AAUKF - Grupo México: Shares Remain Under Downward Pressure 'Hold' For Now (Rating Upgrade)

2023-10-14 08:44:32 ET

Summary

- Grupo México's rating has been changed from a "Sell" to a "Hold".

- The company's stock price is likely to face downward pressure due to a very uncertain scenario for copper prices amid the looming economic recession.

- The chances of success of this strategy are good and the risk of losing a good capital gain by not taking advantage of these levels is low.

This Analysis Suggests a Hold Rating for Grupo México, S.A.B. de C.V.

This analysis changes the view on shares of Grupo México, S.A.B. de C.V. (GMBXF), a Mexican copper miner as well as freight transport operator and infrastructure company worldwide, from a previous Sell rating to a Hold rating.

From now on, this article will refer to Grupo México, S.A.B. CV simply as Grupo México or GMBXF.

In the previous analysis, it was expected that Grupo México would have had to bear the consequences of lower copper prices on the profitability of the group's red metal production.

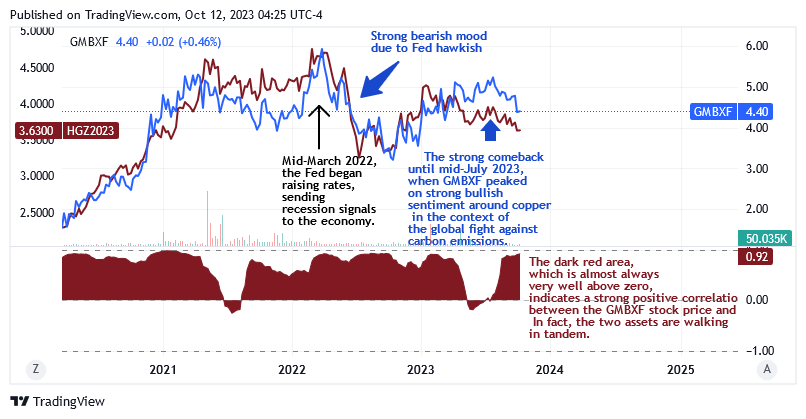

This was indeed the case, as evidenced by the financial performance in the first half of 2023 compared to the same period in 2022 and by the share price chart showing the downtrend in the share price of GMBXF since the peak around mid-2023 when the financial report was published.

The previous Sell rating was suggested to take some profits ahead of the expected decline in the stock price and because the stock price was at the peak of the cycle. The rating was communicated to retail investors a few days before the release of the company's financial results report.

This analysis has changed the stance on GMBXF stock as the opportunity to sell shares to profit from a peak in the cycle has passed.

Grupo México remains a very good player for retail investors looking to benefit from both quick short-term recoveries and long-term positive trends in copper prices. In this perspective, this analysis believes that investors should stick to a 'Hold' stance for the time being, in the sense that they should wait for a bottom in the cycle to form before buying shares.

This analysis sees good opportunities for the formation of a bottom in the stock price cycle, which could make it possible to achieve a very good return when shares are back in an uptrend mode.

The Share Price Against the Last 12 Months of Extreme Volatile Macroeconomic/Geopolitical Background

Despite the US Federal Reserve's aggressive stance on interest rates (against runaway inflation), which does not bode well for copper prices as it points to a recession weighing on demand for the red metal, the GMBXF had a strong comeback in the third quarter of 2022 and grew rapidly until around mid-July 2023 peak on copper as a key player in the global fight against CO2 emissions.

{kind=link}

The chart also shows a strong positive correlation between the price of GMBXF stock, and the price of copper as measured by copper futures (HGZ2023), as this company's business is heavily rooted in the production and trading of the red metal.

With the outlook for copper prices still very uncertain as the continued decline in consumer demand points to an ever-looming economic recession, shares of GMBXF are likely to face downward pressure and therefore be on track to reach significantly lower price levels.

Why Shares Are On Track to Have Lower Prices

Because of a significant decline in consumer expenditures (this component makes up nearly 70% of US GDP ) due to high borrowing costs combined with elevated core inflation weighing on the purchasing power of US households, the economic recession (or deterioration in US GDP growth) will result in headwinds that cannot spare the demand for copper either. The red metal is used to produce many everyday products, from electronics and metallurgy to agricultural and paint products, medicines, and cosmetics, where demand will inevitably be affected by the dynamics just presented.

Based on the strong positive correlation seen in the chart above, lower copper prices will be reflected in a continued headwind for the market value of Grupo México shares as market operators will give fewer chances for the Mexican copper producer to increase its profitability given a gloomier near-term outlook for the red metal.

