BMBOY - Grupo Bimbo: No.1 In The Baking Industry

Summary

- Grupo Bimbo is the world's largest baking industry company, with $19.0 billion in revenues from operations in 33 countries and 138,000 employees.

- Better acquisition integration plus more efficient operations have produced strong financial performance for this industry consolidator.

- Bimbo is not a buy at $20.60 per ADR, however, with the positives outweighing the negatives, Bimbo is a buy at $17.00.

- Interested investors should be patient.

What would stellar results look like for a global company operating in a mature recession-resistant industry? How about the following 3Q2022 over 3Q2021 results:

- Net sales up 20.0%

- Operating income up 37.6%

- Adjusted EBITDA increased 15.2%

- Net income up 50.8%

- Return on equity hit 16.7%

- Net Debt/Adjusted EBITDA ratio was 2.0

What if the company had an equally strong 5-year track record? Consider the following 5-year compound annual rates of growth (CAGRs) through year-end 2021 per Seeking Alpha :

- Revenue: 8.25%

- Operating income: 11.34%

- EBITDA: 10.27%

- Net income: 38.04%

- Levered free cash flow: 9.79%

A Web 2.0 play? A Cloud King? No, it's the world's largest baking industry company, Grupo Bimbo ( BMBOY (ADR), GRBMF ).

NOTE : The ADR is an SEC Level-I ADR and does not report in the U.S. Each ADR represents four Series A "native" common shares that trade on the BMV (Bolsa Mexicana de Valores, the Mexican Stock Exchange). For non-Spanish speaking investors, Bimbo offers annual reports, press releases, and quarterly summary presentations in English. GRBMF is the symbol for Bimbo's Series A shares denominated in U.S. dollars that trade on the U.S. OTC Pink market. Volume is consistently too low to recommend this method of acquiring a position in Bimbo.

The World's Largest Baked Goods Company

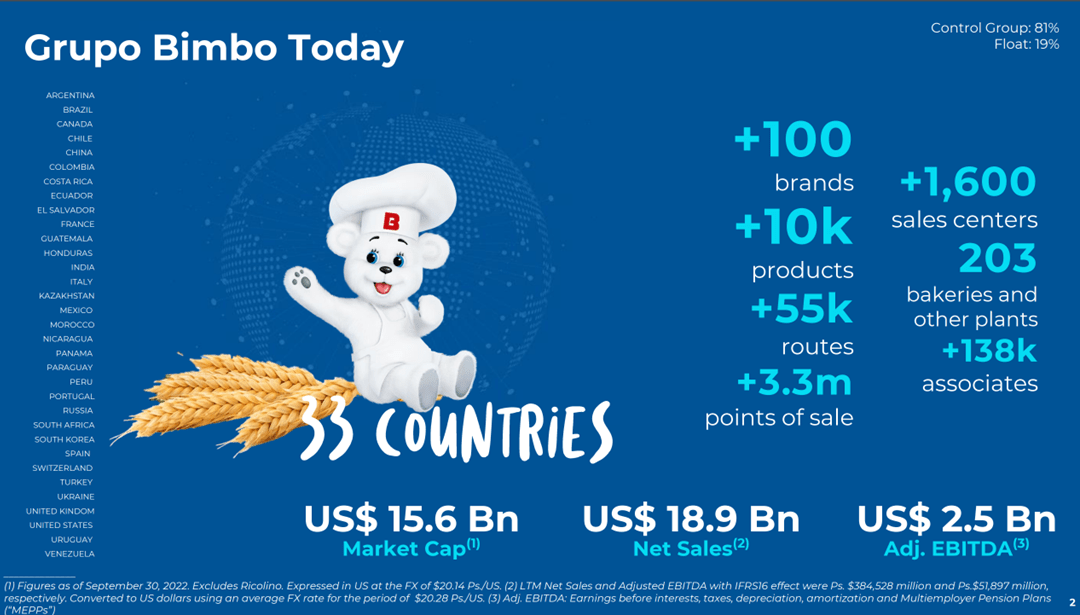

Unless you live in Mexico, you probably don't know much about Bimbo, but recent growth, improved operations, and financial performance have been noteworthy. To get a better handle on this company, we're going to take a look at three informative slides from the company's 3Q2022 Investor Presentation. The first is an overview of the company as of the end of 3Q 2022.

