GXO - GXO Logistics Stock Remains A Buy On Market Opportunity (Rating Downgrade)

2023-11-27 16:44:06 ET

Summary

- GXO Logistics, Inc. Q3 financial results showed modest revenue growth and limited translation to the bottom line due to softness in the consumer-related business.

- Positive factors include improved cash flow performance, contract wins for future revenue growth, and ongoing M&A activity.

- GXO Logistics guides for weaker organic growth but maintains strong adjusted EBITDA and cash flow conversion, indicating resilience in the face of macroeconomic challenges.

In September, I started covering GXO Logistics, Inc. (GXO). Back then, I marked the stock a strong buy, but also noted the company’s financial performance as well as noting that its stock price performance is heavily subject to the macroeconomic environment. That obviously holds for all companies, but I think it even more holds for companies in the freight and logistics industries. As a result, we might also be seeing some additional risk impacting the stock prices. In this report, I will be discussing the Q3 2023 results and provide an updated assessment on the stock.

Q3 Financial Results Good, But Macroeconomic Pressures Radiate

{kind=link}

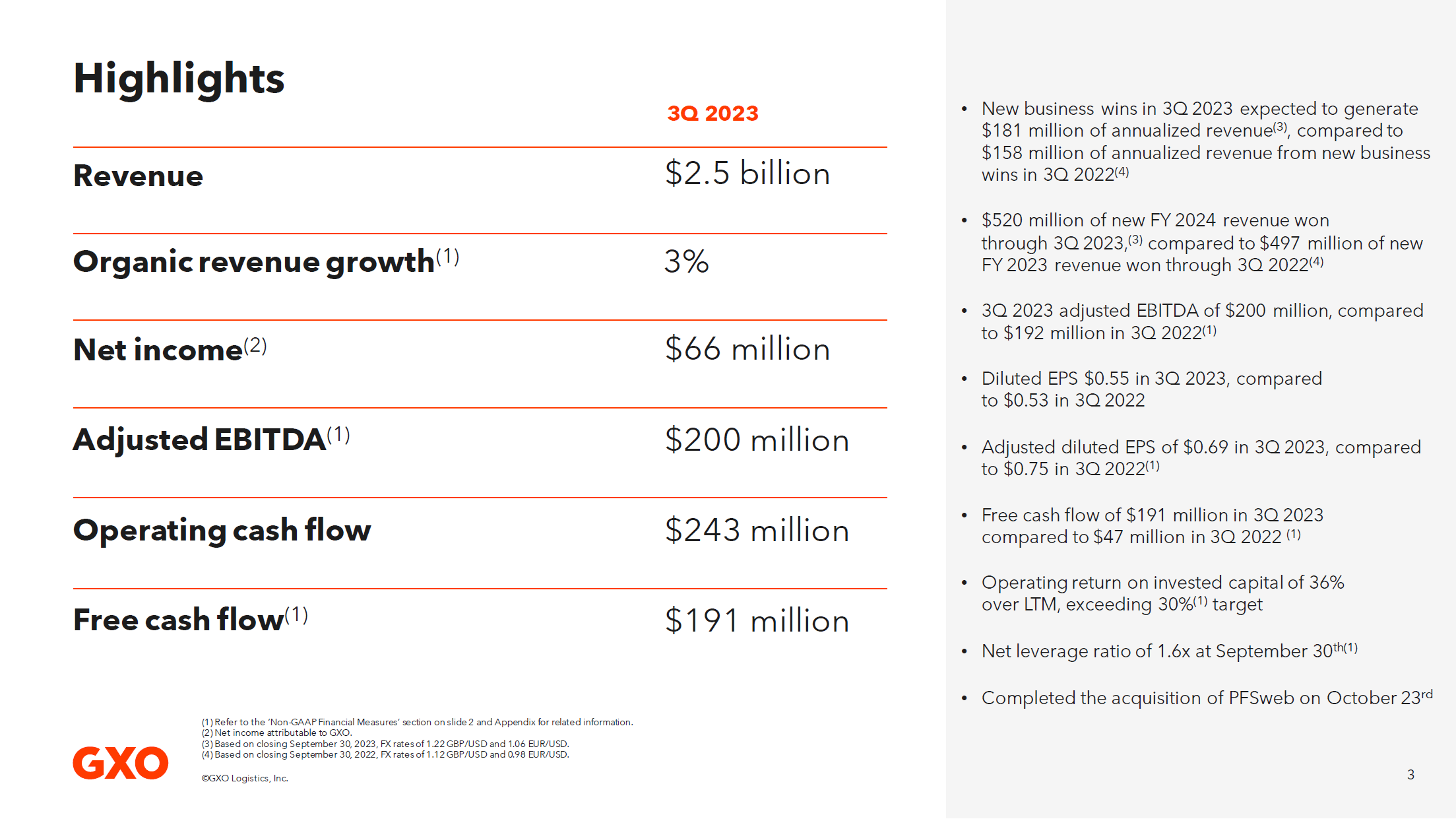

In the third quarter , revenues increased 3% organically, with a total of 8% revenue growth to $2.5 billion. Direct operating expenses, which are the biggest cost item for GXO Logistics, increased 6.7% from $1,885 million to $2,012 million but were lower than the revenue growth providing a better cost amortization profile. Operating income grew 25% to $90 million but due to lower other income and higher interest expenses this year, the earnings before income taxes were unchanged year-over-year and net income grew only 4.7% to $66 million. Year-over-year, adjusted EBITDA grew 4.2% to $200 million.

So, overall we do not see an appreciable translation to the bottom line. That is caused by softness in consumer-related business offsetting strength in technology, aerospace, and food services.

Is It All Bad For GXO Logistics?

