HENOF - Henkel: Raising Guidance And Transformation Progressing

2023-11-18 02:51:05 ET

Summary

- Henkel's Q3 results showed a decline in revenue, but organic growth remained positive.

- Management raised guidance for organic sales growth and adjusted earnings per share for the full year.

- The business transformation and merger of the consumer business are progressing well, with positive results in the Hair and Laundry & Home Care segments.

One of the stocks I bought in the last one or two years as protection against a potential recession is the German consumer goods company Henkel AG (HENKY). In my last article - published in July 2023 - I was bullish and wrote that upside potential remains. But that upside potential has not been visible in the stock price development so far. In Euro - the main currency Henkel is trading in - the stock price is the same as in July when my last article was published. And we must admit that Henkel is certainly not the best long-term investment out there as the business is not able to achieve high growth rates anymore and it also doesn't have the best moat.

Nevertheless, Henkel can rely on its brand names and the resulting pricing power and due to the nature of its business and products we can assume a rather high level of recession-resilience. And I also considered Henkel at least fairly valued (or even undervalued) and that's the reason I bought the stock. Last week, Henkel reported third quarter results - reason enough to take another look.

Quarterly Results

I already wrote above that I don't have high growth expectations for Henkel and on the basis of these rather low expectations, the third quarter results were quite solid. Similar to most German companies, Henkel is reporting only a few numbers and metrics in the first and third quarter.

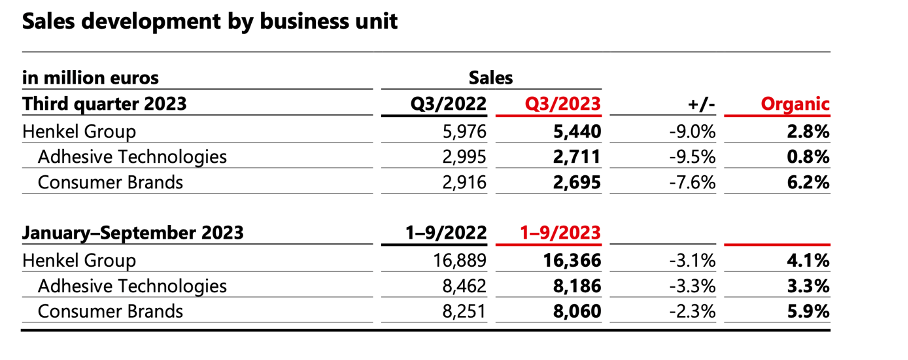

When looking at results, they seem to be a huge disappointment at first. Revenue declined from €5,976 million in Q3/22 to €5,440 million in Q3/23 - resulting in 9.0% year-over-year decline. And both segments were contributing in a similar way to declining sales. While Adhesive Technologies reported a 9.5% year-over-year revenue decline from €2,995 million in the same quarter last year to €2,711 million this quarter, Consumer Brands reported sales declining from €2,916 million to €2,695 million - resulting in 7.6% year-over-year decline.

{kind=link}

So far, these results are nothing to be happy about. But we must point out that Henkel was hit hard by FX effects - similar to Bayer AG ( BAYZF ) ( which I covered recently ) and several other European companies. And when looking at organic growth, Henkel grew its top line by 2.8% year-over-year while Adhesive Technologies reported only 0.8% organic growth and Consumer Brands were reporting 6.2% organic growth. The 2.8% YoY organic growth was the result of volume declining 5.5% while price increased 8.3% and offset the declining volume.

And although Henkel is not providing a lot of information in its earnings release, management gave a few more details during the earnings call. The third quarter trading update does not include margin information. Nevertheless, CEO Carsten Knobel pointed out further improvement in gross profit margin as well as EBIT margin - supported by both business segments. And the CEO also provided some additional information on free cash flow:

Even though, we don't report a Q3 free cash flow number, I would like to share -- I would have assumed Marco would have even been more happy to state that that we have really seen here a significant progress and that we expect this trend to continue also in Q4. And we will end up very clearly above the prior year level in that sense. Very good news. So overall, we are confident to continue on our growth path and we deliver a clear improvement in earnings compared to the prior year.

And while this sounds like good news at first - especially as free cash flow is one of the most important metrics - we should not ignore that free cash flow in fiscal 2022 was only €653 million and therefore much lower than in previous years (in 2021 free cash flow was €1,478 million). However, free cash flow in H1/23 was already €749 million and therefore I assume a much higher number than in fiscal 2022.

