IXP - Google: The Market Is Wrong

- Google’s advertising business is showing robust growth despite a feared slowdown in the ad market.

- Google’s Cloud business is also growing strongly, now has a 9% revenue share.

- TikTok is becoming a challenge for YouTube ad revenue growth.

- Google's significant free cash flow stabilizes the stock. Google is massively undervalued based off of FCF.

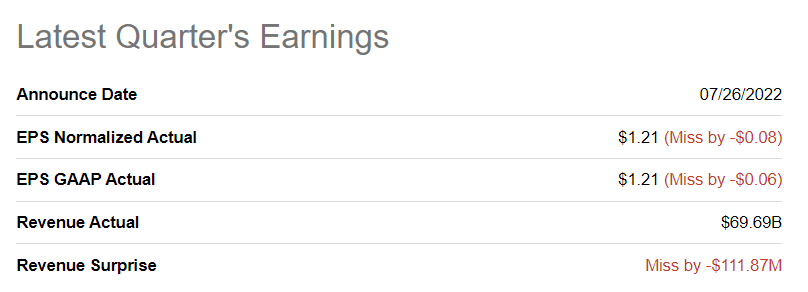

Despite missing analyst estimates for the second-quarter, Alphabet Inc.'s ( GOOG , [[GOOGL]]) ("Google") advertising business held up well in Q2’22 and didn’t experience a Snap Inc. ( SNAP )-like blowout, which some investors feared before earnings. While missing predictions slightly, Google’s performance was not bad at all: with reasonable strength in the search and the cloud business, Google once again demonstrated that it can generate a ton of free cash flow for the company and its shareholders!

Google’s Search/Advertising business keeps growing

The market is still under the influence of Snap’s disastrous earnings report from last week. Snap saw its stock price crater 39% after submitting its second-quarter earnings sheet that indicated a worse-than-expected downturn in the digital advertising market as well as growing competitive pressures from rival companies such as TikTok.

Google, however, presented much better Q2’22 earnings than Snap. The internet search giant achieved EPS of $1.21 on revenues of $69.69B, but slightly missed predictions on both numbers.

Seeking Alpha - Google Q2'22 Earnings

{kind=link}

The EPS and revenue misses were relatively minor and should not affect how investors see Google’s strong core businesses, especially Google Search.

Google’s Q2’22 revenues were $69.69B, showing 13% growth year over year, largely because of two businesses: Google Search and Google Cloud. Google Search, which is Google’s most important business regarding revenue and profit contribution, generated $40.69B in revenues in the second-quarter, showing 14% year over year growth. Although Google’s Q2’22 revenues grew at their slowest rate in two years, the Search business continued to perform well. Concerns over a slowdown in the digital advertising market created an overhang in Google stock before earnings, and the market may now begin to realize that Google will keep expanding its Search/Advertising business despite moderating topline growth.

Google’s Cloud business, which is the fastest growing segment within the technology firm, saw its revenues increase 36% year over year to a record $6.28B. Because of accelerating cloud platform adoption by the firm’s corporate clients, Google’s Cloud business now has a 9% revenue share compared to a 5% share three years ago. Google’s Cloud business is in an upswing , and investors can expect this segment to continue to generate the fastest growth rate within Google going forward. I estimate that Google Cloud will grow to a 14-15% revenue share by FY 2025 and it is by far the most promising business for Google right now.

|

|

| Q2'21 |

| Q2'22 |

| Y/Y Growth |

| Revenue Share (Q2’22) |

| Google Search & other |

| $35,845 |

| $40,689 |

| 13.51% |

| 58.39% |

| YouTube Ads |

| $7,002 |

| $7,340 |

| 4.83% |

| 10.53% |

| Google Network |

| $7,597 |

| $8,259 |

| 8.71% |

| 11.85% |

| Google Other |

| $6,623 |

| $6,553 |

| -1.06% |

| 9.40% |

| Google Cloud |

| $4,628 |

| $6,276 |

| 35.61% |

| 9.01% |

| Other Bets |

| $192 |

| $193 |

| 0.52% |

| 0.28% |

| Hedging |

| ($7) |

| $375 |

| - |

| 0.54% |

| Total revenues |

| $61,880 |

| $69,685 |

| 12.61% |

| 100.00% |

(Source: Author)

Ad revenue growth is slowing at YouTube

TikTok has emerged as the next hot social media platform, and it is extremely popular with younger users. The growing popularity of TikTok, in part, was to blame for Snap’s monetization problems in the second quarter, and YouTube is also seeing a deceleration in ad revenue growth. YouTube ads generated just 5% year-over-year growth in Q2’22 chiefly due to growing competition from other short video streaming platforms. Revenues generated from running ads on the YouTube platform increased at a 14% rate in Q1’22 and at an 84% rate in Q2’22 due to a pandemic boost. The slowdown in YouTube ad revenue growth creates a challenge for Google, but it is not such a material problem that it would speak against owning Google stock.

Free cash flow

What I love about Google is the firm’s massive free cash flow ("FCF"). In Q2’22, Google generated $12.59B in free cash, which calculates to a FCF margin of 18.1%. Although Google’s FCF margin dropped quarter-over-quarter, the enormous size of free cash flow Google’s businesses generate will continue to support large-scale stock buybacks.

|

|

| Q2'21 |

| Q3'21 |

| Q4'21 |

| Q1'22 |

| Q2'22 |

| Revenues |

| $61,880 |

| $65,118 |

| $75,325 |

| $68,011 |

| $69,685 |

| Net cash provided by operating activities |

| $21,890 |

| $25,539 |

| $24,934 |

| $25,106 |

| $19,422 |

| Less: purchases of property and equipment |

| ($5,496) |

| ($6,819) |

| ($6,383) |

| ($9,786) |

| ($6,828) |

| Free cash flow |

| $16,394 |

| $18,720 |

| $18,551 |

| $15,320 |

| $12,594 |

| Free cash flow margin |

| 26.5% |

| 28.7% |

| 24.6% |

| 22.5% |

| 18.1% |

(Source: Author)

Alphabet is expected to have revenues of $334.15B in FY 2023. Applying a 20% FCF margin to this revenue base yields $66.83B in free cash flow. Based off of a market value of $1.39T, shares of Google have a P-FCF ratio of 21 X. Considering that Google is the dominant force in the search market and that FCF margins are very high, Google is an exceptionally good deal for growth investors.

Risks with Google

Google delivered solid earnings for the second-quarter, despite an EPS miss, and fears over a slowdown in the advertising business are exaggerated. What is more of a challenge to Google, and YouTube especially, is the rise of TikTok as an alternative advertiser platform which is attracting a younger demographic. For that reason, YouTube may continue to see a slowdown in ad revenue growth going forward, which would also impact Google's top line prospects.

Final thoughts

The market is wrong about Google and the firm's second-quarter earnings card proved it: The ad market is holding up and the search giant continued to generate a ton of free cash flow in Q2’22. Google’s Search and Cloud showed reasonable growth, despite growing economic headwinds. Since Google’s free cash flow remained strong and the valuation factor remains cheap at 21 X. Google stock continues to have a risk profile that is very much skewed to the upside!

For further details see:

Google: The Market Is Wrong