LGMMY - Grand City Properties: A Value Play In The German Real Estate Market

2023-11-06 10:44:53 ET

Summary

- Like the whole German real estate sector, Grand City Properties shares have decreased significantly since last year.

- GCP has better debt metrics and a lower valuation than larger peers like Vonovia.

- While the sector has recovered partially since summer, Grand City Properties shares have lagged.

- This makes GCP a Strong Buy for investors who can wait for interest rates to go down again.

(Note: All amounts in the article are in EUR. At the current exchange rate, 1 EUR is around 1.07 USD.)

Investment thesis

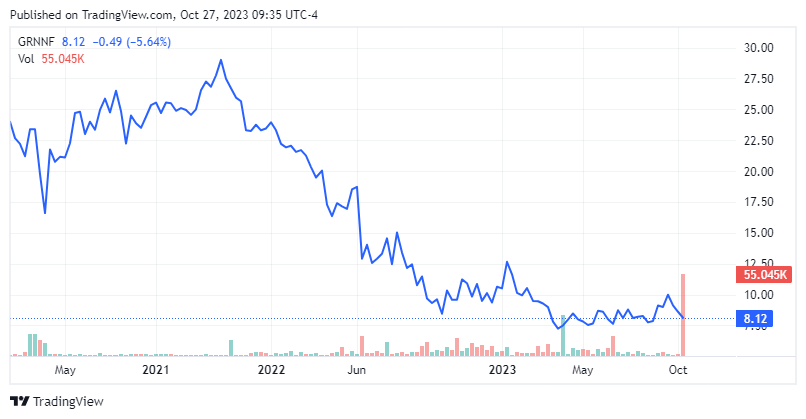

Grand City Properties ( OTCPK:GRNNF , OTCPK:GRDDY ) is a specialist German real estate company focused on investing in and managing residential apartments. In line with the whole German real estate sector, shares have seen a significant depreciation since last year.

Grand City Properties share price (Source: Seeking Alpha)

{kind=link}

I have been buying German residential real estate companies since early summer because I thought they had been oversold. I have described the approach in a recent Seeking Alpha article on Vonovia ( OTCPK:VONOY ) ( OTCPK:VNNVF ), where I gave a Buy recommendation. While Vonovia was already up significantly from its lows in 2022, I argued that there is much more upward potential due to macroeconomic tailwinds. Those tailwinds are coming from a severe supply/demand mismatch in the German residential real estate market, which will get even worse over the next years, and increasing rents that are still lagging behind inflation.

These arguments apply for Grand City Properties as they do for Vonovia, except that Grand City Properties shares are still closer to their lows, despite better debt metrics and a strong operational performance. That makes Grand City Properties a Strong Buy, in my view – and this is also the first time I am putting forward such a Strong Buy recommendation in a Seeking Alpha article. I have a high conviction that Grand City Properties can go up 50-100% once the interest rate environment turns.

Having said that, I also want to point out that Grand City Properties is a relatively small company. While Vonovia is part of the German DAX index and has a market cap of now almost 20bn euros, Grand City Properties is much smaller with less than 1.6bn euros market capitalization. Therefore, investors who are convinced of the thesis might want to spread their investments, as I have done.

Macroeconomic tailwinds

Supply/Demand imbalance in the German rental market

Grand City Properties owns around 63,000 apartments, most of them (around 59,500) in German urban centers, the rest (around 3,500) in London, UK.

The official goal of the German government is to create 400,000 new housing units every year. There is already a supply/demand imbalance in the market, and demographics are making it worse. The German population is growing because of immigration, and this is mostly happening in urban centers. At the same time, housing construction is doing miserably. In 2022 only 295,300 units were built, and it looks like the next years will see even lower numbers as permissions for new construction are down around 30% this year.

The situation in Germany is not unique. Other countries like the U.S. have a shortage of housing supply, too. Complaints about red tape hindering construction seem to be universal. But in the U.S. housing construction is currently at its peak, whereas in Germany it is at its lowest. Additionally, compared to other countries Germany is a nation of renters — fewer than half of Germans own their own homes (and the percentage is decreasing), whereas in the U.S. it is almost 2/3 . The low homeownership rate also stands out in Europe. France , for example, is on a level with the U.S.; Spain is at an even higher level with a homeownership rate of over 3/4.

This has become a political crisis. The key issue is that the rental market is heavily regulated, while ever more complicated building regulations, increased financing costs due to interest rate developments, and high construction costs because of inflation have reduced the financial incentive to build rental apartments. Apartments that are not being built now, will be missing from the rental market in two to three years, making the shortage worse.

