HALO - Halozyme Q3: Navigating The Ups And Downs Of Its Innovative Pathway

2023-11-15 20:26:43 ET

Summary

- Halozyme's Q3 2023 earnings showed robust performance, with a 41% YoY increase in product sales and a 15% YoY growth in royalty revenue.

- The company's strategic moves, including a $250M share repurchase plan and new partnerships, highlight its commitment to growth and shareholder value.

- Key catalysts for the stock price include potential FDA approvals, partnership agreements, product sales growth, and operational and financial performance.

- We maintain a buy rating on Halozyme Therapeutics.

Q3 2023 Earnings Summary and Royalty Income Growth

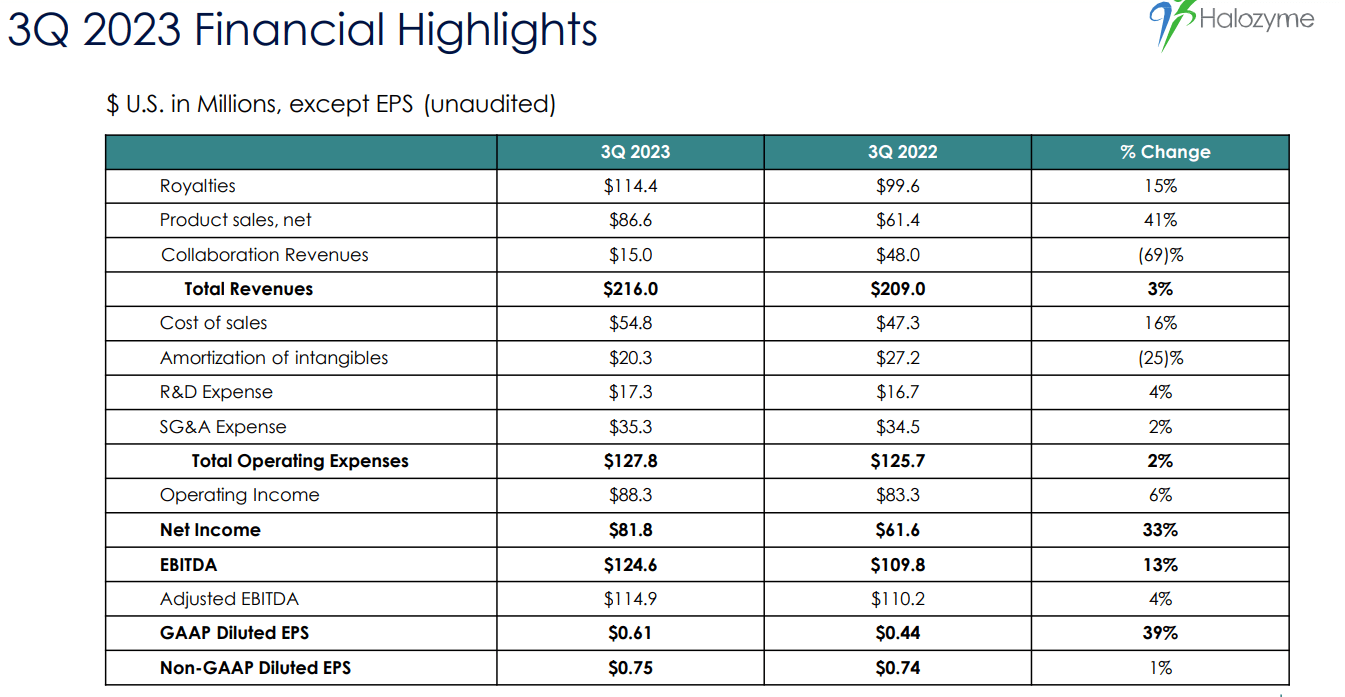

We are updating readers on our key thesis (why we are maintaining our buy rating) and Halozyme Therapeutics' (HALO) positive Q3 2023 earnings. Halozyme's Q3 print demonstrated robust performance, slightly missing consensus total revenue expectations by 1% but showcasing significant growth in other areas. The company reported total revenues of $216M, driven by a strong 41% year-over-year increase in product sales, which notably exceeded expectations. Despite a modest shortfall in royalty revenue, it still grew 15% year-over-year, indicating a healthy growth trajectory. We believe the key to this performance was the company's proprietary Enhanze technology, which enables the subcutaneous delivery of biologics and small-molecule drugs.

