HAS - Hasbro: Great Products Frustrating Business

2024-01-08 07:57:54 ET

Summary

- Hasbro's subsidiary, Wizards of the Coast, has a highly profitable portfolio with Magic: The Gathering and Dungeons & Dragons.

- The true value of Wizards of the Coast is not fully reflected in Hasbro's stock price.

- CEO Chris Cocks has the potential to restructure the business and unlock valuation upside, but a spin-off of Wizards of the Coast would be the most value-accretive move.

- Ongoing transformation into an asset-light business centered around Wizards of the Coast could lead to a share price of $72 (base) - $117 (bullish). Failure would mean $45 - $51.

Hasbro (HAS) is perhaps the quintessential representation of a great product, frustrating business. The investment thesis is simple: the Wizards of the Coast ((WotC)) subsidiary is as close to a money-printing business as is legally possible, with Magic: The Gathering quite literally printing paper currency in the form of collectible cards . Tack on Dungeons & Dragons - the number one leader in table-top role-playing games - and it is clear Wizards of the Coast has a slam-dunk portfolio.

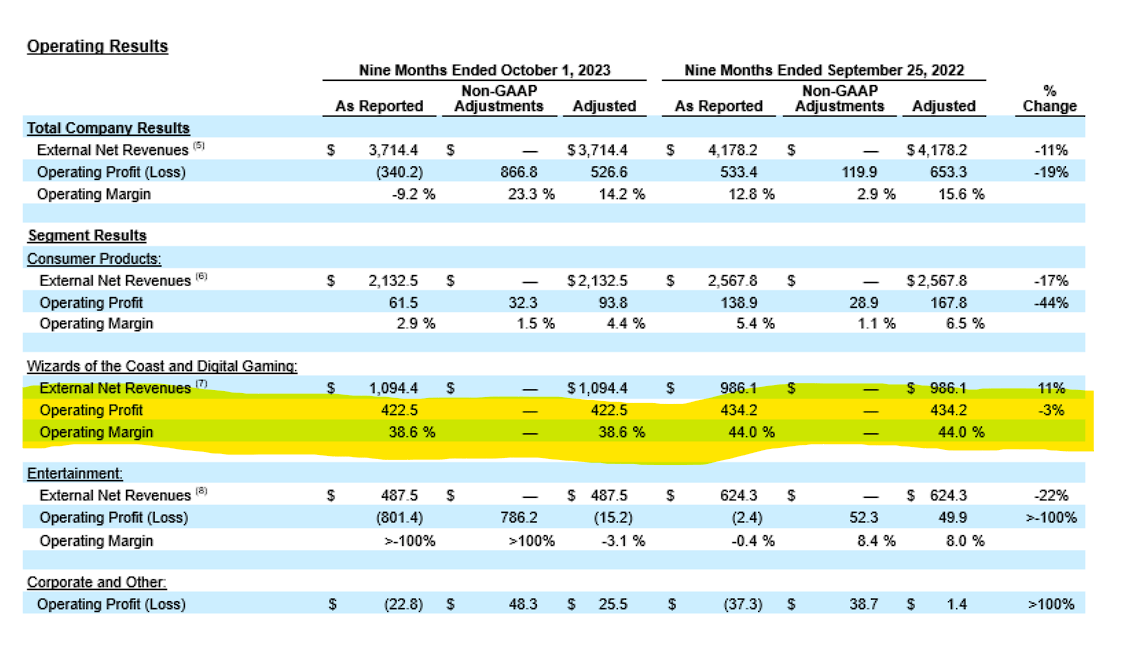

The financial muscle of Wizards of the Coast is apparent in any Hasbro financial statement , where its status as a crown jewel hides in plain sight: 20%-30% of revenues make up 40%-50% of the operating profit. Yet, the real value of this great business remains trapped in the mediocrity of the broader Hasbro corporate umbrella.

Shares of HAS are depressed, and the value of HAS is worth substantially more on just the back of Wizards of the Coast. If, and when, recently appointed CEO Chris Cocks can successfully restructure the business following the disposal of its Entertainment One ((eOne)) business, reset the capital structure, and return the toy business to profitability, then further upside can be achieved. I assign a Buy rating to HAS.