{kind=link}

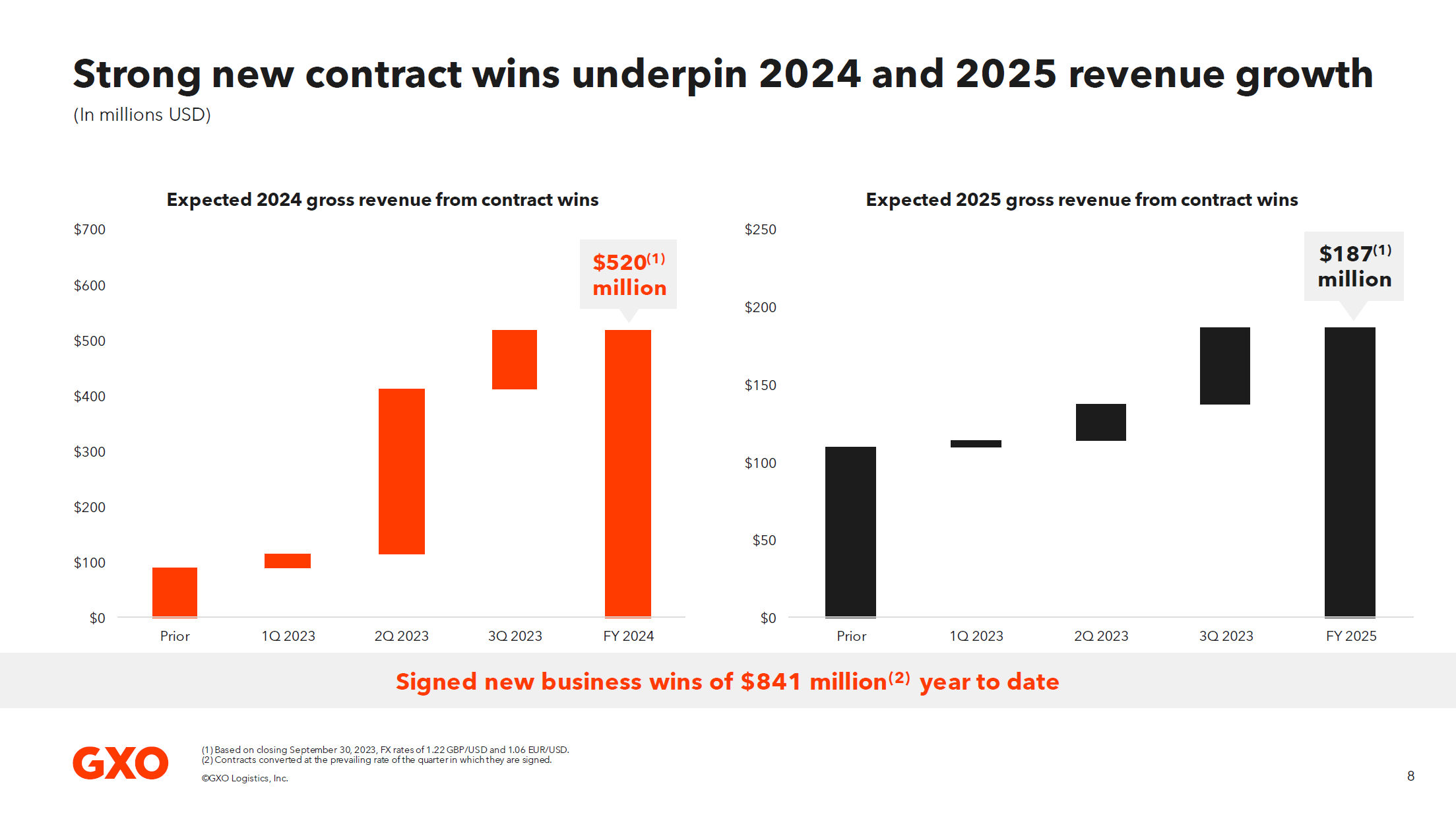

The revenue growth rate was not where it should be if GXO wants to reach its targets I discussed previously, and the translation to the bottom line was also not quite favorable. There are, however, positives. First of all, within the quarter the cash flow performance was significantly better year-over-year, with operating cash flow of $243 million, up from $116 million last year, while free cash flow of $191 million was up from $47 million last year. So, those are very good results. Furthermore, the contract wins booked this year translate into $520 million higher revenues, and for 2025 we are seeing $187 million in new contract win revenues. Not all business is recurring, but with average contract length of five years, the strong contract wins layer in nicely with the strong multi-year growth ambitions.

