HLIO - Helios Technologies: Make Sure To Look Under The Hood

2023-07-11 00:33:29 ET

Summary

- Helios Technologies is expected to hit $1 billion in sales by 2024, but despite this growth, its EBIT margins have been declining over the past decade.

- The company's stock is currently overvalued by 16%, according to a discounted cash flow analysis, despite positive industry growth forecasts.

- While HLIO is in a transition period following acquisitions, it could potentially boost margins and top-line growth, making it a potential investment opportunity in the future.

Investment Thesis

Helios Technologies, Inc. ( HLIO ) has a solid short and long-term growth narrative with respect to revenue. But when you look under the hood, while the sales - and stock price - were soaring in the past ten years, the EBIT margins were eroding. As a result, the stock looks more than 15% overvalued. Hence, I rate it a hold.

Under The Hood

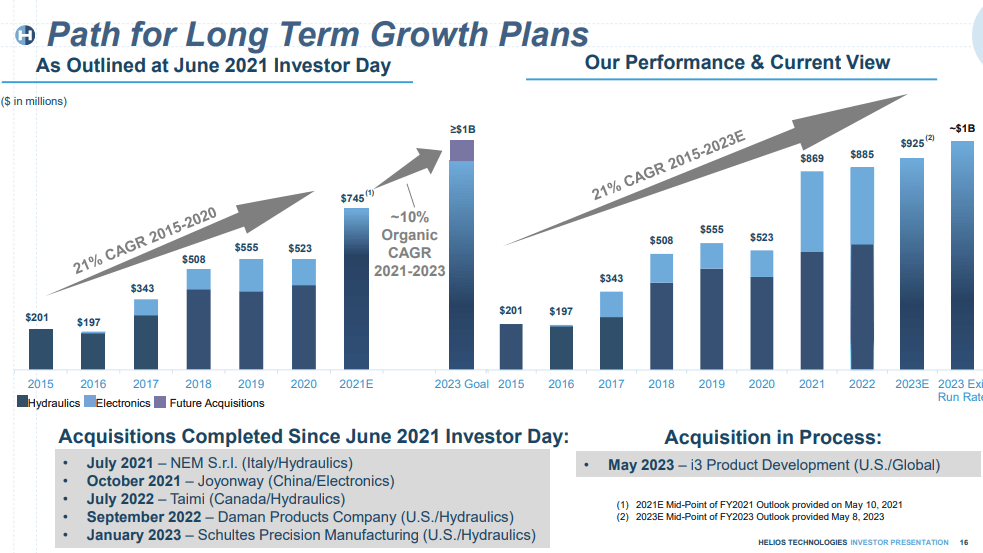

Helios, a manufacturer of electronic control systems and hydraulic components, is tracking to hit $1 billion in sales in 2024, about a year ahead of what they set as a goal back in 2021. They have grown at a CAGR of 21% since 2015, a substantial proportion of which came from acquisitions in 2021 and 2022.

HLIO Sales Growth (Company Q123 Presentation)

{kind=link}

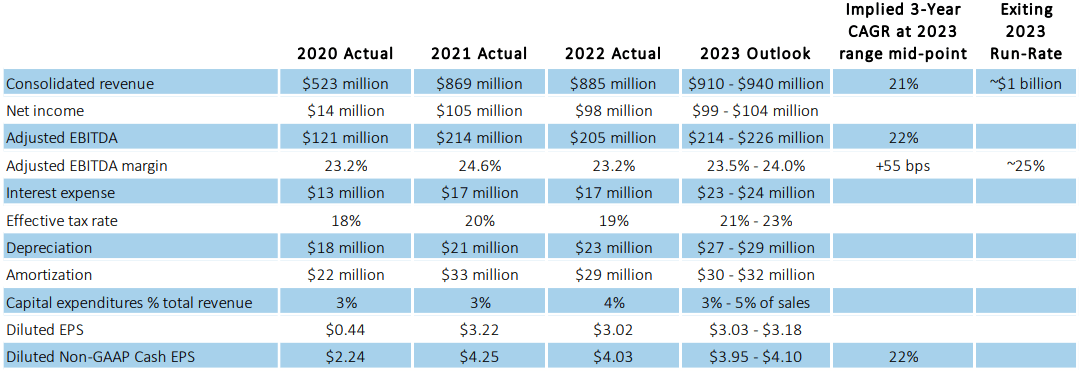

Although the company experienced a major slowdown in Q1 of this year - with sales down 11% year-over-year, and operating profit down almost 40%, Helios says it is still hoping to hit a 4% top line growth target and improved margins. The midpoint for revenue in reiterated guidance is $925 million and the EBITDA margin target is around 24%, which implies an EBIT margin of just over 17% after backing out the projected D&A. This is an important step because, as we shall see, while sales and EBIT grew, the company's margins have fallen dramatically in the past 10 years.

HLIO 2023 Guidance (Q123 Presentation)

{kind=link}

Analysts who cover the stock are almost as optimistic about the revenue targets in the next couple years.

HLIO Analyst Sales Estimates (Seeking Alpha)

{kind=link}

And although they project EPS to fall by almost 8% this year, it is forecast to rebound by over 20% in 2024.

HLIO EPS Estimates (Seeking Alpha)

{kind=link}

The long-term industry forecast also looks favorable for growth. The motion control industry is expected to grow at a CAGR of 5.8% from now until 2027, according to Technavio . Meanwhile, the hydraulic parts market is forecast to grow at a CAGR of 5.3% until 2030, a recent Market Research Future forecast revealed.

