GPRE - Green Plains: Streamlining Efforts Suggest A Valuation Re-Rate Soon

2024-01-18 18:25:19 ET

Summary

- Activist involvement at Green Plains is leading to positive changes and potential for a higher valuation.

- The merger between Green Plains and Green Plains Partners could bring valuable synergies and simplify the business.

- Despite challenges in the ethanol market, the long-term potential for Green Plains is bright, with a potential upside of up to 70%.

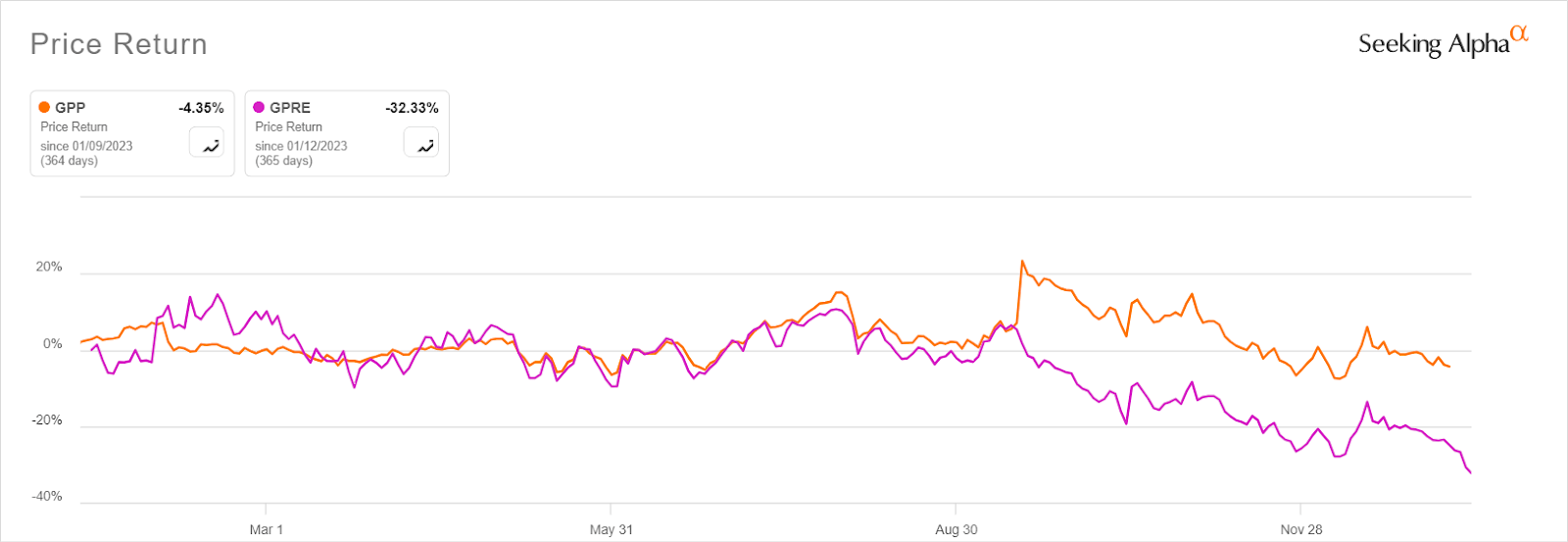

As we previously discussed in September, an activist involvement at Green Plains Inc. (GPRE) is helping shake governance for good. Many changes are taking place, and the company may come out stronger, simpler, and with a higher valuation. The merger between Green Plains and Green Plains Partners is on track and could bring many valuable synergies with it. Even as the stock suffered a hard time due to depressing ethanol prices, we think the long-term potential is bright for the new GPRE.

The merger explained: a valuation re-rate might be in sight

In September the company announced its intention to acquire the remaining 49% interest in the Green Plains Partners LP ( GPP ) that it does not yet own. They offered public investors $2.00 per share and 0.4 shares of GPRE for each share of GPP in exchange. This is not going to impact the business much, as the operations were already quite integrated as the partnership was consolidated as a VIE, and the company retained decision control over it. However, we think that valuation-wise this deal will generate a simpler business. Eventually, simpler also means easier to evaluate, and the market may notice and take note, thus increasing the multiples attached to the stock.

Right now the business is comprised of:

-

Ethanol production, which still represents the core of their activities and the bulk of their revenues.

-

Agribusiness and energy services, which comprise grain procurement and storage services.

-

GPP Partnership, which provides fuel storage and transportation services.

Up to now, it is relatively easy to evaluate the first two segments, but the third one was not straightforward. As GPP merges with Green Plains, we should then have a much clearer picture of the overall value of the group.

{kind=link}

Indeed, if we look at the performance lag between GPP and GPRE, we notice that the fuel transport and storage business is benefiting from more optimism by the market. More ownership of a business with more stable EBITDA margins will definitely benefit the company.

This is also confirmed by a commentary provided in the last earnings call:

We expect that the proposed transaction will simplify our corporate structure and governments - and governance, generate near-term earnings and cash flow accretion, reduce SG&A expense related to the partnership, improve the credit quality of the combined enterprise, and align the strategic interests between Green Plains shareholders and the partnership unitholders.

The ethanol market and a look at the latest earnings

As we wait for the full-year results in about a month, we can have a proxy of where the demand for ethanol stands today. The market has not been very favorable to GPRE in the last months, as a mix of higher supply (i.e., result of expanded capacity), and lower demand tanked the price of ethanol.

