GUG - GUG: Not Perfect But Still A Decent Way To Invest In The Debt Markets

2023-12-26 05:07:27 ET

Summary

- The Guggenheim Active Allocation Fund offers a 9.97% yield and invests in both stocks and bonds.

- The fund's performance since its inception has been poor, with shares down 28.90% over the period.

- The fund is heavily weighted towards bonds, particularly high-yield corporate bonds and bank loans, which offer better risk-adjusted returns in the current environment.

- The fund can theoretically invest in both bonds and equities, but bonds seem to be its focus.

- The fund should be able to maintain its distribution if the market stays strong next year, but there is no guarantee that this will be the case.

The Guggenheim Active Allocation Fund (GUG) is a closed-end fund that income-seeking investors may wish to employ to achieve their goals. The fund's current 9.97% yield is a testament to its success at providing income for its shareholders. Fortunately, investors do not have to sacrifice the upside potential of a common equity investment by purchasing this fund. This is because the Guggenheim Active Allocation invests in both stocks and bonds, although it is very heavily weighted in favor of bonds right now. This is not necessarily a problem since bonds do look somewhat more attractive than common equities in terms of risk-adjusted total return potential right now.

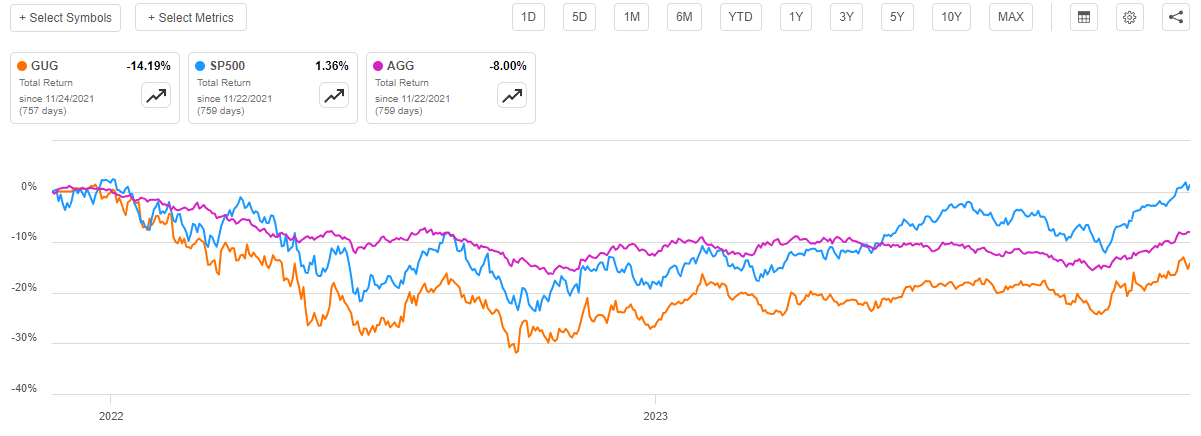

The Guggenheim Active Allocation Fund is a relatively new fund as it only began trading in November 2021. As such, it does not have an especially long performance track record that we can have a look at. However, the fund's performance since its inception certainly does not inspire a lot of confidence. As we can see here, the fund's shares are down 28.90% since the date that they first began trading. That is far worse than the price performance of either the S&P 500 Index ( SP500 ) or the Bloomberg U.S. Aggregate Bond Index (AGG):

{kind=link}

However, the Guggenheim Active Allocation Fund has a substantially higher yield than either of the two indices. That naturally has an impact on the actual investment performance that the fund's shareholders experienced. This is because a distribution can either partially or fully offset a decline in the fund's share price depending on the size of the distribution. As such, we need to include the effects of the distribution in the fund's performance charts. When we do that, we see that the Guggenheim Active Allocation Fund still underperformed either of the indices, but the difference was not as pronounced:

{kind=link}

The fact that the fund underperformed both the American stock and bond indices since it was created probably does not make anyone want to rush out and buy it. However, past performance does not necessarily have any relation to the fund's future performance, so let us have a look at it anyway.

