EPAC - Graham Corporation: A Solid Prospect On Improved Results And Attractive Growth Potential

2023-12-20 09:47:14 ET

Summary

- Graham Corporation, a producer of mission-critical fluid, power, heat transfer, and vacuum technologies, is a small company with potential for investors.

- The company has shown impressive revenue growth in recent years, driven by acquisitions and organic growth.

- With a positive outlook for the future, including expected revenue of over $200 million by 2027, Graham Corporation stock is a solid investment opportunity.

From my experience, some of the smallest companies offer up some of the best opportunities for investors. And very few companies out there have a market capitalization of less than $200 million. One such firm that I believe warrants the attention of investors is Graham Corporation ( GHM ). In recent years, management has done a pretty good job of growing the company's top line. Bottom line results have, unfortunately, been rather mixed. But this year, which is the 2024 fiscal year for the enterprise, has seen some meaningful improvements on that front. Add on top of this a recent acquisition and management's target for the next few years, and I would argue that the company, while not necessarily the greatest prospect on the market, definitely deserves a solid ‘buy’ rating at this time.

Understanding Graham

According to the management team at Graham, the company operates as a producer and seller of mission critical fluid, power, heat transfer, and vacuum technologies. In addition to being used in the process industries, such as the chemical and petrochemical markets, its technologies are also used in the defense, space, and energy markets. Of course, this is a rather vague description of the company. A bit of a dive into it and what specifically its offerings are used for would be valuable for those who have not read about the company previously.

In the chemical and petrochemical processing market, the company produces Liquid ring pumps, heat exchangers, nozzles, ejectors, and other related devices that go into the construction of heat transfer and vacuum systems. Those same devices also create heat transfer and vacuum systems for the energy market. The company produces turbines, generators, compressors, and pumps, which are used in power generation systems and thermal management systems for the energy space. Its fuel pumps, blowers, fans, and turbopumps, are used in the space industry for the production of rocket propulsion systems, cooling systems, and even life support systems. And in the defense market, it produces alternators, regulators, pumps, drive electronics, ejectors, and more that go into certain power plant systems, torpedo systems, and more.