{kind=link}

Bimbo has annual revenues of just under $19.0 billion from operations in 33 countries ranging from Switzerland to Kazakhstan - and employs over 138,000 people. Wherever you live, chances are good that you've consumed Bimbo products. Here's a splash page of their better-known brands:

{kind=link}

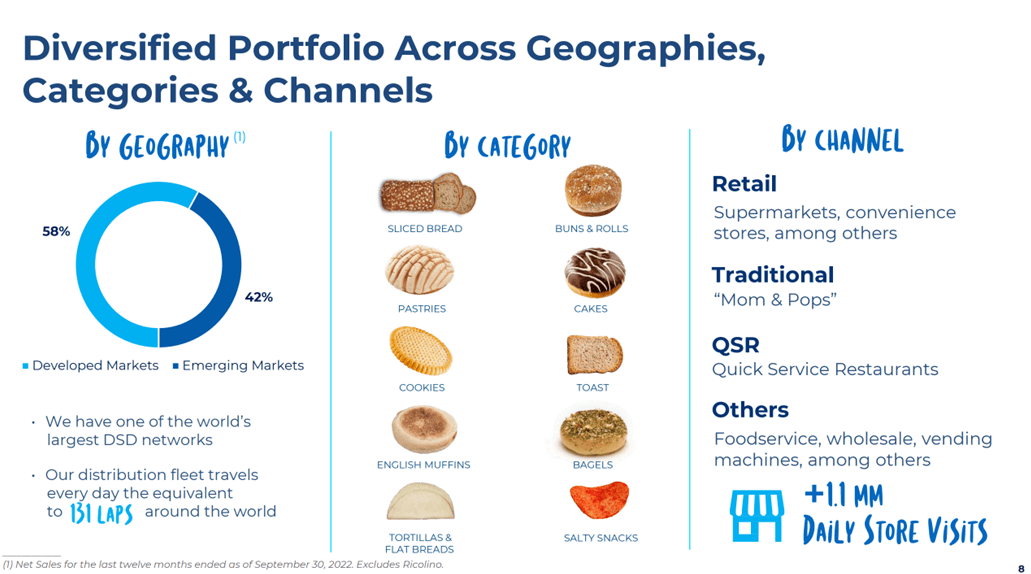

Bimbo is not just a basic purveyor of bread and rolls. Consider this geographic, category, and distribution channel breakdown:

{kind=link}

Headquartered in Mexico City since its founding in 1945, Bimbo is a multinational organization with 58% of revenues coming from developed nations and 42% from emerging markets. The company operates one of the world's largest direct store delivery fleets ("DSD") distributing more than 10,000 products spread across 10 basic baked goods categories sold through at least six different channels of distribution.

Closely-Held: Float Equals 19% of Shares

Bimbo is a closely-held company with the public float consisting of only about 19% of outstanding shares. Many relatives of the founding partners , Lorenzo Servitje Sendra, José T. Mata, Jaime Sendra Grimau, Jaime Jorba Sendra, and Alfonso Velasco, are still closely associated with the company.

The somewhat odd name "Bimbo" was a combination of Bambi and Dumbo from the two Disney films that were favorites of Marinela, Lorenzo Servitje's daughter. The Bimbo Bear began with a bear drawing in a Christmas Card given to Jaime Jorba. Anita Mata, Jaime Sendra's wife, added the hat, apron, and the loaf of bread. Finally, Alfonso Velasco rearranged the face to its present shape.

Over the years Servijte, the driving force within the company, became well-known in Mexico as CEO of Bimbo and as an author. When Servijte died in 2017 at the age of 98, then-Mexican President Enrique Peña Nieto attended the funeral. Servijte was famous for his commitment to ethical standards and social responsibility, a tradition Bimbo has continued. The current CEO, Daniel Servitje, is Lorenzo Servijte's son and the Servijte family controls approximately 71.5% of the company's shares. Additionally, 11 of the 18 board members are related to the extended Servijte, Mata or Sendra families.

