HBB - Hamilton Beach Brands Is Still On Sale

2023-07-18 08:22:38 ET

Summary

- Hamilton Beach Brands, a small electric household and specialty housewares and appliances manufacturer, has experienced weak sales and profit figures recently, but management's outlook for 2023 is promising.

- Despite a downturn in shares, the company's focus on cost reductions and new product offerings in the Home Health and Wellness sector, such as The Smart Sharps Bin and SixClorox True HEPA air purifiers, are expected to drive longer-term success.

- HBB stock is currently undervalued, making it an attractive investment opportunity, especially given the expected recovery in the second half of the year.

As much as I would like to say that I have a perfect track record when it comes to investing, that is sadly not the truth. Every so often, I will find a company that I believe will perform well, only for it to experience pain in the near term. Sometimes, this pain becomes more permanent. In other cases, the company will eventually rebound. Fitting into this latter category, I believe, is small electric household and specialty housewares and appliances manufacturer Hamilton Beach Brands ( HBB ). Even though sales and profit figures for the company have been weak as of late, and even though cash flow data has been discouraging, management's outlook for 2023 is promising. The company is far from being a prime prospect for investors. And those who can't stand volatility would be wise to avoid it. But given how cheap the stock has become, I would argue that a rebound in the stock price is quite probable at this point.

Assessing short-term pain

Early February of this year, I found myself taking a bullish stance involving Hamilton Beach Brands. At that time, i recognized that the company had come under pressure, with sales falling and bottom line results looking quite mixed. Even in spite of this lackluster performance, shares of the company had been performing quite well, achieving upside of 22.6% from April of last year through the time that said article was written compared to the 4.3% decline the S&P 500 saw over the same window of time. In that article , I expressed my view that further upside was likely around the corner. That led me to keep the company rated a 'buy'. Since then, the shares of the company have seen a reversal of fortune. Why all the S&P 500 has increased by 7.3%, shares of Hamilton Beach Brands saw downside of 22%.

