ASOMF - H&M: Potential Pitfalls In Its Growth Story

2023-08-23 00:45:54 ET

Summary

- H&M's fast fashion business model has allowed the business to achieve healthy growth in the last decade, although margins declined as its competitive position is challenged.

- With new e-commerce retailers such as Shein, H&M is struggling to compete on price and choice.

- The fundamental nature of H&M remains attractive due to its breadth of brands, global scale, and strong supply chain. This said the scope for outperformance is minimal.

- H&M's financial performance relative to peers is poor, implying the business is not overly attractive within the industry.

- For this reason, we do not consider this a good investment despite H&M appearing cheap.

Investment thesis

Our current investment thesis is:

- H&M has seen a decline in its competitive position, owing to the rise of retailers such as Shein and the e-commerce trend in general. Further, its brand association with fast fashion is unlikely to support a resurgence in growth, as consumers become more sustainably conscious.

- This has contributed to a decline in margins and softening growth. We suspect the business will continue to underwhelm.

- H&M looks unattractive relative to its peers, with lower margins and growth. For this reason, we do not believe H&M's low valuation is attractive.

Company description

Hennes & Mauritz AB (H&M) ( HNNMY ) is a well-established Swedish multinational clothing retail company. It is renowned for offering fashionable and affordable apparel, footwear, accessories, and cosmetics.

{kind=link}

Share price

H&M's share price performance in the last decade has been disappointing, losing over 50% of its value while the S&P 500 has made impressive gains. This is a reflection of worsening financial performance and threats to its strong commercial position.

Financial analysis

{kind=link}

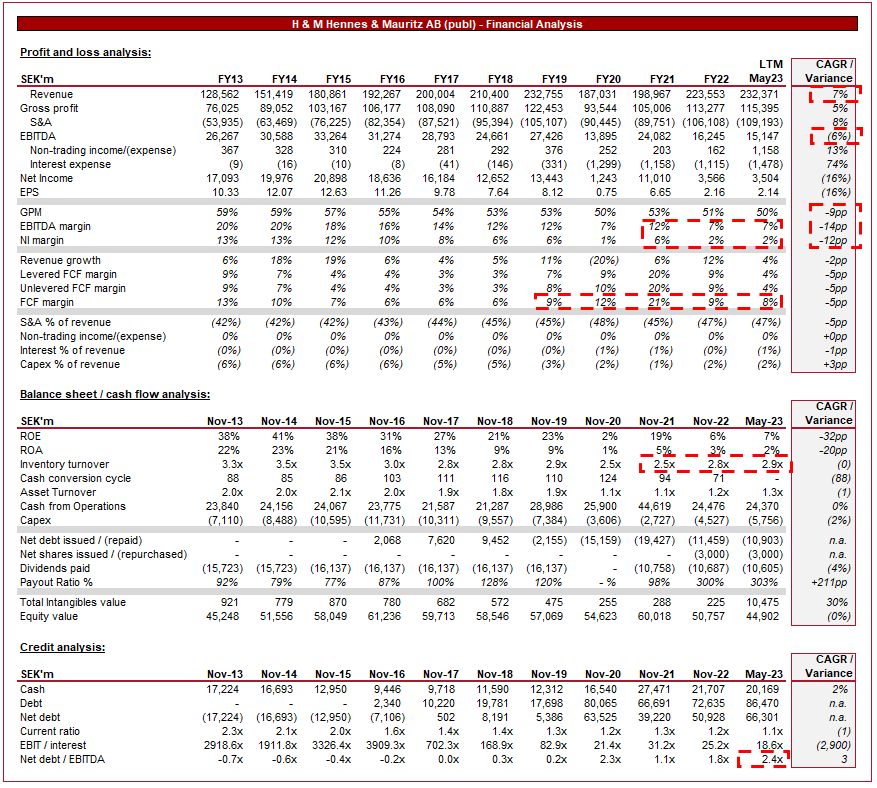

Presented above is H&M's financial performance in the last decade.

