ENSG - HCA Healthcare: Shares Got Just A Well-Deserved Boost On Strong Q1 Earnings

2023-04-22 08:00:00 ET

Summary

- HCA Healthcare has seen quite a meteoric rise over the past several months, with strong financial performance pushing the stock up.

- Management just announced attractive financials covering the first quarter of the 2023 fiscal year, sending shares up further still.

- Even though HCA stock can only climb so far from here, it does seem to deserve even more upside based on valuation.

One of the largest health care service companies in the US is undoubtedly HCA Healthcare (HCA). At the present moment, the company has 180 hospitals in its portfolio, plus 126 freestanding outpatient surgery centers and other miscellaneous assets. It boasts a market capitalization of $75.1 billion and continues to grow its top line year over year. Over the past several months, the market has rewarded the company's performance handsomely. But at some point, upside potential is no longer possible. But thankfully, after management reported good financial results covering the first quarter of the companies 2023 fiscal year, it appears as though this particular prospect's move higher is not over just yet.

Fantastic Q1 results from HCA Healthcare

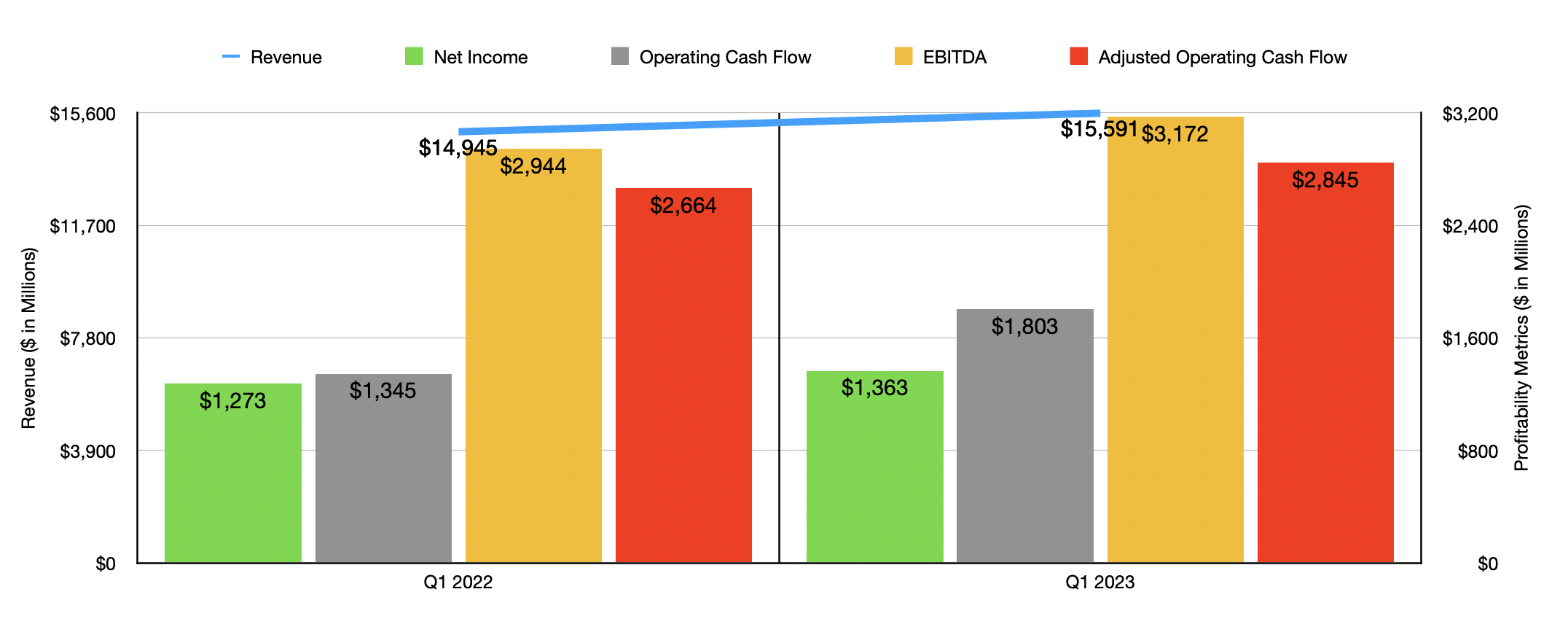

Before the market opened on April 21st, the management team at HCA Healthcare announced financial results covering the first quarter of the company's 2023 fiscal year. On the top line, management reported revenue of $15.59 billion. This represents an increase of 4.3% over the $14.95 billion the company reported one year earlier. In addition to coming in higher year over year, the company also handily topped analysts' expectations to the tune of $324.6 million. There were some drivers behind this sales increase. Even though the number of hospitals in the company's portfolio dropped by 2 year-over-year, the number of admissions grew by 3.6% from 506,956 to 525,235. Equivalent admissions, which makes certain adjustments, jumped an even more impressive 6.7%. Although the company did experience a 2.2% decline in revenue per equivalent admission, it did see a modest increase in inpatient revenue per admission. Inpatient surgery cases during this time grew by 2.8%, while outpatient surgery cases rose 3.5%. What's more, the company saw a rather robust 9.5% surge in emergency room visits.