It must be said that there is no doubt that, apart from this likely short-term setback due to the impending economic recession, the price of copper will again develop more in line with its long-term positive trend.

This means that as a major producer of this important metal in strategic countries, Grupo México shares are therefore well positioned to follow suit.

{kind=link}

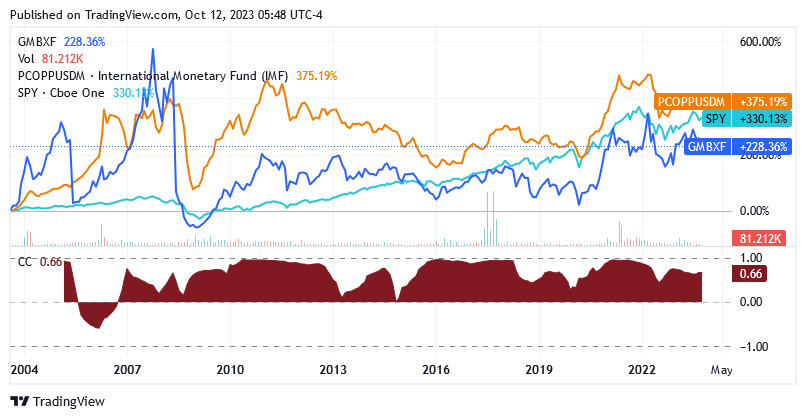

However, by taking advantage of the volatility in the copper price, the retail investor can beat the US stock market ( SPY ) through Grupo México.

This means that by implementing a combined strategy that takes into account the strong positive correlation between the GMBXF share price and the global copper price (PCOPPUSDM), the retail investor can achieve significantly better returns than a strategy based solely on a buy-and-hold approach.

A strategy based solely on a buy-and-hold approach offers the opportunity to take full advantage of Grupo México's consistent dividend payout, as the company has returned twelve years of free cash flow to shareholders, versus an industry average of nine years. But even here there are downsides in the sense that the dividend paid by the company is not overwhelming. Of course, GMBXF cannot be expected to stand up to the companies of the Dividend Aristocrats group, but GMBXF is not a winner compared to its most direct competitors either.

Although GMBXF stock has a dividend yield ((TTM)) of 4.48% compared to the S&P 500's dividend yield of 1.57% as of this writing, the shares are not held long-term because of the dividend the company pays out.

Objectively, there are many better alternatives, as the following comparisons show.

The company paid approximately $0.20 per share over the trailing 12 months ended August 28, 2023, versus the following peer group:

Teck Resources Limited (TECK)'s dividend rate ((TTM)) was $0.37 per share, Anglo American plc ( NGLOY ) paid $0.65, BHP Group Limited ( BHP ) paid $3.40, Materion Corporation ( MTRN ) paid $0.51, Rio Tinto Group ( RIO ) paid $4.02, and Vale S.A. ( VALE ) paid $0.79.

On August 28, 2023, Grupo México recently paid out a quarterly dividend of 0.800 Mexican pesos (or $0.04773) per share to its shareholders. The quarterly dividend is variable as its amount largely depends on the volatility of the copper market.

A strategy aimed at taking advantage of copper price cycles without losing sight of the commodity's positive uptrend now suggests waiting for the formation of stock price levels that could signal the bottom of the cycle.

It won't be long before this happens, as the headwinds of the expected near-term recession will help the retail investor achieve its goal. The retail investor will then have the opportunity to increase the shares of Grupo México by taking advantage of the dips.

The Main Downside Catalyst for the Stock Price in the Near Term: "The Looming Recession"

An economic recession is already looming, given the slowdown in the industrial sector and the difficulties in the housing sector due to the lack of recovery in demand for mortgages for home purchases. These sectors, where the core demand for copper lies, are suffering from the deterioration in financing conditions as a result of the Fed's tightening of monetary policy and even more restrictive access to credit following the crisis of some regional banks last March.

The S&P Global US Manufacturing PMI of 49.8 in September 2023 suggested that manufacturing industry health deteriorated for the fifth consecutive month, as did order intake for the fifth consecutive month, reflecting high rates and inflation both dampening consumer demand while employment creation remains moderate.

Mortgage Bankers Association data on U.S. mortgage applications continues to point to a bleak outlook for refinancing applications and home-buyers. The recovery in mortgage applications and refinances will likely be delayed by several months as Fed rates will remain higher for longer. The Mortgage Bankers Association also indicates that the average interest rate for a fixed-rate mortgage with a term of 30 years is the highest in almost 23 years.