About The Fund

According to the fund's website , the Guggenheim Active Allocation Fund has the primary objective of providing its investors with a high level of total return. The website goes on to state that the fund will achieve this goal through a combination of current income and capital appreciation. This statement does not make sense if this is a pure bond fund, as some sources suggest. After all, bonds do not deliver any net capital gains over their lifetimes because they are issued and redeemed at their face values.

However, it does make a great deal of sense for a blended fund that invests in a combination of common stock and bonds. The fund's website suggests that this is the case:

The Fund's investment objective is to maximize total return through a combination of current income and capital appreciation.

The Fund pursues a tactical asset allocation strategy, dynamically allocating across asset classes, and a relative value-based investment strategy, utilizing quantitative and qualitative analysis to seek to identify securities with attractive relative value and risk/reward characteristics. The Fund's sub-adviser seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies. The Fund's investment philosophy is predicated upon the belief that thorough research and independent thought are rewarded with performance that has the potential to outperform standard indexes on an absolute and/or risk-adjusted basis.

That statement alone makes mention of both fixed-income and equity investments being potential investments in the fund. The website continues to push home this point:

The Fund will seek to achieve its investment objective by investing in a wide range of both fixed-income and other debt instruments selected from a variety of sectors and credit qualities, including, but not limited to, government and agency securities, corporate bonds, loans and loan participations, structured finance instruments (including residential and commercial mortgage-related securities, asset-backed securities, collateralized debt obligations and risk-linked securities), mezzanine and preferred securities and convertible securities. The Fund may invest in non-U.S. dollar-denominated Income Securities issued by sovereign entities and corporations, including Income Securities of issuers in emerging markets. The Fund may invest in Income Securities of any credit quality.

The Fund may also invest in common stocks, limited liability company interests, trust certificates and other equity securities that the Fund's sub-adviser believes offer attractive yield and/or capital appreciation potential. The Fund may employ a strategy of writing (selling) covered call options and may, from time to time, buy put options or sell covered put options on individual Common Equity Securities.

The Fund will use tactical asset allocation models to determine the optimal allocation of its assets between Income Securities and Common Equity Securities.