This will, sooner or later, benefit companies like Grand City Properties with a large portfolio of rental apartments. I do not think the share price reflects this adequately. Despite the recent depreciation, the EPRA NTA (net tangible asset value) per share was 24.7 euros at the end of H1, compared to a current share price of around 9 euros.

Rent increases will continue and even accelerate

The German rental market is heavily regulated through a rent index system called Mietenspiegel. A reference rent for similar-quality local units is determined by a database of rents (the Mietenspiegel) that provides a countrywide benchmark for tenants and landlords. Rents cannot rise more than 20 percent above this reference rent over a three-year period, and not more than 15 percent in certain areas where there is a lack of housing – which are basically the large urban areas. The system also allows some exceptions, such as social housing that can follow different rules in some areas. The rent index system is updated every two years based on the consumer price index set by Germany’s Federal Statistical Office (Destatis).

This ensures that rents rise less when inflation goes up quickly as it did in 2022. But it also ensures that rents keep rising even if inflation has slowed down again, what we are seeing now. Destatis expects inflation in Germany to have slowed down in October 2023 to 3.8%. A year ago, it had been 10.4%.

Balance sheet, debt maturities, and liquidity

Grand City Properties looks mixed on the core debt KPIs:

- LTV (loan to value)

- Net debt / EBITDA

- ICR (interest coverage rate)

While the LTV target value should be below or at 45%, the actual value at the end of Q2 was 47%, due to write-downs in Q1 and Q2. This is also in line with peers in the German market, and probably the key reason why shares have been punished. At the end of Q2 Vonovia had an LTV of 47.2, TAG Immobilien ( OTCPK:TAGOF ) was at 47.5, and LEG Immobilien ( OTCPK:LEGIF ) at 48.2.

Net debt / EBITDA was at 10.4 and the ICR at 5.8. While those numbers have deteriorated from the end of 2022 (ICR was 6.6 and Net debt / EBITDA 11.4), they are still acceptable, in my view.

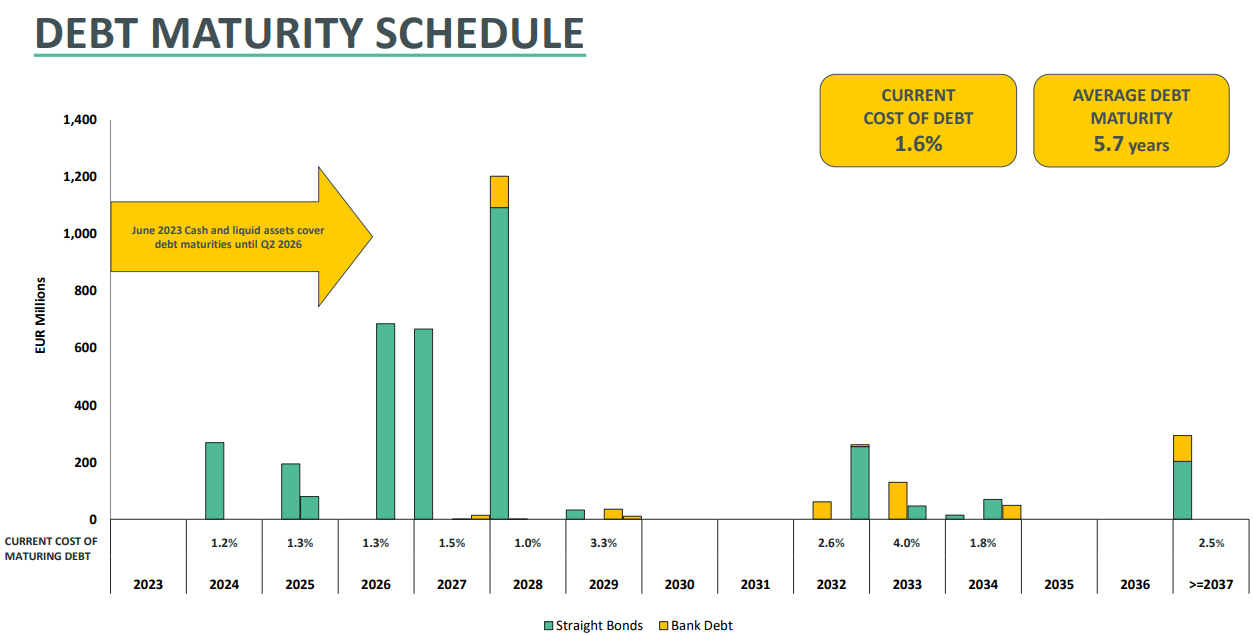

GCP has enough liquidity, and all debt maturities are covered until Q2/2026. The debt maturity schedule looks manageable. In 2026 and 2027 the company needs to repay or refinance around 700mn euros. However, the current cost of debt for those is quite low at only 1.3% and 1.5%.