How Grupo México Might Perform Given "Higher-for-Longer" Rates from the Fed and Elevated Core Inflation

As Grupo México's financial results for the first half of 2023 show , the companies' three major business areas performed as follows.

The mining division accounted for 76.5% of total revenue, while the transportation division accounted for 21.5% of total revenue and the infrastructure division accounted for 4.6% of total revenue.

The mining division achieved marginal revenue growth of just 0.8% year-on-year to $5.60 billion in the first half of 2023: despite being fully offset by a 6.3% year-on-year increase in copper production to 511,738 tonnes, the 10.6% decline in the copper price (Comex) was quite impactful for the company's overall profitability, with a negative fallout for the share price.

After the publication of the company's results for the first half of 2023, which took place on July 27, and highlighted the impossibility of better profitability due to the decline in copper prices, the share price showed a sharp downtrend from the mid-July 2023 peak, as shown in the graph above.

Even a 19.6% YoY revenue increase from the Transportation Division to $1.57 billion, coupled with a 6.5% YoY revenue increase to $335 million from the Infrastructure Division, proved not to be enough to help the company achieve better results in terms of EBITDA and EBITDA margin.

As production cost data tightened due to inflationary pressures, resulting in a 10.2% year-on-year increase in the mining division's global net cash costs to $1.16 per pound in the first half of 2023, EBITDA growth failed to keep up with sales growth.

In the first half of 2023, Grupo México's EBITDA of $3.73 billion increased 3% year-over-year, while Grupo México's revenue of $7.3 billion increased 5%, resulting in an EBITDA margin decline of 100 basis points to 51%, and as a result, the market did not welcome the performance.

The transportation division's EBITDA margin improvement by 250 basis points y-o-y to 47.5% in the first half of 2023, and the infrastructure division's EBITDA margin improvement by 820 bps y-o-y to 48.3%, were not enough to offset the 180 basis points annualized decline in the global mining division's Ebitda margin to 50.6% in the first half of 2023.

As of June 30, 2023, Grupo México enjoyed solid financial condition with $6.52 billion in cash and short-term investments, while total debt stood at $9.16 billion. The debt has an extremely favorable maturity schedule , with annual payments remaining below $1 billion until 2034, while 66% of the total debt does not mature until 2035.

Grupo México has an interest coverage ratio of 11.1x, which is determined by dividing trailing-twelve-month operating income of $5.993 billion by trailing-twelve-month interest expense of $0.5404 million. Thus, the company can easily pay off any financial obligation arising from its outstanding debt, as investors typically consider a ratio of 1.5x or higher as a hallmark of solvency.

A solid financial position, as reflected by the above measures, allows Grupo México to absorb the effects of weaker consumer demand and inflationary pressures weighing on its profitability and to continue to finance ongoing activities, particularly the following kind of activities:

- Higher recovery and normalization of production at the Cuajone mine, a large copper mine in southern Peru, and higher ore grades at the Toquepala mine, a large porphyry open-pit copper mine in Peru.

- Higher production from Mexican facilities and Asarco. Asarco is a Tucson, Arizona-based company that was reintegrated into Grupo México in 2009 and processes copper in Texas after mining the base metal ore at Arizona's three largest open pit mines, Mission, Silver Bell, and Ray.

Grupo México manages the copper business through the Americas Mining Corporation subsidiary which takes control of ASARCO and Southern Copper Corporation (SCCO).

Grupo México owns 88.9% of Southern Copper Corporation, a Phoenix, Arizona-based company that mines, explores, smelts, and refines copper and other minerals in Peru, Mexico, Argentina, Ecuador, and Chile.

The Possible Next Step for the Share Price in the Current Context

A weaker copper price environment amid recessionary headwinds in industrial and residential construction, as well as high inflation, exacerbated by higher energy purchases due to the conflict in Ukraine and the Hamas attack on Israel, will continue to pressure Grupo México's profitability through its mining division.

The bearish sentiment regarding Grupo México's share price is therefore expected to continue and this analysis assumes that the shares may not recover at the moment but will likely provide a more comfortable entry for retail investors to this miner's stock, which is nevertheless a very good candidate to gain exposure to the changes in the copper price.

This analysis assumes that shares may not recover at the moment, but in the short term, they are expected to provide retail investors with a more comfortable entry into the stock of this miner, which is a good candidate to use for gaining exposure to changes in the price of copper.

