GSBD - Goldman Sachs BDC: Signs Of Structural Underperformance Going Forward

2023-12-27 01:42:32 ET

Summary

- Goldman Sachs BDC is a relatively large BDC with a market cap at around $1.7 billion, which for BDC universe is a significant figure.

- GSBD has a high exposure to first-lien debt and a relatively diversified portfolio across various industries. Almost 100% exposure to variable rate investments comes in handy as well.

- However, the quality of portfolio companies has deteriorated, with an increase in lower-rated investments, excessive leverage, and poor debt coverage metrics. The dividend coverage is also a concern.

- Given the current signs of worsening quality and low margin of safety in the context of dividend coverage, I would not consider GSBD a sound investment.

Goldman Sachs BDC (GSBD) is a relatively large-scale BDC, which as of December 2023 ranks as the tenth largest BDC vehicle in terms of the market cap.

GSBD invests primarily in US mid-cap companies (just as most BDCs), with an EBITDA generation of between $5 million and $75 million. The EBITDA range for this BDC is quite wide implying rather agnostic view on the size of these mid-cap businesses.

{kind=link}

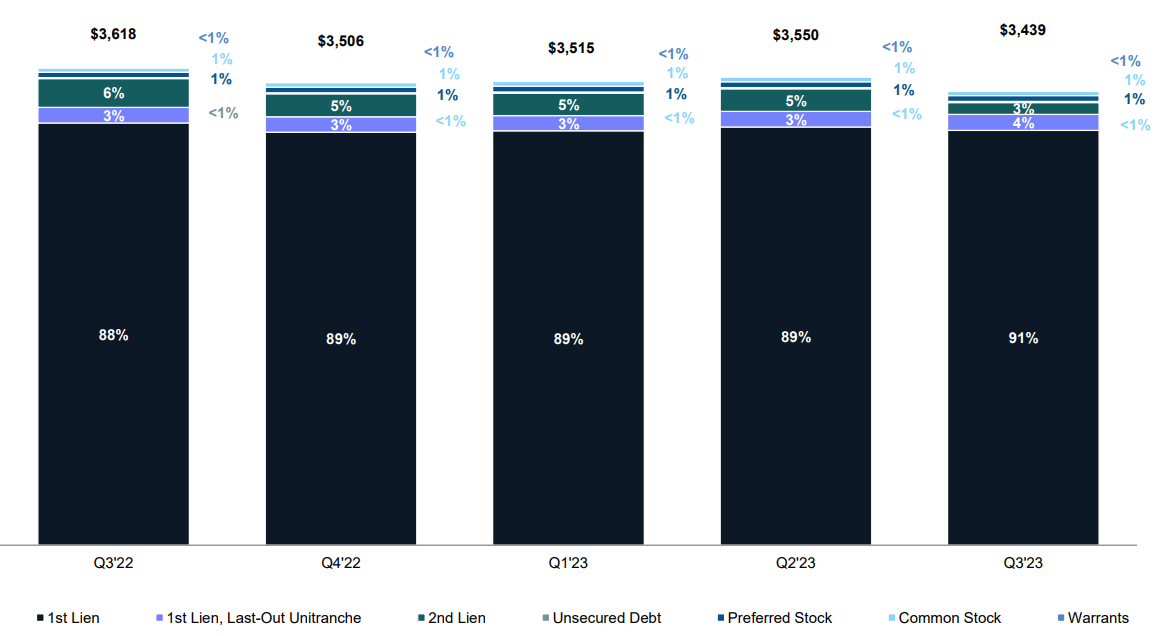

The exposure to the first lien debt has been stable and considerable already for a while, revolving around 90% territory. This kind of portion in first lien could be easily viewed as one of the greatest ones in the entire BDC space since the average lies somewhere between 70 - 80%.

GSBD Investor Presentation

In addition to the safeness that is associated with first lien structures, GSBD carries a relatively diversified portfolio, where the companies are nicely distributed across various industries.

From Top 3 industries, only one - i.e., software - embodies inherently more risky characteristics than an average industry, which tend to have stable and straightforward business models.

GSBD Investor Presentation

Moreover, almost the entire AuM base is comprised of floating instruments, which have definitely helped GSBD capitalize on the prevailing tailwinds associated with high interest rate environment. Plus, while interest rates are seemingly set to normalize (i.e., go lower) and thus there could be some yield reductions in GSBD's portfolio, in absolute terms the yields should still remain at very solid levels (unless SOFR drops to zero).