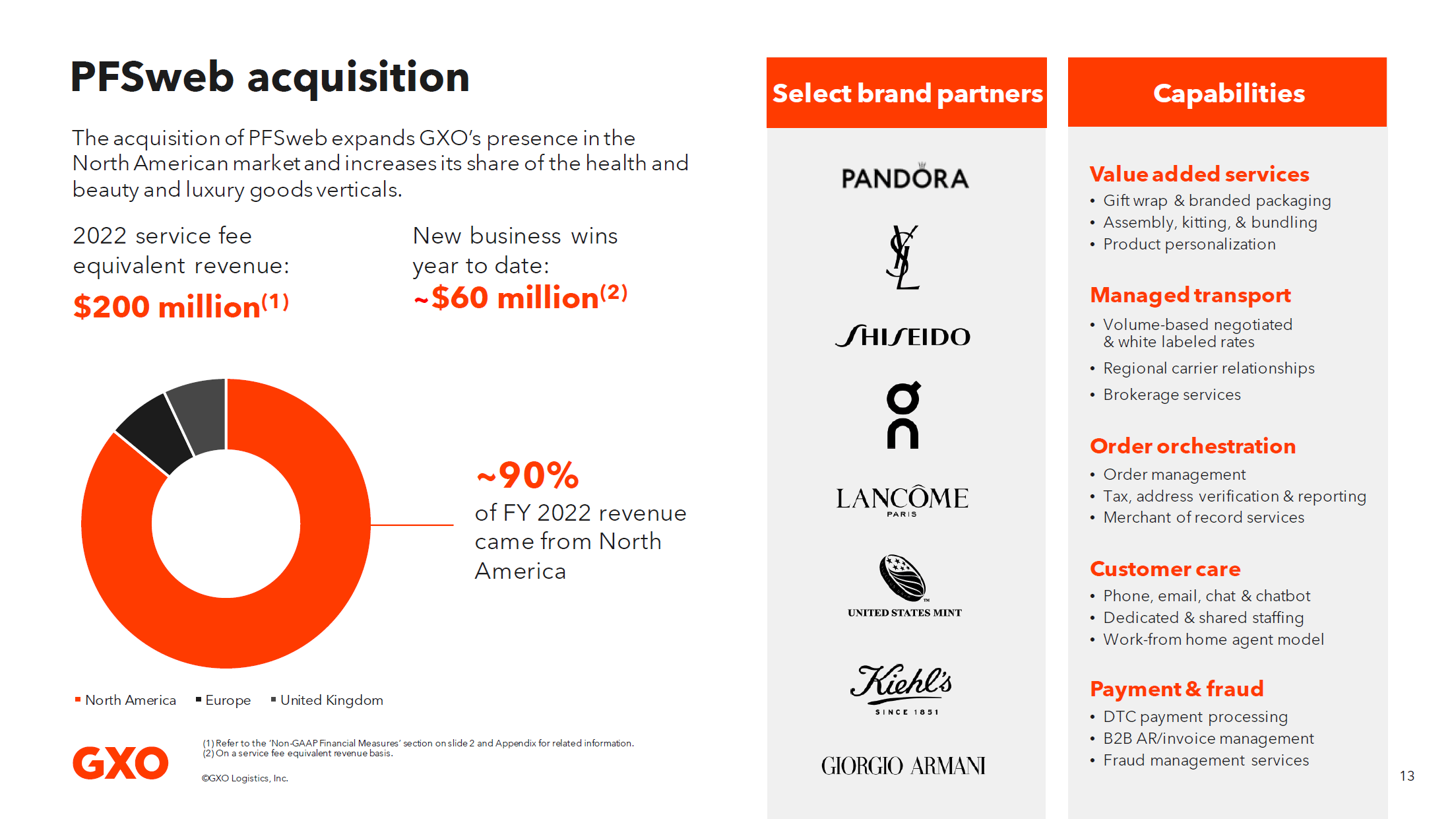

GXO Logistics Completes PFSweb Acquisition

{kind=link}

Another sign that not everything is bad is the fact the company continues its M&A activity, which I believe is key to the company’s ability to achieve its growth targets. The acquisition of PFSweb for $181 million is an example of that, giving the company increased presence in the health, beauty and luxury segments.

The acquisitions are not going to shield the company from macroeconomic headwinds, but they most certainly can be nice diversifications in terms of end market and geographical location and provide higher chances to increase revenue streams meaningfully in the growing end markets. If GXO would be viewing the soft macroeconomic environment as a major challenge for its business, it would have certainly toned down the M&A activity. The fact they have not shows me the current weakness is something that is inherent to the business.