The GMBXF Stock Valuation

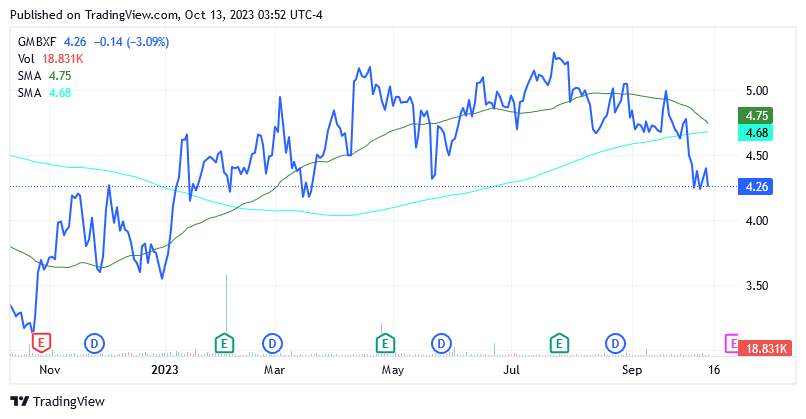

As of writing, shares were trading at $4.26 per unit, giving it a market cap of $34.19 billion, down 13% from the previous analysis.

The stock price is slightly above the $4.21 midpoint of the 52-week range of $3.11 to $5.31, but still far from the lower bound of the interval, say about 37% far.

{kind=link}

The stock is also trading below its 200-day moving average of $4.68 and below its 50-day simple moving average of $4.75.

Stock prices are undoubtedly significantly lower than they were a few weeks ago, but under pressure from the headwinds just highlighted in the analysis, they are heading to even lower levels.

For retail investors who followed the previous analysis and made some profit from their investment in Grupo México, now is not yet the time to add to their positions.

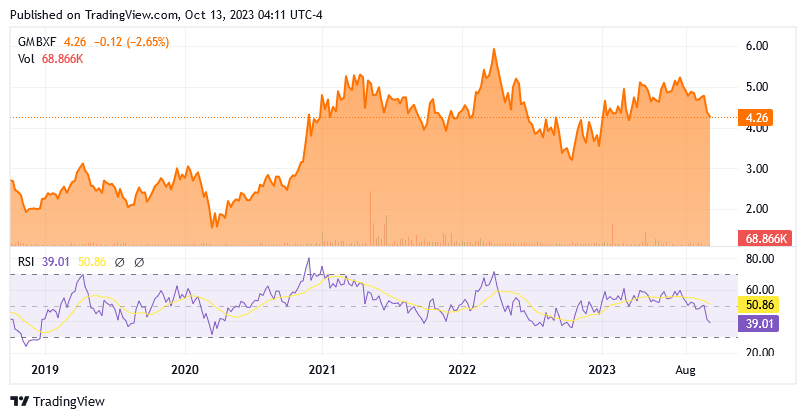

The 14-day relative strength indicator (14-day RSI) at 39.01x suggests that the shares are not yet oversold despite the decline since the peak of the cycle, which was reached around mid-July 2023. This means there appears to be room for the stock price to go further down.

{kind=link}

Retail investors will likely be wondering when it will be time to rebuild the position in Grupo México and therefore abandon the currently proposed Hold rating.

If the retail investor looks at the 14-day RSI chart, he can see that Grupo México shares have historically formed a cycle bottom around 30, which is the benchmark for oversold levels.

This analysis suggests that retail investors should maintain an opportunistic mindset as current times appear to offer a great opportunity to profit from a new low in the cycle. Just like after the outbreak of the COVID-19 pandemic around mid-March 2020, when the 14-day RSI fell below 30, there is now the possibility of another bottom with an extremely comfortable entry point for buying this stock as the economy enters the recession phase. Recession fears will create additional headwinds for the share price.

A recession, which is absolutely not good for the copper price, is highly likely based on the development of relevant economic indicators presented in this analysis and the expectations of prominent voices among economists.

Michael Pearce, senior U.S. economist at Oxford Economics, expects the overall economy to be hit by a sharp downturn.

Equally important is the opinion of the CFO of the US Federal National Mortgage Association (Fannie Mae) Chryssa Halley, who predicts a recession around the end of 2023.

While economist David Rosenberg of Rosenberg Research - an organization that conducts macroeconomic studies and the likely impact on the financial markets - believes that the likelihood of the US economy avoiding a recession is close to zero.

