GHC - Graham Holdings Company: Good Business Culture Poor Business Execution

2023-10-16 12:23:00 ET

Summary

- Graham Holdings Company has a long history of business success due to its ability to successfully pivot its business in big ways.

- However, the current management team has demonstrated less ability to allocate capital effectively. On top of this, I think the company has a relatively low-quality portfolio of businesses.

- I would prefer to invest in the business at 10x my estimate of the current two-year average of free cash flow per share, or $490.

- In this article, I will discuss my thought process behind this price target, and provide an overview of the company's past decade of operations.

Graham Holdings Company ( GHC ) has a long history of business success despite going through many transformations that have changed the way the company looks. The company’s longevity alone is remarkable, but coupled with the fact that it has pivoted its business in big ways along the way makes it all the more impressive. Part of the reason for this success is the company’s deep rooted culture that stems from its association with Warren Buffett and Berkshire Hathaway Inc. ( BRK.A ). Buffett consulted Katherine Graham, the previous CEO of The Washington Post which eventually became Graham Holdings when the Post was sold in 2013 to Jeff Bezos, on the business due to Berkshire Hathaway’s stake in the company. Many of Buffett’s business culture principals became ingrained in the business due to his association with the company.

These principals are still deeply rooted in the company which is a good thing for shareholders. However despite having these principals, the current management team doesn’t have Buffett’s or Berkshire’s capital allocation ability. On top of this, the largest businesses in Graham Holding’s portfolio are not high quality. Low quality businesses coupled with low quality capital allocation is not a recipe for long-term success.

Graham’s earnings are generally lumpy due to the cyclicality of political advertising which significantly increases earnings during election years. To get a better sense of overall earnings power, it is better to take an average of earnings in and out of those years. Additionally, free cash flow is a better way to estimate the economics of the entire company because of large non-cash expenses relating to amortization of intangibles. I estimate that Graham’s current two year average free cash flow per share is about $49, which puts its stock currently at 12x free cash flow.

The stock does not trade like most publicly traded stocks in the U.S. as the shareholder base is much more long-term oriented and management doesn’t provide quarterly or yearly guidance. This makes it less volatile around earnings and less prone to large swings with multiple expansion and contraction. Investors should invest in Graham only if they believe it is trading at a discount to their estimate of intrinsic value or if the free cash flow yield is adequate for their hurdle rate. Graham’s status as a serial acquirer and its diversified operations makes it difficult to predict future cash flows which makes utilization of a free cash flow yield more appealing to me.

With its current operations, I would prefer to invest in the business closer to 10x free cash flow, or $490. In this report, I will discuss why I think this is the case and I will provide some background on the business and its past financials in order to frame my thought process.

Business Overview

Graham has a long history of operations that have changed greatly over time. The following are its major acquisition, divestitures and general changes over the past decade:

- Graham sold The Washington Post to Jeff Bezos in 2013. With this sale, the company sold all of its office space and land associated with the Post.

- Started process to spin off Cable ONE, its cable segment, to shareholders in 2014. This decision was made due to upcoming challenges in the cable industry that would require high focus and a large number of investments. It was determined to be in the best interest of Graham shareholders to divest the business so the parent company could focus on its other more capital light businesses.

- In 2014, Graham traded most of its stake in Berkshire Hathaway, plus cash, plus a television station to Berkshire for Berkshire’s stake in Graham Holdings. Graham subsequently retired the shares they received from Berkshire.

- Graham acquired Joyce/Dayton Corp, a manufacturer of screw jacks and other linear motion systems, in 2014.

- In 2015, Don Graham transitions from CEO role and his son-in-law Tim O’Shaughnessy takes over.

- Graham acquires Dekko, a manufacturer of electrical solutions for uses in workspace power solutions, architectural lighting, and electrical components and assemblies, in 2015.

- Graham acquired two broadcast television stations in 2016, one in VA and one in FL.

- Graham combined Celtic and Residential Healthcare, its healthcare company operations, into one in 2016 in order to make operations more efficient.

- Graham acquired a set of sixth-form schools in the U.K. in 2016.

- In 2017, Graham sold Kaplan University to Purdue University and signed a long-term servicing agreement to assist Purdue with operations.

- In 2017, Graham Media Group (GMG) started to expand beyond traditional broadcasting to more online operations in order to diversify the segment’s earnings streams.

- Graham acquired Hoover Treated Wood Products in 2017.

