GSBD - Goldman Sachs BDC: An Attractive Income Buy With A 12% Yield

2024-01-18 06:17:45 ET

Summary

- Goldman Sachs BDC has large investments in variable rate loans and employs a first-lien strategy.

- The BDC's portfolio value has declined due to higher repayments and loan sales in the last year, but the dividend is well-supported.

- A reboot of the loan origination business may deliver organic NII growth going forward.

- The BDC offers a solid 12% yield and a dividend coverage ratio of 124% implies a reasonably well-supported dividend.

Goldman Sachs BDC (GSBD) runs a first-lien strategy and is an interesting BDC for investors for income, yield and growth. The BDC's shares are currently trading at a small premium to net asset value, but have traded at a higher premium in the past. I like Goldman Sachs BDC's first-lien strategy and although the BDC has seen pressure on its portfolio value, largely due to higher repayments and loan sales, I believe that the dividend is well-supported and should not get cut even if the BDC's interest income were to decline. I don't expect a lot of dividend growth going forward, at least not in a low-rate world, but I do believe that income investors are dealing with a solid 12% yield!

Goldman Sachs BDC is a variable rate, first-lien BDC

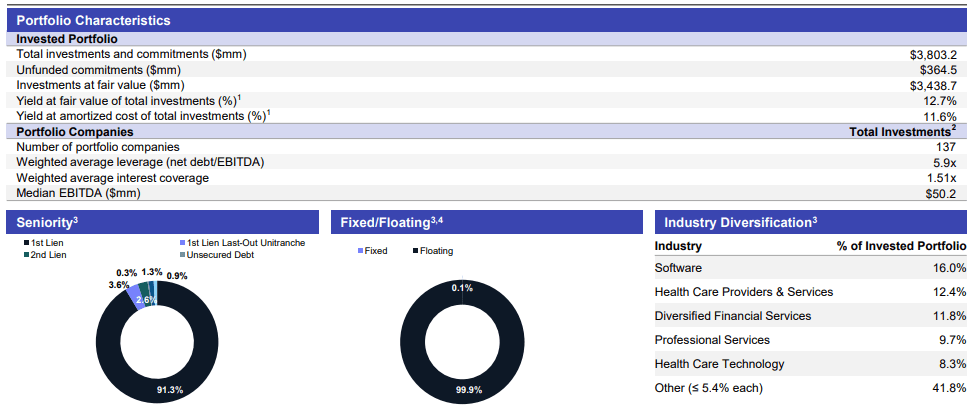

Goldman Sachs BDC's best feature, in my opinion, is that the BDC is focused on first-liens which represented the largest percentage in the BDC's portfolio mix. Goldman Sachs BDC is mostly invested in first liens (95%), followed by second liens (3%) and even smaller percentages attributed to categories like unsecured debt and preferred/common stock.

At the end of the September quarter, Goldman Sachs BDC's portfolio included assets with a combined worth, based off of fair value, of $3.4B. The BDC's portfolio declined 5% on a year over year basis, from $3.62B in last year's Q3'23, chiefly because of higher repayments and loan sales. I expect these trends to continue until the federal fund rate at least comes down a little bit which may help drive loan demand upward. In other words, while the Federal Reserve's high-rate policy has led to income tailwinds in FY 2023, it did affect negatively the BDC's loan, portfolio and net asset value growth. In a low-rate environment, I expect demand for new loans to pick up again which may support Goldman Sachs BDC's organic NII growth in FY 2024.

{kind=link}

With total investments around $3.8B, Goldman Sachs is a mid-sized BDC and it has a focus on variable rate debt investments as well. This means that the BDC's income benefits from increases in the federal fund rate while it may be hurt by decreases in the federal fund rate. At the end of the September quarter, Goldman Sachs BDC's portfolio was almost fully invested in variable rate loans.

{kind=link}

Strong y/y interest income growth, solid dividend coverage

Despite downward pressure on Goldman Sachs BDC's portfolio (and net asset) value, the BDC has been able to deliver significant net investment income growth in the last several quarters.