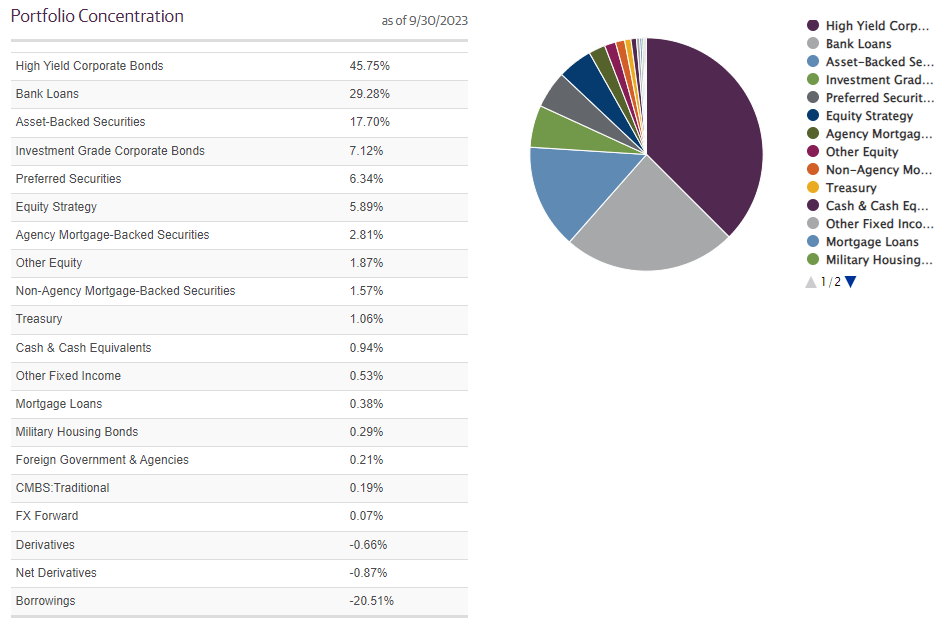

The above could not be any more clear in stating that the Guggenheim Active Allocation Fund is a blended fund that invests in both fixed-income and common equity securities. I will admit though that I generally think of bond funds when thinking of Guggenheim closed-end funds. This is likely because of the popularity of funds such as the Guggenheim Strategic Allocation Fund ( GOF ). Indeed, the Guggenheim Active Allocation Fund seems to be very heavily weighted towards debt securities right now. We can see this by looking at the fund's portfolio allocation:

{kind=link}

As we can see, the top two categories on this list are high-yield corporate bonds ("junk bonds") and bank loans. These two categories alone account for 75.03% of the fund's net assets. In comparison, the two common equity strategies here account for only 7.76% of the fund's net assets. Thus, clearly, the fund is weighted towards high-yielding debt securities. This makes a lot of sense in the current environment. As I have driven home in a few previous articles now, a portfolio that consists of a combination of junk bonds and leveraged loans has better risk-adjusted returns than a common equity portfolio. This comes from the very high yields that are available from these securities in the current interest rate environment and the fact that they are much less volatile than common equity. After all, an investor will not lose money by investing in debt securities as long as these securities are held to maturity. Thus, we can earn an easy 8% to 9% annual return just by purchasing a junk bond today and holding it until potential. While it is possible to get a better return than that by investing in common stocks, common equities can also go down. This is what is meant by junk bonds offering better risk-adjusted returns right now.

The big risk with junk bonds, of course, is that the issuing entity might default before the bond matures. In such a case, the investor who owns the junk bond will lose their money. Thus, we need to take steps to protect ourselves from such a situation. The biggest way to do this is to ensure that only a very small percentage of our portfolios is exposed to any individual junk bond issuer. The Guggenheim Active Allocation Fund is doing a very good job at achieving this diversification. We can see this quite clearly by looking at the largest positions in the fund. Here they are:

Guggenheim

As we can see, the largest position in the fund only accounts for 1.65% of the fund's total portfolio. That is a small enough weighting that it ensures that investors will not even notice a default. After all, the yields on junk bonds are high enough to erase a 1.65% loss pretty quickly. There could still be a risk of losses if a large number of companies were to all default at the same time, but in such a situation it is quite certain that there are big problems in the economy and investors are likely to lose money no matter what they have in their portfolios. In short, there should not be much for us to worry about here. The fund appears to be doing a good job at protecting investors against default losses while maximizing its risk-adjusted returns.

As noted earlier, the Guggenheim Active Allocation Fund also has a high allocation to bank loans and loan participations right now. These are what are known as "leveraged loans," and they can best be thought of as floating-rate junk bonds. These are bank loans that are made to companies that are carrying high levels of leverage or may be at risk of default. These loans are sold off to investors by the banks that made them in order to manage their internal risks. While the fact that these loans are made to companies that may already be financially stressed could be concerning, the risks here are not really much higher than junk bonds. As long as the fund ensures that its exposure to any individual borrower is not a significant part of the portfolio then it should be fine.