- Graham entered the auto dealership business in 2018 through a partnership with Chris Ourisman to acquire two dealerships in DC area.

- Graham entered restaurant industry with acquisition of Clyde Restaurant Group in 2019.

- Graham acquired an additional auto dealership in 2019.

- Graham acquired Frambridge, a custom frame retailer, in 2020. This was more of a start-up stage company at the time of the acquisitions.

- Graham acquired Leaf Group in 2021. Leaf Group is a consumer internet company that creates brands.

- Graham acquired two additional auto dealerships in 2022.

- Three bolt-on acquisitions were made for Graham Healthcare Group ((GHG)) in 2022.

- Graham acquired an additional car dealership through its partnership with Ourisman Automotive.

There have been many small acquisitions in the past decade but the main drivers of the business have been the education, media and healthcare segments. With many years of financials from these segments, investors can determine the quality of these businesses but the capital allocation over the past decade, and especially since Tim O’Shaughnessy took over, has looked a bit different than what it was previously.

The 2015 annual letter, the first one with O’Shaughnessy as CEO, outlines his plan to invest in more technology businesses due to it being within his circle of competence. Determining a premium to free cash flow is dependent on the quality of capital allocation going forward which makes it important to track capital allocation. If returns on acquisitions and invested capital are sustainably high, the stock deserves a premium.