GXO Logistics Guides For Weaker Growth

{kind=link}

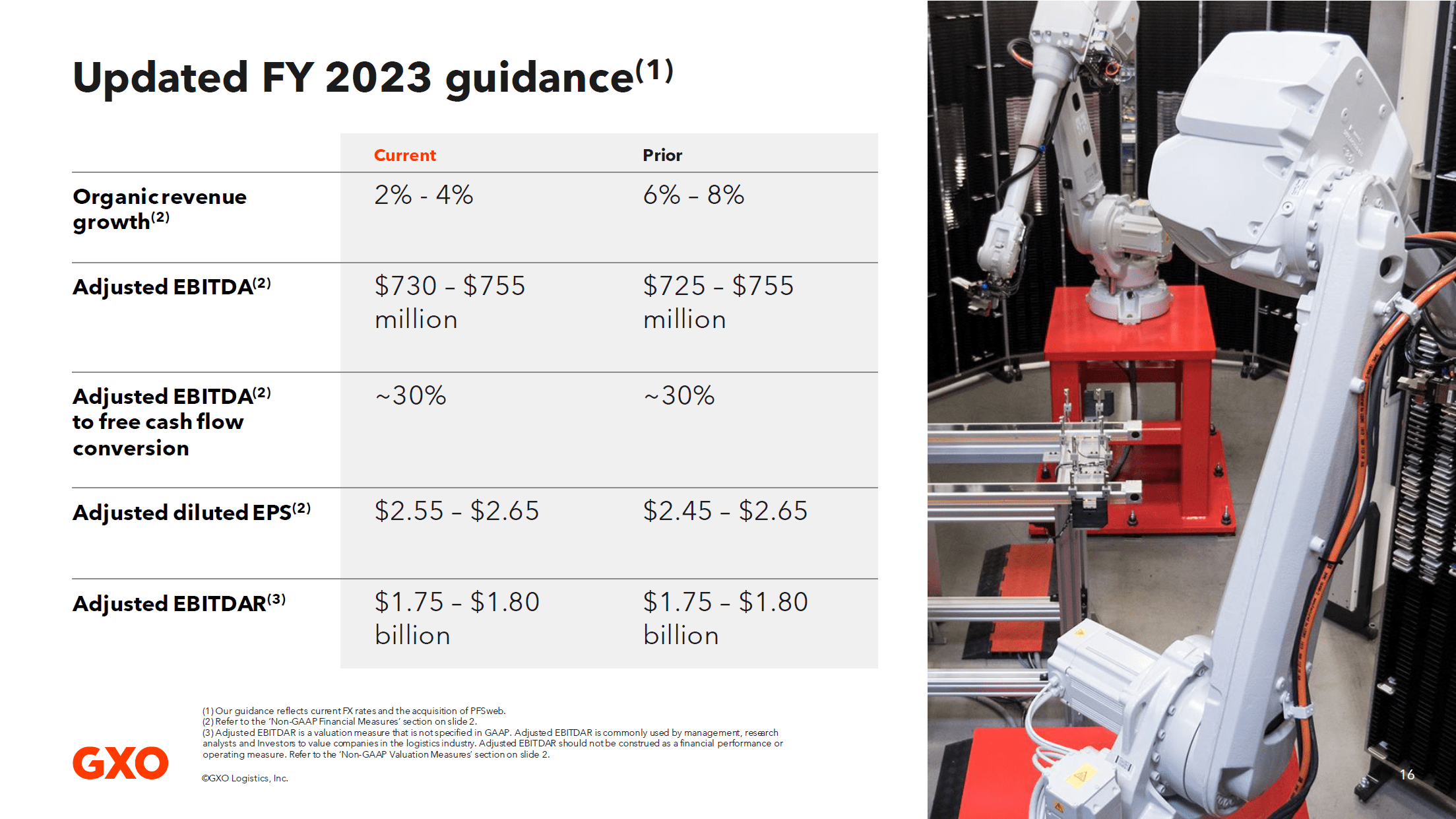

For the full year, GXO Logistics is guiding for weaker organic growth, and the reason is that there is lower demand in consumer lines. As I pointed out previously, the contract setups used by GXO somewhat shield the company from demand reductions. 45% of the business is done via open-book or cost-plus, where costs of variable and fixed revenue plus a mark-up are totaled, against which a variable and fixed cost component is subtracted. In case the volumes go down, the mark-up and fixed revenues remain the same while the variable revenues and costs go down. On higher volumes, this means slightly lower margin due to the fixed component profit being amortized over a higher volume. Vice versa, on lower volumes the margins expand slightly from the baseline.

Half of the business works with hybrid contracts where the same fixed and variable components are present, but instead of a mark-up providing the business with a profit, the margin is provided by a margin achieved on the fixed and variable cost.

In some way, you could say that we are seeing the shielding nature of the GXO’s book also back in the guidance as the organic revenue growth has been dialed back but the adjusted EBITDA and associated cash flow conversion have remained virtually unchanged. The decrease in organic revenue growth is caused by lower expected volumes during the holiday season, as the business is focusing on maintaining price rather than surging volumes and some business is also not returning in the Christmas season due to the lower expected volumes for the fourth quarter.