Revenue & Commercial Factors

H&M's revenue has grown at a CAGR of 7% during the last 10 years, with only a single period of negative growth (pandemic impacted). This consistency is an impressive accomplishment and evidence of inherent strength in its business model.

Business Model

H&M operates on a fast fashion model, which involves quickly producing and distributing new fashion collections in response to current trends. This allows the company to offer a constantly refreshed assortment of clothing and accessories to attract customers looking for the latest styles. Below this, H&M operates a range of brands, all targeting different segments of the wider apparel market.

"Fast fashion" was born from two complementary developments. Firstly, the availability of global supply chains utilizing low-cost labor has allowed the likes of H&M to mass-produce items and move them around the globe quickly. Secondly, the rise of the internet and social media has contributed to a harmonization of interests around trends and hype, with consumers increasingly liking and desiring the same types of things. We broadly expect this to remain the case and if anything, heighten in importance.

H&M offers a diverse range of products for men, women, teenagers, and children, as well as home textiles. Further, H&M has a strong international presence, with stores in numerous countries around the world, utilizing universal designs across regions. This works due to the homogenization of interests discussed previously. This broad coverage allows the business to maximize its consumer reach, leverage the value of its brand, and generate economies of scale. H&M's pricing strategy appeals to price-conscious consumers who want to stay stylish without breaking the bank.

Furthermore, H&M has expanded its ability to reach consumers, creating a loyalty scheme via an app, with a strong e-commerce offering. This omnichannel approach allows customers the convenience of shopping both in-store and online while encouraging greater frequency through rewards.

A key operational competency is H&M's investment in design and trend forecasting to create collections that align with current and upcoming fashion trends. A key risk to the business model is the ability to remain interesting to consumers and thus far, H&M has performed well, as evidenced by growth. Its size acts somewhat as protection, as H&M is able to flexibly adjust to release additional products in response to hype items.

Competitive Positioning

H&M faces competition from various players in the fashion retail sector, such as Inditex's various brands ( IDEXY ), Uniqlo, Forever 21, Abercrombie & Fitch ( ANF ), Urban Outfitters ( URBN ), and many others.

H&M's ability to quickly adapt to changing fashion trends and offer on-trend products inherently maintains its strong competitive positioning, so long as consumers desire the designs of the leading fashion houses. We have no concerns about H&M's ability to successfully innovate over time.

H&M's focus on youth and teen fashion, in particular, should position the business well long term, contributing to strong brand value and the development of products across age demographics.

Current economic conditions, which we will explore in detail later, are contributing to financial hardship for many, particularly those in the working/middle classes. This is part of a broader period of stagnation for many, which commenced following the GFC. A continuation of this has the potential to increase H&M's TAM as more individuals seek affordable apparel.

H&M's scale allows the business to partner with designers, celebrities, and brands to create hype and excitement around H&M's collections, attracting new and existing customers. This can be strategically utilized to support growth and brands.

Thus far, this paper has been broadly positive, so why has H&M declined? We believe it is because the traditional "fast fashion" model is dying... which is to say innovation has replaced it and outsized growth is likely gone.

Firstly, the major issue with fast fashion is the environmental and social impact, as low-cost labor and materials are utilized to produce the items. Further, many of these items are seen as disposable, contributing to greater wastage. Although H&M has innovated in response to this, using recycled materials in its production and allowing consumers to trade in their items, the impact has not been felt. According to research by McKinsey , " When consumers are asked if they care about buying environmentally and ethically sustainable products, they overwhelmingly answered yes". Despite improvements by H&M, its brand remains synonymous with fast fashion (which is why its development of other brands is a strategic imperative for Management).

