IEI - Good News On U.S. Inflation Won't Prevent A July Rate Hike

2023-07-12 11:30:00 ET

Summary

- We have had a big surprise in the June consumer price inflation report with both headline and core (ex food and energy) rates rising.

- The Fed is focused on stamping out all inflation threats and is obsessed with services ex energy ex housing as they fear that this is where the tight jobs market will keep wage pressures elevated.

- This is certainly not enough to prevent a July rate hike given the Fed's current position, but suggests less need for the second hike it is currently indicating.

- The inflation backdrop should allow the Fed to respond to any recession threat with interest rate cuts next year.

CPI slows more sharply than expected

We have had a big surprise in the June consumer price inflation report with both headline and core (ex food and energy) rates rising 0.2% month-on-month rather than the 0.3% expected. In fact, it is even better than that as out to 3 decimal places it is 0.180% for headline and 0.158% for core. This means the annual rate of inflation slows to 3% from 4% for headline CPI while core has dropped to 4.8% from 5.3%. MoM readings of slightly under 0.2% MoM are exactly what we need to see to return annual inflation to 2% over time, so this is great news. However, it needs to happen consistently for the Federal Reserve to relax and is unlikely to deter the Fed from hiking policy rates another 25 basis points on 26 July.

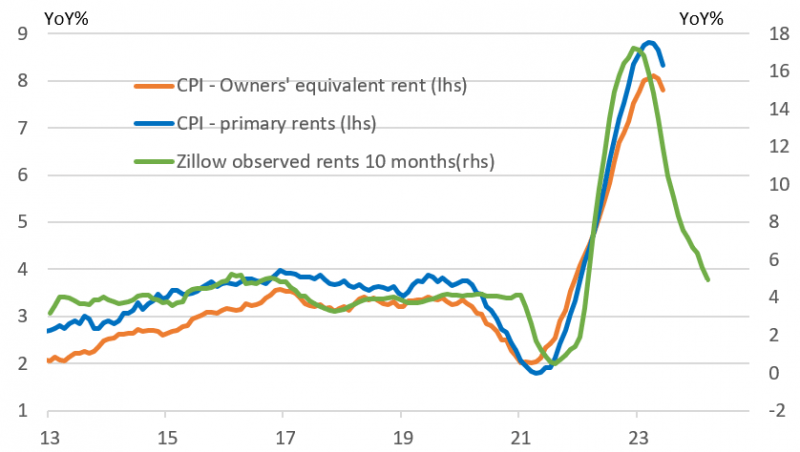

Looking at the details the main area of upward pressure remains housing costs with owners' equivalent rent rising 0.4% MoM and primary rent rising 0.5%. The good news is that we know that this will slow rapidly through the second half of 2023 given the lags with observed rents. The chart below hints at sub-4% CPI rent readings before the end of the year versus the current 8% inflation rates.

Housing CPI components will slow sharply (YoY%)

{kind=link}

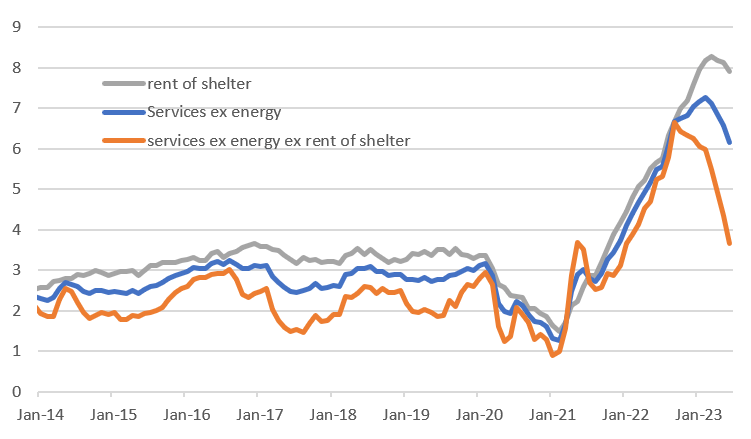

Core services ex housing offers real encouragement

Outside of housing everything else was soft with only apparel (+0.3%) and gasoline (+1%) amongst the major sub components coming in above 0.2% MoM. Food, recreation and commodities all rose just 0.1%. New vehicles and medical care were 0%, used vehicles were down 0.5% and airline fares fell 8.1%.

The Fed is focused on stamping out all inflation threats and is obsessed with services ex energy ex housing as they fear that this is where the tight jobs market will keep wage pressures elevated. Given labour costs are the biggest input to businesses in this sector and demand for these services remains pretty strong, this could keep price pressures elevated for longer. However, we got a sub 0.2% MoM reading for this with the year-on-year rate slowing to 3.7% from 6.6% last September.

Core CPI services ex housing should please the Fed (YoY%)

{kind=link}

Another tick higher before renewed falls in annual inflation

Unfortunately over the next couple of months we are likely to see headline annual inflation rise again, albeit modestly. This will largely reflect the fact that 0% and 0.2% MoM readings from July and August last year will drop out of the annual comparison. Core inflation won't have this problem as we saw 0.3% and 0.6% prints for the same periods last year, making it more likely that the annual core rate of inflation will continue to slow through July and August.

Moreover, with housing set to slow sharply based on observed rents and used car prices set to fall further based on auction prices we are increasingly confident of a sub 3.5% YoY core CPI print by year-end while headline inflation could be around 2.5%. This is certainly not enough to prevent a July rate hike given the Fed's current position, but suggests less need for the second hike it is currently indicating.

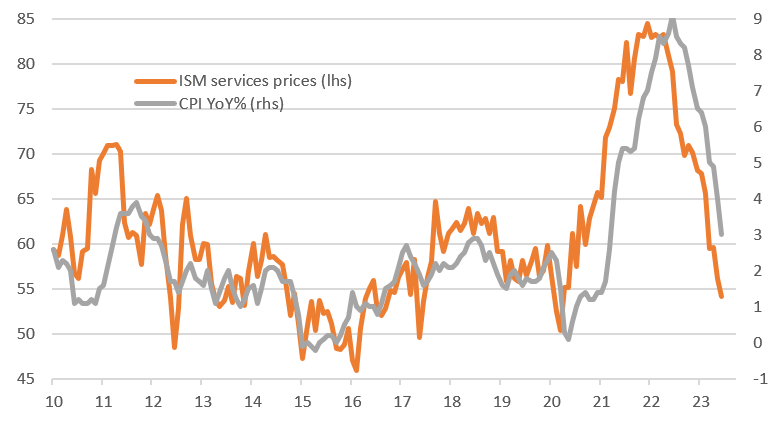

ISM services prices paid points to further sharp falls in inflation

{kind=link}

Moreover, with business surveys pointing to weakening pricing power, such as the ISM services index being consistent with 1% headline CPI, the inflation backdrop should allow the Fed to respond to any recession threat with interest rate cuts next year.

Content Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Good News On U.S. Inflation Won't Prevent A July Rate Hike