AGNCM - Goldilocks Is Back

2023-06-04 09:00:00 ET

Summary

- U.S. equity markets rebounded this week as a critical slate of employment data provided evidence of a 'soft' economic landing, showing stronger-than-expected job growth combined with a cooldown in wage pressures.

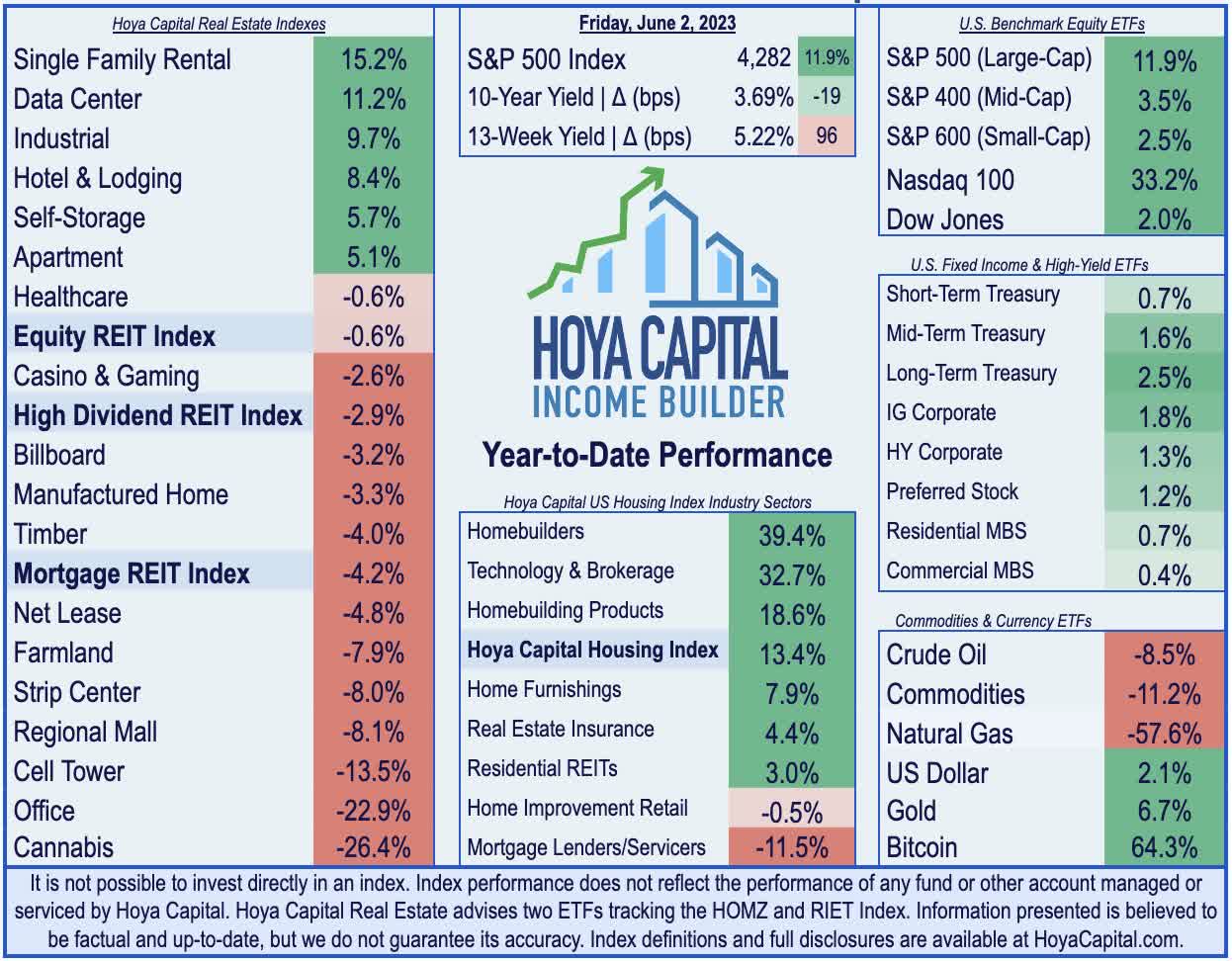

- Closing the week at its highs for the year, the S&P 500 advanced 1.9% this week, lifting the major benchmark to the cusp of 'bull market' territory with gains of nearly 20%.

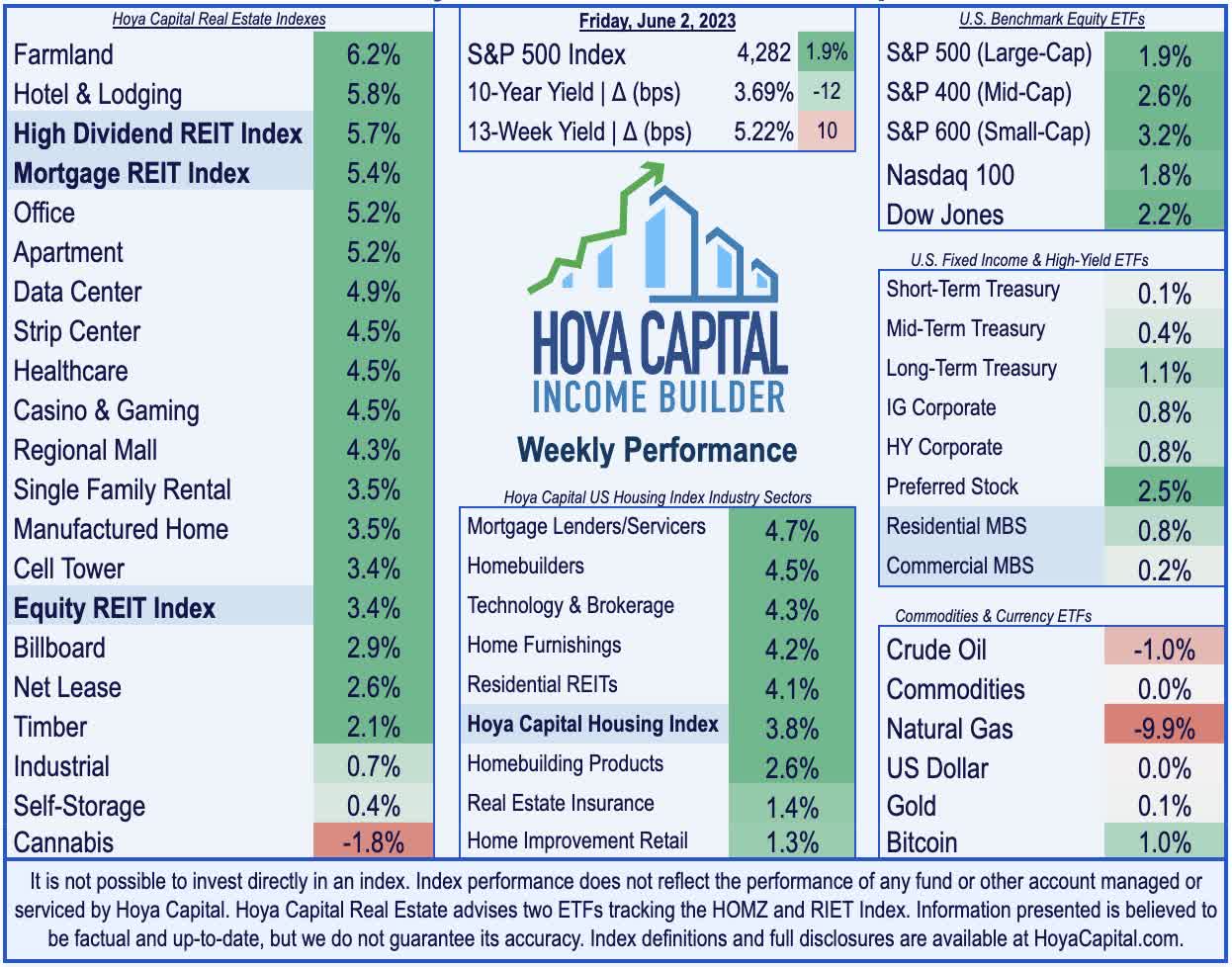

- Real estate equities were among the leaders this week, lifted by a moderation in benchmark interest rates and an encouraging slate of business updates ahead of the annual REITweek industry conference.

- Apartment REITs rallied more than 5% after a series of operating updates showed sustained buoyancy in rental rates. Equity Residential raised its full-year outlook, while AvalonBay reported a continued acceleration in rent growth since bottoming in December.

