WRB - Hartford Financial: Cheap With Catalysts

2023-09-12 06:19:53 ET

Summary

- Hartford Financial's shares are below fair valuation based on my analysis involving peer and historical comparisons.

- There are re-rating catalysts for HIG relating to the profitability of the workers' compensation business and the company's share buybacks.

- I have a Buy rating for Hartford Financial, as I deem HIG to be undervalued, and I have identified relevant re-rating catalysts for the stock.

Elevator Pitch

I assign a Buy investment rating to The Hartford Financial Services Group, Inc. ( HIG ).

I view Hartford Financial's shares as cheap based on historical and peer valuation comparisons. Future share buybacks and the resilience of the workers' compensation business are expected to act as favorable re-rating catalysts for HIG. As such, I am bullish on HIG, which translates into a Buy rating for the stock.

Company Description

Hartford Financial refers to itself as a "leader in property and casualty insurance, group benefits, and mutual funds" in the company's media releases .

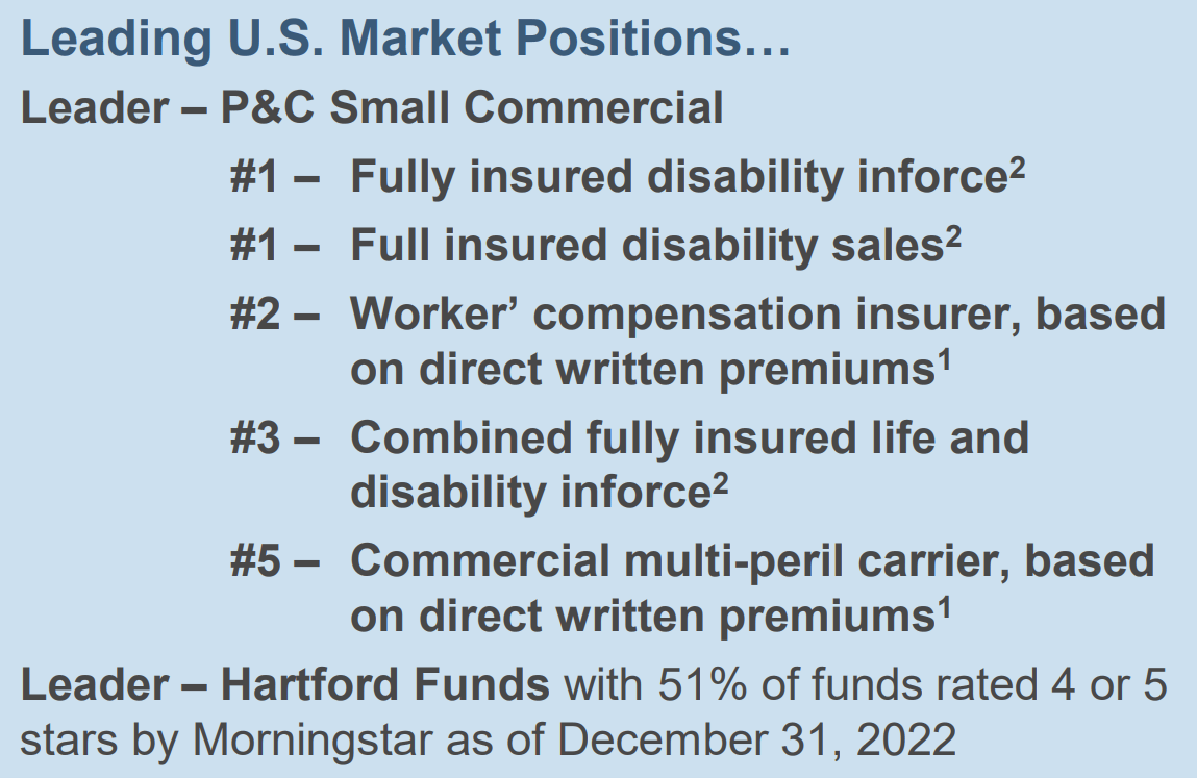

Hartford Financial's Market Leadership

{kind=link}

HIG derived 72% of its fiscal 2022 core earnings from the company's Commercial Lines business segment as indicated in its investor presentation slides . Group Benefits, Hartford Funds, and Personal Lines accounted for 16%, 7%, and 5% of Hartford Financial's FY 2022 bottom line, respectively.