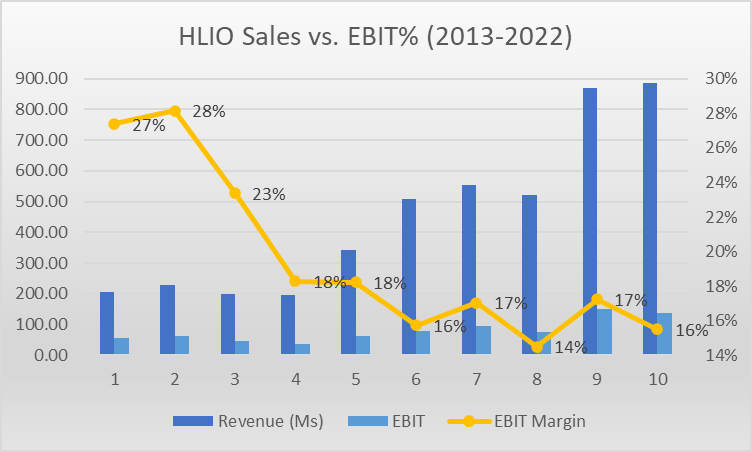

Despite all of these positive indicators, when we take a closer look at the growth picture, there are some concerning trends. For instance, although sales have grown dramatically over the past decade, EBIT margin has fallen steadily and steeply.

HLIO Sales vs. EBIT 10Y Historical (Data Source: Seeking Alpha)

{kind=link}

And, although base on the guidance Helios should see double-digit free cash flow margins in 2023, nearly 20% of the value is driven by depreciation dwarfing capex spend by 160% (while the industry average goes in the other direction).

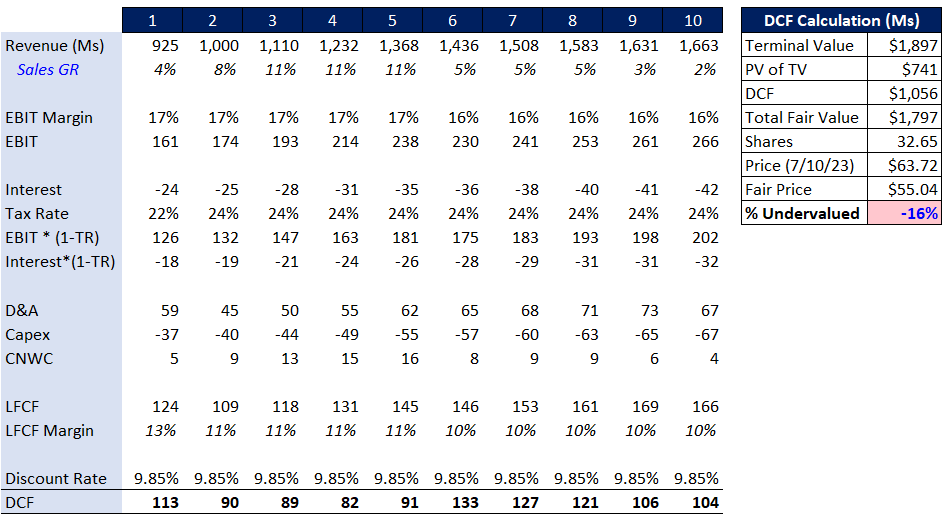

And, most importantly, when you put it all together, the exciting growth prospects still do not justify the current price, which, according to a discounted cash flow analysis, is 16% above the stock's intrinsic value.

Intrinsic Valuation

The good news for the stock analyst in this case is the quality detailed data the company has provided to build a basis for year 1 of our DCF model, which I will lay out here followed by a table that addresses my assumptions for the sales growth rate, EBIT margins, and capex inputs.

HLIO DCF Analysis (MH Analytics)

{kind=link}

| Sales |

|

| EBIT |

|

| Capex |

|

In terms of sensitivity analysis:

Bulls

- Sales GR - For those bullish on the market growth, extending the 11% growth rate until year 10 would still leave the stock 2% overvalued.

- EBIT - If you raise EBIT margin to 18% (assuming we keep our original top line), across the board, the stock would be overvalued by 3%.

Bears

- Sales GR - Conversely, for the bearish, who doubt the growth rate will rise above 8% in the early and middle years, the stock would be overvalued by 21%.

- EBIT - If you lower EBIT to 15% across the board, the stock would be 27% overvalued.

Risks

The main risk is holding onto this stock despite the fact it is potentially overvalued. And, if it is so overvalued, it would be fair to ask why in the world I would give it a hold rating. My thoughts are that this is not a company in decline or distress. It is simply in a transition period post-acquisition spree. When the dust settles, I think there is a good chance the company could turn things around, boost margins and surprise us on the top-line growth, thereby raising the valuation - assuming the stock price does not soar out of proportion at the same time. And to dump a stock only to find it appealing again in a few months, makes for unnecessary transaction costs.

Conclusion

Helios is a high-quality company with solid top-line growth prospects in both the near term and long term. However, these growth forecasts do not justify the current stock price, which is about 16% too high versus its intrinsic value. The problem is, when you look under the hood, while the sales were skyrocketing, EBIT margins were getting squeezed. That said, if the company is able to elevate operating margins in the next couple quarters, it could become an attractive investment. For these reasons, I rate it a hold.

For further details see:

Helios Technologies: Make Sure To Look Under The Hood