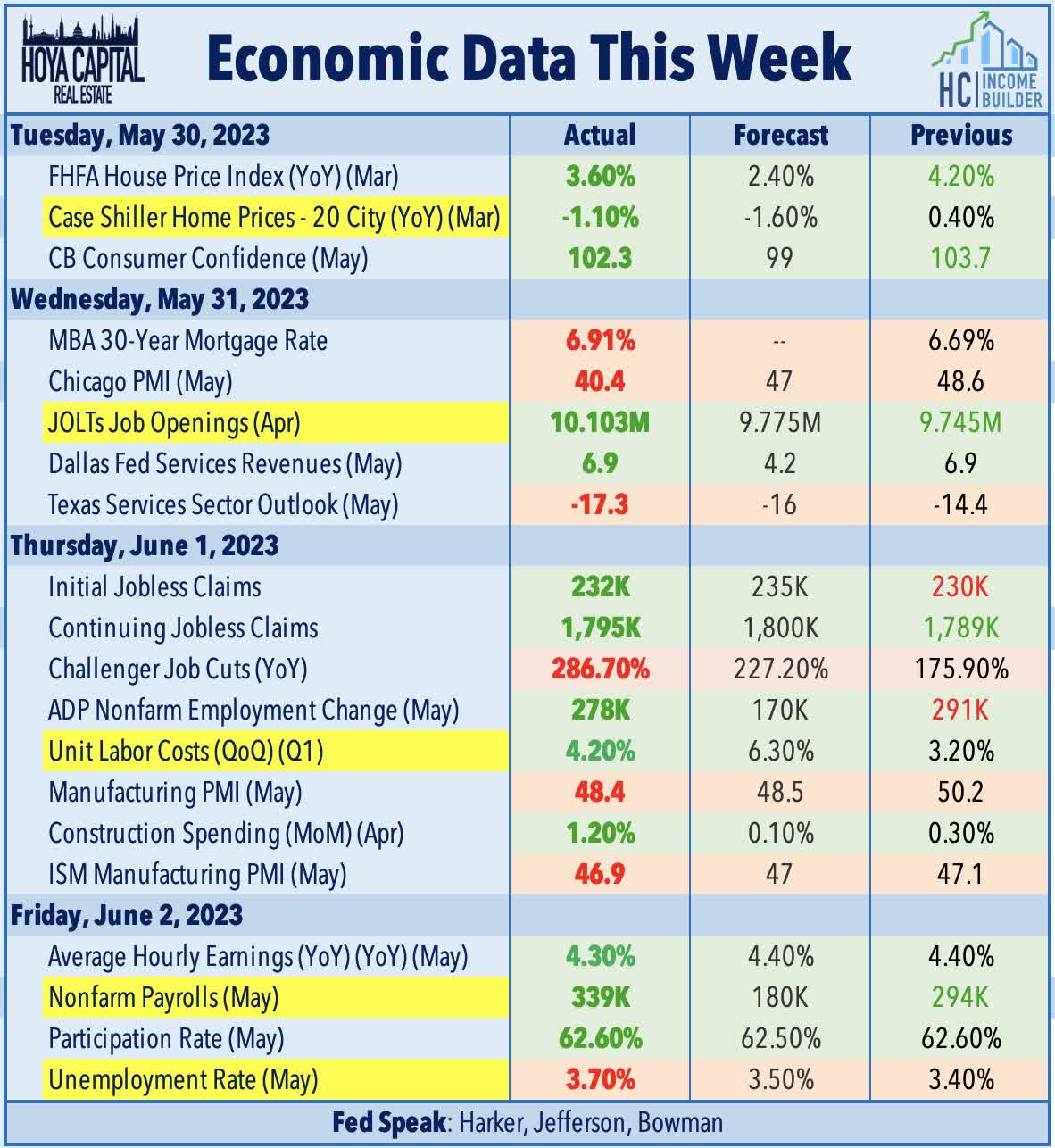

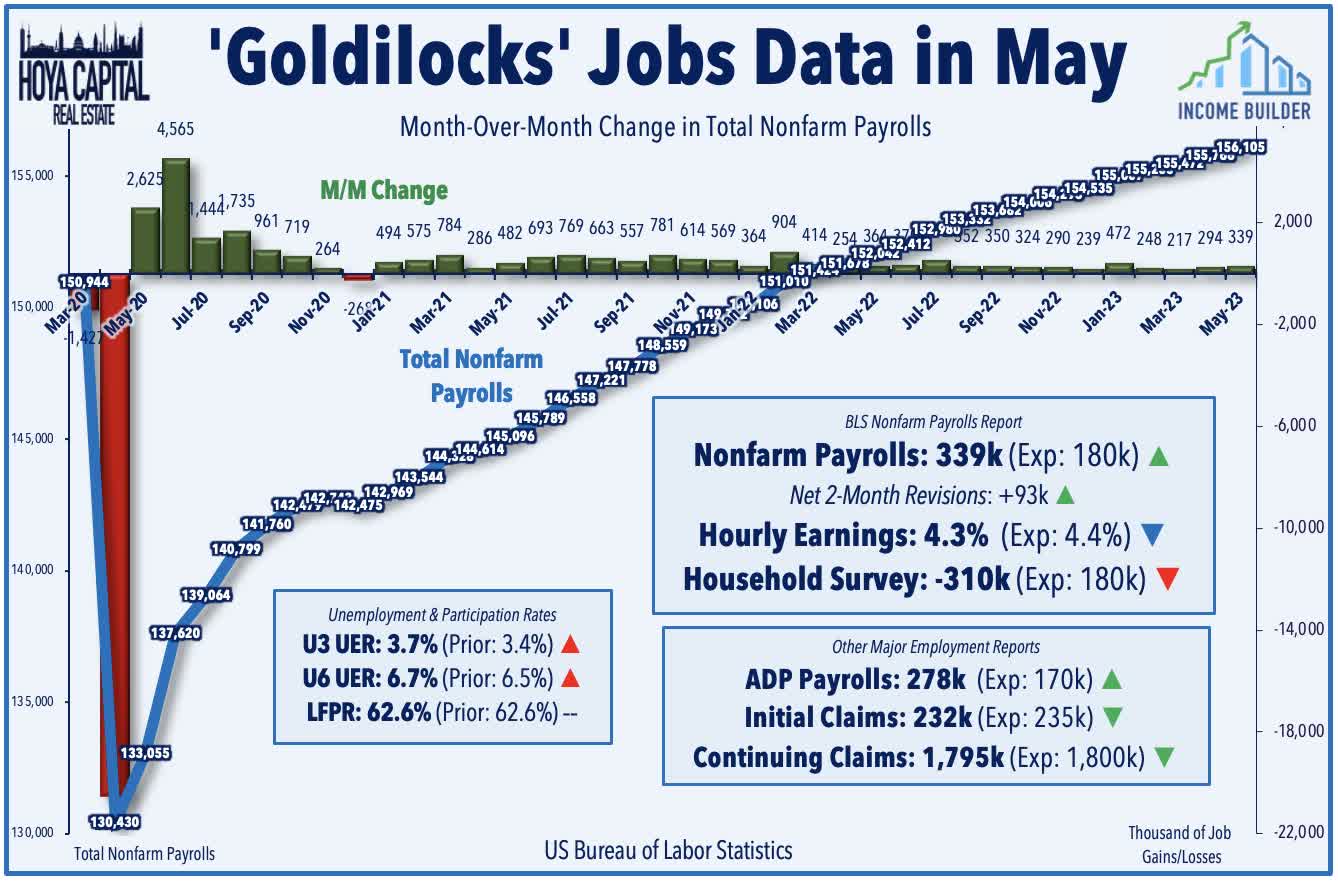

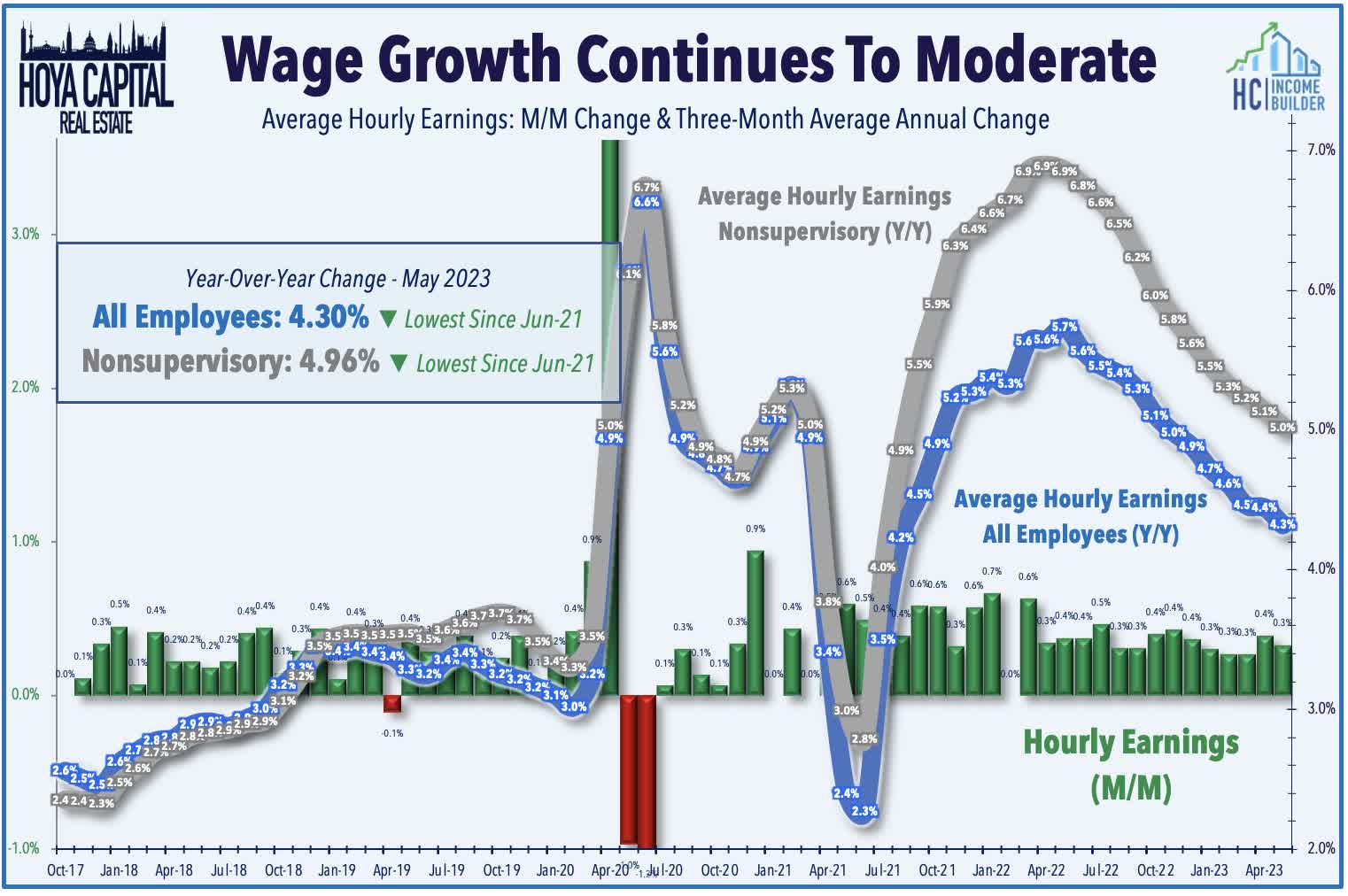

- The critical BLS nonfarm payrolls report showed that the U.S. economy added 339k jobs in May - well above expectations of 180k - marking the 29th straight month of positive job growth. Average hourly earnings, a key inflation indicator, increased less than expected while the unemployment rate increased to its highest level since October 2022.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 3rd.

U.S. equity markets rebounded this week as a critical slate of employment data provided evidence of a 'soft' economic landing, showing stronger-than-expected job growth combined with a cooldown in wage pressures. Another critical complication was resolved this week with the successful passage of a debt ceiling agreement to avoid a U.S. default and enact modest cuts to non-defense federal spending. Meanwhile, Fed officials entered the 'quiet period' before their June meeting with a notably less hawkish tone, signaling a likely 'pause' in their historically aggressive rate hiking cycle.