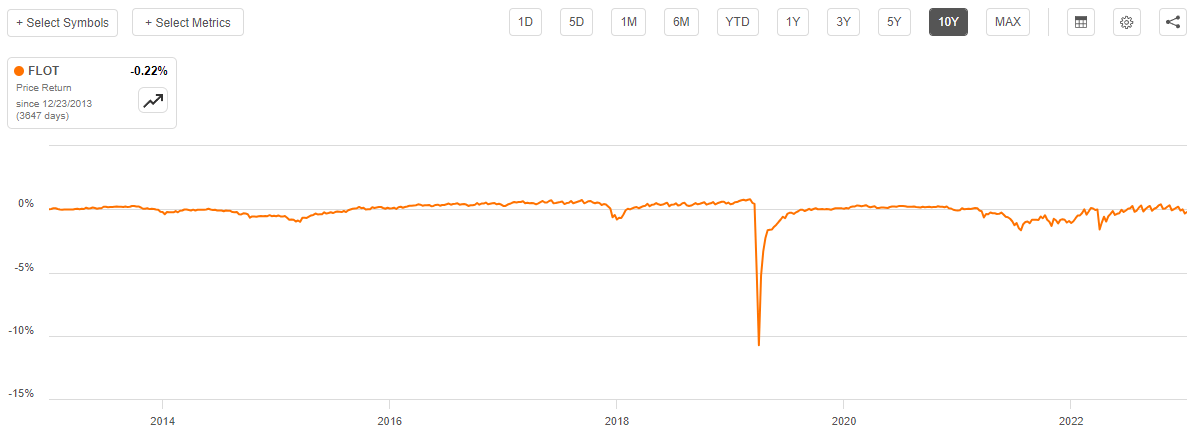

The big advantage of leveraged loans is that they tend to be stable in price regardless of changes in interest rates. I pointed this out in a recent article . We can also see this quite clearly by looking at a performance chart of the BBG US Floating Rate Notes 5 Yrs. And Less Index ( FLOT ). Here is the index's price performance over the past ten years:

{kind=link}

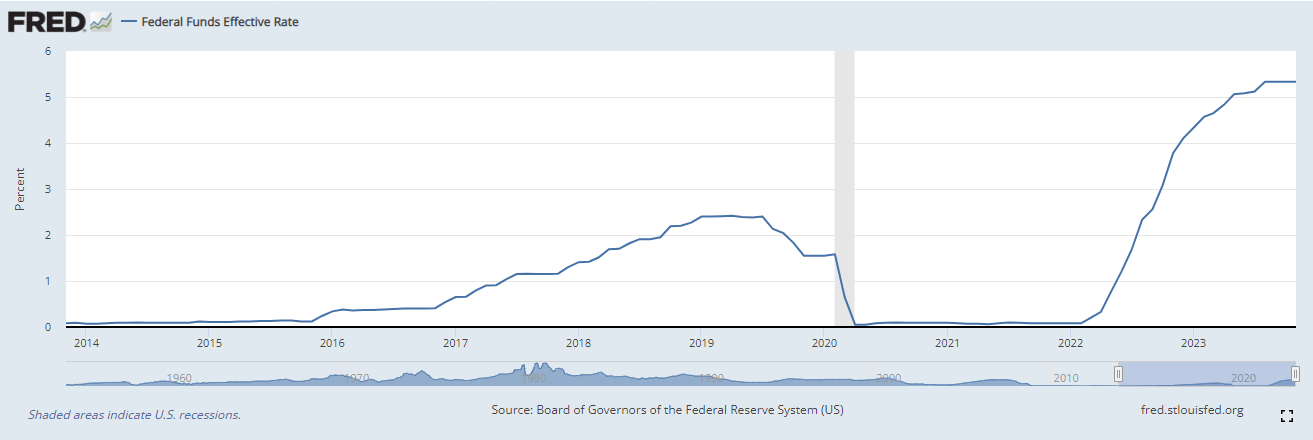

As we can clearly see, the index has been almost completely flat over the past ten years. The only exception to this stability is a very brief period at the outset of the COVID-19 pandemic and the lockdowns when investors were panicking and selling everything in their portfolios to go into cash. The index quickly recovered from that event though and has been otherwise almost perfectly flat. This stability came despite the fact that there were a number of macroeconomic events over the period as well as quite a few changes in monetary policy. Here is a chart of the effective federal funds rate over the same ten-year period:

Federal Reserve Bank of St. Louis

{kind=link}

We can clearly see that interest rates were both increased and cut a few times during the ten-year period. However, this had no real impact on the index. Thus, the fund's allocation to these securities should result in its portfolio exhibiting slightly less interest-rate sensitivity than it would if it were entirely invested in fixed-rate securities. However, fixed-rate securities do make up a higher percentage of the fund's assets than floating-rate loans so we can still expect that the fund's shares and net asset value per share will go up if interest rates continue to fall.