As a closely-held company, Bimbo, less pressured by Wall Street quarterly expectations, has been focused on achieving long-term goals. As CEO Servijte noted in the 3Q2022 Conference Call :

We remain fully committed with our investments for [the] long haul as we see potential to continue growing in multiple categories and markets as well as improving productivity, cost management programs and digital solutions throughout our company.

Industry Consolidator

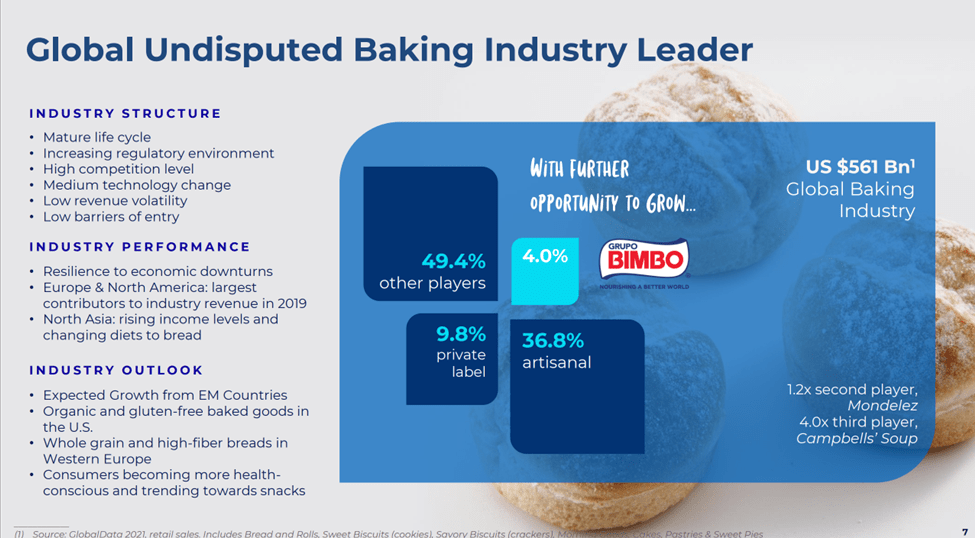

Bimbo has acquired its way to scale, consolidating a highly fragmented mature industry. According to research firm Global Data, baking is a $561 billion global industry. The top three companies, Bimbo, Mondelez ( MDLZ ), and Campbell ( CPB ) control only about 4%, 3%, and 1%, respectively. Approximately 92% of the industry consists of smaller companies, the largest of which is $4.3 billion-sales Flowers Foods ( FLO ) owner of Dave's Killer Bread, Wonder, etc., private labels Walmart's ( WMT ) Great Value, and locally-owned small bakeries. The global baking industry is projected to grow at a relatively slow rate of 2% to 3% annually for the next five years, roughly in line with population growth but also benefitting from a switch to more expensive whole-grain products in developed countries and the substitution of bread for other staples in developing countries.

{kind=link}

Bimbo is the industry's top consolidator, acquiring 11 different companies since 2019. The company has been criticized by analysts for past acquisitions that were slow to integrate and generate meaningful cash flow. CEO Servijte mentioned one key reason for the slow payoff from U.S. acquisitions in his first U.S. television interview in 2013 on CNBC .

The industry in the U.S. has been an old industry that has been quite fragmented. So many of the plants that we have found have been in existence for 80, 90, 50 years, so that's the baking industry in the U.S. Now that we have scale in each city and town, we can have the opportunity to leverage that scale with new, more efficient lines. That will allow the consumer to have a product that is more consistent and also fresher than the one that we had before when we had fewer bakeries of smaller size.

As Bimbo re-tooled or closed and consolidated old bakeries, quick results were not necessarily possible.

