HBB - Hamilton Beach Brands: Significant Near Term Risks Initiate At Hold

2023-10-12 22:01:09 ET

Summary

- Hamilton Beach Brands is a small appliances company which was facing stagnating growth and declining profitability historically, which further weakened this year.

- Management is optimistic of better growth, however, we remain skeptical given the current consumer environment.

- We initiate at Hold and await any tangible progress in improving profitability while stemming the declining sales.

Investment Thesis

Hamilton Beach Brands ( HBB ) is a small appliances player with a volatile history with shares cratering over 60% as a result of weak operating metrics and the company's quest of profitable growth turning more and more elusive. Recent earnings also suggests that the fundamentals are weakening, however, an improvement in working capital have lend them a helping hand to reduce their debt burden. We believe there are downside risks to the management's overbearing optimism and await any tangible progress to arrest a sales decline while maintaining profitability. Initiate at Neutral.

Company Background

Hamilton Beach Brands is a small electric household and specialty houseware appliances company serving a range of consumers such as coffee makers, food processors, blenders, juicers and slow cookers as well as commercial products. Key brands include Hamilton Beach, Proctor Silex, Weston and TrueAir. It licenses the brands for countertop appliances, air purifiers and electric water filtration appliances. In addition, it markets cocktail delivery machines and specialty appliances to create Numilk on demand.

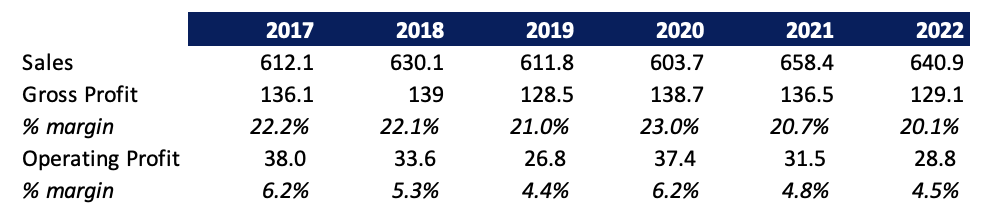

Patchy Financial Track Record

The company had a patchy run with sales being flattish for its history and decline in its gross margins as a result of higher product costs which were not followed with a similar price increase to spur demand.

{kind=link}

Note: FY22 Operating profit excludes $10 mn of insurance

The company wound down its Kitchen Collection business in Oct 2019 which contributed about $100 mn in revenue but was loss making with peak operating annual losses of $28 mn in a bid to move to profitability. However, despite that, the company's efforts have not been successful due to sub-par operating profits which has now been lower even compared to 2017 (even after excluding the operating loss of 2 mn from KC business). The shares have cratered by over 60% since spin off in late 2017, due to weak operating metrics and poor return ratios.

Weak Q2 Earnings

HBB reported a weaker set of numbers for Q2 with revenues declining 7% YoY as a result of soft consumer demand with lower unit volumes and shift towards low margin products. The decrease was driven by reduced inventory levels at its retail customers due to cautious outlook amidst record inflation and declining consumer confidence along with higher inventory levels through last year. In addition, revenues within its global commercial market declined as a result of normalization of the demand environment due to outsized demand last year from food service industries as a result of reopening post COVID-19.

Gross margins declined 170 bps primarily as a result of unfavorable product mix due to shift towards lower value products as consumers seem to be trading down along with fixed cost deleverage. SG&A dollars remained flat but deleveraged as a result of declining revenue growth compared to sticky fixed costs. Operating margins declined 320 bps to 0.5% as a result of contraction in gross margins and SG&A deleverage. Operating margins have been on a downward spiral since past few quarters which is typical in a company with lower margins as fixed cost deleverage would significantly erode profitability should the revenues fail to sustain.

Inventory levels continue to normalize as a result of the management's focus on rightsizing the inventory leading to $42 mn cash generated from working capital (in inventories and account payables) in H1 which has been the silver lining. In addition, it has also been able to use the cash generated from operations (primarily working capital) to pay down debt and ended with a net debt of $58 mn compared to $126 mn last year.

Management reiterated its expectation of flat revenues for the year implying H2 revenues to surpass last year's revenues by high single digits. It expects operating profits to be higher than the previous year (excluding the insurance recovery of $10 mn) implying an operating margin of 8.5% which has not been achieved within the company's history. The strong growth in H2 is based on management's belief of gaining consumer market share with incremental placements and promotions, particularly during the holiday sales. We remain skeptical on the company's ability to drive growth as several large appliance makers have flagged a bleak outlook as a result of ongoing economic pressures within North American market. Whirlpool ( WHR ), one of the largest small appliance maker through its brands Kitchen aid and others, had a muted Q2 with the management guiding towards an even cautious outlook.

Even though we are starting to see early, but clear signs of a strengthening U.S. housing market, which will benefit us disproportionately, but broader consumer sentiment is still cautious and not yet pointing towards more discretionary purchases.

- Marc Bitzer, Chairman and CEO (Source: Q2 Earnings )

In addition, Electrolux, maker of popular brand Frigidaire which offers ovens, cooktops and wide range of other appliances, also noted a continued decline in shipments , negative product mix and higher promotional environment eroding profitability.

We expect H2 revenues to stay flat to slightly positive which yields to ~$350 mn in revenue for H2 and $615 mn in revenue for the year. In addition, we expect operating margins to decline by about 100 bps to 5% and operating profits to be $18 mn implying full year operating profit to be $14 mn.

Valuation

HBB trades at ~15x EV/ 2023E EBITDA assuming an operating profit of $14 mn and D&A of $4 mn in line with historicals. Given HBB is a small player, it is difficult to accurately list down its peer set, hence we have only used 3 peers which has similar business model. HBB's EV/ EBITDA multiple is at a premium to its peer group average of 12.8x.

We believe there are significant downside risks to management's optimism and await any tangible progress made on the progress to achieve sales growth while maintaining profitability. Initiate at Hold.

Risks to Rating

1) Significant decline in consumer confidence resulting in reduced discretionary spends can continue to throttle recovery

2) Competitive pressures may intensify and high promotional environment may lead to a decline in operating margins

3) Upside risks include an improvement in consumer spending, better offtake of newly launched products and cost control measures to boost operating margins

Final Thoughts

HBB has been facing with declining sales and eroding profitability as a result of current economic pressures. However, we remain uncertain on the company's profitable outlook as a result of patchy track record of execution and lingering near term uncertainty. It has done well in reducing their debt load and releasing the working capital from inventories and payables. However, we believe there are significant downside risks given the current environment and we await tangible progress on whether the better offtake of newly launched products can arrest a decline in overall sales growth. Initiate at Neutral.

For further details see:

Hamilton Beach Brands: Significant Near Term Risks, Initiate At Hold