{kind=link}

Author - SEC EDGAR Data

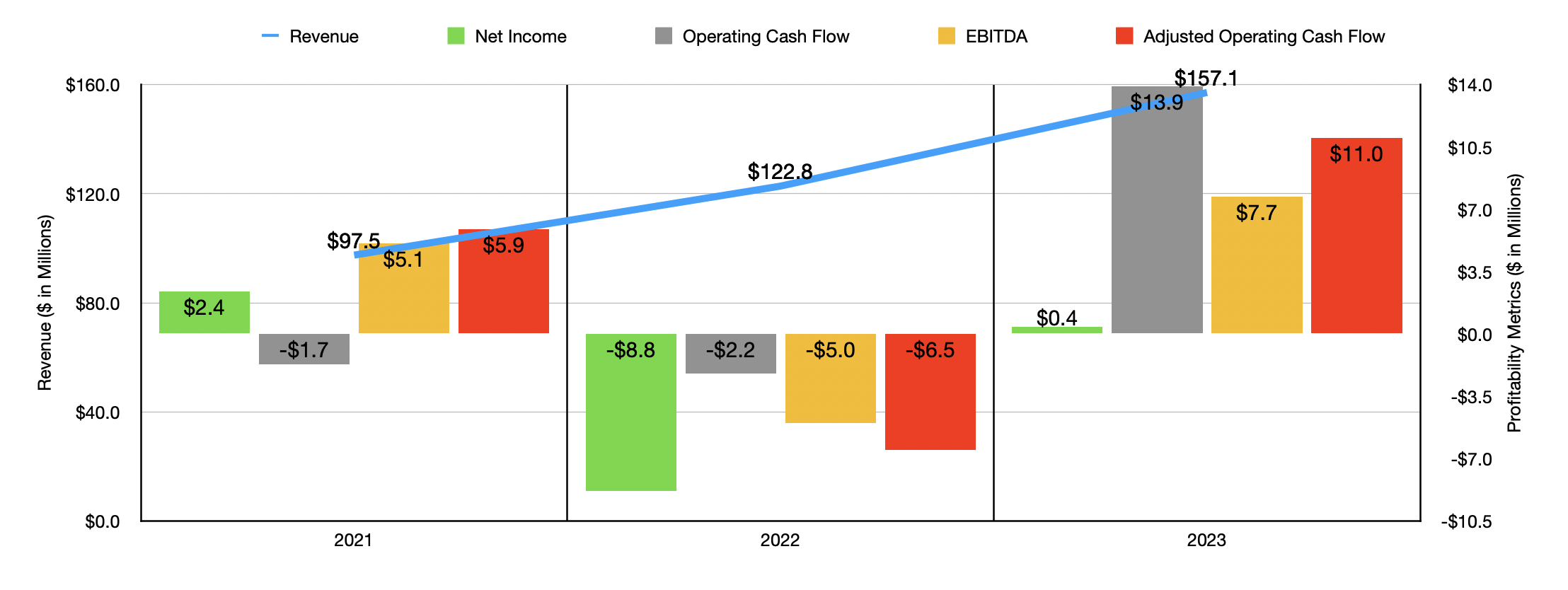

Over the past few years, management has done a fantastic job of growing the company's top line. Revenue has gone from $97.5 million in 2021 to $157.1 million in 2023. Over this window of time, the company has benefited from acquisitions, as well as growth in aftermarket sales to the refining and petrochemical markets thanks to a pickup in energy production. The commercial space market and the defense market also reported attractive growth over this window of time. However, not everything has been great. In April of this year, Virgin Orbit Holdings entered into Chapter 11 bankruptcy. About $5.3 million of the company’s revenue this year came from that enterprise and management had to mark reserves of about $2.5 million regarding accounts receivable and inventory associated with that company. They also had to cross off the list $4 million worth of purchase orders.

On the bottom line, the picture has been much more volatile. As the first chart in this article illustrates, net income has been all over the map. The same is true of the cash flow figures for the company, with 2022 being a particularly unpleasant year. The good news is that the 2023 fiscal year was the best in most respects. Operating cash flow hit $13.9 million. If we adjust for changes in working capital, we get a reading of $11 million. Meanwhile, EBITDA for the company stood at $7.7 million.