Past Financial Results

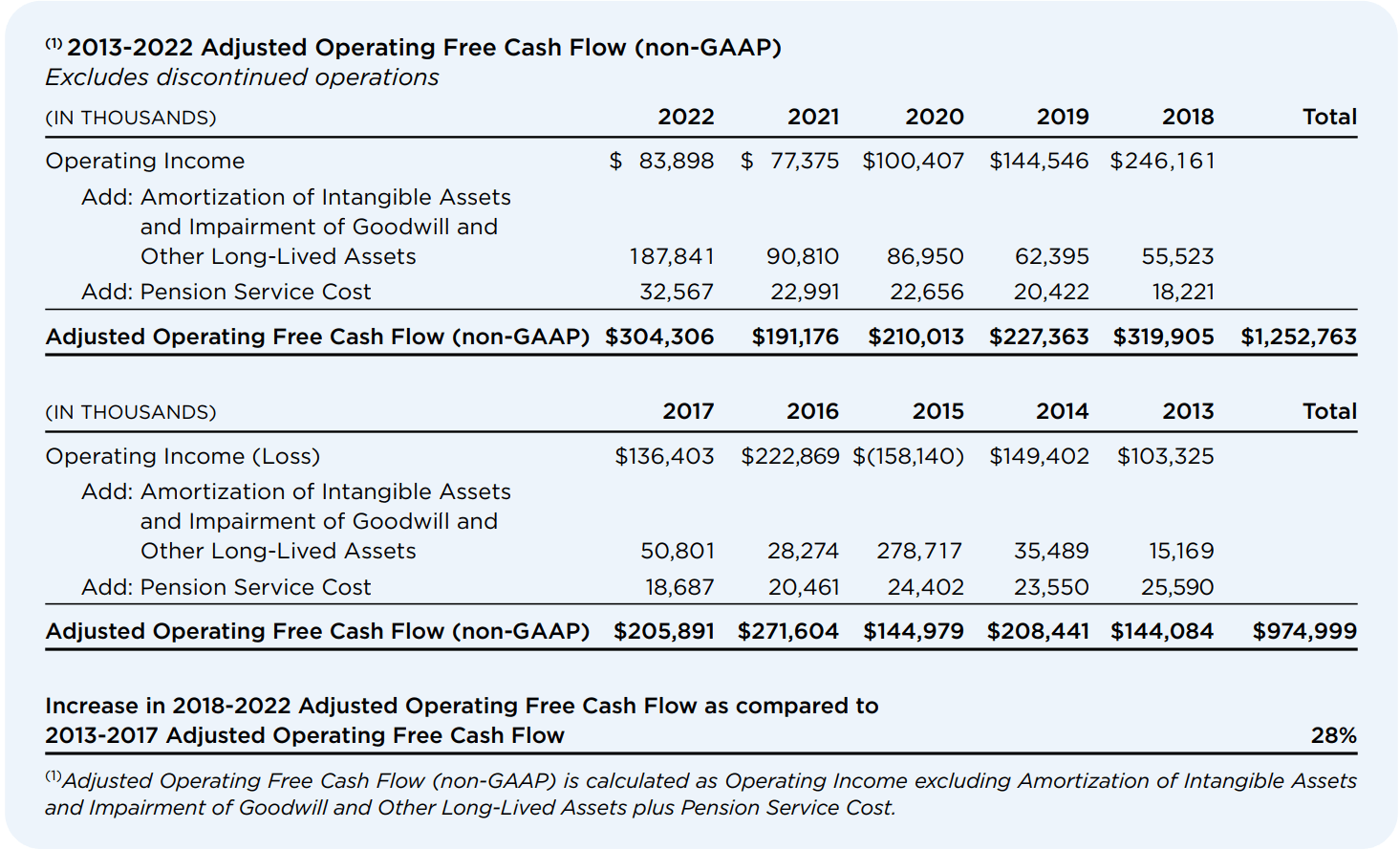

Graham’s operating results over the past decade have been lumpy as a result of its many acquisitions and divestitures. Management recently mentioned its long-term growth in adjusted operating cash flow as defined by operating income plus amortization of intangibles and pension servicing costs to show that the company is growing despite any year-to-year lumpiness.

Graham Holdings Company Reported Adjusted Operating Cash Flow (Graham 2022 Annual Report)

{kind=link}

Yet growth in and of itself is not always a good thing. If the growth is generated through smart investments and acquisitions that provide high returns, it is a good thing. This makes management’s skill at allocating capital extremely important, especially for a serial acquirer like Graham Holdings that doesn't run extremely high quality businesses. A look at the company’s returns on invested capital, including investments in acquisitions, since Tim O’Shaughnessy became CEO shows that management has not been very skilled at capital allocation.

{kind=link}

Graham’s ROIC shows that the company's investments are not generating high returns. The growth in invested capital is from a combination of capital intensity from the education segment, and growth in intangible assets due to acquisitions. The sustainability of this ROIC is an important factor when determining the proper multiple of free cash flow to pay for the business.

As a note, the adjusted free cash flow calculations above do not include changes in working capital or taxes paid. This is done in order to smooth out free cash flow to make each year more comparable to each other.

Valuation and Price Target

Graham’s earnings volatility primarily stems from its media segment which houses various local television broadcasting stations. During election years, political advertising spending is much higher which adds around 20-30% in operating income to the segment during election years. Because of this, it is best to take an average of election and non-election years to get a better sense of the earnings power of the entire business.

Based on extrapolated H1 2023 financial results, I estimate that free cash flow for the full year 2023 will be about $197 million. To this, I am adding $16.5m as an estimate for Graham’s share of free cash flow from its partial ownership of businesses in its stock portfolio, which puts total free cash flow at $213.5m.

For an estimate of 2024 free cash flow, I will assume no growth in the other segments, and I will add $40 million of operating income for the election year bump in earnings. Assuming a 25.6% tax rate (the same as H1 2023), and the same capital expenditures when compared to 2023, I estimate full year 2024 free cash flow is $227 million. Adding an additional $16.5m for its equity portfolio, my estimate of 2024 free cash flow is $243.5m.

Taking the average of the two years and dividing by the current fully diluted share count of 4.7 million, I estimate that Graham’s current collection of businesses generate free cash flow per share of about $49. This means the stock is currently trading at about 12x the current company’s free cash flow.

The multiple to free cash flow per share that an investor is willing to pay should take organic earnings growth, returns on future acquisitions, and returns on incrementally invested capital into account. Given the average to low quality nature of the current collection of businesses, current management’s poor acquisition decisions in recent years (they recently took a $128 million goodwill impairment for their acquisition of Leaf Group), and the high capital intensity of Kaplan in recent years, I would feel comfortable paying 10x free cash flow. This would put the stock at $490, or about 16% lower than its current price.

Final Thoughts

I think that many of Graham’s current shareholders enjoy the culture of the company that shares many of the same philosophies as Buffett’s Berkshire Hathaway. While this culture may lead to some investors paying a premium for the stock as the current management team returns capital to shareholders and is very open about the mistakes it makes, it does not make up for poor capital allocation.

I estimate that the company as is generates ~$49 per share of free cash flow. I would not pay more than 10x this figure as the current management has recently shown a lack of skill in capital allocation for both capital investments and acquisitions.

For further details see:

Graham Holdings Company: Good Business Culture, Poor Business Execution