{kind=link}

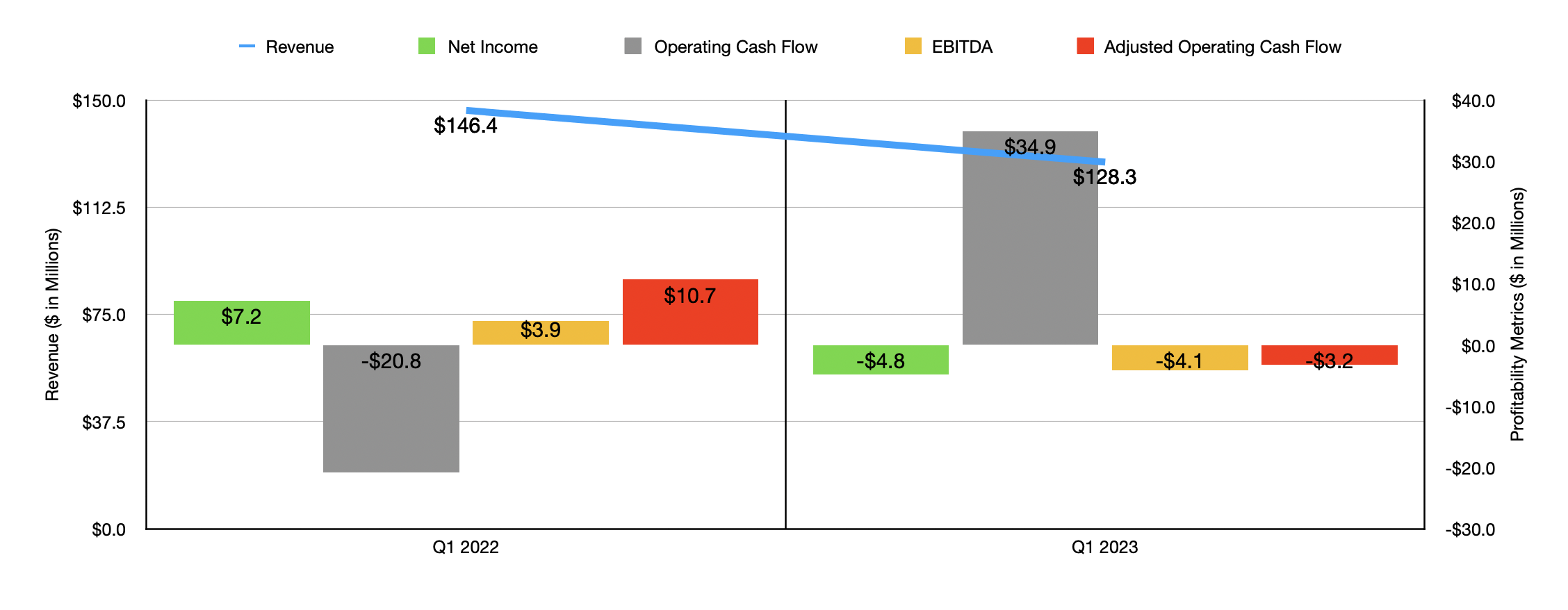

This downturn was not without cause. Though I do believe it was an overreaction. Consider how the company performed during the first quarter of the 2023 fiscal year. During that time, revenue came in at $128.3 million. That's 12.4% below the $146.4 million the business generated the same time last year. The company did benefit during this time to the tune of $4.3 million from sales price increases. However, a $22.3 million plunge associated with lower unit volume and a shift in product mix more than offset this. That volume reduction and product shift was driven by softer consumer demand trends and the decision by retailers to address their bloated inventory levels.

Naturally, in any industry where margins tend to be low, a decline in revenue can bring about a disproportionate decline in profitability. During the most recent quarter, the firm generated a net loss of $4.8 million. That compares to the $7.2 million gain experienced during the first quarter of 2022. It is true that operating cash flow for the company went from negative $20.8 million to positive $34.9 million. But if we adjust for changes in working capital, we would see that number shift from $10.7 million to negative $3.2 million. Meanwhile, EBITDA for the company went from $3.9 million to negative $4.1 million.

