HALO - Halozyme: Intriguing Buy Prospect Despite This Week's PDUFA Setback

2023-09-12 17:59:16 ET

Summary

- Halozyme Therapeutics, based in San Diego, has developed ENHANZE technology based around its proprietary enzyme, rHuPH20.

- The enzyme makes it possible for many intravenously administered drugs to be administered subcutaneously instead.

- Not only is the SC method of administration quicker and easier for patients, it can help drug manufacturers extend patent protections.

- Halozyme's partners include Roche, Bristol Myers Squibb, Argenx, and many others. Revenues will exceed $825m in 2023, with positive EPS implying a forward PE of ~14x.

- An SC version of Roche's Tecentriq was due to be approved this week by the FDA, but that has been postponed, although investors should not panic. It will likely happen in 2024, alongside multiple other approvals. Halozyme Revenues can easily climb to $1.5bn -$2bn by 2030, making the bull case.

Investment Thesis

San Diego, California-based Halozyme Therapeutics ( HALO ) is a company investors ought to be paying close attention to in my view as a potentially strong buy opportunity, despite the postponement of a potentially significant share price catalyst that was set to arrive on Friday, September 15- the approval of a subcutaneous version of Roche's Tecentriq leveraging Halozyme's unique drug delivery technology.

Short-term catalyst aside (I will discuss the Roche situation in more detail below) Halozyme presents a generally attractive opportunity for investors looking to gain exposure to the lucrative, high margin biopharmaceutical industry. Halozyme's business model is described as follows in the company's Q2 2023 10Q submission (quarterly report).

Our proprietary enzyme, rHuPH20, is used to facilitate the subcutaneous ("SC") delivery of injected drugs and fluids. We license our technology to biopharmaceutical companies to collaboratively develop products that combine our ENHANZE® drug delivery technology ("ENHANZE") with the partners' proprietary compounds. We also develop, manufacture and commercialize, for ourselves or with our partners, drug-device combination products using our advanced auto-injector technologies.

rHuPH20 is a patented recombinant human hyaluronidase enzyme - as the 10Q continues:

rHuPH20 works by breaking down hyaluronan ("HA"), a naturally occurring carbohydrate that is a major component of the extracellular matrix of the SC space. This temporarily reduces the barrier to bulk fluid flow allowing for improved and more rapid SC delivery of high dose, high volume injectable biologics, such as monoclonal antibodies and other large therapeutic molecules, as well as small molecules and fluids.

Subcutaneous drug delivery is generally preferable to intravenous drug delivery as it is faster, may require less frequent dosing regimes, and may result in fewer infusion site reactions. SC delivery also offers another major advantage for pharmaceutical companies partnering with Halozyme - turning to the 10Q again:

Lastly, certain proprietary drugs co-formulated with ENHANZE have been granted additional exclusivity, extending the patent life of the product beyond the patent expiry of the proprietary IV drug.

Patent expiry is arguably the single toughest challenge faced by the Big Pharma industry - when patents expire, generic and biosimilar copies of the drugs are permitted to be marketed alongside the original, at a much cheaper price point, dragging down both the sale price and sales volume of the original.

A good example would be AbbVie's "mega-blockbuster" autoimmune drug Humira, which lost its patent protection this year. Revenues in H1'23 were $7.6bn, compared to $10.1bn in the prior year period, and to date, only one or two generic versions of the drug have been launched. By the end of 2023, there will be as many as eight generic versions of Humira on the market, some priced at an 85% discount to the original.

Pharma's are therefore desperate to extend patent protections for key drugs, and moving from an intravenous to a subcutaneous method of administration is one way to do so. For example, Pharma giant Merck ( MRK ) hopes to extend the patent life of its $20bn per annum selling cancer drug Keytruda - set to expire ~2027 - well into the next decade, thanks to a switch from IV to SC administration.