{kind=link}

Hoya Capital

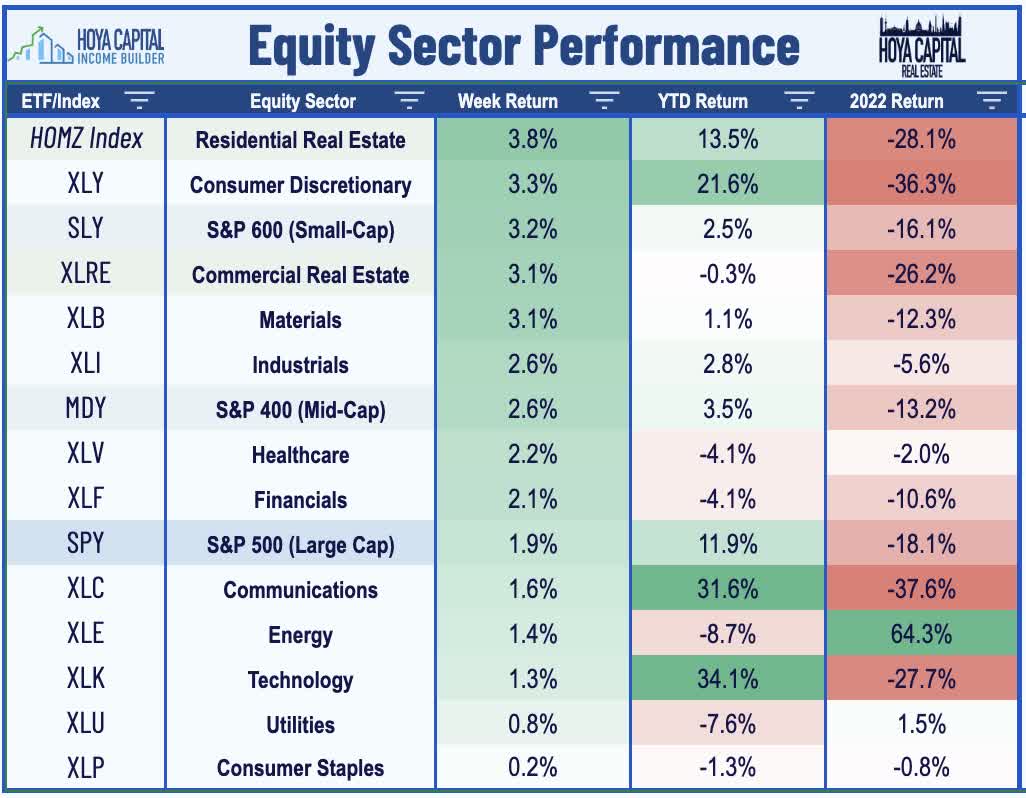

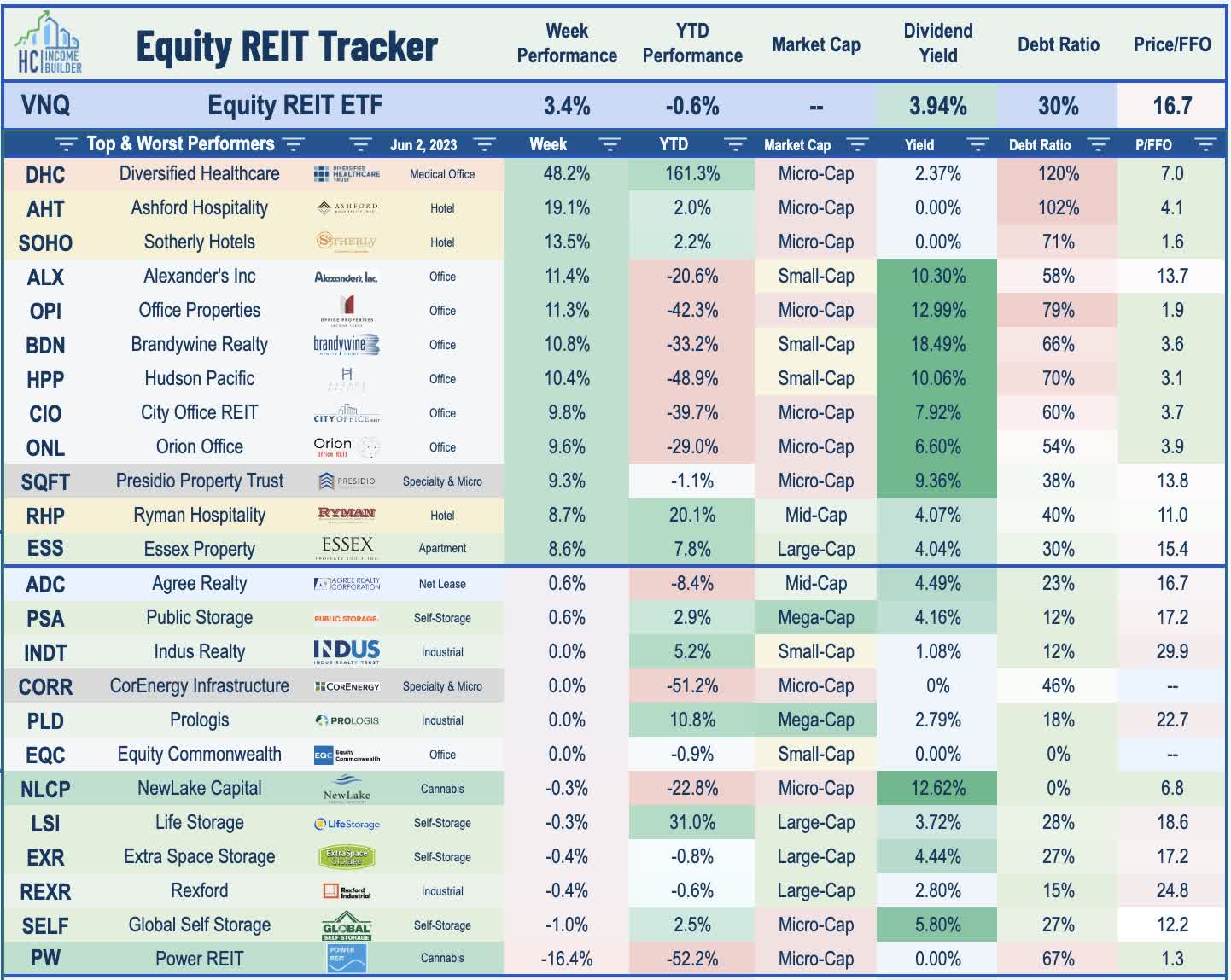

Closing the week at its highs for the year, the S&P 500 advanced 1.9% this week - lifting the major benchmark to the cusp of 'bull market' territory with gains of nearly 20% from its lows last October. The Mid-Cap 400 rallied 2.6% while the Small-Cap 600 gained more than 3%, each narrowing their wide year-to-date underperformance gap with the tech-heavy Nasdaq 100 . Real estate equities were also among the leaders on the week, lifted by a moderation in benchmark interest rates and an encouraging slate of business updates ahead of the annual REITweek industry conference. The Equity REIT Index rallied 3.4% this week, with 17-of-18 property sectors in positive territory, while the Mortgage REIT Index rallied more than 5%. Homebuilders and the broader Housing Index continued their strong start to the year on data showing continued buoyance in home prices and rents.

{kind=link}

Hoya Capital

The 'Goldilocks' slate of jobs data - combined with the debt ceiling agreement and dovish comments from Philadelphia Fed President Harker and Fed Governor Jefferson - sent the swaps-implied likelihood of a June rate hike down to just 25%, down sharply from the 75% implied probability last week. Benchmark interest rates retreated from three-month highs set last week, with the 2-Year Treasury Yield declining 5 basis points on the week to 4.51%, while the 10-Year Yield dipped 12 basis points to 3.69%. Oil prices and commodities remained under pressure this week ahead of a closely-watched OPEC+ meeting this weekend. Pressured by concerns over Chinese demand following a five-month-low PMI print this week, the WTI Crude benchmark briefly dipped below $68/barrel to the lowest levels since December 2021 before rebounding later in the week to close around $72/barrel. All eleven GICS equity sectors finished higher on the week, with Consumer Discretionary ( XLY ) and Materials ( XLB ) stocks leading on the upside.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

The critical BLS nonfarm payrolls report this week showed that the U.S. economy added 339k jobs in May - well above expectations of 180k - marking the 29th straight month of positive job growth following the historic declines in March and April of 2020. Services sectors fueled the job gains in May - accounting for 313k of the 339k in job gains - led by strength in professional services, government, healthcare, and transportation. Hiring in leisure and hospitality also remained firm with 48k jobs added, but this represented a moderation from its twelve-month average of 77k. Outside of construction - which added 25k jobs for the month - other goods-producing sectors produced just 1k in job gains for the month. Earlier in the week, ADP reported that private payrolls rose 278k, which was also well above the median estimate of 170k while JOLTs data was also better-than-expected, showing that job openings unexpectedly rose in April with 1.8 job openings for every unemployed person, which remains above the roughly 1.2x historical average.

{kind=link}

Hoya Capital

Beneath the impressive headline prints, however, there was some evidence of 'loosening' in labor market conditions as wages rose at a slower-than-expected pace during the month while the unemployment rate rose to its highest level since 2022. Average hourly earnings ("AHE"), a key inflation indicator, rose 0.3% in May - below the expected 0.4% increase, which pulled the annual increase down to 4.3%. Since the start of 2023, AHE has averaged just 3.8% on an annualized basis - which is only marginally above the 3.3% increase in 2019 in a year that CPI inflation averaged just 1.8% - suggesting that concerns over wage-driven inflation are overstated. The average workweek also edged down by about 10 minutes to 34.3 hours in May, which was the lowest since the start of the pandemic and down nearly an hour per week from the multi-decade highs set in early 2021, providing further evidence of normalizing labor market conditions following pandemic-era shortages.