{kind=link}

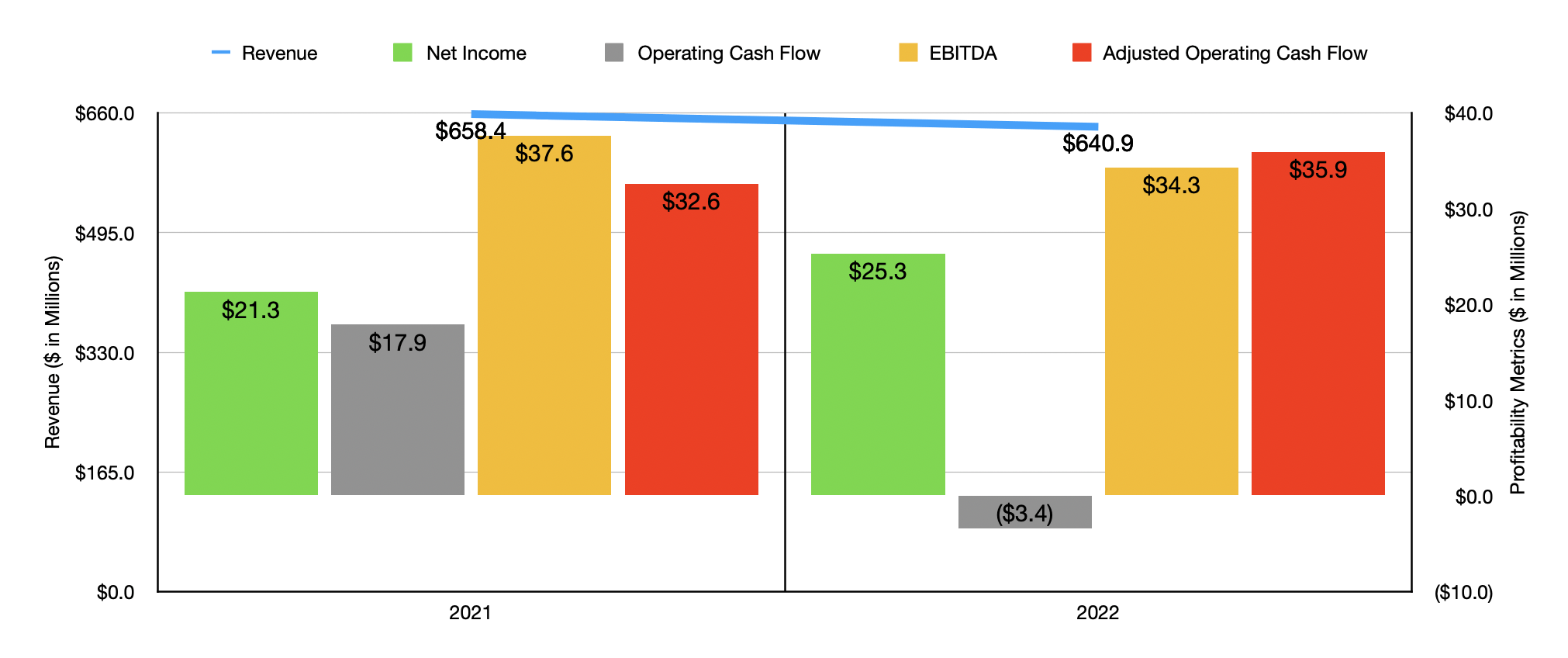

To be clear, the first quarter of 2023 was not the first time that the company has seen weakness. Consider how the business performed during 2022 compared to 2021 . Those results can be seen in the chart above. Revenue of $640.9 million was a bit lower than the $658.4 million reported in 2021. It is true that net income and adjusted operating cash flow both improved year over year. But operating cash flow and EBITDA worsened. The good news for investors is that the picture does seem to be improving to some extent. Even though management is expecting overall financial performance in the first half of this year to be problematic, the second half of the year should see better results. In fact, management is forecasting that revenue for 2023 in its entirety should be flat compared to what it was last year. Operating profits, excluding $10 million of insurance proceeds received in 2022, should actually be higher than what they were last year.

In addition to the company focusing on cost reductions, it stands to benefit from its burgeoning Home Health and Wellness offerings. In that vein, the company has introduced a variety of new products focused on this market niche, one example being The Smart Sharps Bin that is powered by HealthBeacon. The goal here is to assist with at home injection care management for customers. And what's really exciting is that the system is eligible for coverage under programs such as FSA, HSA, Medicare, and Medicaid. Another example involves the SixClorox True HEPA air purifiers and replacement filters that the company launched last year. These new initiatives, combined with the company's decision to focus on its core growth opportunities, should set the business up for longer term success.