Halozyme - Business Overview & Performance

As of Q2'23, Halozyme earned royalties from six globally approved partnered products, revenues from its proprietary auto-injectors, and product sales from its specialty products. Last quarter, the company earned $112m of royalties - up 31% year-on-year - $74m of product sales - up 60% year-on-year - and $35.4m of collaboration revenues - up 71% year-on-year.

Operating income came in at $94.5m, and net income at $74.8m, whilst EBITDA was $115.1m. GAAP earnings per share ("EPS") was $0.56, and non-GAAP $0.74, annual increases of 250% and 40% respectively.

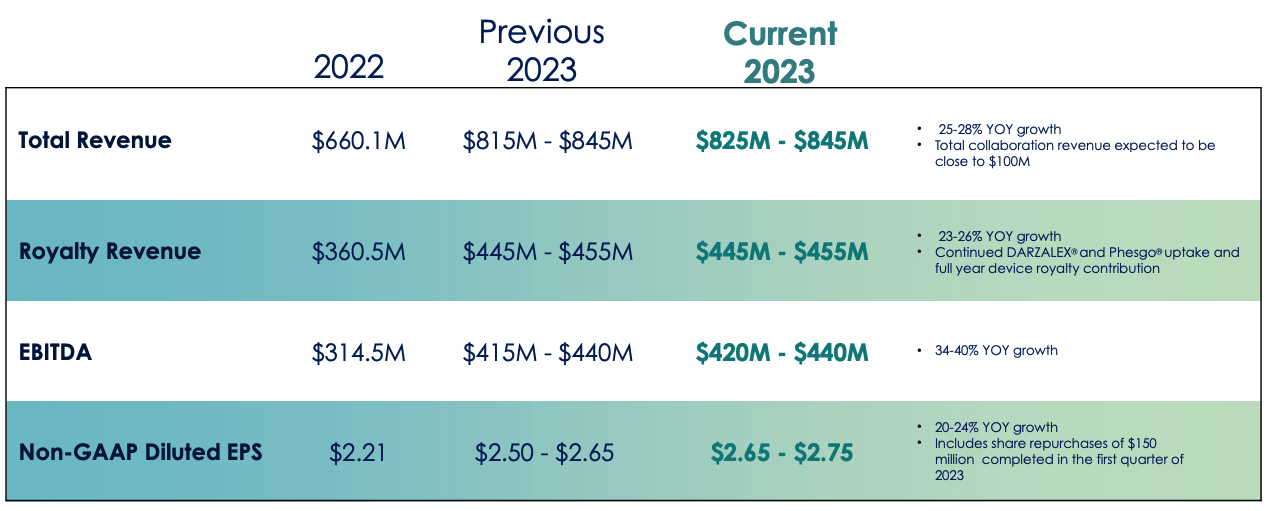

Halozyme 2023 guidance (Halozyme earnings presentation)

{kind=link}

After easily outperforming analysts' expectations in Q2'23, Halozyme raised its FY23 guidance as shown above, predicting revenues of $825-$845m, and Non-GAAP EPS of $2.65-$2.75, which translates to a forward price to sales ("P/S") ratio of ~6x, and a forward price to earnings ("P/E") of ~14x, based on current market cap valuation of $4.95bn, and share price of $37.50. Attractive numbers by the standards of any sector.

As of Q2'23, Halozyme reported current assets of $766m, including $221m of cash, and $127m of marketable securities, versus current liabilities of $116m. Long-term debt stands at $1.5bn - interest expense in 1H23 came in at $9m.