{kind=link}

Hoya Capital

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

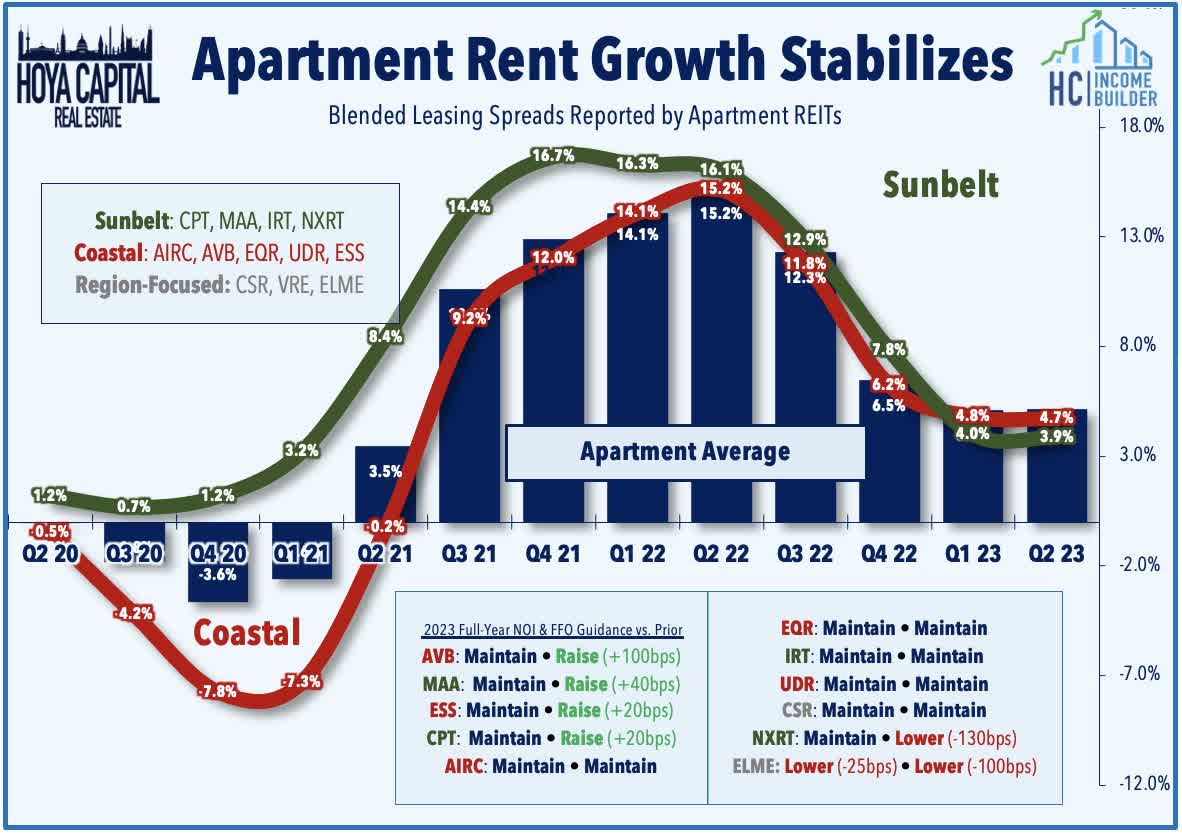

Apartment : Ahead of the annual REITweek industry conference next week, apartment REITs rallied more than 5% after a series of positive operating updates showing sustained buoyancy in rental rates. Equity Residential ( EQR ) rallied more than 6% this week after it boosted its full-year earnings outlook citing strong demand in New York and lower than previously anticipated delinquency in southern California. EQR now expects full-year FFO growth of 7.1% at the midpoint - up 80 basis points from its prior outlook provided in April - and expects to report 2023 same-store net operating income (NOI") growth of 6.5% at the midpoint, up 100 basis points from its prior midpoint of 5.5%. EQR commented that its "benefiting from limited new apartment supply in most of our markets as well as the high prices and low availability of single family housing in these markets." AvalonBay ( AVB ) gained nearly 6% after it reported that rent growth has accelerated sequentially in each month since bottoming in December, noting that its blended spreads were roughly 5% in April and May while its renewal offers for June and July were delivered with average increases in the "low-7% range."

{kind=link}

Hoya Capital

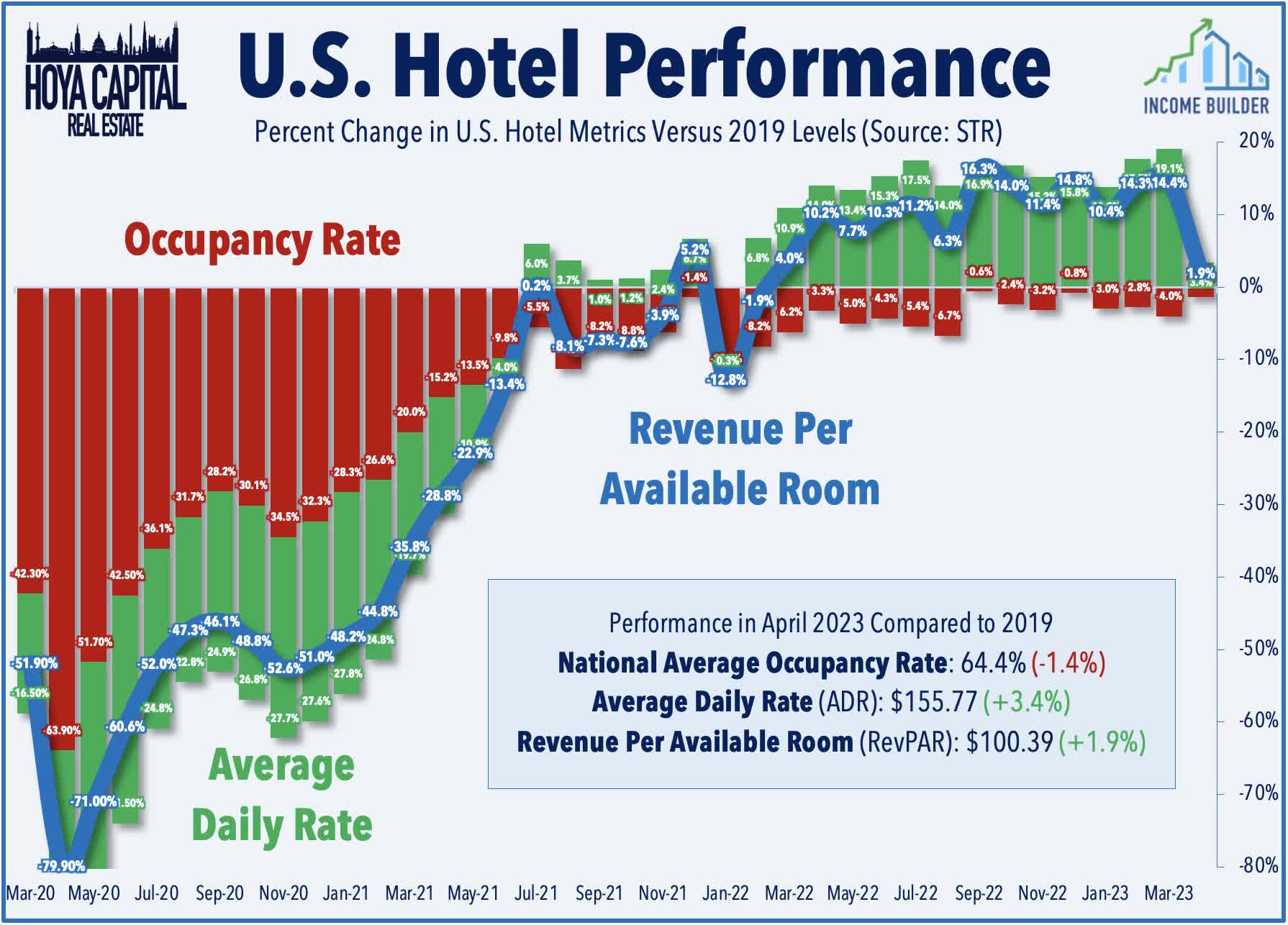

Hotels : Economically-sensitive property sectors were also among the leaders this week, with small-cap and micro-cap REITs enjoying particularly strong gains. Small-cap Sotherly Hotels ( SOHO ) rallied more than 13% after it announced that it would make a $0.50/share special dividend for its suite of preferred stock - its Series B, Series C, and Series D. SOHO's preferred stock dividends were suspended from mid-2020 until January 2023 and thus accumulated 9 quarters of cumulative unpaid distributions. The special dividend represents one quarters-worth of these unpaid dividends. Service Properties ( SVC ) rallied more than 7% after it announced that it purchased the 250-room Nautilus Hotel in Miami for $165.4M, or $661.6K per key. The hotel will initially be branded as the Nautilus Sonesta Miami Beach, and undergo a $25M repositioning starting in mid-2024 with plans to reopen in early 2025. As noted in Hotel REITs: The Pandemic Is Over , despite lingering recession concerns, hotel REITs are pacing for a second-straight year of outperformance after punishing early-pandemic declines, buoyed by steady operating improvement and the long-awaited return of dividends.