{kind=link}

Author - SEC EDGAR Data

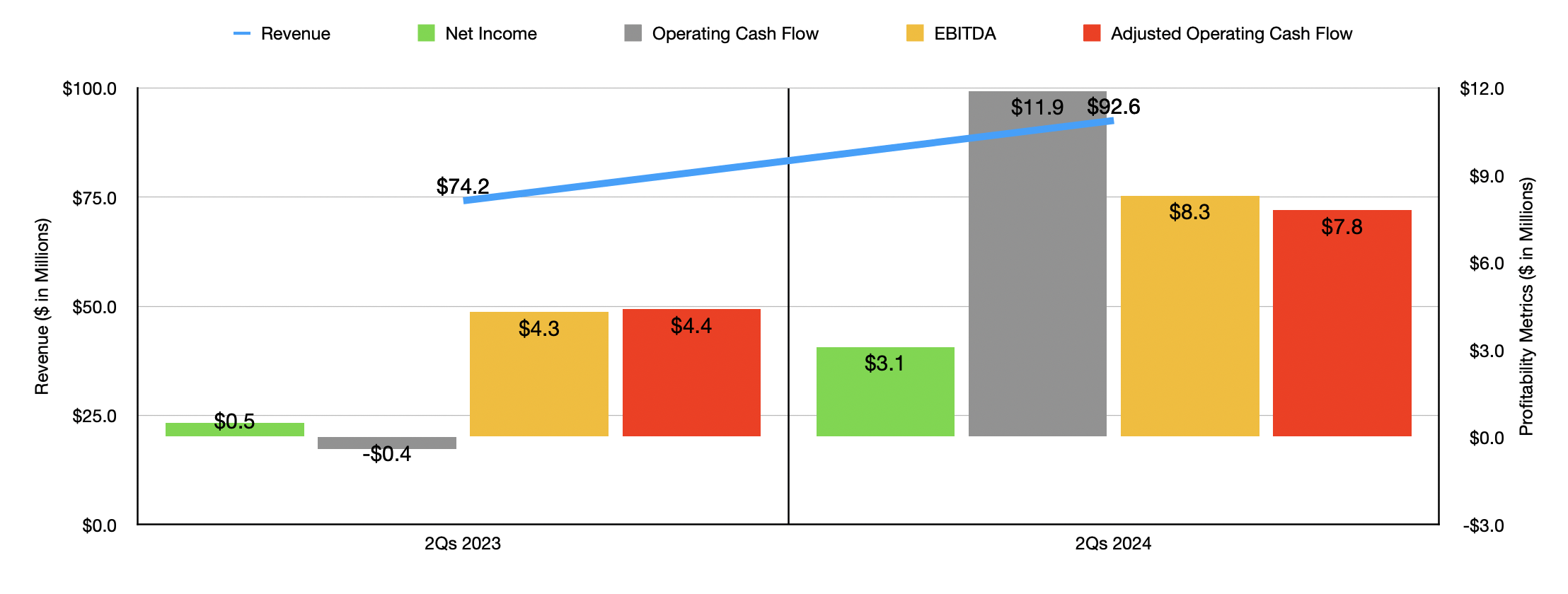

When it comes to the 2024 fiscal year that we are now in, the picture looks even better. Robust demand in the defense segment, combined with higher aftermarket sales associated with the chemical and petrochemical markets, have been key drivers in pushing revenue from $74.2 million in the first half of the 2023 fiscal year to $92.6 million the same time for 2024. This jump in revenue brought with it a rise in net profits from $0.5 million to $3.1 million. As the chart above illustrates, the cash flow metrics for the company have also come in far stronger. It's important to note that, for 2024 in its entirety, management is expecting revenue of between $170 million and $180 million, with EBITDA likely to come in at between $11.5 million and $13.5 million. No estimates were given when it came to other profitability metrics. But according to my estimate, adjusted operating cash flow should be around $17.9 million for the year.

{kind=link}

Author - SEC EDGAR Data

This gives us the ability to easily value the company. In the chart above, you can see how shares are priced using data from 2023 and forward estimates for 2024. The stock looks substantially cheaper on a forward basis than it does using data from 2023. I then compared the company to five similar firms as shown in the table below. On a price to operating cash flow basis, two of the five ended up being cheaper than our prospect. This drops to one of the five when we use the EV to EBITDA approach.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Graham Corporation |

