HDB - HDFC Bank: Why The $21bn Rout Was Not Unjustified

2024-01-21 23:09:11 ET

Summary

- HDFC Bank continues to muddle through a challenging post-merger rest.

- While asset quality is trending in the right direction, getting back to pre-merger growth and profitability remains a big hurdle.

- Expectations may now also be a lot lower than before, but I would be cautious about calling a bottom just yet.

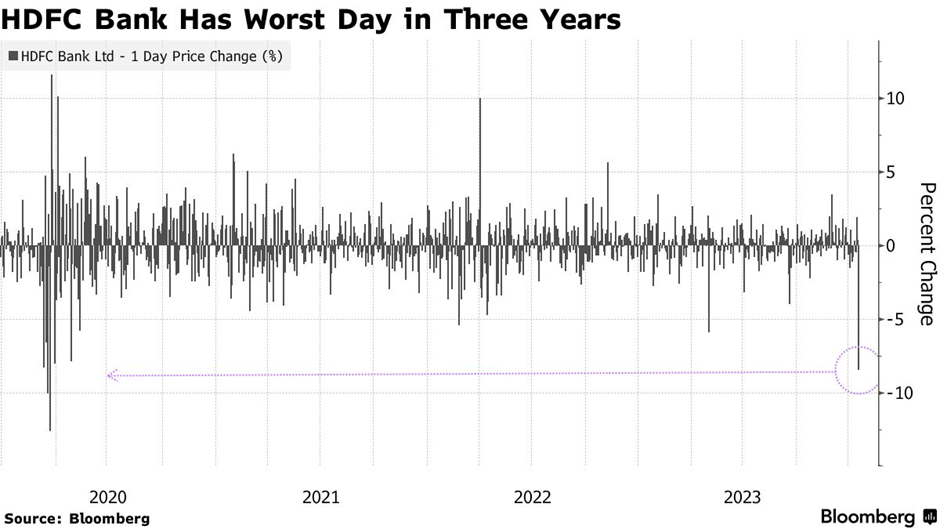

HDFC Bank Limited ( HDB ) has long been India's version of a 'hedge fund hotel.' And rightly so, given its best-in-class track record of compounding through the years. But things have changed since the merger with housing finance parentco HDFC Ltd (see coverage here and here ); for all the pre-merger scale and synergy promises, investors now find themselves holding a far more complex pro-forma entity but with little offsetting benefits. Q3 FY24 was a case in point in this regard, as lower net interest margins and lagging deposit growth prompted investors to hit the reset button on forward earnings expectations. For context on how big of a reset this was, HDFC's post-earnings selloff single-handedly wiped out over $21bn of banking sector market cap last week.

{kind=link}

Despite the pessimism, I'm not sure we've quite hit peak levels, particularly with management sticking with an ambitious mid to long-term guide that seems increasingly out of reach. Plus, there are rate cuts on the horizon (likely in H2) and an increasingly competitive deposit pricing environment to contend with - neither of which bode well for the margin expansion path. While valuations are also getting a lot more reasonable (historically and vs key peer ICICI Bank (IBN), I remain cautious about picking up HDFC Bank stock here.

Deposits and Margins Cloud the Quarterly Report

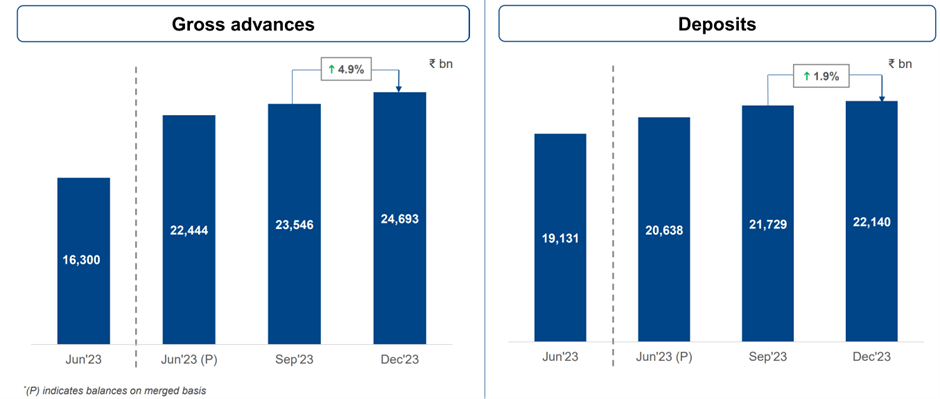

While HDFC Bank did outpace headline expectations slightly in Q3 FY24, all eyes were on the finer details, particularly deposits, which came in at a less-than-stellar +1.9% sequential growth. On the post-results call , management called out India's system-wide liquidity deficit as the key driver of the below-par deposit growth result.