Ethanol Price (Tradingeconomics.com)

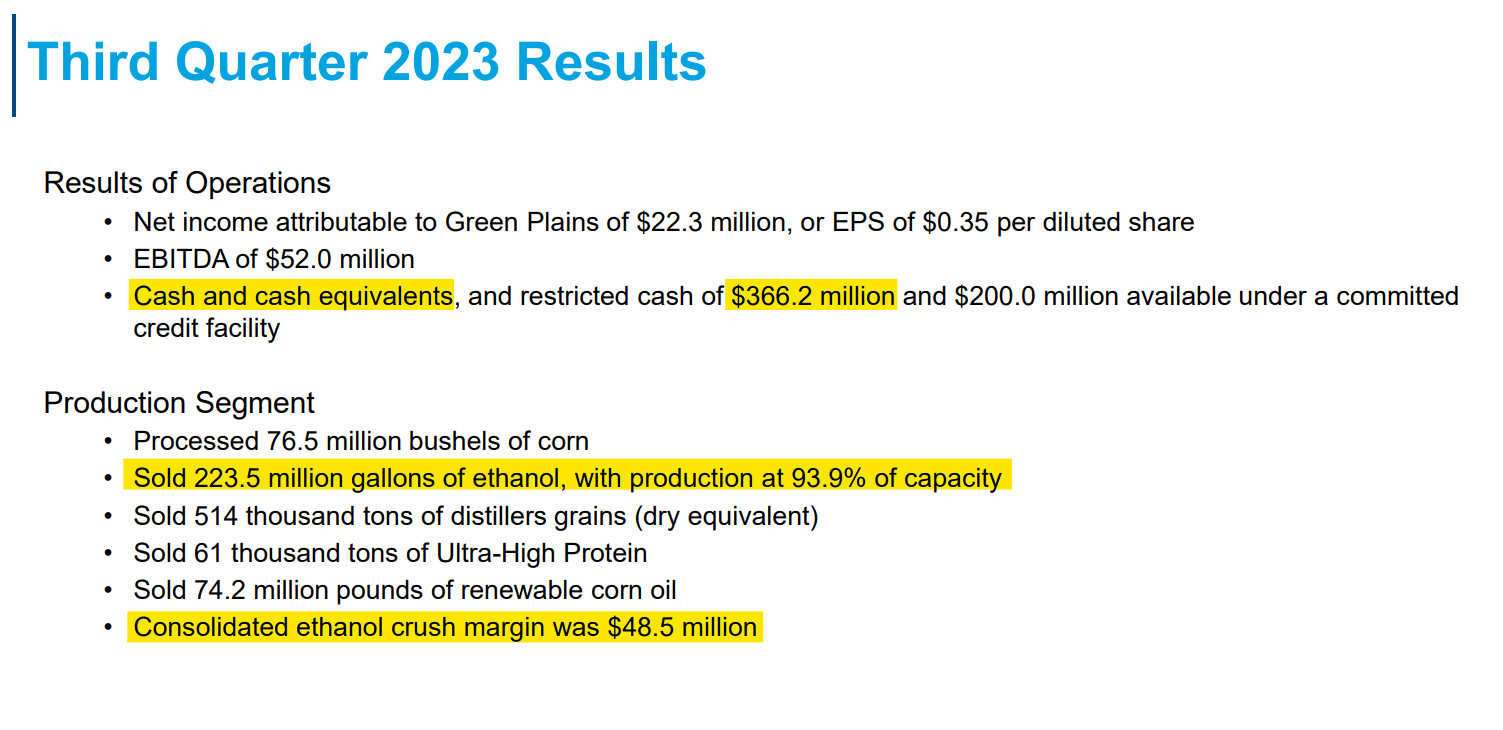

Today the price per gallon is around $1.58, a 30% drop for the beginning of 2023. However, if we go back to the pre-COVID levels of 2017-2019, we notice that the average price was even lower, at around $1.30-1.40. This means that the business model of GPRE is sustainable at substantially lower prices. If we look at the Q3 results, we indeed notice continued strength in the ethanol business in the form of high capacity utilization.

{kind=link}

94% of their capacity has been utilized, and the crush margin - primarily driven by the price of ethanol - was also consistently positive at around $50 million. As the company integrates GPP, we should expect a slight expansion of margins and more stabilization as a result of consolidating its entire business instead of just 50%.

Valuation: higher fair price and better margin of safety

In our previous article, we used a creative approach to evaluate this company that assumed a fair price in the case of an acquisition. The previous analysis did not age well, with the stock down 30% since, mostly due to decreasing ethanol prices. In this article, we are providing a similar analysis that also takes into account two new factors: (1) improving margins after the merger, and (2) worse conditions of the ethanol market at least in the short term.

Again, we shall take two different scenarios in terms of EBITDA generation, and attach the same multiples to both. After weighing each outcome for its probability, we will end up with a fair value per share that reflects the highly volatile nature of EBITDA in this sector.

-

Case 1: Average EBITDA of $165 million - referring to the period 2013/2019 - and a multiple of 18x. Probability of 80%.

-

Case 2: Average EBITDA of $3 million - referring to the period 2019/2023 - and the same multiple of 18x. Probability of 20%.

The resulting fair price is around $36. Compared to our first analysis, this is more reflective of a worse overall environment for ethanol and thus more conservative. The good news is that this means that the current margin of safety (i.e., upside potential) is around 70%, even more generous than the first case. This is because the stock has been dramatically sold down, much more than the supposed decline in fair value per share.

Conclusion

Green Plains is a very resilient ethanol producer that is in the middle of the process of diversifying and improving its business model. The merger with GPP will improve the margin mix and enhance valuation multiples for the company, eventually benefiting shareholders. We believe there is an upside potential of up to 70% as the stock has been sold down dramatically over the past months.

For further details see:

Green Plains: Streamlining Efforts Suggest A Valuation Re-Rate Soon