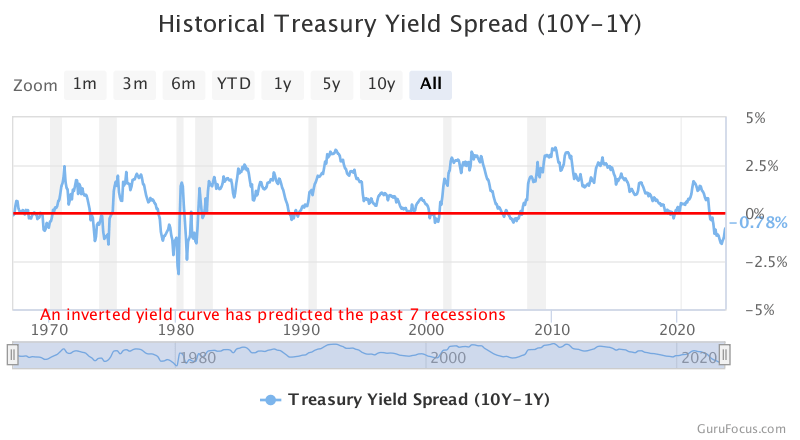

In addition, the analysis recommends that retail investors closely monitor the evolution of the difference between the yield on a one-year US government bond and the yield on a ten-year US government bond, as this indicator, currently consisting of an inverted yield curve, continues to point to a recession.

Under normal conditions, the curve should not be inverted because the 10-year U.S. Treasury yield typically exceeds the 1-year U.S. Treasury yield and this is because longer-term loans carry a higher risk of financial insolvency than shorter-term loans. So, when short-term yields outperform longer-term yields, it means that the short-term outlook is viewed by investors as extremely risky, likely heralding the start of a sharp deterioration in the economic cycle.

This type of indicator is great for predicting an economic recession because, according to GuruFocus' chart, seven out of seven negative cycles since 1965 have been predicted by an inverted yield curve.

{kind=link}

Currently, the one-year yield is 5.426% versus a 10-year yield of 4.648%.

The Risk of a "Hold" Stance for GMBXF

The risk associated with a "Hold" stance is that the shares of GMBXF will recover from approximately where they are now and retail investors will de facto lose the chance to exploit current stock prices, which, as illustrated, are no longer that high.

However, this risk is low because all previous economic forecasts indicate that a recession is actually imminent.

But objectively speaking, what else can one expect after the Federal Reserve has raised interest rates so aggressively - through the most restrictive monetary policy since the 2007-2008 financial crisis - to combat the highest inflation in more than 40 years?

Financial conditions are very tight, and the cost of living threatens the integrity of families in fulfilling their regular obligations, as disposable income is under severe pressure while unionized workers are currently fighting for wage increases and other working conditions.

Wage adjustments are slow in keeping pace with core inflation, which, among other things, threatens to wake up again due to geopolitical conflicts. Many employees will never be able to make a living on their current wages and will therefore have to look for a better-paying job.

But by the time this realignment occurs, consumer demand will have continued to slow down under the weight of the current macroeconomic situation. As they face a drop in turnover and their budgets come under pressure from increased labor costs, companies will be forced to cut staff, starting with not renewing contracts with precarious working conditions.

Companies in the technology industry have already cut many jobs and announced further job cuts. Other industries will follow the trend.

In addition, consumer demand is falling so sharply that not only store looting or credit card defaults could indicate widespread dissatisfaction with the current situation and distrust of the future, but the closure of numerous stores in strategic cities such as San Francisco by consumer-oriented giants also rings the alarm bells.

With many market participants still convinced of the soft-landing propaganda, which is not actually a message to the economy but something the markets would like to hear about, the recession will come as a bolt from the blue. They will be caught off guard by the news and once they panic, their irrational behavior will be reflected in a devaluation of US-listed stocks.

The stock has a 24-month beta of 1.20 (on this Seeking Alpha page , scroll down to the "Risk" section), meaning Grupo México shares are vulnerable to strong headwinds should the recession hit the stock market as forecast. Therefore, a "Hold" rating today indicates low risk or a high probability of a successful strategy.

Conclusion

The short-term future remains problematic for the profitability of Grupo México, S.A.B. This is due to weaker consumer demand negatively impacting copper prices, as well as ongoing inflationary headwinds driving up production costs.

The company's copper mining division will prevent improvement in the company's profitability as this division accounts for 75% of total revenue. This puts further pressure on stock prices but increases the chance that they will form the bottom of the cycle in the coming weeks.

Before these significantly lower prices occur, retail investors should take a neutral stance on this stock now as a subsequent step after the sell recommendation from the previous analysis.

For further details see:

Grupo México: Shares Remain Under Downward Pressure, 'Hold' For Now (Rating Upgrade)