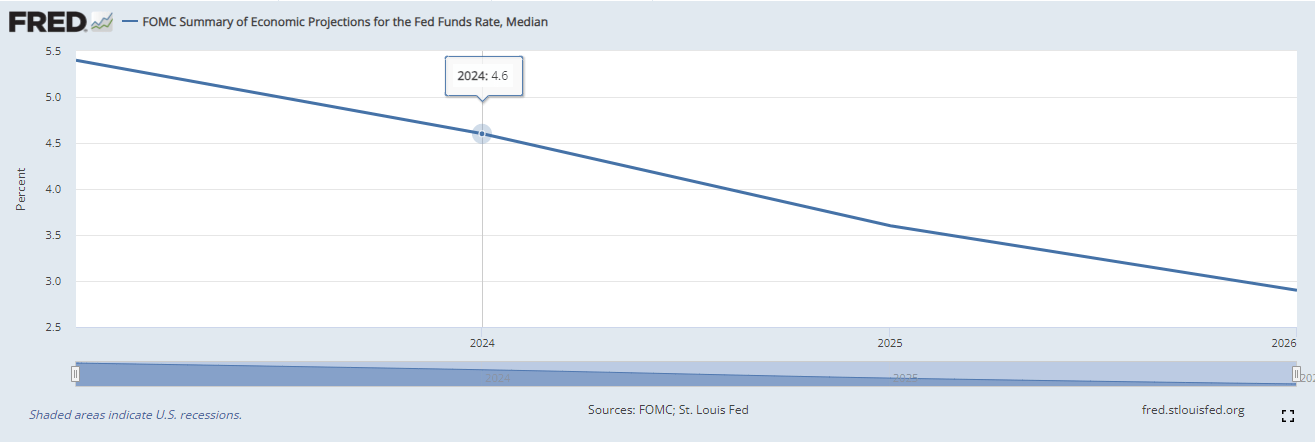

It is currently expected that interest rates will decline over the course of 2024. Indeed, the Federal Reserve has already provided guidance suggesting that the effective federal funds rate will be at 4.6% at the end of 2024:

Federal Reserve Bank of St. Louis

{kind=link}

That equates to three 25-basis point cuts over the next twelve months.

The market is pricing in more rate cuts than this, however. Barron's points this out in a recent news release :

Federal Open Market Committee members updated their projections for future interest rates on Wednesday. Officials' median estimate now calls for the federal-funds rate to end 2024 at 4.6% - implying three quarter-point cuts from the committee's current target range of 5.25% to 5.50%. That compared with futures-market pricing before the meeting that pointed to a target rate of around 4.00% to 4.25% at the end of 2024, which would mean four or five quarter-point cuts.

Markets took an even more dovish message from the committee's statement announcing the decision, its economic projections, and a press conference from Federal Reserve Chair Jerome Powell. The greatest odds implied by futures pricing on Wednesday afternoon were for a year-end 2024 fed-funds rate in the range of 3.75% to 4.00%. That would mean 1.5 percentage points of reductions in the Fed's target next year, or six cuts of a quarter-point each.

Thus, the market is clearly pricing in more interest rate cuts than the Federal Reserve has guided for. The market's expectations have already shown up in bond prices, as evidenced by the rapid increase in the price of the ten-year U.S. Treasury over the past three months:

{kind=link}

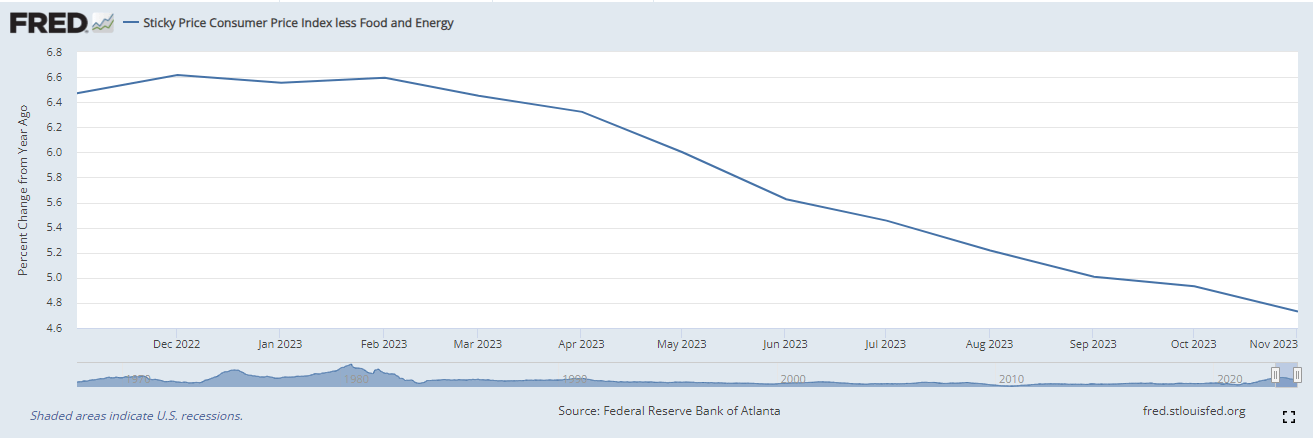

The concern here is that fixed-rate bonds might have become overpriced. There are reasons to believe that the Federal Reserve will stick to its guns and not comply with the market's desire for six rate cuts. In particular, inflation is still far above the Federal Reserve's target range. For example, the sticky consumer price index appreciated 4.73063% year-over-year in November.

Federal Reserve Bank of St. Louis

{kind=link}

The year-over-year figure looks much better if we exclude shelter costs as well, but the point remains that inflation is far from beaten. Thus, there could be a reason that the Federal Reserve will be forced to keep rates at far higher levels than the market is projecting. This is especially true if the economy avoids a recession in 2024 and energy prices start to rise again. As much of the progress that has been made in reducing the headline inflation rate has been due to energy prices being lower than in 2022, that scenario would reignite inflation and probably cause the central bank to reverse course on the projected interest rate cuts.

As such, risk-averse investors probably do not want to go all-in on fixed-rate bonds yet. It would be better to have a mixture of fixed-rate and floating-rate securities to reduce your interest-rate risk. The Guggenheim Active Allocation Fund is certainly doing that to a certain extent, but its allocation to floating-rate securities is not as high as funds such as the Ares Dynamic Credit Allocation Fund ( ARDC ) or the Apollo Tactical Income Fund ( AIF ), so it might still be a good idea to hold onto those funds if you have them to hedge the interest-rate risk.

Leverage

As is the case with most closed-end funds, the Guggenheim Active Allocation Fund employs leverage as a means of boosting its effective yield and total return. I explained how this works in a number of previous articles in similar funds. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase fixed-rate bonds, leveraged loans, and other income-producing assets. As long as the total return that it receives from the purchased securities is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield that it earns from the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates so this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much leverage because that would expose us to an excessive amount of risk. I generally prefer a fund's leverage to remain below a third as a percentage of its assets for this reason.