{kind=link}

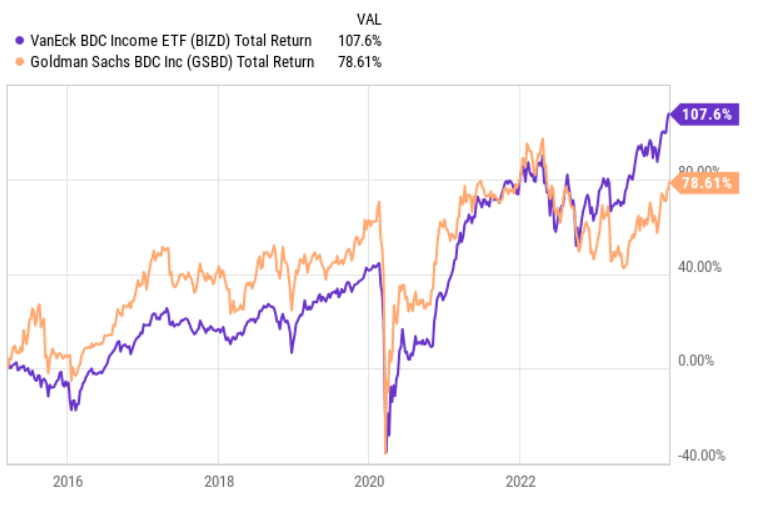

However, if we look at the total return chart above, we can notice very interesting dynamics:

- In the pre COVID period, once the interest rates were extremely accommodative, GSBD managed to consistently outperform the broader BDC index.

- Post COVID, GSBD has struggled to deliver alpha and really once the interest rates started to surge, the Fund has significantly diverged from the rest of BDC market.

I find this quite interesting given almost 100% exposure to floating rate instruments, which should theoretically allow GSBD to fully capture the current tailwinds warranting the alpha element (as in many instances BDCs still carry fixed rate investments).

Thesis

Let me know explain why this is the case and why I would not recommend owning GSBD at this moment.

In a nutshell, it is the combination of excessive leverage and relaxed standards with respect to investment underwriting.

The quality of portfolio companies has clearly deteriorated in the recent quarters. For example, the concentration of GSBD companies in third and fourth rating buckets has increased from 3.9% to 9% in just 9-month period.

{kind=link}

According to GSBD explanation , "rating 3" implies the following:

- Investment's risk has increased materially since origination or acquisition. Borrower may be out of compliance with debt covenants; however, payments are generally not more than 120 days past due.

"Rating 4" category is obviously even worse.

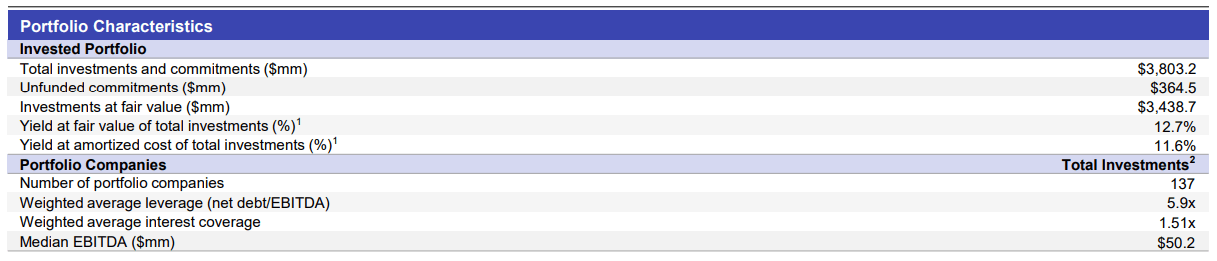

Looking at the portfolio characteristics below it should not be a huge surprise that we see worsening conditions within GSBD's portfolio.

{kind=link}

For example, the fact that weighted average interest coverage of all portfolio companies stands at only 1.51x indicates already there a significant risk in the overall structure. The net debt to EBITDA is also on the aggressive end with 5.9x as of Q3, 2023.

I should also underscore that the quality in relation to the debt and coverage metrics is not getting better either. The weighted average interest coverage of the companies at quarter end dropped from 1.56x to 1.51x as indicated above.

Now, while the leverage of GSBD has indeed improved, the prevailing levels are still skewed towards the aggressive end with debt to equity around 117%. This is slightly above the sector average .

Given the low margin of safety in portfolio companies that is associated with very narrow interest rate coverage ratios and high indebtedness, having aggressive leverage is not optimal.