| 10.7 |

| 9.9 |

| L.B. Foster Co. ( FSTR ) |

| 9.2 |

| 18.1 |

| NN Inc. ( NNBR ) |

| 4.0 |

| 12.4 |

| Enerpac Tool Group ( EPAC ) |

| 20.9 |

| 16.5 |

| Tennant Company ( TNC ) |

| 11.9 |

| 9.2 |

| Barnes Group ( B ) |

| 14.2 |

| 14.3 |

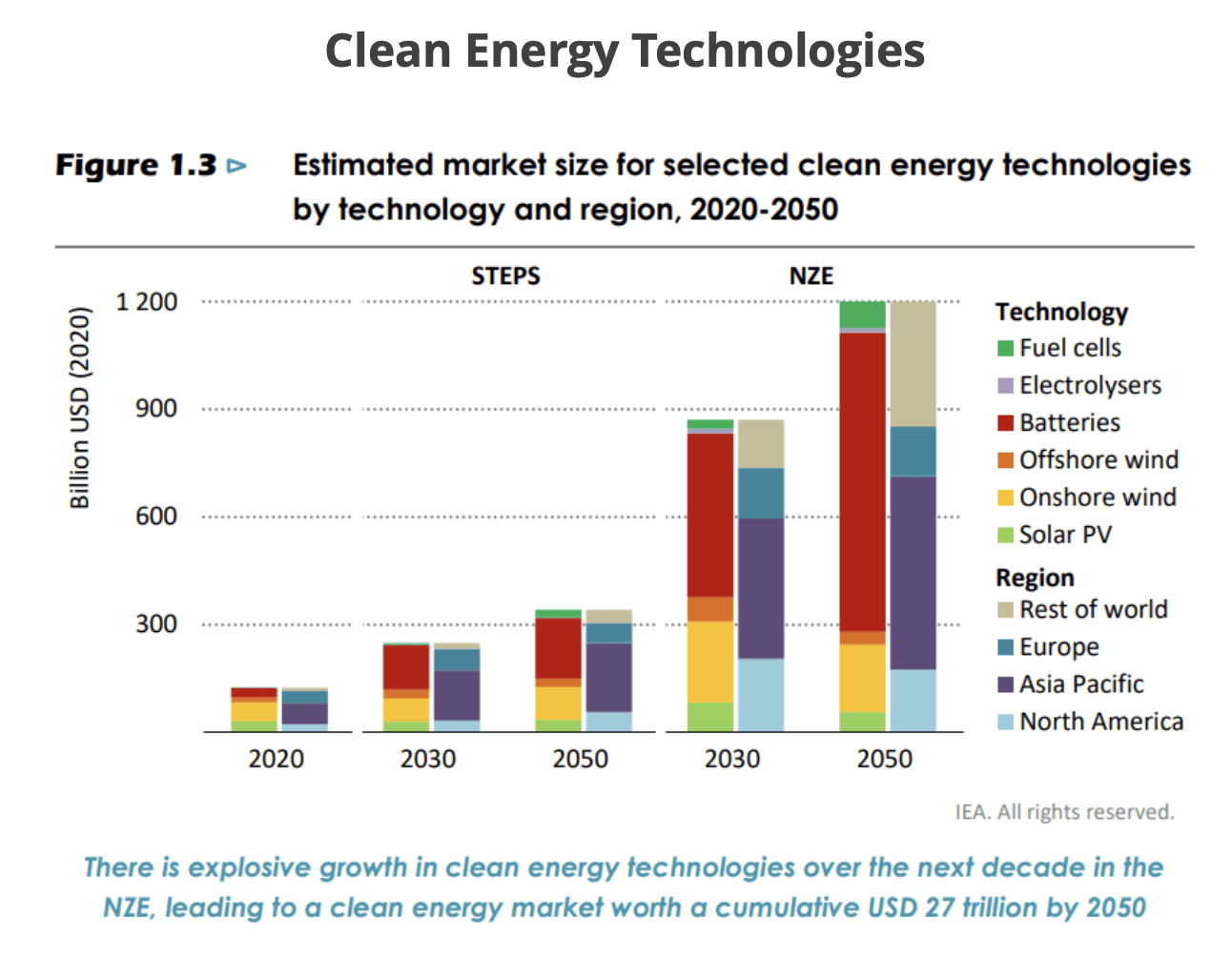

When we look at the longer term picture, we end up with a positive outlook for the company. Management expects, for instance, for revenue to be in excess of $200 million by 2027. Some of this growth should be driven by rapid expansion in some of the markets in which the company operates. The global space economy, for instance, is expected to continue growing at a rather rapid pace for the next several years. Growth should particularly begin to accelerate toward the end of this decade. But even so, as the image below illustrates, expansion should be the name of the game regardless. And when it comes to clean energy technologies, the expectation is for investments to grow to just shy of $300 billion by 2030 compared to less than $150 billion per year back in 2020. In fact, from 2020 through 2050, it's believed that total global spending on the clean energy market will come in at around $27 trillion.

{kind=link}

Graham Corporation

In addition to growing organically, Graham has also been focused on growing by means of acquisition. In early November, for instance, the company announced that it was acquiring P3 Technologies, Producer of propulsion products, pumps, and other fluid flow technologies that provides its products for the aerospace market, industrial markets, new technology markets, and even the medical space. Management has not disclosed the purchase price of that business. But they did say that there was a stock component that involved the issuance of about $2 million worth of units. Annual revenue associated with P3 Technologies is $6 million, and the company brings with it $8 million in backlog. Small nuts and bolts purchases like this can go a long way toward achieving attractive growth, especially if the terms of the transactions are right.