Separately, California, New York, Texas, and Florida represented 12%, 10%, 8%, and 5% of HIG's earned premiums for the most recent fiscal year, respectively, as highlighted in its 10-K filing . Apart from these four markets, no other region contributed over 5% of Hartford Financial's fiscal 2022 earned premiums.

HIG's Shares Are Cheap

Hartford Financial stock is undervalued in my opinion, taking into account a number of factors.

Firstly, HIG is valued by the market at a discount to its historical averages. Hartford Financial currently trades at a consensus forward next twelve months' normalized P/E multiple of 8.1 times. As a comparison, HIG's 10-year and 15-year mean P/E multiples were relatively higher at 10.5 times and 9.0 times (source: S&P Capital IQ ), respectively.

Secondly, Hartford Financial's P/E and P/B valuation metrics are very attractive as compared to its key peers.

Peer Valuation Comparison For Hartford Financial

| Stock |

| Consensus Forward Next Twelve Months' Normalized P/E Multiple |

| Historical Trailing Last Twelve Months' P/B Multiple |

| Hartford Financial |

| 8.1 |

| 1.59 |

| The Hanover Insurance Group ( THG ) |

| 10.0 |

| 1.67 |

| The Travelers Companies ( TRV ) |

| 10.1 |

| 1.69 |

| Chubb Limited ( CB ) |

| 10.5 |

| 1.59 |

| W. R. Berkley Corporation ( WRB ) |

| 11.7 |

| 2.32 |

| Cincinnati Financial Corporation ( CINF ) |

| 17.5 |

| 1.49 |

Source: S&P Capital IQ

Thirdly, there is a significant mismatch between Hartford Financial's high single-digit P/E multiple and the company's low-to-mid-teens percentage ROE. HIG's forward P/E ratio is 8.1 times as mentioned earlier. In contrast, Hartford Financial's ROEs for full-year FY 2022 and Q2 2023 were 14.5% and 13.6%, respectively, as disclosed in the company's recent quarterly earnings presentation . Looking forward, HIG stressed at its Q2 2023 results call that "we are confident in our ability to deliver core earnings ROE in the 14% to 15% range" going forward.