Why does this opportunity exist?

It would be easy to say that Hasbro's troubles are simply macroeconomic in nature and that they - like the majority of the consumer discretionary sector - are experiencing an amplified down-cycle. This is all true for HAS, but their troubles pre-date the current macroeconomic environment.

In 2019, HAS made an egregious bet on being able to replicate the success of Disney-Marvel by purchasing eOne , enabling Hasbro to develop and produce their own television shows and movies based on their great IP. This made sense - after all, Transformers movies (a Hasbro IP) have continually been successful at the box office , and there is significant untapped potential in Magic: The Gathering, Dungeons & Dragons, and other Hasbro IP. Any brilliance that may have come from this transaction will never see the light of day as, sadly, the former CEO died soon after the merger happened. Add the COVID-19 pandemic and the WGA/SAG-AFTRA strikes shutting down the production and movie industry, and Hasbro had one black swan event after another that cut any legs the eOne acquisition would have had.

Hasbro clearly has had enough, and finally sold off the majority of eOne to Lions Gate ( LGF.A ) for $500 million (including assumption of production loans), expected to close end of 2023. This follows a $385 million sale of the music division in 2021 . Hasbro is keeping production capabilities for their owned IP as well as Peppa Pig; but it is undeniable that the original $4 billion transaction will incur significant losses. However, the impact is longer-lasting, as Hasbro over-leveraged by taking on billions in debt, diluted its shareholders, and suffered ongoing losses from the entertainment division (exasperated by the black swan events) making it difficult to have de-leveraged and successfully executed the acquisition.

Still, the troubles of Hasbro go even further back. For years, management had continually underinvested in their WotC crown jewel: letting the quality of its products decline; refusing to transform the company to leverage its ficonic and loved IP into new formats, media, and entertainment verticals; and continually championing legacy products and IP with poor prospects and margins. A proxy fight with a minority investor, Alta Fox Capital , revealed these cultural issues that have been so systemic to Hasbro for years; however, any consumer of WotC products could have pointed to this simply by the products they interacted with. Diverse ways to engage with WotC products (i.e., digital), and the quality of WotC products have been missing or declining over the years.

These points have all ultimately led to an implosion of HAS equity once the macroeconomic environment deteriorated - HAS in, particular, being hit one of the hardest, given all of these compounding factors: shares have been cut in half since pre-pandemic levels, from $100 to $50.

With new CEO Chris Cocks coming from Wizards of the Coast, there has been a shift in direction to tap into growth verticals, a pouring of new investment in Wizards of the Coast, an acknowledgment of the issues plaguing Hasbro, and a course of action put in place to make Hasbro a more efficient, asset-light business. Management calls this their Blueprint 2.0. I categorize Hasbro as a turnaround: the right products are already in place, but the business needs to reset. Time will tell if Chris Cocks and his team execute successfully.

Valuation (of Wizards of the Coast)

Bottom line, up front: I believe Hasbro is worth between $73 - $117 per share, depending on the success of their transformation.

The low end is attributed to a normalization of the macroeconomic environment and inventory levels and Hasbro chugs along as a predominantly toy-driven business that follows the secular low-single-digit growth projections . Hasbro management would argue that they are actually a gaming business; I agree with management that they are a gaming business, or rather, should be a gaming business. All of Hasbro's profits belong to their gaming products - Monopoly, WotC products, video games, etc. - but still only amount to ~1/3 of the company's total revenue. The high-end of my price range is based on Hasbro successfully transforming enough into a gaming business that the market re-rates Hasbro as such.

Comparison to peers

To illustrate the point, consider Bandai Namco (NCBDY), a Japanese toy and gaming conglomerate that I would argue is the closest peer to Hasbro on the planet, more so than Mattel ( MAT ) (which has the opposite problem to Hasbro, great business, limited stand-out IP beyond Barbie). Bandai Namco is a publisher of video games and had explosive success with Elden Ring , while Hasbro is also involved with video games and experienced their own blockbuster success very recently with 2023 Game of the Year winner Baldur's Gate 3 that drove $63 million in incremental revenue in Q3 for WotC. In addition to games, Bandai Namco is a significant (and profitable) toy business, dominated by Gundam, whereas Hasbro has their own large robot flagship IP in Transformers. The similarities between the two companies are uncanny.