Grand City Properties debt maturity schedule (Source: Grand City Properties)

{kind=link}

If GCP chooses to refinance, the interest expense will probably go up. The company has a BBB+ investment grade rating from S&P (with a negative outlook), but the current EUR bonds trade between 5 and 7 percent. The increased interest rate expense will offset rental growth but should be manageable. GCP expects the market potential of its annualized rental income to be 465mn, 17% above the annualized 398mn June value.

A note on the credit rating from S&P and the negative outlook – S&P kept the investment grade rating in June 2023 but changed to outlook to negative to align the rating with the rating of the majority shareholder Aroundtown ( AANFF ). Aroundtown has a stake of 59%.

Dividend

Per policy , Grand City Properties pays out 75% of Group FFO as a dividend. This is in line with peers. Vonovia , for example, has a dividend policy that says it pays out 70% of FFO.

As is common for German and European companies, the dividend payment is once per year. To preserve liquidity, the payout was suspended in 2023. If the dividend payments continue (which is not assured), an FFO of 1.035 per share (the midpoint of the company guidance range) would mean a very substantial dividend yield of over 9%.

My best guess would be that the payout will be at least half of the 75%. The company will present Q3 2023 earnings on November 15, and the 2023 dividend will certainly come up.

Everything depends on interest rates

While a continuation of the strong operational performance (which I expect) could move the stock up, the interest rate environment will eventually determine the trajectory of the stock price.

After having hiked interest rates up 10x in a row, the ECB left rates the same at the recent October meeting, and there is reason to assume that the hiking campaign is not just pausing, but over. If that is so, the question remains when interest rates will start going down again.

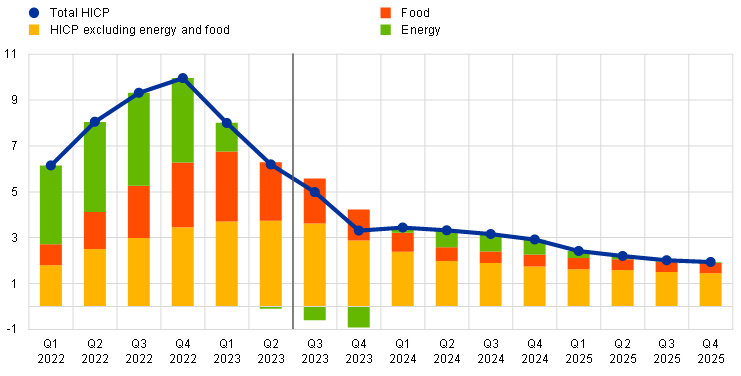

While inflation in the Eurozone has fallen significantly, it is still too high above the 2% target for the ECB to start reducing rates now. The ECB expects headline inflation to be 3.2% in 2024 and 2.1% in 2025, after an average of 5.6% in 2023.

ECB headline inflation projection (Source ECB)

{kind=link}

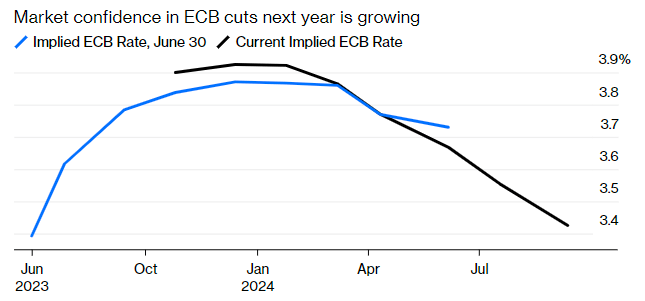

It is likely that the market will move before the ECB actually cuts interest rates. Bloomberg expects that the rate cuts will start in Q1 next year.

Source: Bloomberg World Interest Rate Probabilities

{kind=link}

If you believe in that scenario, as I do, the current share prices are a good entry point in my view.

Valuation

Earnings were negative in H1 2023 due to the write-downs. Therefore, it is better to look at funds from operations to see how the valuation looks compared to the operational performance.

FFO took a small hit in Q2 2023 (-3.3% YoY) due to higher financing costs and was 16.92 euros per share, so 8.46 on an annualized basis.