As a natural consequence of the aforementioned situation, Tucker Greene - COO - commented on the increasing amount of non-accrual (as per the recent earnings call ):

And finally, turning to asset quality. As of September 30, 2023, two new positions were placed on non-accrual and one portfolio company was removed from non-accrual during Q3. Investments on non-accrual status amounted to 2.3% and 4.2% of the total investment portfolio at fair value and amortized cost respectively.

In the context of overall BDC space, 4.2% of non-accrual at amortized cost is very high.

{kind=link}

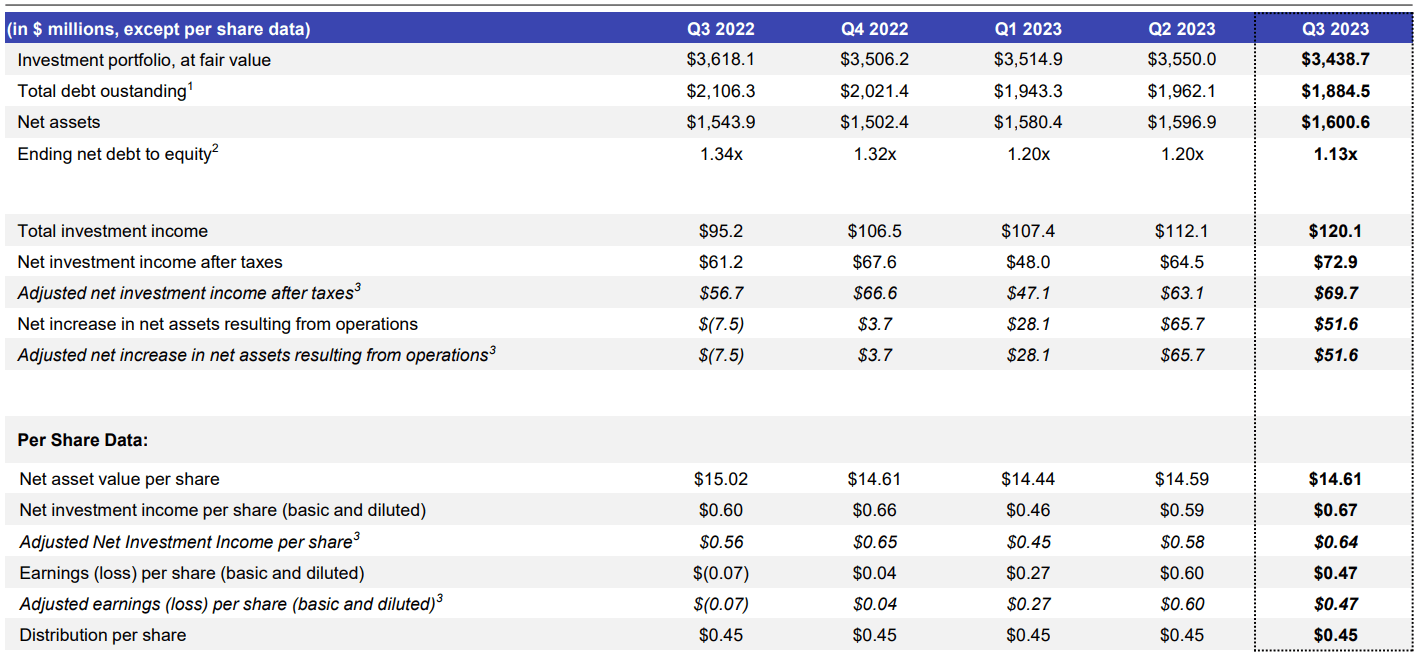

Finally, to make the matters worse, GSBD has recently experienced some struggles with the dividend coverage (i.e., in Q1, 2023, when the adjusted NII barely covered the underlying dividend because of more severe write-downs). On an adjusted earnings per share basis, the dividend coverage looks even more pessimistic.

While currently GSBD remains at a safe territory especially based on the Q3, 2023 data, it is also clear that as soon as more write-offs emerge, the sustainability of the dividend will become questioned.

The bottom line

GSBD has a sound portfolio structure in terms of the massive exposure to first lien and great industry diversification coupled with 100% floating investments, which make it easier to benefit from the high interest rate environment.

Nevertheless, the prevailing trend in portfolio quality, where an increasing amount of investments are classified under risky category and are written down make this BDC an unattractive investment. Excessive leverage and poor debt coverage metrics of portfolio companies could potentially magnify these consequences in the scenario of contracting economy.

The market seems to have already recognized this as since early 2022 GSBD is in a constant negative alpha territory. The fact that GSBD trades at a slight premium to NAV of 1.04x does not make this story better.

For further details see:

Goldman Sachs BDC: Signs Of Structural Underperformance Going Forward