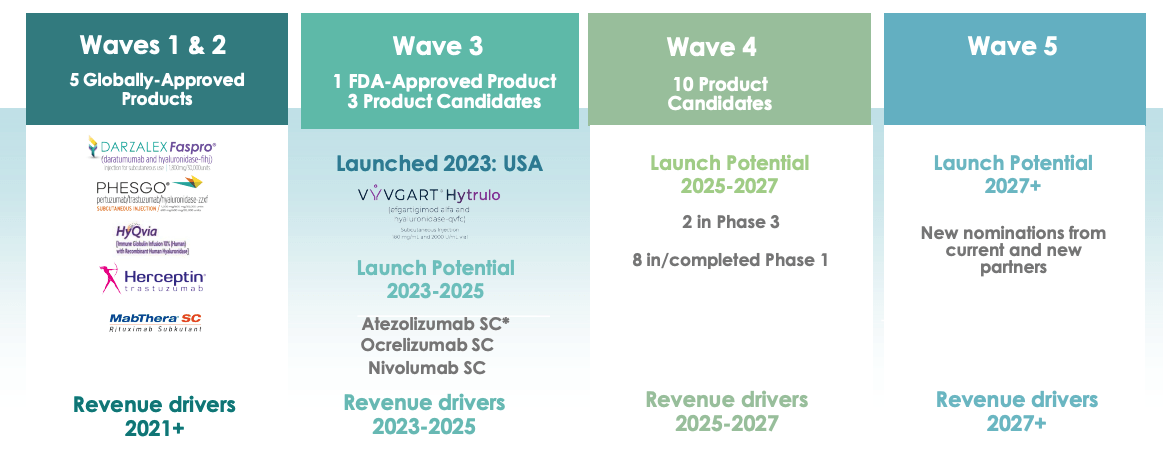

Between 2014 and 2023 Halozyme increased revenues from $75.3m, to $660m, but if anything, revenue can be even more supercharged going forward. Halozyme discusses its products and partnerships in terms of "Waves". Sitting within Wave 1 and Wave 2 are the five approved and partnered products from which the company earns royalties, which amount to an "average mid-single digit percent rate" of the product's net sales (source - 2022 annual report ).

These products are Swiss Pharma giant Roche's breast cancer therapies Herceptin - ~$2.4bn of revenues generated in 2022, and PHESGO - $775m sales, and chemotherapy, MabThera - $2.3bn sales, Japanese Pharma Takeda's HyQvia, ~$5bn sales, and Janssen's multiple myeloma therapy DARZALEX - $8bn of sales in 2022.

It's an impressive list that on its own could see royalty revenues increase substantially, given DARZALEX alone has peak sales expectations of over $13bn, but the next "Wave" of product launches also substantially enhances the value proposition.