{kind=link}

Hoya Capital

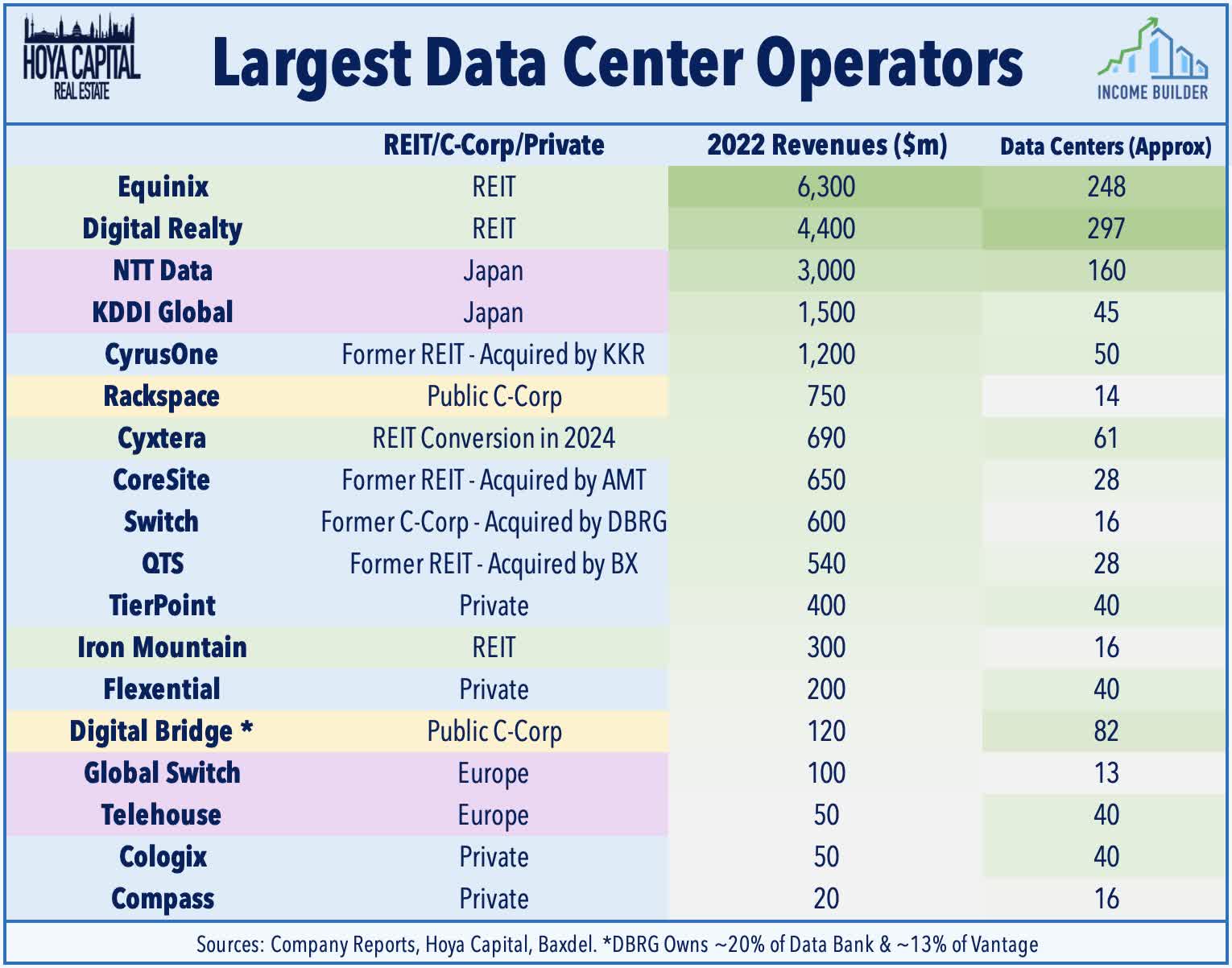

Data Center : Extending its rally sparked last week by the blowout Nvidia ( NVDA ) earnings results last week, Digital Realty ( DLR ) advanced another 6% on the week on reports of M&A activity in the data center space. Asset manager Brookfield Infrastructure ( BIP ) and former REIT DigitalBridge ( DBRG ) are reportedly competing to purchase privately-held Compass Datacenters for more than $5.5 billion, including debt. Compass currently operates roughly 16 data centers across the US, Europe, and Israel. Brookfield and DigitalBridge are leading separate consortiums with an outcome of the sale process expected by next month. Last week, Nvidia said that it is "significantly increasing its supply of data center chips" to meet "surging" demand resulting from investments in artificial intelligence ("AI"). In our REIT Earnings Recap , we noted that data center REITs have seen improved pricing power in recent quarters as supply/demand conditions have tightened after a three-year stretch of lackluster rent growth.

{kind=link}

Hoya Capital

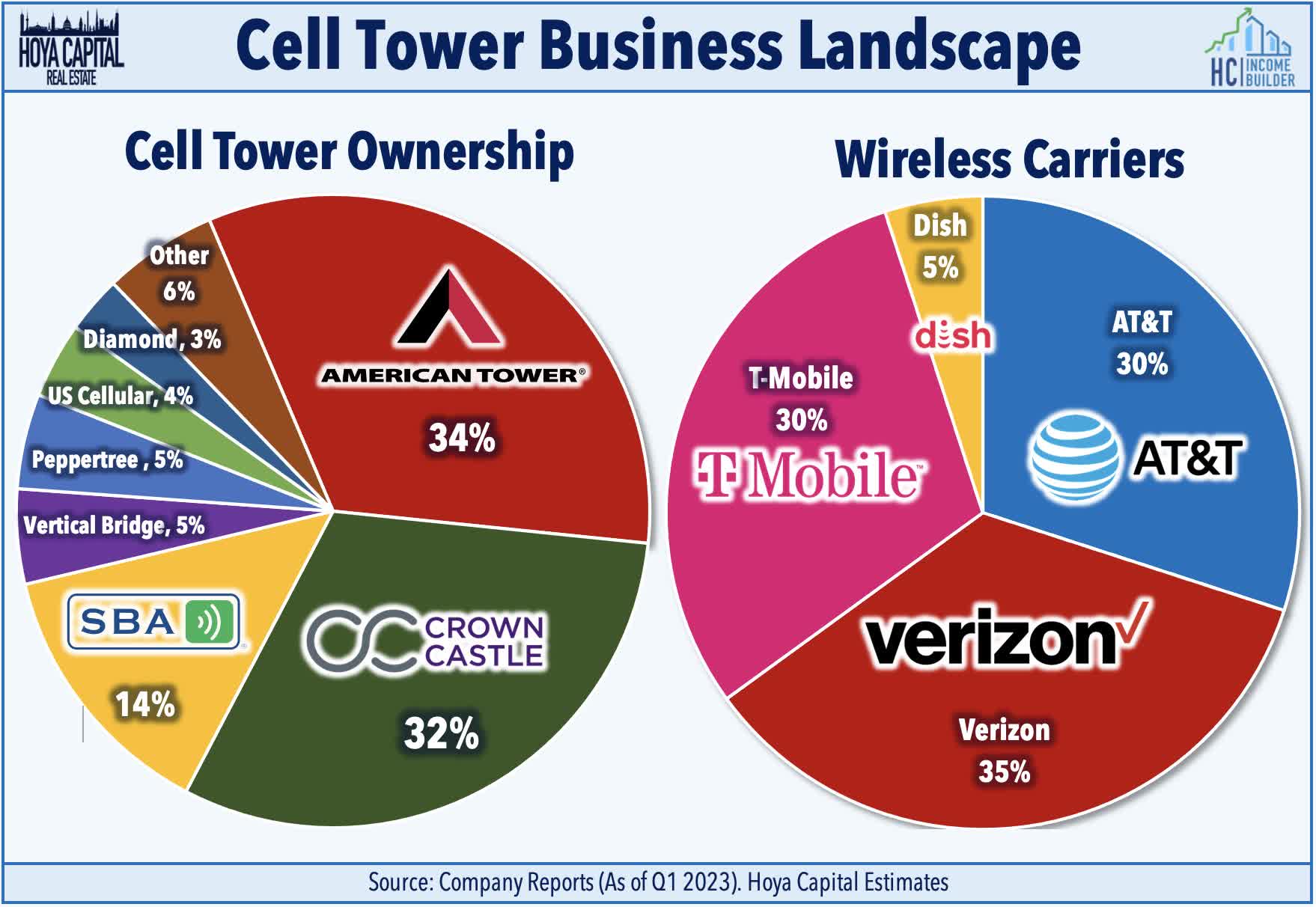

Cell Tower : Sticking on the technology theme, the trio of cell tower REITs - American Tower ( AMT ), Crown Castle ( CCI ), and SBA Communications ( SBAC ) - all traded higher this week on reports that e-commerce giant Amazon ( AMZN ) has been in talks with wireless carriers about offering low-cost or free nationwide mobile phone service to its Prime subscribers. The company is reportedly negotiating with Verizon ( VZ ), T-Mobile ( TMUS ), and Dish Network ( DISH ) to get the lowest possible wholesale prices. The deal would reportedly allow AMZN to offer Prime members wireless plans for $10 a month or less. DISH surged on the report, while the three major carriers posted sizable declines. In our Cell Tower REIT report, we've discussed the possibility that DISH could become a legitimate fourth competitor if it partners with one of the major technology firms that have shown interest in entering the internet provider business over the past half-decade.