The reason for introducing Bandai Namco is to argue there should be a valuation floor of 12x EV/EBITDA prescription for Hasbro, in line with Bandai Namco. Historically, HAS multiples have traded similarly to MAT, but the businesses are in reality not close. Apart from Uno, Mattel does not have much of a gaming division and is instead a predominantly traditional toy business with Barbie as its flagship IP. The more appropriate comparison to NCBDY is considered a floor given its extremely conservative nature operating under Japanese management and risk-averse growth; however, it is also experienced and matured in the gaming business. This makes NCBDY a solid barometer for where HAS should normally trade, and if HAS can successfully improve the bottom line by cutting costs and shedding asset-heavy business from the consumer products toy business, then a multiple closer to that of pure-play gaming businesses, like Games Workshop (GMWKF), of 15-16x is warranted.

Undeniably, HAS does not deserve a premium multiple given its current conditions as a business. A simple look at the earnings margins clearly punctuates this point.

However, what is frustrating about Hasbro is that the WotC segment absolutely experiences the kinds of margins that the pure-play gaming companies do, but trades at toy company multiples like Mattel because of the legacy Hasbro anchor.

{kind=link}

{kind=link}

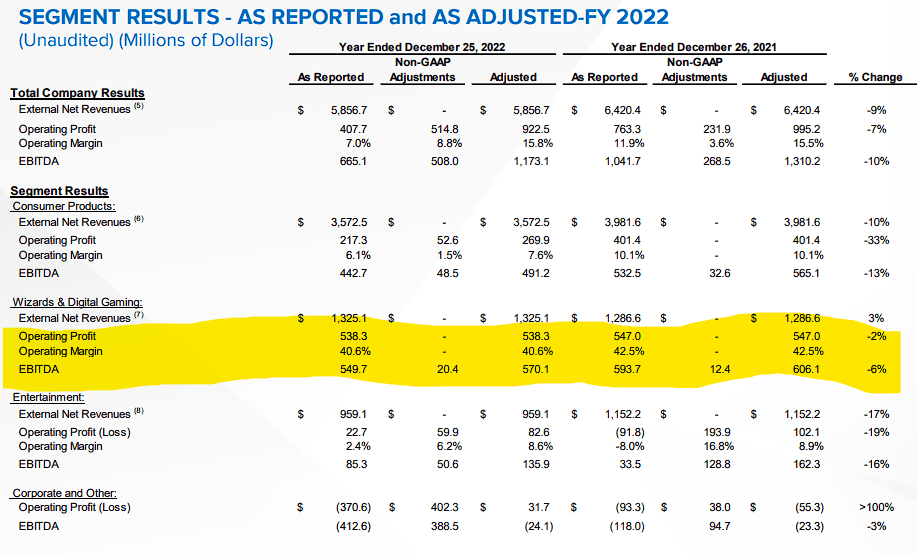

Between 2014 and the eOne acquisition in 2019, HAS was growing on the back of WotC outperformance due to the excellent growth of Magic: The Gathering and the Dungeons & Dragons 5th edition release, evidenced by return on equity rising while debt remained flat. The working capital needed to grow the WotC business segment amounts to securing the supply of paper and printing capabilities, likely de minimis relative to total revenue, and a small portion of the total working capital of the business.

In other words - Wizards of the Coast is a fantastic business. Well-loved products that are high-margin and asset-light, generating revenues twice as much as what Games Workshop makes ($580 million in FY23), with similar margins, yet trading several multiples turns lower. Wizards of the Coast trading on its own would be a ~$10 billion company based on $550 - $600 million of EBITDA that it generates if it traded at multiples like Games Workshop, which I would argue is still an undervaluation given the larger and more diversified hits that WotC owns over Games Workshop's singular product. The current enterprise value of Hasbro is $10 billion, or in other words, the entire value of Hasbro is Wizards of the Coast. Put another way, the toys and entertainment business of Hasbro is currently negative value to the overall company.