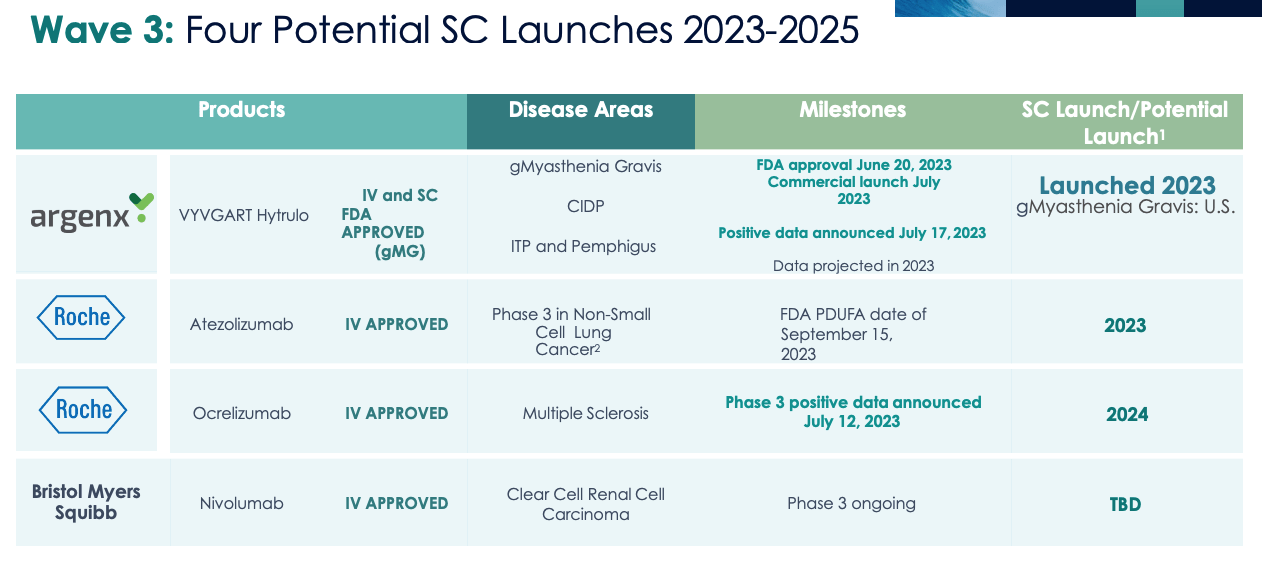

Wave 3 Breaking - Roche's Tecentriq Set To Go SC With Approval Date Upcoming This Week

Wave 3 SC partner launches (Halozyme presentation)

{kind=link}

As we can see above, the first of the "Wave 3" products - Argenx' ( ARGX ) VYVGART Hytrulo - indicated for Myasthenia Gravis - received approval for its subcutaneous version co-formulated with ENHANZE in June this year. The drug could potentially be approved in up to four more autoimmune indications as a subcutaneous therapy, and analysts have speculated revenues could surpass $3bn per annum by 2026.

The next "cab off the rank" was set to be Roche's Atezolizumab - marketed and sold as Tecentriq, this cancer immunotherapy is a rival to Merck's Keytruda. The drug has been approved as an intravenous therapy since 2016, and has secured approvals in that form in bladder, lung, and breast cancer, earning ~$4bn revenues in 2022.

Tecentriq was approved as a subcutaneous therapy in the UK at the end of August, and its Prescription Drug User Fee Act ("PDUFA") date - when the FDA rules on whether to approve the SC version for commercial use in the US - was set to arrive this Friday, September 15. The SC version of the drug with ENHANZE takes around seven minutes to administer, Halozyme President and CEO Helen Torley told analysts on the Q2 2023 earnings call , compared to 30-60 minutes for the IV treatment.

Given that advantage, and positive Phase 3 study results studies showing the SC produced similar levels of active drug in the bloodstream of patients to the IV version, an approval looked to be a formality, but at the end of last week the Swiss Pharma ruled that it still needs to make updates to its Chemistry, Manufacturing, and Controls ("CMC") before the FDA will agree to approve SC Tecentriq.

Roche has cautioned that it might not receive approval until 2024, which will be a disappointment for the Pharma as well as Halozyme, although the delay shouldn't be considered too much of a setback for either company. Typically, CMC issues are the easiest to resolve with the FDA, who have not questioned the approval on efficacy, safety, or interchangeability grounds, but on certain manufacturing concerns - usually straightforward to resolve.

Halozyme has not included any SC Tecentriq revenue contribution in its FY23 guidance, and Roche is still likely to be the first Pharma to bring a version of this type of PD-1 targeting cancer immunotherapy to market. As soon as it is approved in SC form, Roche will hope to extend the patent protection of Tecentriq beyond 2028, when it is set to expire, well into the next decade.

For its role in the switch to SC, Halozyme will likely receive an upfront milestone payment, as well as royalties somewhere in the mid-single digit percentages. Something similar will happen should Roche's Ocrevus, a ~$6.5bn selling multiple sclerosis therapy, also be approved for SC administration, which again seems likely to happen based on the positive Phase 3 data obtained.

Intriguingly, Halozyme is also working with Bristol Myers Squibb ( BMY ) on nivolumab. Marketed and sold as Opdivo, this drug is a PD-1 inhibitor like Tecentriq, although it is approved across more solid tumor indications, and it generated revenues of over $8bn last year. Doubtless, BMY will be looking to extend the patent life of one of its most important drugs with an SC version, and it is tempting to wonder if Merck will choose Halozyme as its partner when looking to do similar with Keytruda.