As of the time of writing, the Guggenheim Active Allocation Fund has leveraged assets comprising 26.41% of its portfolio. This is a pretty low level for any closed-end fund, especially one that is weighted towards investing in debt securities, and it is well below the one-third level that we ordinarily like to see. As such, the balance between the risk and the reward seems to be quite reasonable here. We should not need to worry about the fund's leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Guggenheim Active Allocation Fund is to provide its investors with a very high level of total return. In pursuit of this objective, the fund invests in a blended portfolio of debt and equity securities. However, right now it is very weighted towards junk bonds and leveraged loans. These securities primarily deliver their investment return in the form of direct payments to their owners. In the current environment, these payments can be quite large, as the Bloomberg High Yield Very Liquid Index ( JNK ) currently has a yield-to-maturity of 7.80%. The yield from leveraged loans is higher than that right now. The Guggenheim Active Allocation Fund invests in these and similar securities and uses leverage to control more securities than it could solely with its own equity capital. The fund collects all the payments that it receives from the assets in its portfolio and combines them with any money that it realizes from capital gains through either common stock or fixed-income trading. Finally, the fund pays all of this money to its shareholders, net of its own expenses. We might expect that this would give the fund's shares a very high yield.

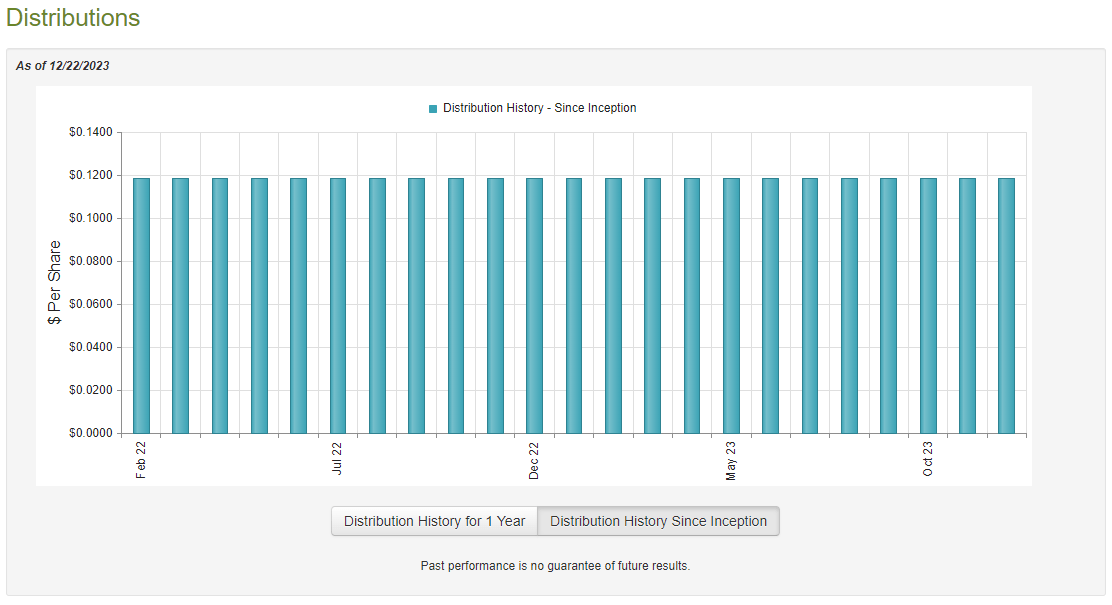

This is indeed the case, as the Guggenheim Active Allocation Fund pays a monthly distribution of $0.1188 per share ($1.4256 per share annually), which gives it an impressive 9.97% yield at the current share price. This is reasonable for a debt closed-end fund right now, although it is not the absolute best yield that can be found. The fund has been remarkably consistent with respect to its distribution over the years:

{kind=link}

This is a much greater degree of consistency than we usually find with closed-end funds, especially ones that weight their assets to fixed-income assets. This is at least partly because the rapid increase in interest rates in 2022 and early 2023 caused most bond funds to take very severe losses. However, as we have already seen, the Guggenheim Active Allocation Fund is capable of investing in bank loans and funds that had sufficient exposure to those securities were generally able to avoid losses over the past three years. However, the fact that the fund's investors saw a negative return since its inception suggests that the fund itself did take losses despite not cutting its distribution. As such, we want to investigate this fund's finances in order to see how well it has handled the past few years. After all, if the fund's distribution is too large and is destroying its net asset value then it indicates that it is highly unlikely to be sustainable and could result in some large distribution cuts later on. This is the last thing that we want as income-seeking investors.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on May 31, 2023. As such, this report will not include any information about the fund's performance for the past six or seven months. This is quite disappointing as many things have happened during that period. In particular, the market began to accept the Federal Reserve's "higher for longer" mantra over the summer and drove long-term interest rates up. That almost certainly caused the fund to take some losses, as the price of bonds moves inversely to interest rates. The report will also not include any information about how well the fund was able to take advantage of the recent rally in bonds that started around the middle of October. Thus, we are missing two periods that could have had a significant impact on the fund's finances. We will probably have to wait until the second half of January to get an updated financial report that includes information about more recent events. For now, we will have to go with what we have in the annual report and track the fund's net asset value to determine how sustainable its distribution is likely to be.