Value of Hasbro's transformation

The good news is that new management seems to understand the discussed issues. That's not to say there is a plan to spin off WotC (the best solution in my opinion), but the next best thing is to cut costs on the legacy company and squeeze cashflow out of it to fuel growth, quality improvement, and investment into Wizards of the Coast. There is very recent evidence of the business (finally) prioritizing Wizards of the Coast:

Through Q3, we repaid $107 million of long-term debt and spent $160 million on capital expenditures led by investments in Wizards of the Coast for future digital gaming releases. - Q3 2023 Hasbro Earnings Call.

Further evidence of Hasbro's growing investment into Wizards of the Coast and its gaming journey can be found with its wholly-owned video game studio Archetype Entertainment. This studio is made up of ex-BioWare renowned studio veterans and creators who are responsible for such critically acclaimed and beloved games as Dragon Age , Baldur's Gate 1 & 2 , and Mass Effect , all commercial successes. Chris Cocks has essentially given the all-star veteran team free rein to organically develop an entirely new IP franchise for Wizards of the Coast, and they recently announced their first AAA game .

The investments and transformation at Hasbro are summarized by management's Blueprint 2.0, with an aim for $8.5 billion in revenue by 2027 and total company operating margins of at least 20%. I will ignore the revenue goals, as they are laughable and obviously laid out during the consumer goods craze of the pandemic era. However, the operating margins goal is achievable, especially with the significant downsizes that Hasbro announced this year .

I assume 2027 revenues reach $5.2 billion (a far cry away from management's $8.5 billion target), or 1% CAGR, which is not even in line with the toy industry at 3.5% , let alone gaming. I am emphasizing the value potential of bottom-line improvements; thus, I assume management successfully executes on the bottom-line transformation of Hasbro to reach 19.5% EBIT margins by 2027, or $1.23 billion in total EBITDA. Net debt should drop to $3.3 billion following the disposal of eOne (which includes ~$100 million in production loans), as management stated definitively that the proceeds would go to de-leverage:

We expect the transaction to complete by the end of 2023. Hasbro will use the proceeds to retire a minimum of $400 million of floating rate debt by the end of the year and for other general corporate purposes. - Q2 2023 Hasbro Earnings Call.

I expect another $700 million in debt paydown from free cash flows over the years, which brings the debt-to-EBITDA (using historical EBITDA in the $1 billion range) leverage ratio down to 2.5x, the target that management provided to investors. By 2027, this amounts to ~30% of available free cash flow, along with ~65% of dividend (and thus zero room for dividend growth), leaving 5% for general corporate or growth capex purposes. The result is net debt standing at $2.3 billion by 2027.

Altogether:

| HAS: FY27 Exit |

| EBITDA |

| Net Debt |

| Multiple |

| Market Cap |

| Price |

| Base Case |

|---|

| $1,233 mil |

| $2,258 mil |

| 10 |

| $10,070 mil |

| $73 |

| Bull Case |

| $1,233 mil |

| $2,258 mil |

| 15 |

| $16,234 mil |

| $117 |

A prescription of 10x multiple puts HAS below that of NCBDY and MAT, indicating that HAS fails to convince the market of its place as a gaming company. It also implies that HAS efficiency metrics do not converge toward historical levels. The base case indicates a 15% IRR (including dividends) by the 2027 management target timeline. Meanwhile, a 15x multiple (still below that of Games Workshop) indicates a successful transformation, but not so overly optimistic. The bull case indicates a 27% IRR (including dividends) over the same timeline.

Risks

It should be made clear that the valuation presented absolutely depends on Hasbro management succeeding at least on its bottom-line transformation and reaching their 20% EBIT margin goal, which is not a given considering Hasbro's historical precedent for shooting themselves in the foot. The rest of the projection simply expects that Hasbro's top line remain essentially flat, below the broader toy and games industry, which is also not a given due to macroeconomic concerns. If Hasbro continues its existence in its present state, EBITDA may be similar to historical levels of $1 - $1.1 billion and a share price of $45 - $51 using a low-end of historical range 10x multiple: what are typically considered "dead money." This is the bear case.