{kind=link}

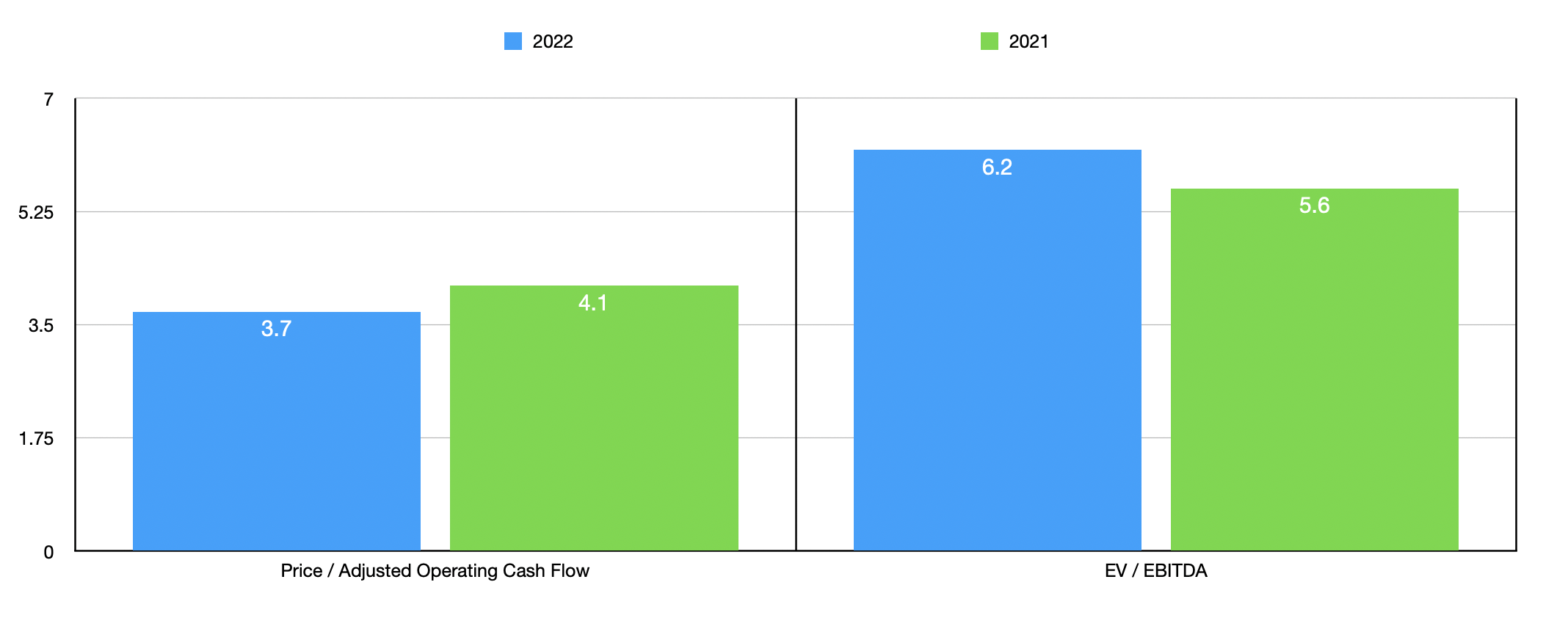

Given the forecast that management has provided, I have to assume that financial performance is unlikely to look worse than it was in 2021. In the chart above, I priced the data using both that year and 2022. On a price to adjusted operating cash flow basis, shares are trading at a multiple of between 3.7 and 4.1. And when it comes to the EV to EBITDA approach, the multiple is between 5.6 and 6.2. As I do with other companies, I decided to compare Hamilton Beach Brands to some similar firms. But it is difficult to find companies of a similar size it performs similar work to what Hamilton Beach Brands is engaged in. So instead of five comparables, I had to settle with four. As you can see in the table below, Hamilton Beach Brands ended up being cheaper than all of the companies I compared it to.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Hamilton Beach Brands |

| 4.1 |

| 5.6 |

| Traeger ( COOK ) |

| 17.1 |

| N/A |

| Helen of Troy ( HELE ) |

| 14.9 |

| 16.0 |

| National Presto Industries ( NPK ) |

| 13.4 |

| 11.5 |

| Cricut ( CRCT ) |

| 15.5 |

| 32.1 |

Takeaway

From what I can tell right now, the picture for Hamilton Beach Brands could be better. It could also be worse. If management is to be believed, the second half of this year should mark a nice recovery for the company. The stock looks fundamentally attractive, both on an absolute basis and relative to similar firms. Given these matters, and in spite of the share price weakness we have seen in the past few months, I have no problem keeping the company rated a 'buy' for now

For further details see:

Hamilton Beach Brands Is Still On Sale