{kind=link}

Hoya Capital

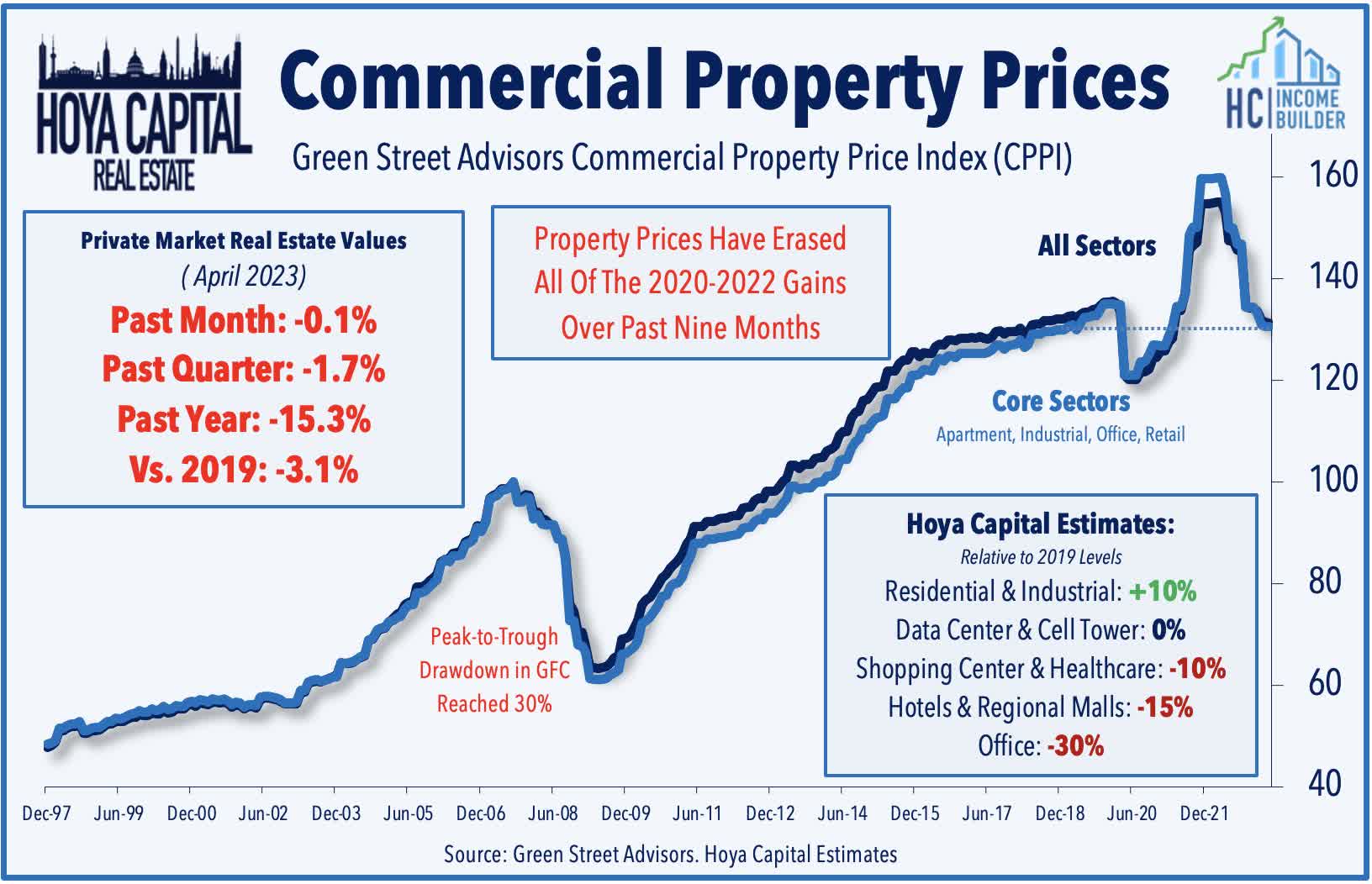

This week, we published State of REITs: Distress & Opportunity . Whether fundamentally justified or not, commercial and residential real estate markets continue to bear the brunt of the Federal Reserve's historically swift monetary tightening cycle. Commercial real estate, in particular, has been the boogeyman that bank executives have blamed for unrelated distress. While there are pockets of distress, actual default rates remain historically low. The pockets of distress are almost entirely debt-driven, with the notable exception of coastal urban office properties. Nearly every property sector reported "same-store" property-level income above pre-pandemic levels. Property-level fundamentals are fine, but some balance sheets are not. Many real estate portfolios - particularly private equity funds and non-traded REITs - were not prepared for anything besides a near-zero-rate environment. With commercial property values now 15-20% below 2022 highs, and with interest rates doubling from last year, the tide is just beginning to recede for many highly-levered portfolios or those lacking access to capital.

{kind=link}

Hoya Capital

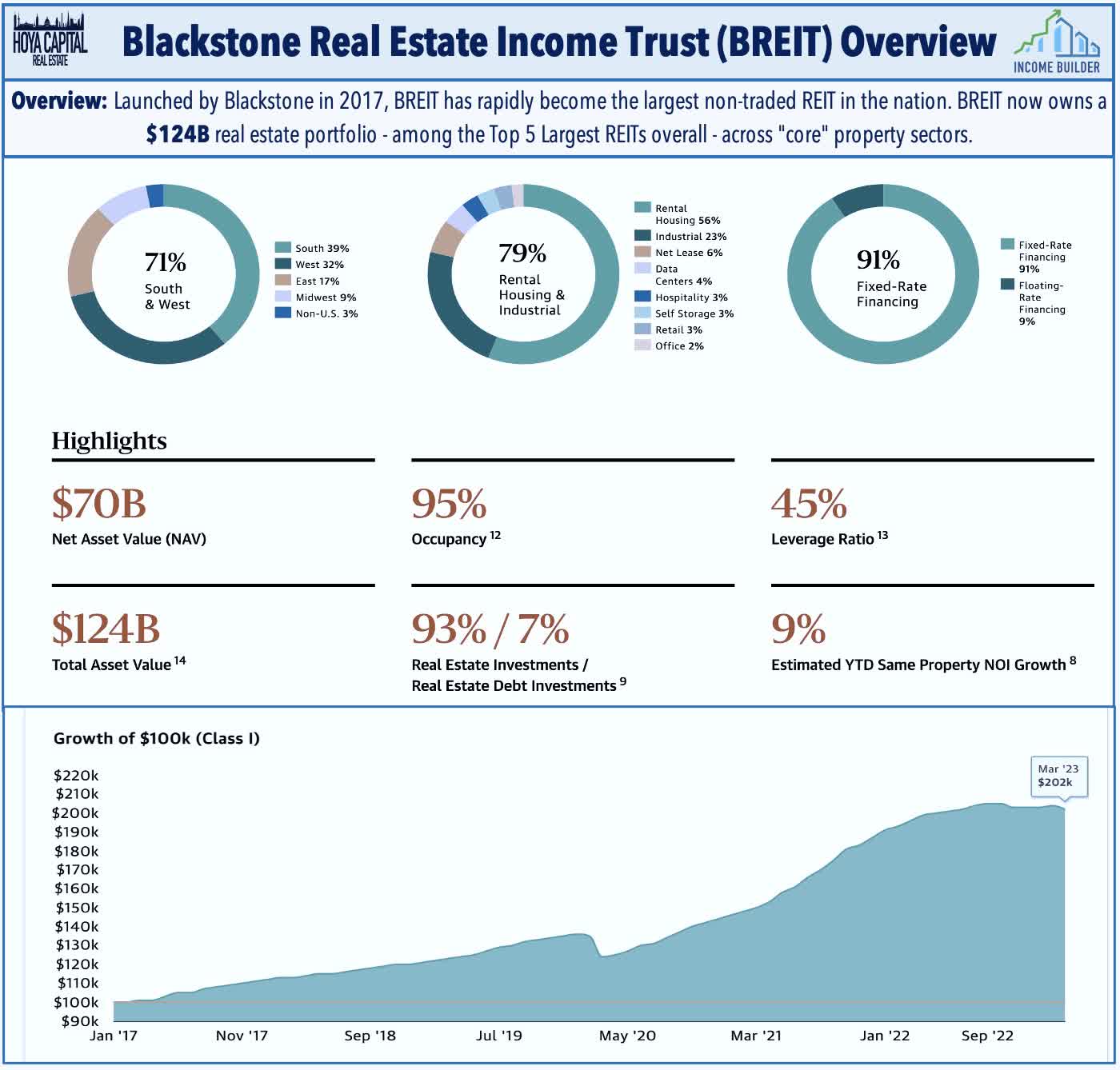

Speaking of pockets of distress, asset manager Blackstone ( BX ) disclosed this week that it again had to limit withdrawals from its non-traded real estate platform in May - the seventh straight month that the firm's flagship fund limited redemptions. BREIT received $4.4 billion of redemption requests in May and paid out just 30% of those requests to investors, up slightly from the 29% of requests fulfilled last month. BREIT has paid out $7.5B to redeeming shareholders since November 30, 2022 when redemption limits began. BREIT noted that an investor that requested their money back beginning last November - and did so in every month since then - has received 90% of their money back - which BREIT cited as evidence that "the semi-liquid structure is working as intended." As noted in our Casino REIT report last month, analysts have questioned BREIT's self-reported NAV, and investors have seized on the opportunity to redeem shares at these premium NAV valuations.

{kind=link}

Hoya Capital

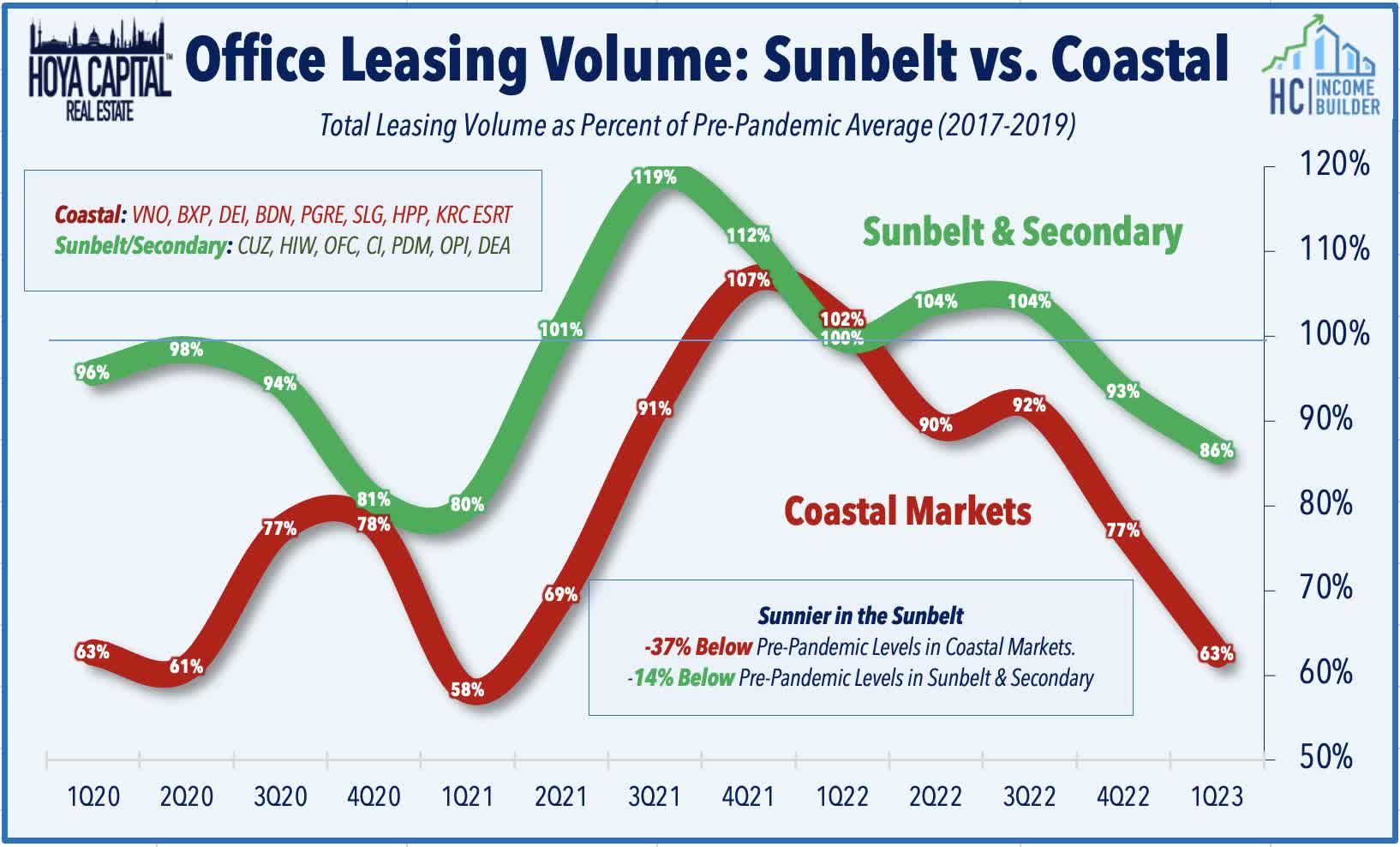

Office : Sunbelt-focused office REIT Highwoods Properties ( HIW ) announced that it sold two non-core assets for combined proceeds of $40.2M at an implied capitalization rate of 6.5%. HIW commented that the transactions "highlight that high-quality buildings with healthy occupancy continue to generate solid interest from qualified buyers" and noted that proceeds from these sales will "fortify our already healthy balance sheet." Independence Park - a 116K square foot office building in Tampa - was sold for $19.5M. The property is 100% occupied by a single user under a lease the company signed with the new user last year. As part of the sale of One Independence Park, the Company provided $9.8 million in non-recourse first mortgage seller financing at an annual rate of 5.50%. Riverbirch - a 60K square foot office building in Raleigh - was sold for $20.7M. It's also 100% occupied by a single customer that recently renewed under a long-term lease. As we discussed in Office REITs: How Bad Is It , we believe that the longer-term outlook remains far "sunnier" in the Sunbelt and in secondary markets with net population growth, shorter commute times, and a more favorable industry mix.

