cash costs. I would expect the cash costs to increase by first pour, and the capex is likely to also increase. They are hoping to complete the Goliath deposit permits in 2023, with construction to begin shortly after, with production in 2025.

They expect to complete the Goldlund permits in 2024 and production about a year after. So, after the Goliath deposit gets into production, they have a nice pipeline, along with exploration potential.

Goliath is a large property (12,000 acres) with exploration potential, and the deposit is open at depth. I would expect them to extend the mine life to at least 15 years. The CEO is confident they will find at least 2 million oz at Goliath and thinks the property could contain 3 or 4 million oz. The management team is optimistic that they will increase production from exploration success.

Goldlund is also large (70,000 acres) with exploration potential. Between the two, I'm sure they are targeting at least 3 million oz of reserves and probably much more. This creates growth opportunity for Treasury in the long term. The problem is first pour is not until 2025. That is a long wait.

Osino Resources

{kind=link}

Osino Resources ( OSIIF ) is developing its first mine (Twin Hills) in Namibia (South Africa). It is on a large property with many drill targets. The deposit is 3 million oz (1 gpt) and growing in size.

They completed a PEA in 2021. The capex is $200M, which is a bit high, but they will likely increase production. Initial production is 125,000 oz for the first 3 years. It is forecast to drop in year 4, but I don't think it will.

They plan to complete a feasibility study in 2022 and are cashed up with about $8 million. They plan to complete permitting in 2022 and then likely begin construction in either 2022 or 2023. I would expect at least one more financing before funding the capex. Share dilution is low and unlikely to get high before first pour.

It's a good management team that used to run Auryx Gold before it was acquired by B2Gold ( BTG ). They have 10 properties in Namibia (over 1 million acres) and are likely to find a few more mines. The upside looks good. Insiders own about 32% of the company, including around 15% by Ross Beaty. While Namibia is in South Africa, the population is only 2.5 million, and they have a democracy. They do not have any political issues at the moment and appear to be mining-friendly, with 25% of their GDP via mining.

Bonterra Resources

{kind=link}

Bonterra Resources ( BONXF ) is trying to become a mid-tier producer in Canada. They acquired Metanor Resources in 2018 and now have aggressive plans to become a mid-tier producer in 2024. They have 3 properties with a combined 3 million oz and a mill in Quebec. They have 4 drills turning and expect to expand their resources at Barry (1.4 million oz at 5 gpt) and Gladiator (1.4 million oz at 8 gpt).

Then they plan to develop 3 deposits (and expand the mill from 800 tpd to 2400 tpd): Barry, Moroy, and Gladiator to produce 190,000 oz annually. That seems very aggressive. I'm only valuing them as a 125,000 oz producer because their guidance is not clear. But they have 4 drills turning, and a new resource estimate will be out in 2022-23. It might increase to 3.5 million oz. They will need to spend additional capex to expand production. I'm not sure what production will begin in 2024.

If they can produce 150,000 oz annually at $800 per oz cash costs (that is below their PEA forecast) in Quebec, this is going to be a very valuable company. Of course, they will need to expand their resources to get investors' attention. Plus, we have to wait until 2024 for production.

I like their potential and think it is highly undervalued. I'm not sure why investors don't like it, but I do. I like the location, exploration potential, management, and project. I don't see any red flags, other than the long wait to first pour. If gold goes higher, this should be a 5 bagger. They have strong insiders, including Eric Sprott and Kirkland Lake.

9/7/2022: Made the decision to place the underground infrastructure at the Bachelor-Moroy deposit (only 150,000 oz) on long-term care, and maintenance will reduce the annual maintenance costs by at least $3 million/year.

Investigator Resources

{kind=link}

Investigator Resources is advancing a silver discovery (Paris) in Australia. It is already a 40 million oz resource (130 gpt) at surface. They have a PFS to mine 4 million oz a year for 6 years. This is likely to be extended. The capex is $100 million with an AISC of $12.50 and a high IRR. It is likely to get financed.

They are working on a DFS and permitting, both of which are due in 2023. It is a 1-year build, with a production forecast for 2024. Investors are ignoring it, giving it a valuation of only $45 million. That gives it 10-bagger potential.

Next to the Paris deposit is Helen, which is a gold/copper exploration target. They think Helen could be a second mine. They also have a 30% for a potential large iron/copper project (Maslins) that OZ Minerals ( OZMLF ) is exploring.

It has a high share dilution at 1.3 billion shares. So, expect a reverse share split. They have about $4 million in cash and no debt. Expect more dilution to complete the DFS and permitting, but it shouldn't be much. I'm not sure why investors don't like it. At $30 silver, I think they will.

Note: This stock does not trade in North America.

For further details see:

Gold And Silver Development Optionality Plays (Part 2 Small Caps)