To have the three most significant cancer immunotherapies - Tecentriq, Opdivo, and Keytruda - as partners would be a major coup for Halozyme that would surely push revenues and the share price skywards. To be close to already securing two out of three makes the bull case on its own, in my view. Based on revenues, the four Wave 3 products have the potential to more than double Halozyme's royalty revenues, which puts Halozyme on track for blockbuster revenue generation itself.

Looking Further Ahead - Waves 4 & 5 - & Considering Some Risks

Halozyme clearly has a product in rHuPH20 that is highly sought after - as we can see below, beyond Wave 3, there are another 10 product candidates in "Wave 4", which could be launched before 2027, and management is confident that there will be a "Wave 5" also, given how successfully the company's proprietary enzyme has proven to work with some of the world's largest pharmas.

ENHANZE's durable revenue potential (Halozyme presentation)

{kind=link}

Not only that, but Halozyme continues to innovate with its auto-injector products - granted, this is not the company's major area of focus, but still a valuable source of revenue that could surpass $500m per annum before the end of the decade, based on current growth rates. Collaboration revenue performs a similar function, and with multiple new products expected to arrive in Waves 4 & 5, further milestone payouts of over $1bn before the end of the decade doesn't seem too unrealistic a possibility.

With these kinds of growth prospects in play, and as I have already discussed, with current P/S and P/E ratios low enough to suggest Halozyme is undervalued based on performance today, in my view Halozyme has the potential to double its market cap valuation in the coming years, entering the double-digit billions. The company's share price has risen over 115% across the past five years, although it is down 34% year-to-date, after a sharp selloff following Q4'22 and FY'22 earnings results.

In my view, that seems a little harsh on the company, which is projecting over 25% year-on-year revenue growth in 2023, in a tough economic environment, while the long-term growth outlook appears exceptional, given the Tecentriq, Ocrevus, VYVGART and Opdivo opportunities.

One obvious risk to consider is that Halozyme is entirely dependent on rHuPH20 and its ENHANZE technology remaining the optimal candidate for Pharma's looking to move drugs from IV administration to SC administration to partner with.

The company did spend $960m acquiring Antares and its auto-injector products last year - a valuable source of recurring revenues - but there's no question its enzyme is its most valuable asset, and if for any reason - trial setbacks, safety issues, a rival developing a superior product - the value of rHuPH20 is compromised, Halozyme's partnerships could collapse, followed by its share price.

The biggest risk that I can think of relates to the patent expiries of rHuPH20 and ENHANZE technology. According to Halozyme's 2022 10K submission, one US patent expires in 2027, and a European patent in 2024, which could be the trigger for generic and biosimilar drug manufacturers to attempt to produce their own versions.

This could have a significant impact on Halozyme's business, although would major Pharmas - paying a modest ~5% of royalties to partner with Halozyme, feel the need to renegotiate with Halozyme's rivals? Plus it is worth noting Halozyme has multiple other patents that last longer, which could keep generics out of the market for another decade.

Concluding Thoughts - PDUFA Setback Aside, Signs Appear To Point To Revenue, Income, & Valuation Growth

Halozyme certainly has a unique business model and product which earns revenues via collaborations, proprietary product sales, and royalties, and at present, so far as I am aware, there are few rivals capable of challenging the company's technology, meaning Halozyme attracts some very notable, extremely well-resourced Pharma partners, prepared to pay attractive development milestones and royalties.

Having already secured some notable wins, and with several more major product approvals to come, the likelihood appears to be that Halozyme has every chance of doubling its royalty revenues before the end of the decade, and substantially increasing collaboration revenues and product revenues, and its share price and valuation.

Already profitable, Halozyme has been known to reward investors with generous share buyback programs, buying back ~$750m of stock across the past three years. Despite this week's setback in relation to the Tecentriq SC approval, this could actually work out well for investors, who can open a position ahead of a likely approval in 2024, alongside Ocrevus SC, and who knows, possibly Opdivo as well. That alone makes a good case for owning Halozyme stock, and as discussed above, the wait for another "wave" of approvals may not be long.

For further details see:

Halozyme: Intriguing Buy Prospect Despite This Week's PDUFA Setback