HDB - HDFC Bank: Cleaning Out The Closet

2023-11-16 19:13:15 ET

Summary

- Even after a big reset to expectations pre-earnings, HDFC Bank delivered a mixed quarter.

- NIM compression remains the pressing concern, particularly relative to a seemingly ambitious midterm plan.

- Given its lower return profile and uncertainties related to post-merger integration, the stock deservedly trades at a narrower book value premium here.

In the lead up to Q2 FY24 earnings, newly formed HDFC Bank (HDB), the product of a merger between its previous parent company, leading Indian housing finance company, HDFC Ltd, and legacy HDFC Bank, one of the most profitable banking franchises in the world, had hit a big reset button on expectations (full September analyst meet replay here ), triggering a massive stock price selloff.

In effect, the merged entity will not only start from a lower book value per share base than standalone HDFC Bank pre-merger but also generate a lower return on assets due to (among other things) excess liquidity post-merger weighing on net interest margins (‘NIMs’). Crucially, the bank also disclosed higher non-performing assets from its parentco HDFC’s corporate loan book, adding to the post-merger concerns I had outlined previously .

While Q2 results did, for the most part, surpass the lowered hurdle, the ‘new’ HDFC Bank still has plenty of challenges to navigate, including NIM pressure as the post-merger integration process unfolds and with rapidly decelerating inflation paving the way for lower policy rates next year. Structurally, the jury’s also still out on whether the bank's merger synergies outweigh its dis-synergies, and thus, I wouldn’t underwrite the kind of returns and valuation premium HDFC Bank stock used to command. Net, the relative fwd book value discount to key peer ICICI Bank ( IBN ) seems fair.

NIMs Under Pressure as Post-Merger Integration Gets Underway

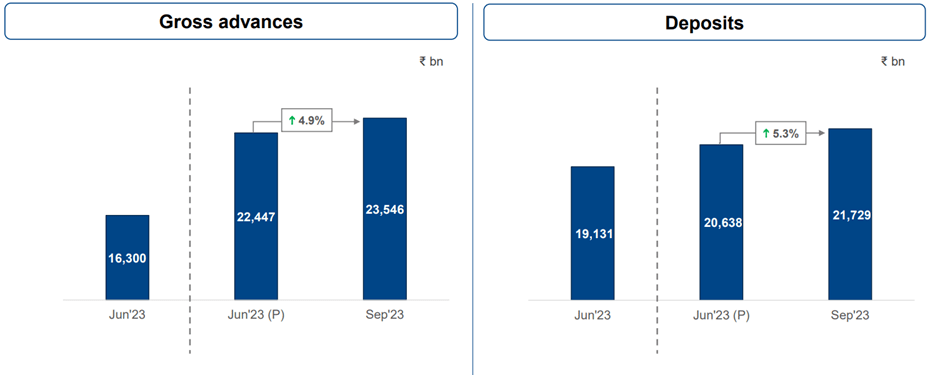

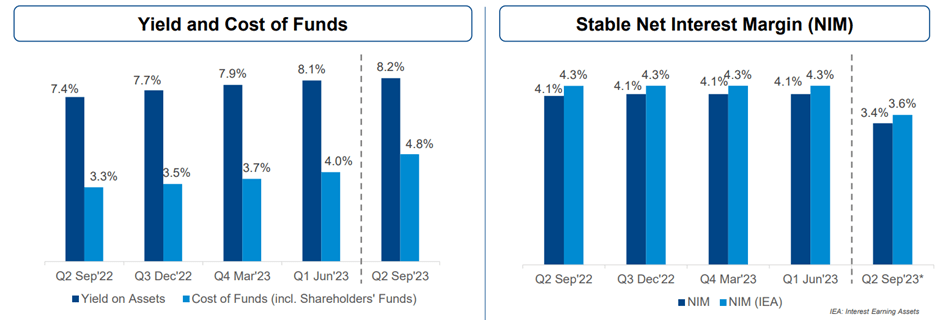

On a headline basis, HDFC Bank outpaced a lowered after-tax profit bar in Q2 FY24, though a closer look indicates a low-quality beat driven by lower taxes and higher treasury gains rather than the core banking business. Fundamentally, there were certainly some positives, particularly on loans/advances and deposit growth. But the major disappointment was the lower NIMs (i.e., the spread between the bank’s interest income and interest expenses), even falling short of rebased expectations pre-earnings.

{kind=link}

To recap, reported NIMs were 3.4% on total assets and 3.6% on interest-earning assets (3.65% on core NIMs on total assets and 3.85% on interest-earning assets), as merger-related costs and liquidity needs weighed on margins. Digging deeper, the bank’s lending yields post-merger was actually slightly above that of legacy HDFC Bank (8.2% in Q1 FY24). The issue was the higher cost of funds post-merger, which has seen an ~80bps uptick to 4.8% (vs ~4% for legacy HDFC Bank), a result of higher funding costs from the HDFC book coming onto the P&L.