{kind=link}

There's a fair bit of truth in the bank's assessment - deposit competition in India has intensified of late, with steep short-term deposit rate hikes spilling over from public banks into the large-cap private banks as well (Kotak Mahindra Bank is the first mover at up to 85bps). Thus far, HDFC Bank management has mitigated the worst of the impact by being selective (e.g., avoiding more competitive wholesale deposits). Unless the RBI addresses this prevailing liquidity deficit (and soon), though, the path of least resistance for deposit rates is likely higher for now.

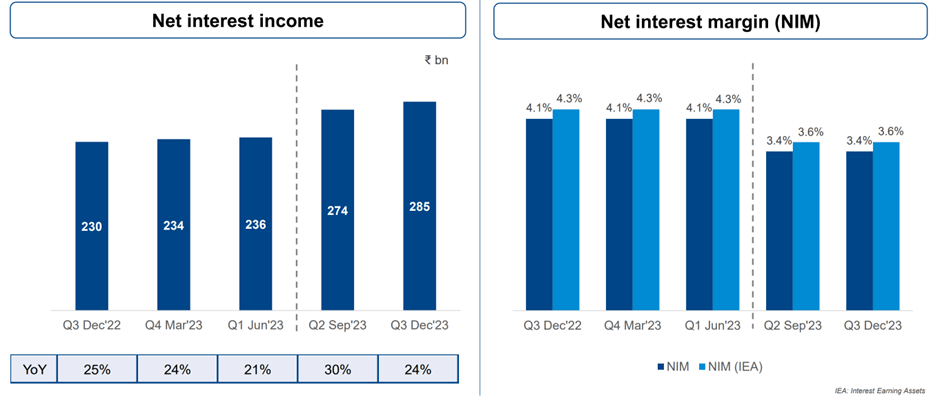

With the worst of the deposit headwinds not yet played out, investors should be very concerned about the bank's path back to pre-merger net interest margin ('NIM') norms (currently 3.4% vs >4% for standalone HDFC Bank pre-merger). Plus, existing low-cost deposits are already well-utilized, as the bank's current ~108% loan-deposit ratio shows, so any incremental uptick in deposit costs will weigh heavily on margins.

{kind=link}

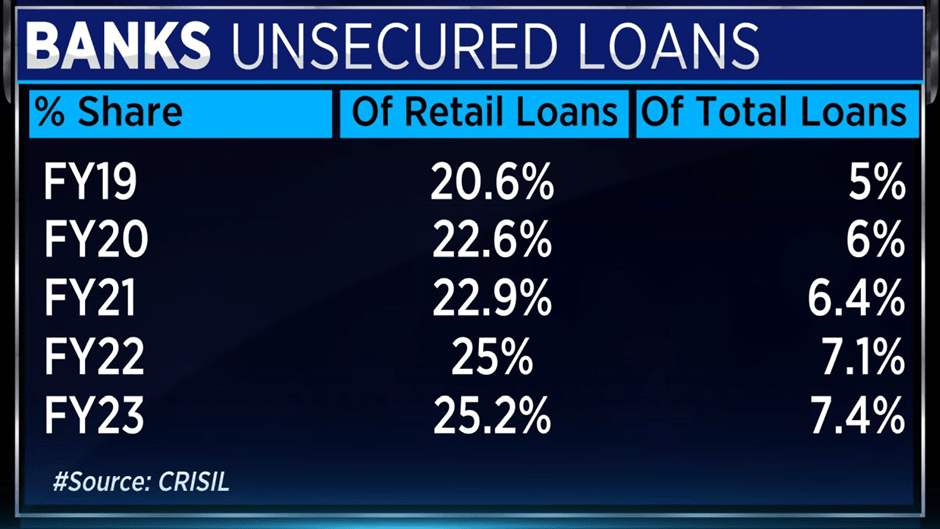

Further complicating the deposit/NIM management task are increased regulatory restrictions on the lending side, particularly with regard to unsecured loans - a major recent driver of credit growth for the Indian banking system. In essence, the bank has one less lever for NIM expansion in the interim, and thus, re-accelerating earnings growth back to pre-merger norms will not be an easy task from here.