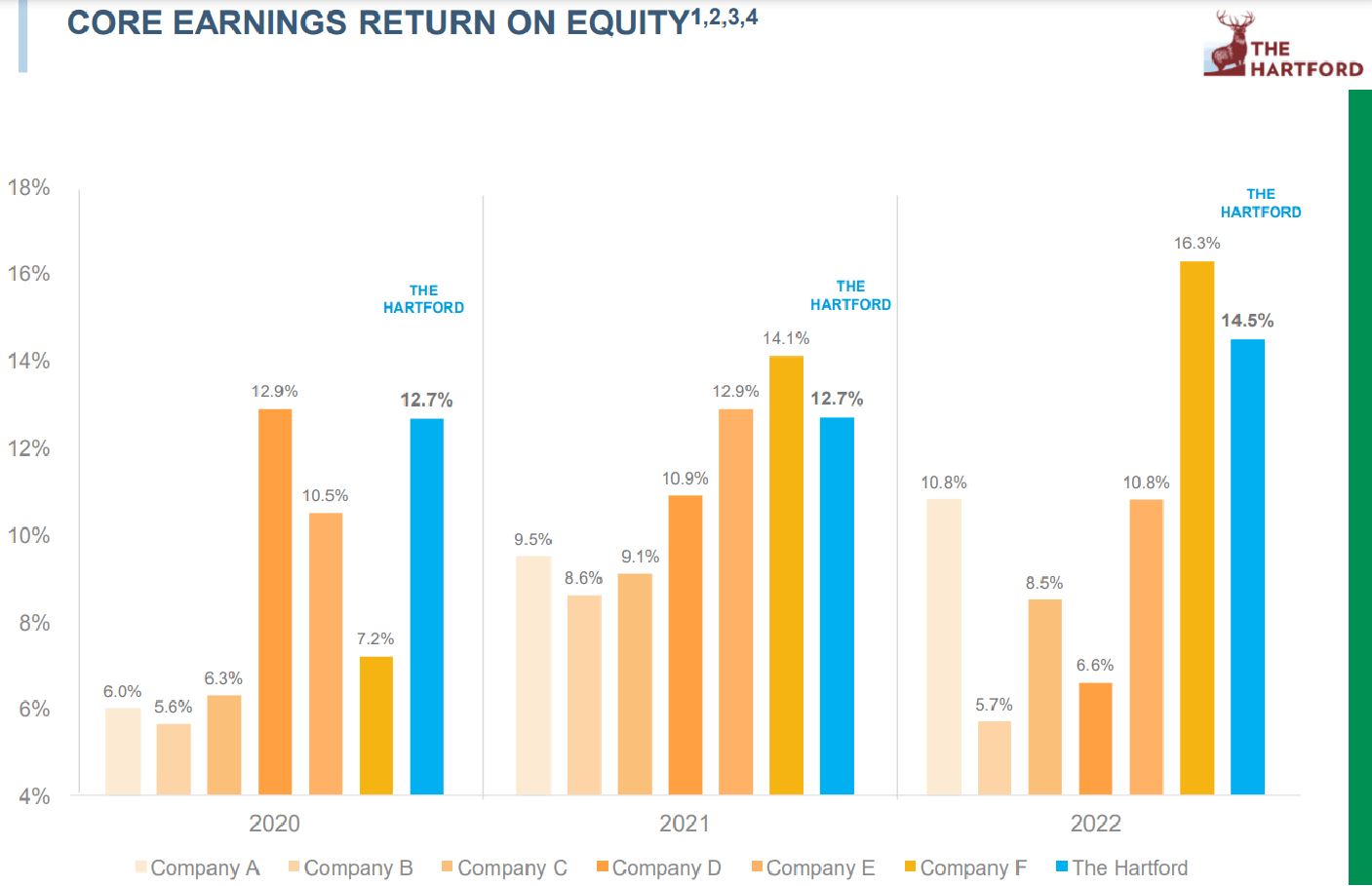

It is also worth noting that Hartford Financial's historical ROEs have been higher than most of the company's listed peers as highlighted in the chart below.

A Comparison Of Hartford Financial's FY 2020-2022 ROEs With Its Peers

{kind=link}

With the company consistently generating ROEs in the low-to-mid teens percentage range, I think that HIG deserves to command a P/E multiple of 10 times or higher.

In the subsequent section, I touch on potential catalysts that could help to bring about a positive re-rating of Hartford Financial's valuations.

Potential Re-Rating Catalysts For Hartford Financial

In my opinion, there are two visible catalysts in place that might drive valuation multiple expansion for HIG.

The first potential catalyst for Hartford Financial is continued share buybacks.

In the first half of this year, HIG spent approximately $700 million on share repurchases, and the company still has around $2 billion remaining from its current buyback authorization, which lasts till the end of next year.

At the company's KBW Insurance Conference on September 7 last week, Hartford Financial highlighted that the company will "deploy it (excess capital) in a very systematic, consistent way", and described its share repurchases as "being very accretive, especially where our shares trade." HIG's recent management commentary implies that there is a very high probability of Hartford Financial continuing with its share buybacks and completing the remaining $2 billion worth of share repurchases by end-2024.

Consistent share buybacks will help to provide support for Hartford Financial's share price and boost the company's ROE with the shrinkage of its equity base.

HIG's second potential catalyst is the alleviation of the market's concerns regarding the future profitability of its workers' compensation business. Hartford Financial is the second-largest player in the US workers' compensation market as indicated in the "Company Description" section of this article.

A sell-side analyst from BMO questioned at HIG's Q2 2023 results briefing whether "an uptick in medical inflation" has affected the company's workers' compensation business. Hartford Financial responded to this question by noting at its most recent quarterly earnings call that its "medical severity trends (for Q2 2023) are consistent with" its Q1 commentary and "lower than the 5% that we assume in our pricing and reserving."

Hartford Financial explained at the September KBW Insurance Conference that its "outstanding claim capabilities where we challenge and regularly review medical bills" and "multi-year contracts that have stated and set rates for procedures" have allowed its workers' compensation business to be largely unaffected by medical inflation. If the actual profitability of the workers' compensation business turns out to be better than expected, the company's ROEs in subsequent quarters and years should end up higher than the analysts' consensus financial projections.

The proof is in the pudding, and I expect HIG to prove to the market over time that medical inflation will have a very limited impact on its workers' compensation business and the company's overall performance.

Closing Thoughts

HIG's shares are cheap, and I expect catalysts relating to its workers' compensation business and share repurchases to be supportive of a positive re-rating. Therefore, I have decided to rate Hartford Financial as a Buy.

For further details see:

Hartford Financial: Cheap With Catalysts