To be clear, not all of the NIM headwinds are structural – managing down the elevated >120% liquidity coverage ratio (i.e., high-quality liquid assets held to cover potential outflows) should unlock more capital to fund the bank’s growth. Additional levers available to management in the near future include adjusting its overall lending/borrowing mix, for instance, by moving toward higher-yielding personal loan products.

{kind=link}

Over the mid to long term, though, HDFC Bank’s pre-merger growth plans are likely to slow - note the pace of branch additions slowed significantly in Q2 to +85 vs a 13k-14k branch addition target over the next four to five years. The post-merger book is also more rate-sensitive and could see greater than expected margin compression as India heads toward a rate-cut cycle next year (note that rate expectations were previously pushed out due to transitory weather headwinds). So against management’s intact mid-term target of generating ~2% return on assets (in line with legacy HDFC Bank), I wouldn’t be quite as bullish. Also concerning is the unadjusted headline target to “double in 4-5 years,” as it still leans too heavily on the merged entity successfully cross-selling across an expanded customer base and distribution network.

Post-Merger Asset Quality Reset but Not as Bad as Initially Feared

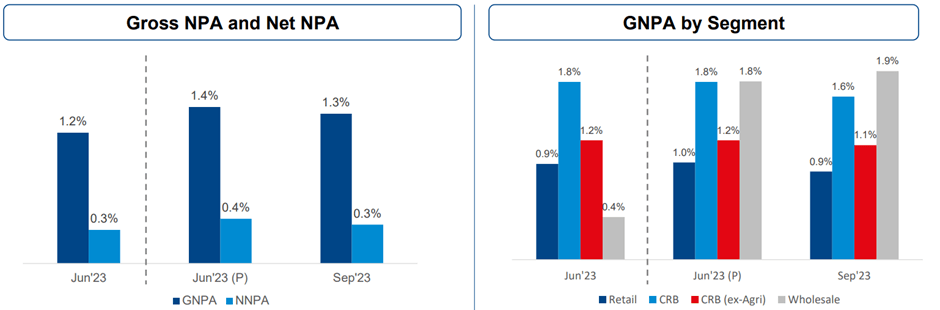

There were some concerns about asset quality heading into the Q2 print, particularly with September's analyst meet disclosing an additional ~20bps to the pro-forma gross non-performing asset ratio (as a % of total loans). Disclosed post-merger adjustments to the equity base had also been negative, mainly on account of asset quality and taxes, as well as dividends paid out by legacy HDFC Bank, driving the revised post-merger book value per share surprisingly lower than standalone HDFC Bank pre-merger.

For now at least, asset quality appears to be under control - on a like-for-like basis in Q2 FY24, the 1.3% annualized ratio was down by 7bps sequentially, helped by healthy recovery rates. Similarly, net of provisions, the non-performing asset ratio was resilient despite some asset quality deterioration in the wholesale book (up ~10bps QoQ to 1.9%).

{kind=link}

Going forward, the key positive is that another rate hike is likely now off the table with food-driven inflation pressures starting to ease. For HDFC Bank investors who now own a far more rate-sensitive book post-merger with housing finance parent company HDFC, this will provide some reprieve for asset quality. It also gives management more leeway to extract synergies from an expanded customer base post-merger, providing some fee-driven offset to NIM pressure in a rate-cut cycle.

Whether these initiatives generate enough value to offset the merger dis-synergies remains to be seen, particularly in light of the RBI tightening regulations around unsecured loans (a key tenet of management’s cross-sell strategy). I’m also not entirely sure all of the skeletons in HDFC’s book have been cleared with the latest ~20bps bump up in gross non-performing assets; any additional provisions could trigger a reset to the bank’s ambitious mid-term growth plans.

Cleaning Out the Closet

HDFC Bank had a lot going for it pre-merger, but the early results of its merger with previous parentco, HDFC, have been rather disappointing. While expectations have also been rebased lower by management, the bank might not be out of the woods just yet, particularly on the profitability and asset quality sides. Offsetting synergies (via cross-selling opportunities across a larger customer base and distribution) should provide some P&L uplift, though early signs point to the addition of HDFC’s book being a dilutive rather than an accretive move.

The bank isn’t immune from a lower rate backdrop either, so expect NIMs to come under pressure as India enters its rate-cut cycle sometime next year. To be fair, HDFC Bank has also seen some of its book value premia dissipate post-merger, though at ~2.6x fwd book, there still isn’t much margin for error here. Pending visibility into a narrowing performance gap vs pre-merger HDFC Bank and key peer ICICI, I remain neutral on the stock.

For further details see:

HDFC Bank: Cleaning Out The Closet