There is also an upside risk if the top-line improves beyond flattish levels by FY27; however, I disregard that case to maintain a conservative stance and because it is difficult for me to divine when (or indeed if) Hasbro's business environment will normalize. Management has much more control over the bottom-line operations that is the centerpiece of the provided valuations.

One last consideration is the dividend. D.A. Davidson analysts suggest a dividend cut is in the near future for Hasbro to reach its leverage goals until after 2025. I agree; HAS will have enough free cash flow to cover its dividend but only reach slightly less than half of the required ~$700 m to achieve the 2.5x leverage goals. Part of this is helped by interest rate savings from the elimination of floating rate debt following the close of its eOne sale. That being said, only $1.2 billion of debt will mature before 2027, so HAS could reach its leverage goals by 2027 without cutting its dividend, lining up with its Blueprint 2.0 transformation timeline.

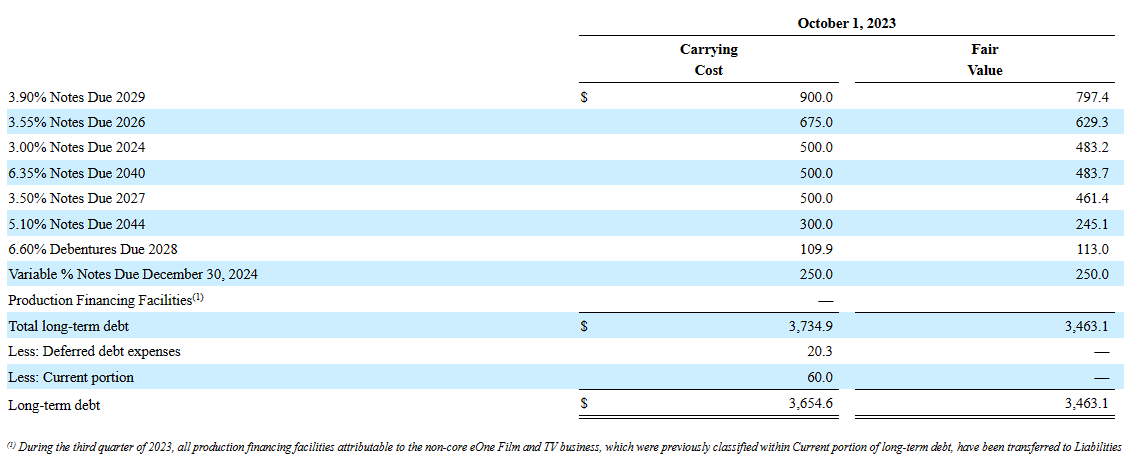

HAS Financial Instruments Q3FY23 (Hasbro Q3FY23 10-Q )

{kind=link}

Of course, this assumes the macro environment does not deteriorate materially from current levels. Regardless, I will welcome a temporary dividend cut if it means accelerating the deleverage plans to reset the capital structure and refocus Hasbro on its higher-quality business prospects.

Conclusion

In my opinion, it is unfortunate that activist investor Alta Fox Capital could not gather enough support to lead to a Wizards of the Coast spin-off, but at least there is optimism that CEO Chris Cocks and the rest of Hasbro management understand the true value and growth driver of Hasbro is in WotC. Additionally, the tone of investor presentations and earnings calls has shifted to acknowledge the cultural issues at Hasbro and to actively progress away from these endemic problems. Identifying that decisions in the previous regime were made based on legacy rather than KPIs or quantitative measures and implementing new decision-making processes are good steps forward.

The shares of HAS should meaningfully appreciate the upside on the return to a normalized toy environment and the successful execution of Hasbro's bottom-line driver initiatives. I am cautiously optimistic that the future of Hasbro under Chris Cocks will lead to a more efficient business that properly invests in their strongest segments and returns their business - and their products - to higher quality. However, I still firmly believe that the most significant value-accretive maneuver would be to spin off Wizards of the Coast.

After all, Hasbro, the WOTC stock ticker is available.

For further details see:

Hasbro: Great Products, Frustrating Business