{kind=link}

Graham Corporation

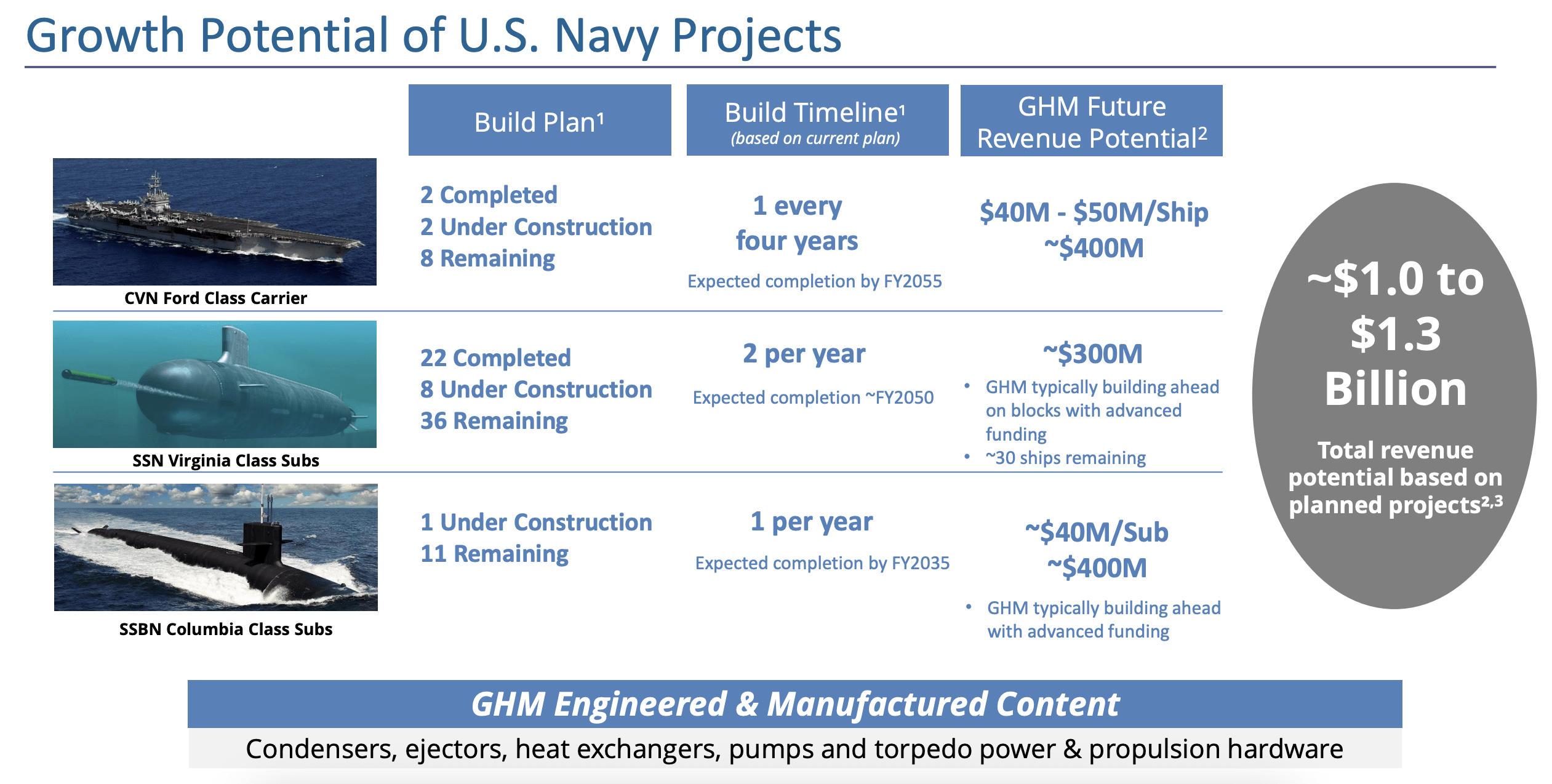

The company also has growth potential from some very interesting initiatives. For instance, there are some projects that are being planned by the U.S. Navy that involve the construction of major war ships and submarines. Although some of this revenue might not be available until as late as 2055, the total size of the opportunity that management estimates that it can capture between now and then is between $1 billion and $1.3 billion. For a company of its size, this is material, even spread across a couple of decades.

Takeaway

Generally when I invest, I prefer companies with a market capitalization of $1 billion or more. That's because they tend to be more stable and they offer lower levels of risk. But every so often, a rather small prospect will come across my radar that I become interested in. Based on the data provided, I would make the case that Graham is definitely an interesting prospect for investors who don't mind small firms. The company's track record is impressive, particularly when it comes to revenue. Shares are attractively priced on a forward basis and the company has cash that exceeds debt in the amount of $14.8 million. All of these factors combined have led me to rate it a ‘buy’ at this time.

For further details see:

Graham Corporation: A Solid Prospect On Improved Results And Attractive Growth Potential