This is significantly below the historic average, but also below peers. Based on the share price per November 3 and H1 FFO, Vonovia had FFO per share of 20.76 in H1 2023, LEG Immobilien came to 22, and TAG Immobilien to 23.04.

The companies are also comparable regarding their NTA (net tangible asset) values per share compared to the share price. While all have a low number, GCP stands out with only 0.37. Vonovia and LEG Immobilien are at 0.49, and TAG Immobilien higher at 0.6.

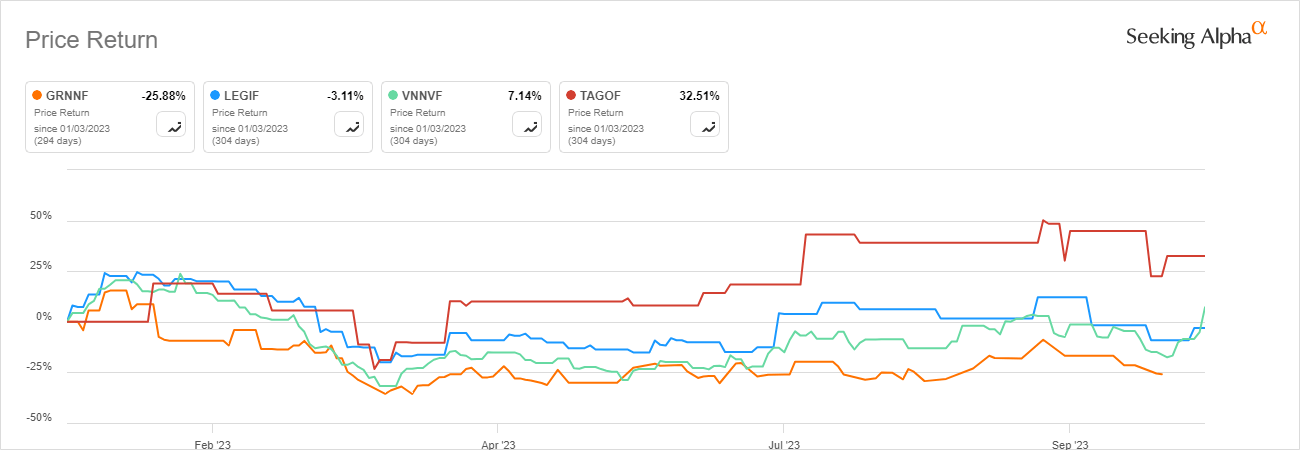

The difference in valuation is because Grand City Properties appreciated much less YTD than the other three.

Price/Return comparison ((Source: Seeking Alpha))

{kind=link}

While valuation is lower than its peers, Grand City Properties will probably only improve in line with the real estate sector and real estate prices. Once the macroeconomic environment for the sector improves, I think shares will go back to a range between 15-20 euros, where they had been in mid-2022 – an upside of over 50-100%.

Risks to the investment thesis

The biggest risk to the investment thesis is that interest rates stay higher for longer, or even go up. As we have seen, the inflation in Germany is trending downwards. However, the geopolitical situation looks unpredictable, so things can happen.

I consider the long-term economic environment favorable for Grand City Properties. If interest rates stay higher for longer, the investment thesis is still correct, in my view. It will just take longer to play out.

A further need to write down the value of its properties is another key risk. The share price would probably suffer if the write-down was significant. There is a high uncertainty as to what level property could fall in the short term as a response to higher interest rate levels.

In H1 2023 GCP wrote down the value of its property assets by -5.4%, based on a reevaluation of the whole portfolio. In H1 around 250mn in property disposals were executed at ~3% below book value, so the -5.4% seems reasonable.

As a way of comparison though, Vonovia has written down the value of its real estate portfolio by around 11% since the peak in June 2022, and this looks more in line with where market prices went. According to the numbers from Destatis, which are based on actual market transactions for new and existing buildings, prices have declined by an average of 9.9% in that period. Therefore, I would not rule out a further write-down in Q3 or Q4.

Even if that were to happen, GCP still would be far above the covenant levels in its bond contracts. According to the Q2 results presentation , there is a 43% headroom on asset values before GCP reaches the Total Debt / Total Assets limit.

In the long term, the dynamics of supply and demand point to rising property prices and rising rents.

Conclusion

Once the interest rates environment turns, Grand City Properties should benefit from macroeconomic tailwinds: the worsening demand/supply imbalance in the German residential real estate market and rising rents. I expect that over two years the share price could go back to 15 to 20 euros where it was just a year ago, an upside of over 50-100%.

For further details see:

Grand City Properties: A Value Play In The German Real Estate Market