{kind=link}

Company IR (Company IR)

{kind=link}

Halozyme key launch metrics (Company Source)

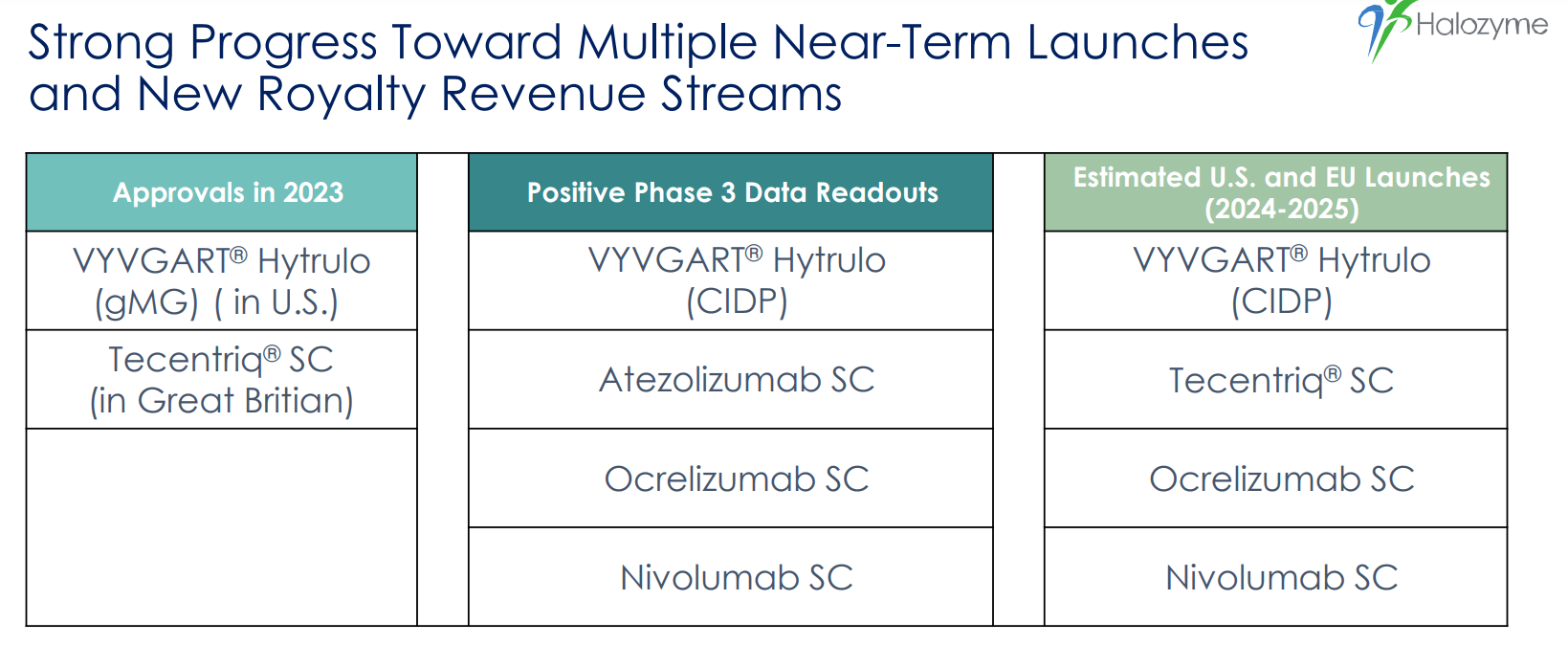

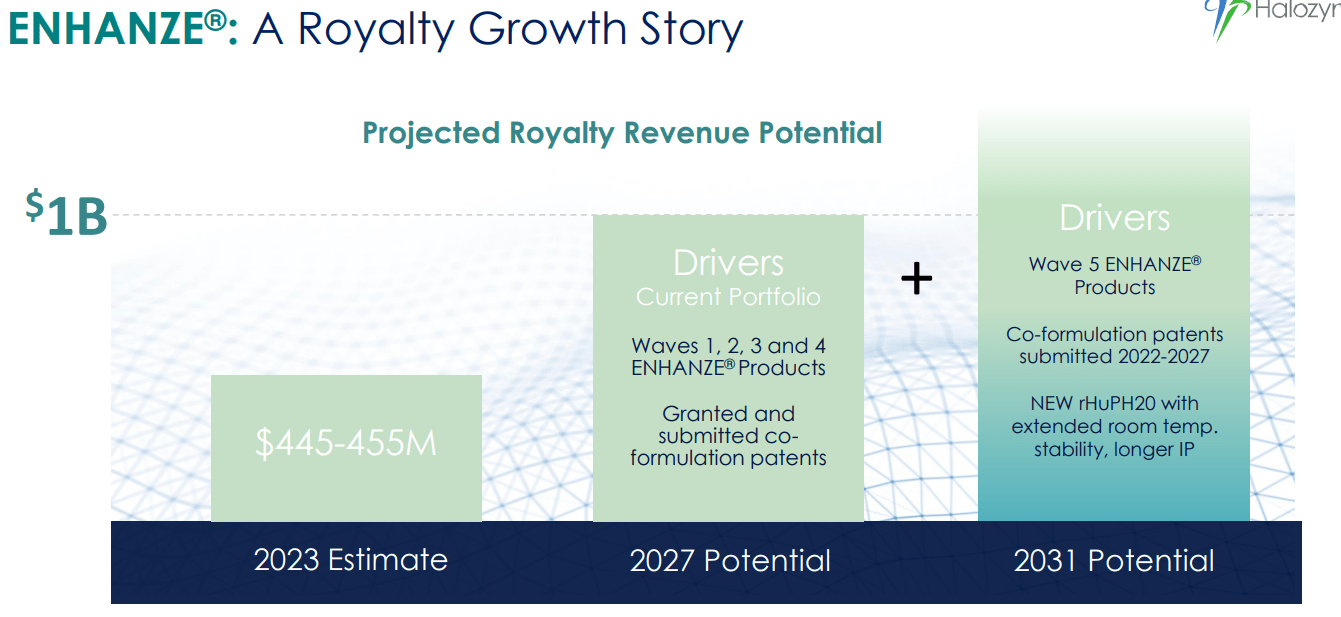

Looking ahead, the continued growth of royalty cash flow seems promising due to the expanding adoption of Enhanze technology. This adoption is expected to be further bolstered by new partnerships and the advancement of existing collaborations, which are critical drivers of growth. The upcoming catalysts, including potential FDA approvals and new partnership announcements, are likely to materially impact the stock in the future.

Recent Deals and Positive Impact

Halozyme's recent strategic moves, particularly in the realm of partnerships and share repurchases, highlight the company's commitment to growth and shareholder value. The announcement of a $250M accelerated share repurchase plan reflects confidence in the company's valuation and prospects. These actions, along with the maintained FY23 guidance and raised EBITDA and EPS expectations, underscore the company's strong financial position and strategic foresight.

During Q3 2023, Halozyme made some notable strategic moves:

-

Acumen Pharmaceuticals Deal: Halozyme announced a licensing agreement with Acumen Pharmaceuticals for ACU193, a monoclonal antibody targeting amyloid-? oligomers for the treatment of early Alzheimer's disease. This deal is significant as it extends the application of Halozyme's Enhanze technology to a new therapeutic area. However, it's important to note that this agreement is not exclusive, allowing for potential future collaborations with other biopharma companies targeting similar pathways.