Significant progress in supply chain efficiency and integration speed began in 2017 with the migration of systems to Oracle ( ORCL ) Cloud Applications. A more even-handed approach to capital allocation was also demonstrated by the almost simultaneous 2022 acquisition of St. Pierre, a premium brioche baker in the U.S. and U.K, and sale of the Mexican confectionary business Ricolino to Mondelez for $1.3 billion. According to CFO David Gaxiola :

This transaction strengthens our financial profile, as it is highly accretive for us, while it enhances our long-term focus in our core categories.

Proceeds from the Ricolino sale were expected to be used to reduce debt, increase capital investments and pay a special dividend. Bimbo's 3Q2022 results, achieved while maintaining a capital expenditure budget of about $1.3 billion and net debt to EBITDA of 2.0, may indicate that its acquisitions are beginning to pay off through critical mass and more efficient integration.

Better Acquisition Integration + More Efficient Operations = Better Financial Performance

Improving operations, hedging, and the ability to push through price increases more than offset higher commodity costs over the past three years, but the sharp increase in wheat prices due to the Ukraine war had a negative impact beginning 1Q2022. The adjusted EBITDA margin had been in an uptrend, increasing from 13.0% in 2019 to 14.0% in 2021, but fell to 13.4% YTD 3Q2022.

Increased volumes and efficiency, however, more than offset the lower margins. Prior to the impact of the Ricolino transaction, YTD 3Q2022 gross revenues increased 18.7% to $15.3 billion from $12.8 billion YTD 3Q2021. Management drove more pesos to the bottom line over the same periods as the net income margin increased to 6.1% from 4.9%, helping produce a strong 48.7% increase in net income to $937.0 million from $630.2 million.

EPS assignable to the BMBOY ADR per share was $0.79 YTD 3Q2022, a 51.4% increase over $0.52 YTD 3Q2021. BIMBO has tended to pay token dividends with the ADRs receiving about $0.21 in 2021 and about $0.27 in 2022. There will also be a special dividend of approximately $0.14 per ADR in connection with the Ricolino sale to be paid in early 2023. With a 1.31% yield on regular dividends, Bimbo is not an income play, however, the roughly 30% year-over-year dividend increase was accompanied by indications management would be more generous with dividends in the future.

Baked-In Risks

To this point, we've focused on the upside. Bimbo is the world's largest bakery company consolidating a highly fragmented industry while achieving scale and operational efficiencies that are driving better financial performance. What are the relevant risks?

- Bimbo is closely-held and becoming even more so.

The Servijte family controls the company and their interests may not always be aligned with those of outside investors. One example might be the company's token dividend, however, it is hard to conceive of circumstances where maximizing shareholder value would not be in the interests of all shareholders. The company has also bought back about 4% of outstanding shares from the public float since December 2019, thereby increasing the majority owner's share, but also increasing each outstanding share's proportional ownership share of the company.

- Somewhat limited publicly-available information for non-Spanish speakers.

Bimbo does not report in the U.S. but does report on IFRS standards. The annual report and quarterly summary PowerPoint presentations are available in English, but the BMV-required detailed quarterly reports offer the main tables in English while the narratives and secondary tables are in Spanish. Currency translation might also be an issue for some investors.

- Industry consolidators depend on debt and interest rates are rising.