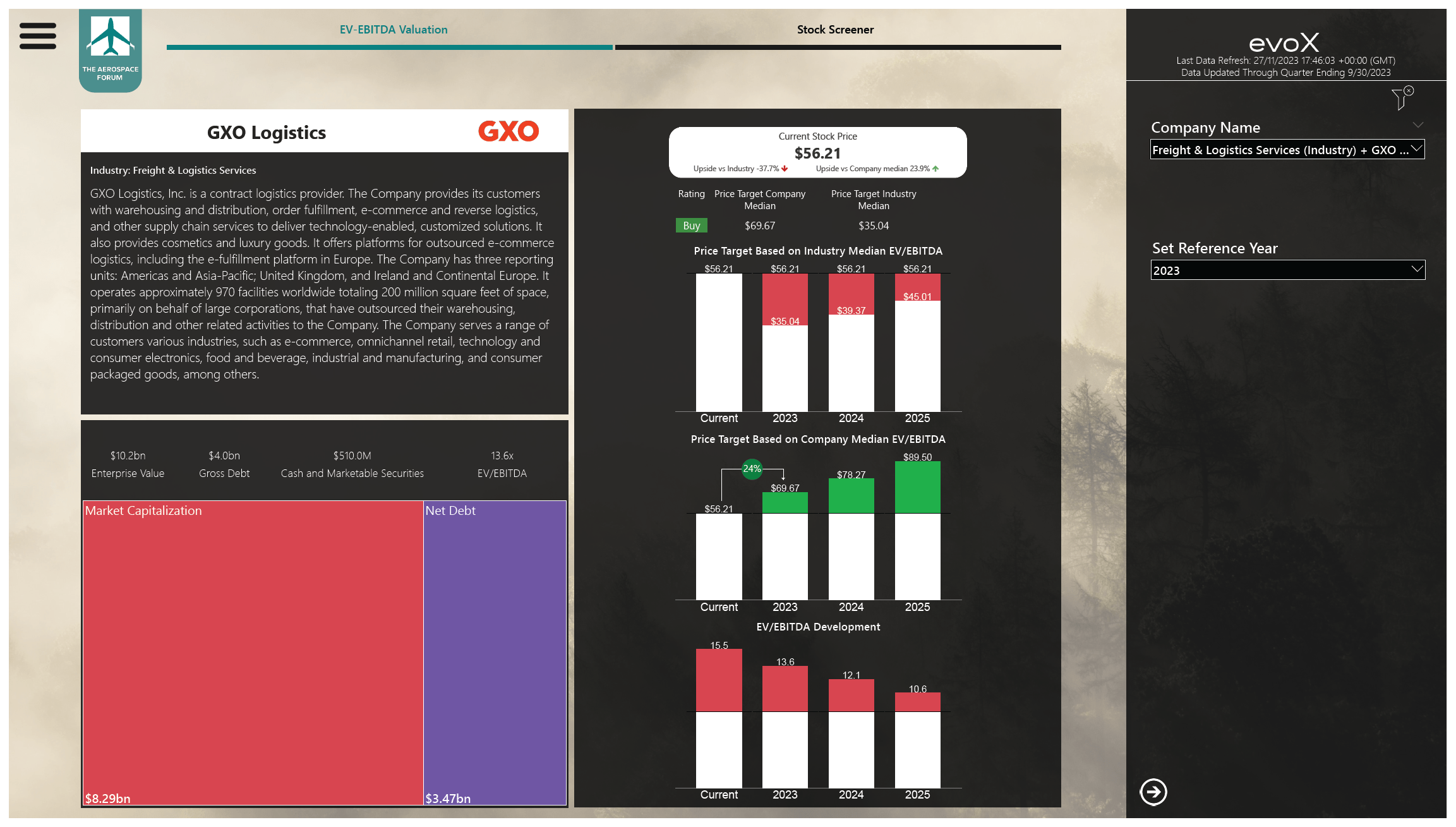

What Is GXO Logistics Worth?

I previously put a strong buy rating on shares of GXO Logistics stock, but the stock lost around 5% of its value while the broader markets gained 2%. I would say that the macroeconomic headwinds put some pressure on logistics stocks even if the margins are holding up relatively well.

For 2023, the estimates on EBITDA has not changed much and actually improved modestly, while free cash flow generation is expected to be 5% lower. For the 2023-2025 timeframe, EBITDA estimates have come down 2.3% while free cash flow estimates have come down by 12%, which I would attribute to an initial free cash flow conversion estimate in 2025 that was unusually high.

{kind=link}

Compared to sector peers, GXO stock has no upside. However, I do not believe that there is a proper justification to have the company trade in line with peers as it has significant growth opportunities ahead and it aims to solve some of the industry’s challenges. So, using the median EV/EBITDA, I believe there is 24% upside with a $69.67 price target, which is in line with the $68.25 average price target from Wall Street analysts.