Furthermore, fast fashion has seemingly been replaced by what we are calling "faster fashion". This is the fast fashion model on steroids, pioneered by the likes of Boohoo ( BHHOF ), ASOS ( ASOMF ), and others, and perfected by the likes of Shein. These businesses have further reduced the quality of products, focused purely on e-commerce to minimize costs, increased the number of SKUs, and dramatically reduced prices. This has left the fast fashion brands in limbo, unable to compete on price due to their fixed overheads and faced with the inability to match the breadth of products.

Although these two seem slightly contradictory, we believe there is a convergence in issues. Those who are ultra-price-conscious are increasingly shopping at other retailers (such as Shein), while others a (more design focused) are less motivated to shop with H&M due to sustainability concerns.

Broadly, we believe H&M is still highly competitive within its fast fashion segment but has lost ground in the wider apparel industry. This has contributed to competitive pressures, forcing prices down.

Economic & External Consideration

Current economic conditions represent near-term issues for the business. With an extended period of high inflation and elevated rates, consumers are reducing their discretionary spending to protect their finances.

H&M has performed modestly during this period, with revenue growth in the most recent quarter at 5.7% with GPM down 1.1%. This revenue resilience is a reflection of scale expansion across its portfolio, increased discounting, and resilience of its business model.

We conservatively suggest further growth is possible, but uncertain due to economic conditions.

Margins

Margin development has been the biggest issue for H&M, with EBITDA-M declining by 14ppts while NIM has fallen by 12ppts. This is why its growth is deceiving, as it is partially fueled by a declining GPM.

This margin erosion is a reflection of its declining competitive position during this period, fueled by a fall in GPM, a change in brand mix, and an increase in S&A spending.

Margins will likely normalize, at a minimum, within this current EBITDA-M range of 7-12% we feel. However, we are not overly confident of improvement going forward, owing to the high level of competition in the industry.

Balance sheet & Cash Flows

H&M's inventory turnover has returned to its pre-pandemic levels (as has CCC), implying any further FCF improvement will come from profitability. H&M currently has a FCF-M of 8%, a respectable level to fund shareholder distributions.

Industry analysis

Apparel Retail Stocks (Seeking Alpha)

Presented above is a comparison of H&M's growth and profitability to the average of its industry, as defined by Seeking Alpha (31 companies).

H&M's performance is relatively poor we feel. Its growth over an extended period has been noticeably below the market, in part due to its size, but also a reflection of its commercial weakness.

Further, the company's margins are noticeably below the average, despite scale economies, contributing to a significantly smaller ROE.

Valuation

{kind=link}

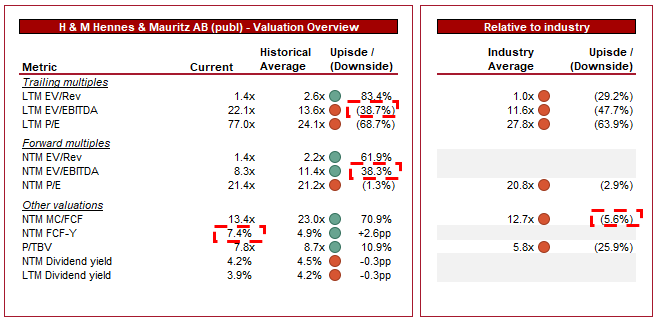

H&M is currently trading at 22x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average on a NTM basis.

Our view is that a discount to its historical average is undoubtedly warranted, primarily due to the increased competition and margin erosion during the period. At a 38% discount to its NTM EBITDA average, this does imply value.

Further, a discount to its peer group is also justifiable, given the weak financial performance. This is not the case, with a NTM premium on a FCF basis (5.6%).

Based on this, H&M is not clearly undervalued. The increased FCF yield of 7.4% is certainly tempting but given the commercial weakness in conjunction with financial decline, we believe further patience is warranted.

Final thoughts

H&M's financial performance over the last decade has been poor, as changing industry dynamics have contributed to a decline in its competitive position. We do not believe the business will experience a parallel decline in the coming years, yet its performance is unlikely to be appealing.

For further details see:

H&M: Potential Pitfalls In Its Growth Story