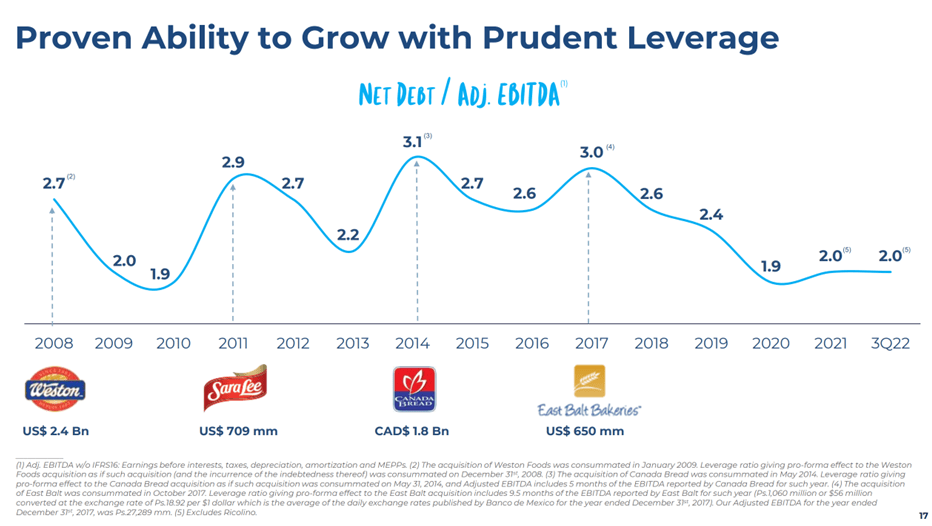

Bimbo is due for an upgrade from the ratings agencies, especially after the Ricolino sale. S&P rates the company as a BBB credit, Moody's as Baa2. As of 3Q2022, Bimbo carried about $5.0 billion in well-laddered debt with an average debt maturity of 13.9 years and an average cost of 5.7%. The nearest-term maturity is $800.0 million at 3.875% maturing in 2024. Bimbo should be able to easily refinance this debt, although new 5-year debt will likely cost roughly 5.75%. Based on an estimate of run-rate free cash flow YTD 3Q2022 (adjusted EBITDA less an estimated $1.0 billion in annual capex) the ratio of free cash flow to interest expense was a robust 4.5 and, as noted previously, net debt to EBITDA was 2.0. In addition, take a look at Bimbo's success in paying down post-acquisition debt:

{kind=link}

As the slide above demonstrates, Bimbo has consistently been able to pay down debt from internally generated cash flow.

- The price of wheat, Bimbo's basic commodity input, has been increasing for several years, pressuring margins.

The Ukraine war sharply increased the global price of wheat which was already rising primarily due to below-average harvests. According to the IMF , the global price of wheat increased 136.3% between September 2019 and November 2022. Bimbo employs extensive hedging strategies but has been forced to push through a series of price increases to preserve margins.

Conclusion

As I completed this article on January 12, 2023, BIMBOY shot up 21% to $20.60 from the previous day's $17.04. Volume "skyrocketed" from 154 to 1,500 shares. This is not an unusual move for BMBOY as it's a low-volume ADR with a bid-ask spread that is often two or more points, but that 21% move wiped out my margin of safety.

Nevertheless, I find Bimbo interesting as it is:

- A multinational recession-resistant consumer staple company that is No. 1 in its industry.

- A company that has managed through both acquisitions and organic growth to achieve high single-digit growth over a long period of time while most consumer staple companies have stagnated.

- An industry consolidator becoming more efficient at integrating acquisitions and operating at scale in a highly fragmented basic industry.

- A closely-held company where the interests of the owners and the minority shareholders are aligned.

With a reasonable EPS estimate of $1.05 to $1.08 for 2022, Bimbo's ADR is selling at a 19.1 to 19.6 PE multiple compared to 15.8 to 16.2 one day before. The less-interesting Flowers sells for a 27.2 PE multiple with 3.15% dividend yield, but sports weaker financials, performance, growth, and brands. Bimbo's lack of liquidity for small investors via its ADR and semi-transparent financial reporting are detractions but are not enough to account for such a large valuation discrepancy.

As the graph below indicates, BMBOY began outperforming the S&P 500 and Flowers beginning roughly in the third quarter of 2021 as the durability of its improved performance became noticeable - even before its sharp price spike.

Bimbo, owned through the BMBOY ADR, is not for everyone. It should be the fourth or fifth consumer staples stock an investor buys for international diversification or to add a mildly speculative element to a portfolio. Spanish-speaking investors buying "native" shares on the BMV are in effect buying a different security with a different degree of financial disclosure. However, both sets of investors face securities that are not currently a good value proposition. Bimbo is not a buy at $20.60 per ADR, however, with the positives outweighing the negatives, Bimbo is a buy at $17.00 per BMBOY ADR or around Mex$80.84 per share on the BMV. Interested investors should be patient and wait for a better entry.

For further details see:

Grupo Bimbo: No.1 In The Baking Industry