Conclusion: GXO Logistics Stock Remains A Buy

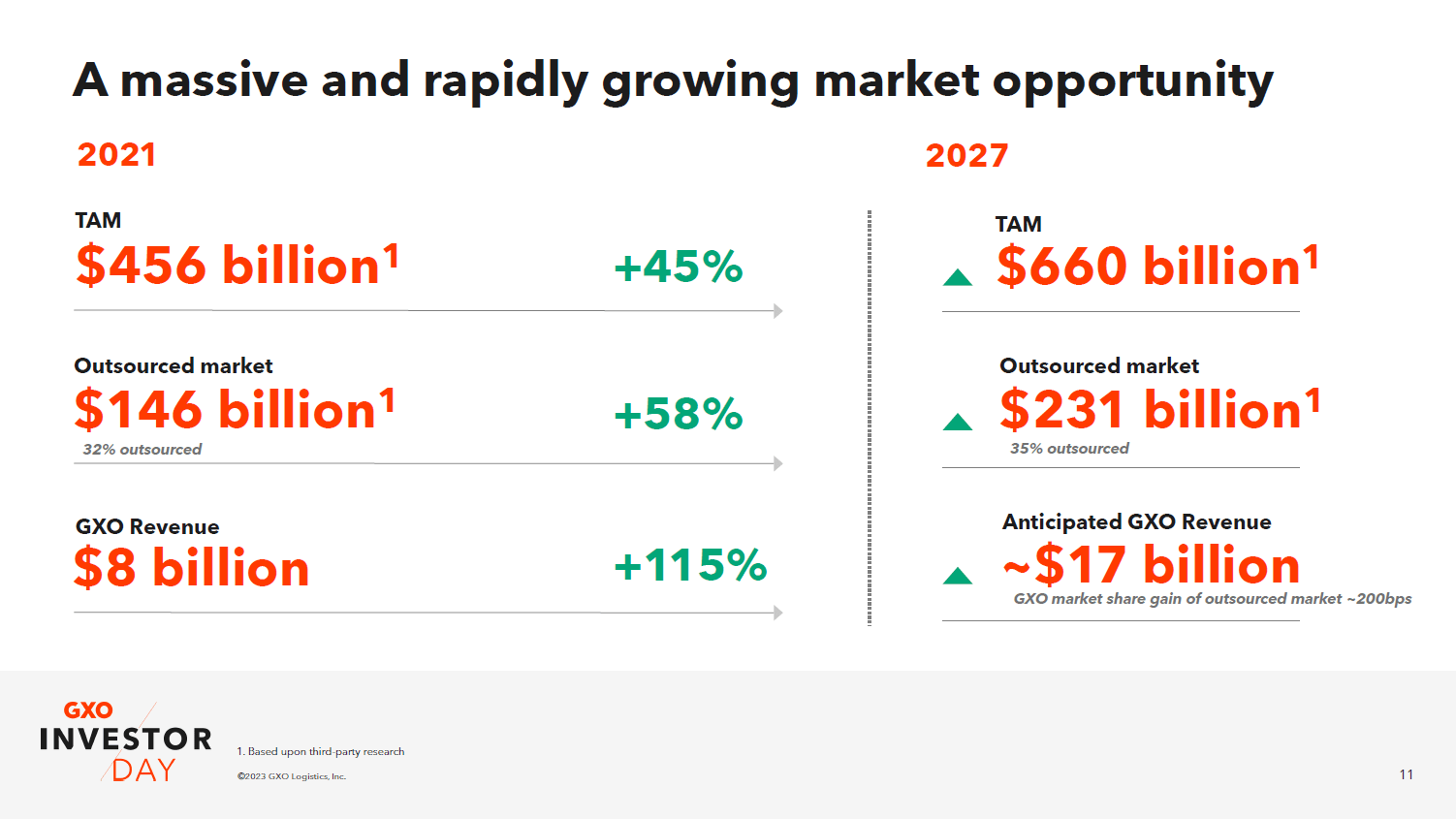

I previously assigned a strong buy rating. In recent months, I have developed a scoring mechanism that assigns a rating. Using this scoring formula, GXO Logistics is a buy rather than a strong buy, but we see significant opportunities ahead for the stock to appreciate in the years ahead and even beyond our current projections on a total addressable market of $660 billion by 2027.

{kind=link}

For further details see:

GXO Logistics Stock Remains A Buy On Market Opportunity (Rating Downgrade)