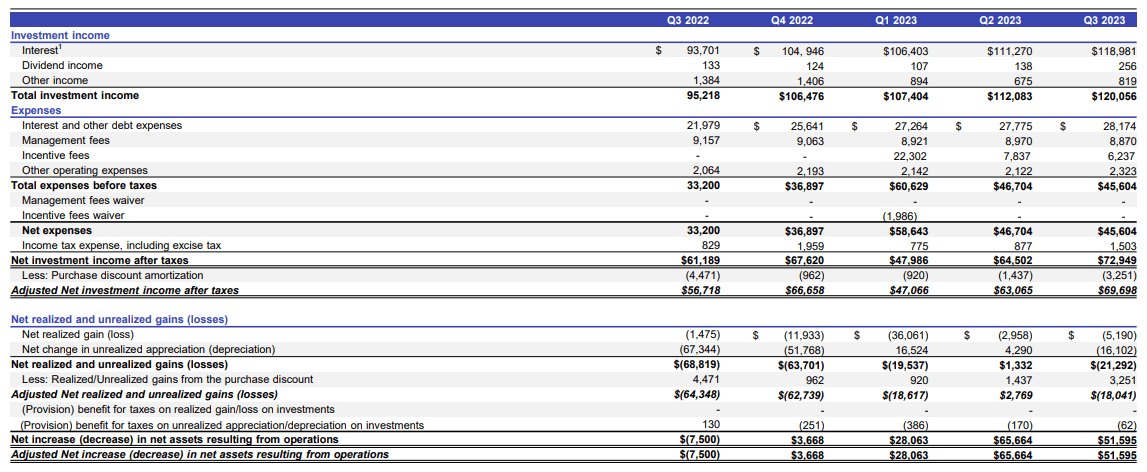

This positive trend in the BDC's business can be traced back to the Federal Reserve raising the federal fund rate in the first half of FY 2023 which benefited Goldman Sachs BDC's variable rate debt investments. Over the course of the last year, Goldman Sachs BDC's total investment income rose 26% year over year to $120.1M with the bulk of this growth being attributable to surging interest income from its loan investments.

Goldman Sachs BDC's adjusted net investment income, which should be used to calculate the BDC's dividend coverage, soared 23% year over year to $69.7M, but this growth should be expected to slow drastically now that the Federal Reserve is preparing for a pivot.

Goldman Sachs BDC's dividend coverage, calculated based off of per-share adjusted NII, in the first nine month of the FY 2023 was 124% so I believe the BDC does offer a well-supported dividend yield of 12% at the moment. My opinion on Goldman Sachs BDC may change going forward based on the level of excess coverage. A drop of the dividend coverage ratio below 110% is something that would make me uncomfortable and potentially lead to a rating downgrade to hold.

{kind=link}

A solid BDC yielding 12% demanding only a small NAV premium

If a BDC trades at net asset value, it means that investors can generate about the same yield on their shares that the BDC generates on its portfolio. At the end of the September quarter, Goldman Sachs BDC achieved a yield on all of its investments (debt, equity and warrants) of 12.7%. Since the BDC pays $0.45 per-share quarterly to shareholders, investors following an income strategy get to collect a 12.1%.

Goldman Sachs BDC trades at a marginal premium to net asset value of 2% which places the BDC in the midfield when compared against Ares Capital ( ARCC ) and Blue Owl Capital ( OBDC ). However, Goldman Sachs BDC achieved a 3-year average P/NAV ratio of 1.10X which I would also consider to be more appropriate now given the BDC's double-digit NII growth and high dividend coverage. I believe that the BDC could ultimately trade at 1.10-1.15X net asset value if Goldman Sachs BDC manages to deliver stable dividend coverage and net investment income growth in a low-rate world.

Risks with Goldman Sachs BDC

Goldman Sachs BDC has considerable variable rate exposure which obviously is a challenge in a low-rate world. The BDC's investable assets were 99.9% variable rate, meaning the BDC is at risk of seeing deteriorating profitability, on a net investment income basis, throughout the year.

The Federal Reserve has effectively said in December that the tightening policy has run its course which indicates falling interest income in 2024. On the other hand, a lower federal fund rate may make loans more affordable and therefore boost demand. Considering that Goldman Sachs BDC is a seasoned investment manager with more than a decade experience investing in credit, I believe the BDC will be able to navigate a changing interest landscape in FY 2024.

Closing thoughts

Goldman Sachs BDC appears to be a solid investment for investors that are interested in generating recurring income or that follow a high-yield investment strategy. Although Goldman Sachs BDC has seen a decline in its portfolio value in FY 2023, the BDC is focused on first-liens and the BDC has good enough dividend coverage, based off of net investment income, to suggest that even a contraction in NII will not endanger the current $0.45 per-share quarterly dividend. The premium to NAV is only small and I see a 1.10X P/NAV ratio in the longer term as achievable.

For further details see:

Goldman Sachs BDC: An Attractive Income Buy With A 12% Yield