{kind=link}

Hoya Capital

Healthcare : Healthcare Realty ( HR ) - which we own in the REIT Focused Income Portfolio - rallied more than 6% on the week after it announced a new $500M stock buyback program of its common stock. The Company does not intend to use debt to fund the share repurchase program. Elsewhere in the healthcare space, CareTrust REIT ( CTRE ) advanced nearly 7% after it announced that it has acquired a 105-unit, two-facility memory care portfolio with facilities located in Ohio and Michigan. The facilities will be managed by Ridgeline Management, which signed a new 15-year master lease with CareTrust that includes two, 5-year renewal options and annual CPI-based rent increases. CareTrust’s initial investment in the facilities was $21.1 million. The deal was funded using proceeds from the company’s $600 million unsecured revolving credit facility and provides for initial annual base rent of $1.79M.

{kind=link}

Hoya Capital

Malls : Mall owner Seritage Growth ( SRG ) - which continues to sell its properties as part of its strategic liquidation - rallied 6% on the week after it announced that it made a voluntary prepayment of $200M toward its $1.6B term loan facility provided by Berkshire Hathaway Life Insurance. With this prepayment, Seritage has repaid $1B since December 2021, and $600M of the term loan facility is outstanding. In April, Seritage announced that it has generated $290.4M of gross proceeds from the sale of 27 assets since the start of 2023 to bring its portfolio to 72 properties, down from its peak in 2019 of over 200 properties. SRG noted that the $255 million from the sale of 21 stabilized properties were sold at a blended cap rate of 9.2%, up roughly 200 basis points from early 2021 when it reported a similarly-size portfolio sale closed at a cap rate of 7.5%. In May, SRG announced an additional $21.1 million of gross proceeds from the sale of four wholly owned assets.

{kind=link}

Hoya Capital

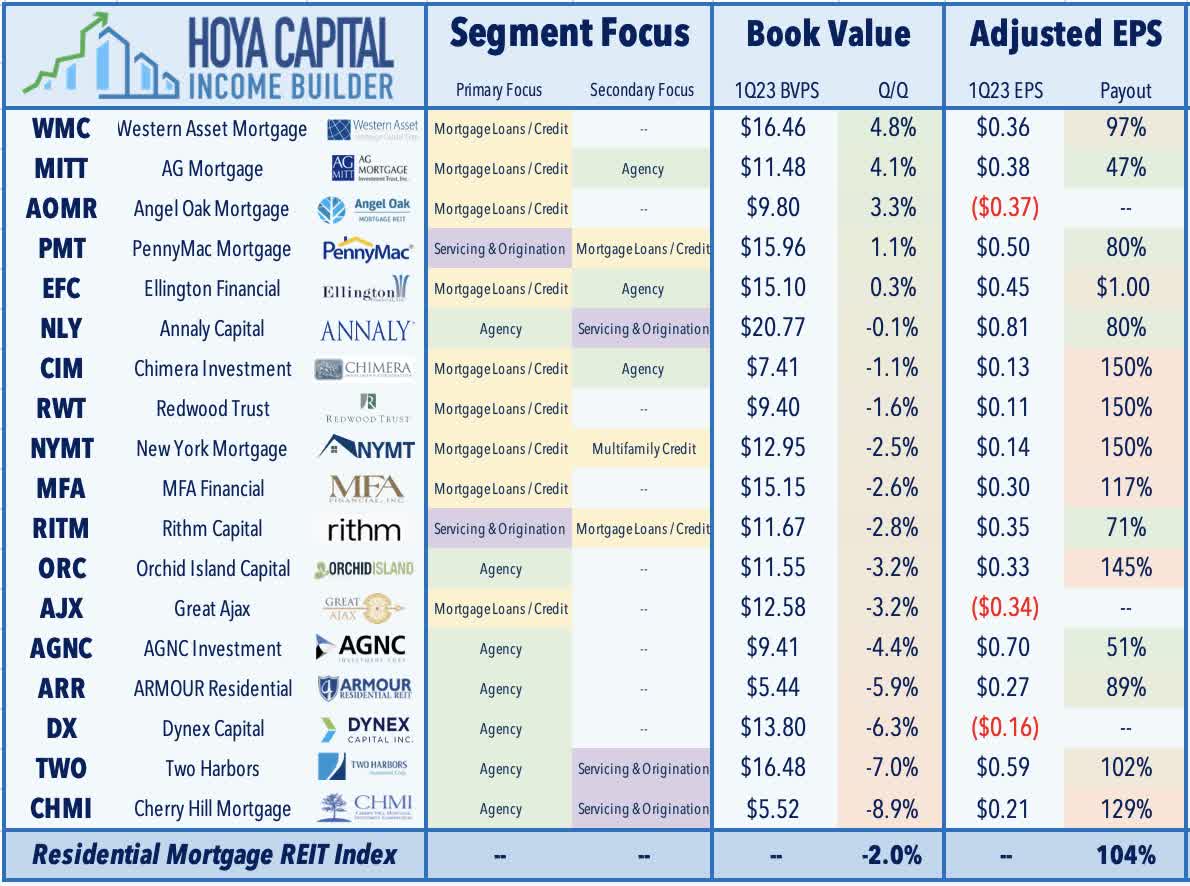

Mortgage REIT Week In Review

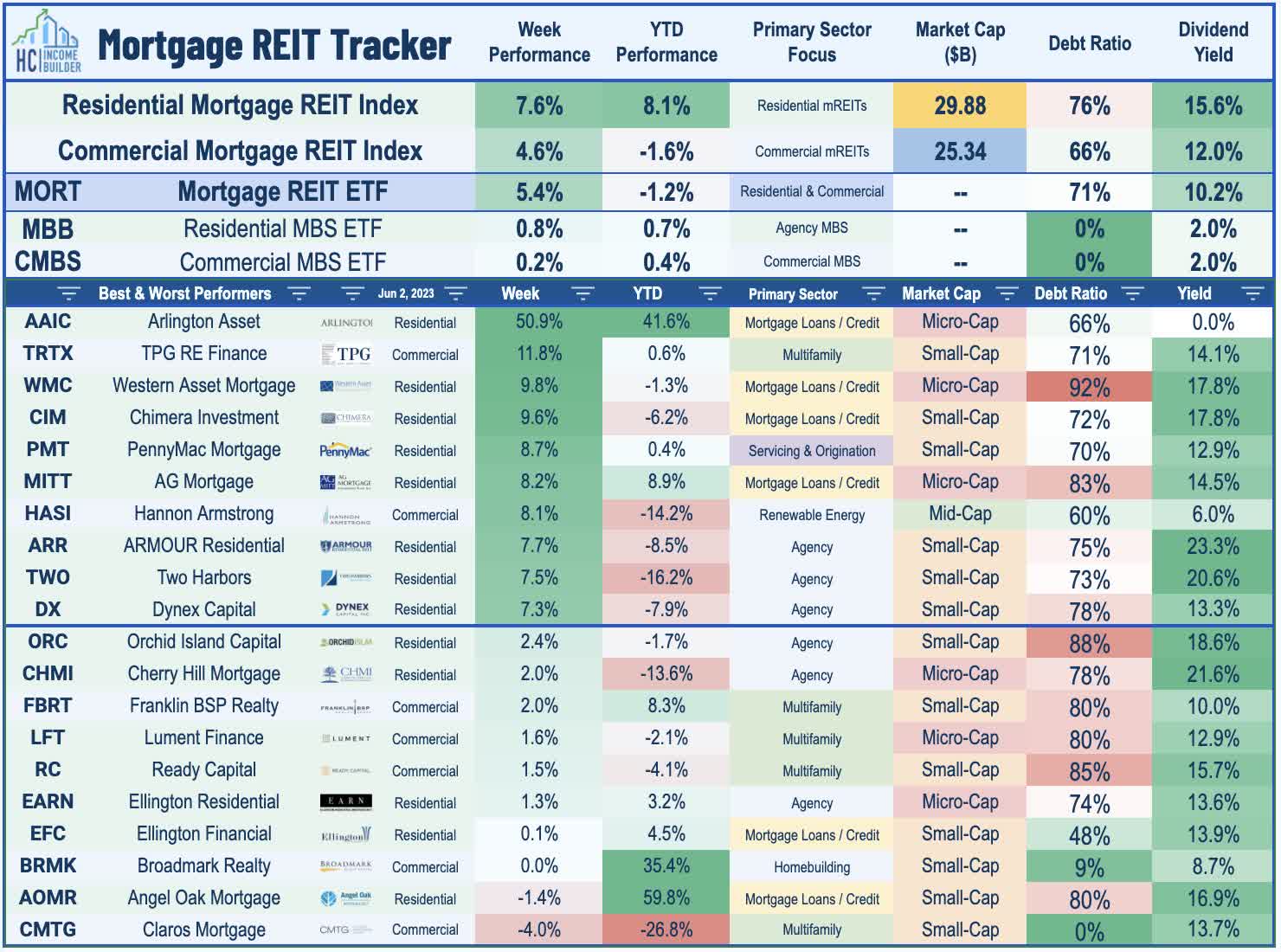

Mortgage REITs posted their best week since early January as hopes of a 'soft landing,' and a flurry of M&A news lifted the iShares Mortgage Real Estate ETF ( REM ) to gains of 5.4%. Arlington Asset ( AAIC ) rallied more than 50% on the week after Ellington Financial ( EFC ) announced that it would acquire the small-cap residential mREIT in a stock and cash deal at an implied price of $4.77 per share - a 73% premium to AAIC's prior close - representing a 15% discount to its tangible book value. The combined company will have pro-forma equity capital base of more than $1.5B, of which EFC shareholders will own 85% while AAIC's owners will hold 15%. The acquisition is expected to add to EFC's earnings per share this year and to its book value "within a year." EFC finished higher by 0.1% on the week. Ready Capital ( RC ) announced that its acquisition of Broadmark Realty closed this week. Announced back in March, the deal was the first of six REIT merger deals announced over the past quarter. RC also announced that its Board approved a $100.0M stock repurchase program of its common stock.