Asset Quality Intact; Watch the Capital Ratios

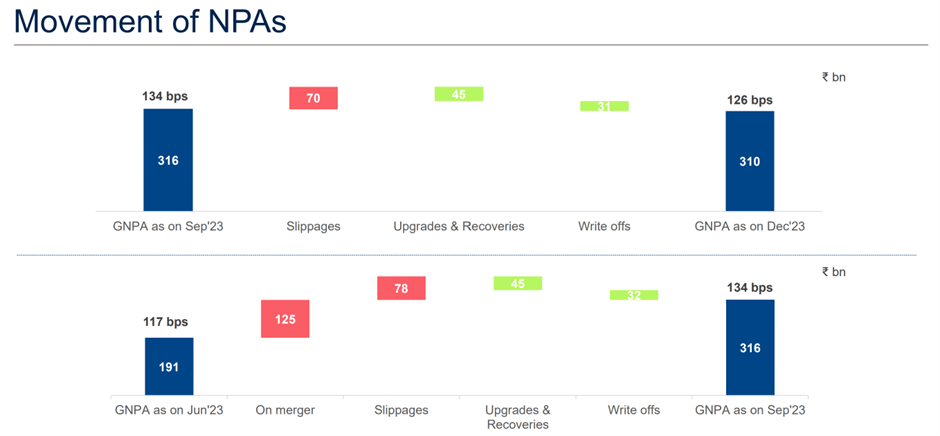

The good news, on the other hand, is that HDFC Bank's post-merger asset quality is trending in the right direction. Non-performing assets are down ~8bps from last quarter to ~1.3% gross, while on a net basis, the non-performing book has improved by a smaller ~4bps to ~0.3%. Digging deeper, the slippage portion (i.e., when loans become 'non-performing') also saw further sequential improvement after the big merger reset, so we may well have cleared the bottom in this regard.

{kind=link}

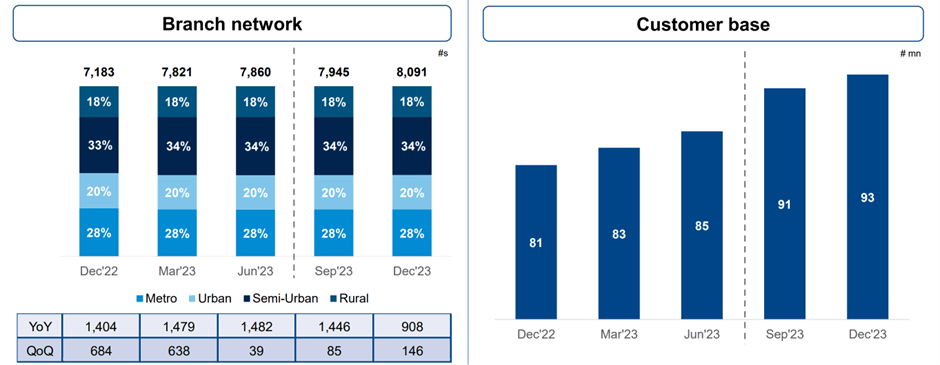

While better asset quality is a positive in and of itself, I wonder if there's a growth tradeoff here - note that branch expansion has also slowed down in fiscal Q3 and now stands at a cumulative 270 for the fiscal year-to-date. The bank has also lowered its branch addition target to 800-1k (vs. 1.5k-2k guided previously); while still very respectable, it doesn't bode well for the kind of credit or deposit growth investors have become accustomed to.

{kind=link}

Plus, there's the capital impact from the RBI announcing sharply higher risk weights for unsecured retail loans for banks. For the system, limiting 'higher risk' unsecured loan growth may well be a good thing for bank and non-bank asset quality. But the 'catch-all' approach to risk weights will probably hurt best-in-class underwriters like HDFC Bank, which thus far has managed the cost side very well. In any case, a capital ratio impact of >25bps won't threaten the balance sheet, but it does impact ROEs at the margin. Perhaps more importantly, cuts off one more growth avenue for the bank - hardly good news at a time when tight system liquidity is already impacting growth and margins.

{kind=link}

Re-adjusting to a New Post-Merger Normal

It's been a tough couple of months for HDFC Bank shareholders, but even with its mega-merger completed, the negative revisions don't appear to be over just yet. The bank appears to be caught in a tough balancing act - getting net interest margins back to pre-merger highs at a time when deposit growth is subpar (vs. loans) and funding pressures are on the rise. If the sector backdrop is anything to go by, things could still get worse before they get better either - rising deposit competition, tighter regulatory constraints, and a pending rate cut cycle point to margins going lower, at least in the near term.

All things considered, the bank's "double every four years" strategy looks far too ambitious post-merger, and until management properly resets its mid to long-term guidance bar (or pulls something big out of the merger synergy bucket), this cycle of downward earnings revisions likely still has legs. Even with valuations now at a relative discount to key peer ICICI Bank (unprecedented pre-merger), I don't yet see compelling value in the post-merger entity here.

For further details see:

HDFC Bank: Why The $21bn Rout Was Not Unjustified