-

Share Repurchase Program: Halozyme also announced a significant $250M accelerated share repurchase ((ASR)) plan. This decision reflects management's confidence in the company’s valuation and its commitment to enhancing shareholder value. By buying back shares, Halozyme is essentially investing in itself, a move often interpreted as a positive signal about the company's future prospects.

-

Potential High-Volume Autoinjector (HVAI) Partnerships: Although not finalized in Q3, Halozyme hinted at ongoing discussions and developments regarding their HVAI technology. They mentioned that one existing partner had begun clinical studies with Halozyme's HVAI, and another was considering moving into clinical studies. These potential partnerships, expected to materialize possibly in 2024, are highly anticipated as they would mark a significant expansion of Halozyme's technology application.

These strategic initiatives demonstrate Halozyme's active engagement in expanding its technology's applications, enhancing its market position, and returning value to its shareholders.

Key positive catalysts for the stock price

The key upcoming catalysts that could significantly influence Halozyme's stock price include:

-

FDA Approvals and Clinical Trial Results: The potential FDA approval of partner drugs using Halozyme's Enhanze technology is a major catalyst. For instance, the anticipated FDA approval for Roche's subcutaneous ((SC)) atezolizumab in 2024 could be significant. Additionally, Phase 3 data from ARGX's Vyvgart Hytrulo in primary immune thrombocytopenia ((ITP)) and bullous pemphigoid ((BP)) expected by year-end 2023 are crucial. Positive outcomes in these areas could lead to a surge in royalty revenues for Halozyme.

-

Partnership Agreements: The finalization of new partnership deals, especially those involving Halozyme's high-volume auto-injector (HVAI) technology, could provide a boost. The expected agreements, one for ENHANZE/HVAI and one for a small volume auto-injector, are anticipated to be significant, though there is a possibility they may shift to 2024.

-

Product Sales and Revenue Growth: Continued growth in product sales, especially for key products like Darzalex Faspro and Phesgo, can positively impact the stock. The company's ability to sustain and grow its royalty revenue streams from these products is vital.

-

Strategic Acquisitions and Share Repurchase Programs: Strategic moves like acquisitions or share repurchase programs can affect investor confidence and, in turn, stock price. For instance, the execution of the $250M accelerated share repurchase program and potential strategic acquisitions in line with the company's growth strategy could be positive signals to the market.

-

Operational and Financial Performance: Any updates or changes to Halozyme's financial guidance, especially regarding revenue and EBITDA, can influence investor sentiment. Meeting or exceeding current financial projections would likely have a positive effect on the stock price.

These catalysts represent a combination of short-term and long-term factors that could impact Halozyme's market valuation and investor perception.

{kind=link}

Company IR (Company IR)

Risks

Investing in HALO does present certain risks. These include dependency on the success of its Enhanze technology, potential market competition, regulatory uncertainties, and the eventual expiration of key patents. Additionally, the company's high dependence on its major partners for royalty revenue could be a vulnerability if there are any shifts in these relationships or the performance of partnered products.

Conclusion

Halozyme stands out as a strong buy candidate due to its innovative Enhanze technology, robust product sales, and promising royalty revenue growth. We like Halozyme's de-risked royalty-based base business and cashflow-positive nature, which we believe makes Halozyme a de-risked investment for generalist investors as well. The company's strategic partnerships and recent deal-making activities further reinforce its growth trajectory. While there are risks associated with patent expirations and partner dependencies, the company's current performance and future prospects (especially around royalty cash flow growth) provide a solid foundation for continued success. We maintain a buy rating on HALO, anticipating strong near to medium-term growth and significant potential for continued expansion in its market presence.

For further details see:

Halozyme Q3: Navigating The Ups And Downs Of Its Innovative Pathway