During the full-year period, the Guggenheim Active Allocation Fund received $40,780,589 in interest and $3,542,106 in dividends from the investments in its portfolio. This gives the fund a total investment income of $44,322,695 during the full-year period. The fund paid its expenses out of this amount, which left it with $26,140,913 available for shareholders. That was, unfortunately, nowhere near enough to cover the distributions that the fund paid out over the period. The Guggenheim Active Allocation Fund paid a total of $46,996,618 to its shareholders over the period. This may be concerning at first glance since we normally prefer a debt fund to fully cover its distributions with net investment income. This fund obviously failed miserably at accomplishing that task.

However, there are other methods through which the fund can acquire the money that it needs to cover the distributions. For example, it might have been able to realize some capital gains from the common stocks that it has in its portfolio. It can also exploit the bond price swings that accompany changes in interest rates to achieve realized capital gains. Realized capital gains are not considered to be investment income, but they clearly do give the fund money that can be paid out to the shareholders.

Unfortunately, this fund failed to generate sufficient capital gains to cover its distributions. During the full-year period, it reported net realized losses of $1,008,866 and had another $32,248,518 net unrealized losses. Overall, the fund's net assets declined by $54,107,970 after accounting for all inflows and outflows over the period. This is obviously a bad sign that strongly suggests that the fund cannot afford its distributions and is destroying its net asset value by not cutting the payout.

Fortunately, it has managed to do a bit better since the end of the reporting period. As we can see here, the fund's net asset value per share is up 4.60% since June 1, 2023:

{kind=link}

This tells us that the fund's investment portfolio delivered sufficient returns to cover all of the distributions that it has paid out since the reporting period ended with money left over. If it can sustain its recent performance, it may be able to avoid a distribution cut. As already discussed though, there is a real possibility that it will not be able to sustain its recent performance unless it is actively realizing gains so there is still a risk, and we need to keep an eye on the fund and the market environment.

Valuation

As of December 21, 2023 (the most recent date for which data is currently available), the Guggenheim Active Allocation Fund has a net asset value of $16.57 per share but the shares currently trade for $14.29 each. That is a 13.76% discount on net asset value at the current price. This is not as good as the 14.13% discount that the shares have had on average over the past month. However, as I have pointed out in numerous previous articles, a double-digit discount is generally a reasonable price to pay for any closed-end fund that is managing to achieve its objectives. As such, the current price is not a bad entry point for those investors who want the fund.

Conclusion

In conclusion, the Guggenheim Active Allocation Fund is an interesting fund that can invest in either debt or equity securities. It appears to have a strong emphasis on debt investing though, so we should probably treat it as a debt fund. It does reasonably well at that task, although the current allocation is exposing it to a significant amount of interest rate risk. As such, it might be a good idea to hold the fund alongside a good floating-rate fund to protect yourself against the risk that the Federal Reserve will not cut rates to the degree that the market is currently expecting. The fund has struggled to maintain its distribution in the past, and it appears that even now it is dependent on the fund's ability to earn capital gains. As such, there may be a risk of a distribution cut if the market corrects at some point next year. Overall, though, this fund is still better than some other debt funds.

For further details see:

GUG: Not Perfect, But Still A Decent Way To Invest In The Debt Markets