{kind=link}

As I mentioned already, the company did experience a decrease in the number of hospitals in its portfolio. This means that, on a same property basis, results for the company were even more impressive. Admissions, for instance, shot up 4.4%, while equivalent admissions grew 7.5%. Inpatient surgery cases grew by 3.6% on a same property basis, while outpatient surgery cases jumped 5.1%. Meanwhile, the number of emergency room visits skyrocketed 10.3%.

With revenue rising, profits also expanded. During the quarter, the company reported earnings per share of $4.85. That was $0.87 per share higher than what analysts were expecting. This translates to $1.36 billion in profits, up from the $1.27 billion reported one year earlier. Operating cash flow grew even more significantly, soaring from $1.35 billion to $1.80 billion. Though if we adjust for changes in working capital, the increase was more modest from $2.66 billion to $2.85 billion. Meanwhile, EBITDA for the company expanded from $2.94 billion to $3.17 billion.

Beyond any doubt, the results the company reported for the first quarter were helpful in pushing the stock price higher. But this was not the only major development that proved abolish for investors. The most important development involved management's guidance for the current fiscal year. Previously, management was expecting revenue for the year to come in at between $61.5 billion and $63.5 billion. That number has now been pushed higher to between $62.5 billion and $64.5 billion. Management attributes this guidance increase to strong demand as the healthcare sector continues returning to the same dynamics enjoyed prior to the COVID-19 pandemic.

{kind=link}

This improvement in guidance has also filtered down into the company's bottom line. Previously, net income was going to be between $4.53 billion and $4.90 billion. That number has now been increased to between $4.75 billion and $5.16 billion. Management also provided an estimate when it came to EBITDA. Instead of the $11.8 billion to $12.4 billion that management previously anticipated, they now believe that the reading will come in at between $12.1 billion and $12.7 billion. No guidance was given when it came to operating cash flow. But based on my estimate, and assuming that midpoint guidance is what is ultimately achieved, I believe that a reading of $9.9 billion is realistic. Management is very clearly comfortable with this guidance increase. After all, during the first quarter alone, the company not only paid out $175 million in dividends. It also repurchased almost $850 million worth of stock.

Given these developments, you can imagine my own joy in seeing the company do well. After all, when I last wrote about the company in July of last year, I had a rather bullish stance on it. At the time, I described the investors in the company as being fearful and I found myself drawn to just how cheap shares were. In that article, I ended up rating the company a 'buy' to reflect my view that shares should outperform the broader market moving forward. But even I underestimated the significant upside that the company would experience. You see, since the publication of that article, shares of the enterprise have roared higher, generating a profit for investors of 59.4%. This compares to the 5% upside experienced by the S&P 500 over the same window of time.

{kind=link}

After such a significant move higher relative to the broader market, it may be something to think that further upside is unlikely. But that is not the case in my opinion. Using data from the past two completed fiscal years and using estimates for 2023, I decided to value the company. The results can be seen in the chart above. In short, particularly from a cash flow perspective, shares of the business do look cheap on an absolute basis at this time. In the table below, you can see five companies that I decided to compare HCA Healthcare to. On a price to earnings basis, HCA Healthcare ended up being the cheapest of the group. Using the price to operating cash flow approach, only one of the five firms was cheaper. Finally, using the EV to EBITDA approach, I found out that only two of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| HCA Healthcare |

| 13.3 |

| 7.8 |

| 9.6 |

| Universal Health Services ( UHS ) |

| 15.4 |

| 10.4 |

| 9.2 |

| Tenet Healthcare Corporation ( THC ) |

| 18.8 |

| 7.0 |

| 7.9 |

| Encompass Health Corporation ( EHC ) |

| 23.5 |

| 9.0 |

| 10.1 |

| Acadia Healthcare Corporation ( ACHC ) |

| 24.7 |

| 17.8 |

| 14.3 |

| The Ensign Group ( ENSG ) |

| 25.0 |

| 20.6 |

| 14.7 |

Takeaway

Based on the data provided, it seems to me as though HCA Healthcare is in really good shape at this time. Management continues to achieve attractive results, due in large part to favorable industry conditions. The stock has roared higher over the prior several months because of this robust financial data, but I would argue that shares are still quite cheap at this time. This is so much the case that I believe a 'buy' rating is still appropriate for the firm at this time.

For further details see:

HCA Healthcare: Shares Got Just A Well-Deserved Boost On Strong Q1 Earnings