{kind=link}

Hoya Capital

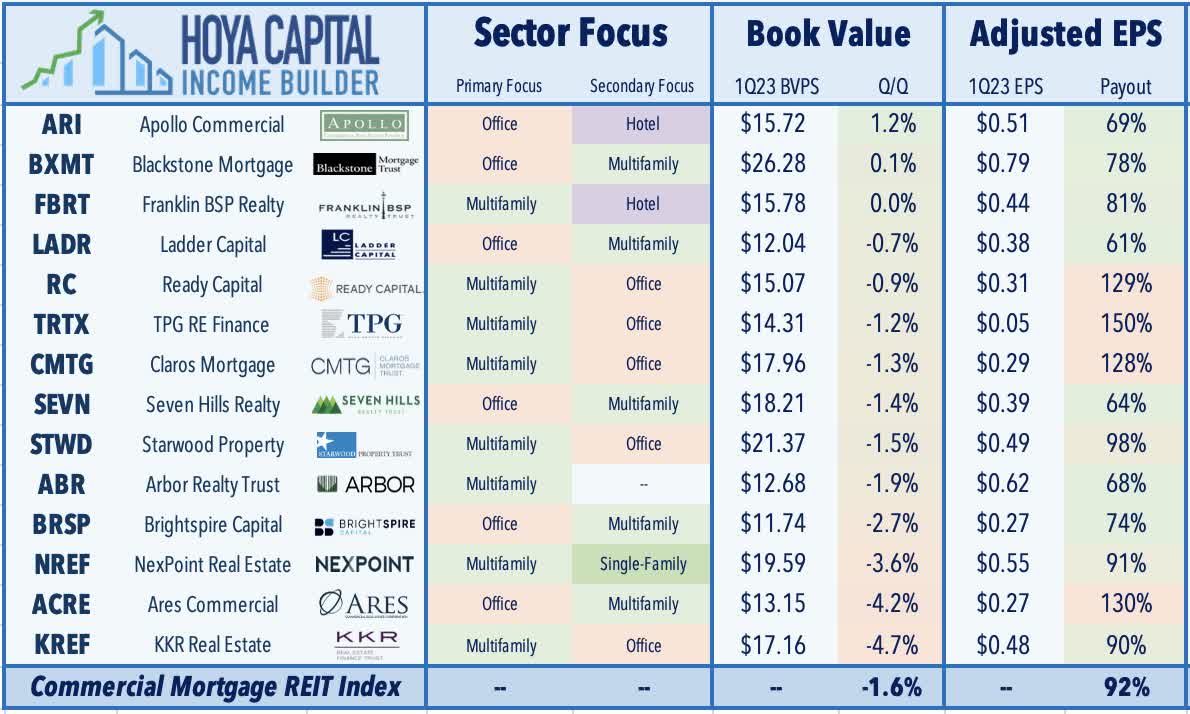

Elsewhere, Hannon Armstrong ( HASI ) rallied more than 8% after a similar-sized decline last week following a $300M secondary common stock offering. This week, HASI announced that it increased its revolving credit facility by $240M to $840M and also expanded the accordion feature by $420M, resulting in total capacity of up to $1.26B. Several office-heavy lenders were also among the leaders this week, including TPG Real Estate ( TRTX ), Granite Point ( GPMT ), and Ladder Capital ( LADR ). Residential lender Arbor Realty ( ABR ) - which we own in the Focused Income Portfolio - rallied nearly 6% on the week after Wedbush analyst Jay McCanless initiated coverage with a buy rating, citing its stable earnings stream and attractive dividend yield which is "well-supported by both GAAP EPS and earnings available for distribution." As noted in our Earnings Recap , residential mREITs reported an average decline in BVPS of 1.9% in Q1, while commercial mREITs reported a 1.8% average decline. Dividend coverage was stronger for commercial mREITs with about 75% of commercial mREITs covering their dividend with Q1 adjusted EPS while just 50% of residential mREITs covered their dividend.

{kind=link}

Hoya Capital

{kind=link}

Hoya Capital

2023 Performance Recap & 2022 Review

Through twenty-two weeks of 2023, the Equity REIT Index is now lower by 0.6% on a price return basis for the year (+0.4% on a total return basis), while the Mortgage REIT Index is lower by 4.2% (-0.2% on a total return basis). This compares with the 11.9% gain on the S&P 500 and the 3.5% advance for the S&P Mid-Cap 400 . Within the real estate sector, 6-of-18 property sectors are in positive territory on the year, led by Single-Family Rental, Data Center REITs, and Industrial REITs, while Office and Cell Tower REITs have lagged on the downside. At 3.69%, the 10-Year Treasury Yield has declined by 19 basis points since the start of the year - up from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 2.2% this year. Crude Oil - perhaps the most important inflation input - is lower by 11% on the year and roughly 40% below its 2022 peak.

{kind=link}

Hoya Capital

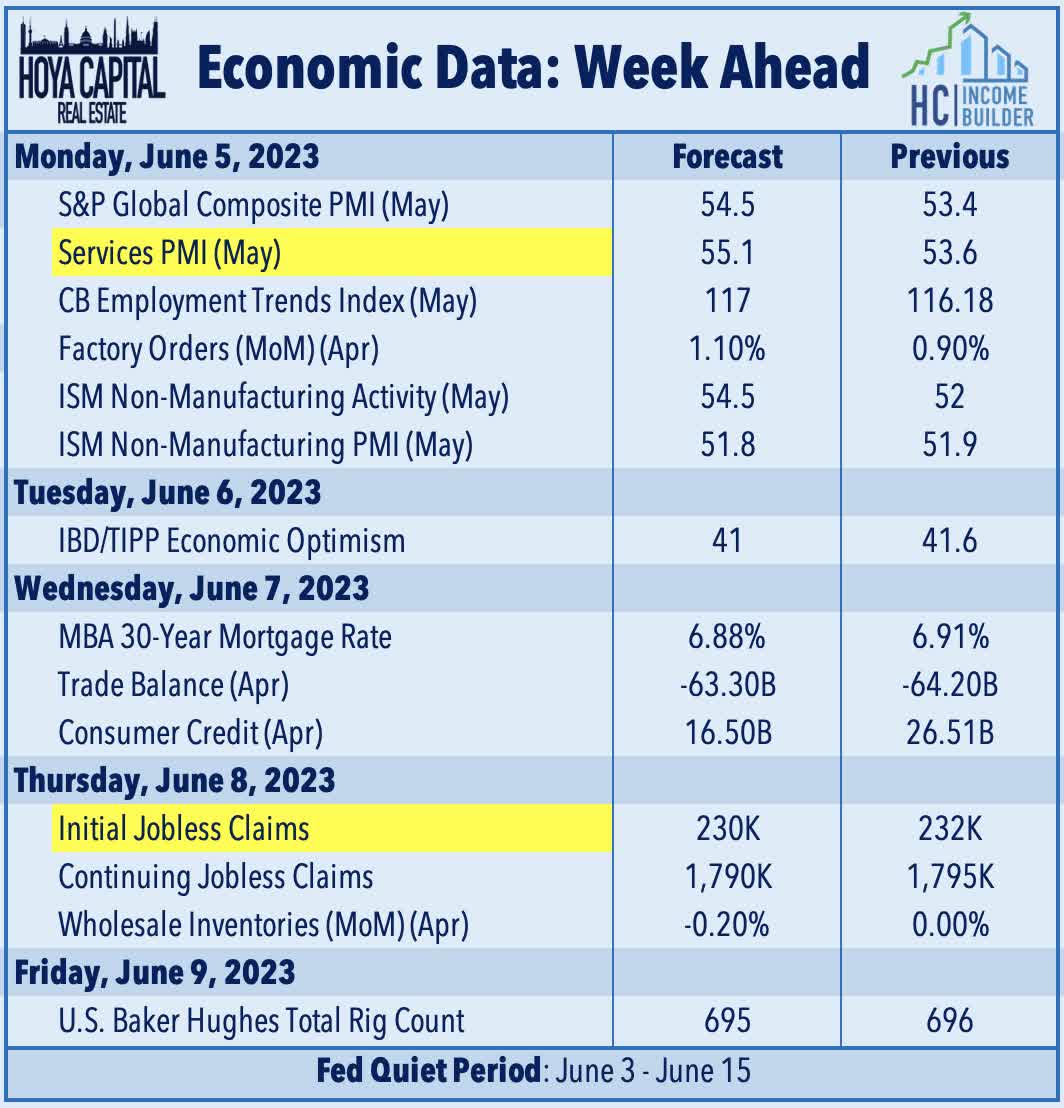

Economic Calendar In The Week Ahead

The economic calendar slows down in the week ahead while the Federal Reserve enters its "quiet period" ahead of its June 14th policy decision in the following week. As noted above, swaps markets now imply a 25% probability that the Fed will hike rates by 25 basis points in their June meeting to a 5.50% upper bound, down from the nearly 75% probability in the prior week. The major reports of the week include the final look at May PMI data from the Institute for Supply Management ("ISM") and S&P Global. Recent PMI data has been largely consistent with the 'soft landing' thesis, with S&P reporting an acceleration in activity last month combined with a cooldown of input price pressures. ISM reported a "dramatic" decline in price pressures in its manufacturing PMI survey this past week, with 85% of businesses reporting 'lower' or 'same' prices in May compared to April. We'll also be watching weekly Jobless Claims data on Thursday and weekly mortgage market data from the Mortgage Bankers Association on Wednesday.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Goldilocks Is Back