Raising Guidance

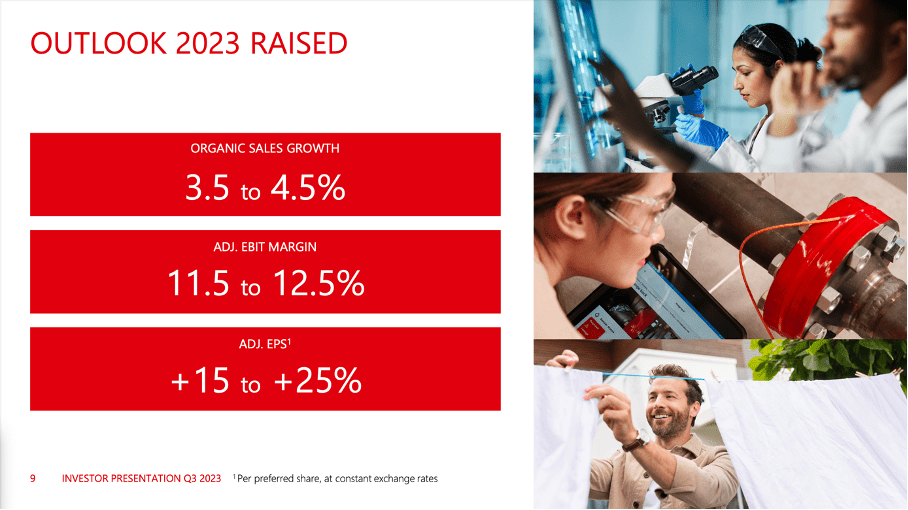

Management was quite optimistic for the rest of the year and after Henkel had already raised its guidance in August 2023, full year 2023 guidance was raised once again. Henkel is now expecting organic sales growth to be between 3.5% 4.5% (compared to 2.5% to 4.5% in the previous guidance). And especially expectations for the bottom line have been raised. While management expected previously for adjusted earnings per share to grow between 5% and 20%, Henkel is now expecting between 15% and 25% growth at constant exchange rates.

Henkel Q3/23 Roadshow Presentation

{kind=link}

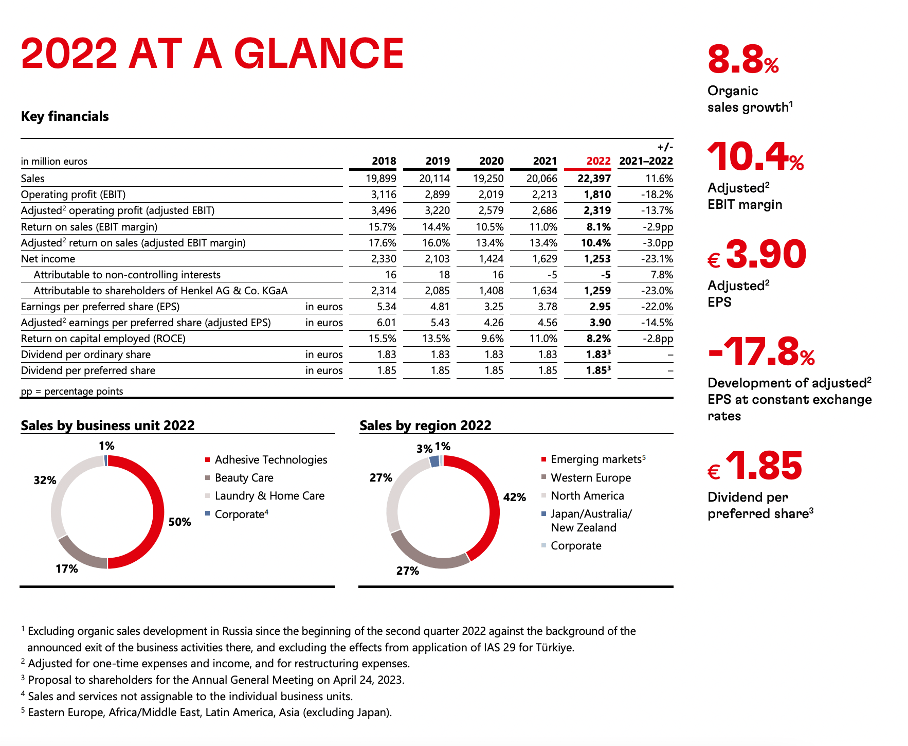

Of course, we should point out that earnings per share in fiscal 2022 were not great. Henkel reported only €2.95 in earnings per share with adjusted earnings per share being €3.90. And as these were the worst numbers Henkel reported in the last five years, it is not such a great achievement to grow in the double-digits.

{kind=link}

Nevertheless, it is a good sign that Henkel can grow its bottom line again and we should be optimistic that Henkel will come back to pre-crisis levels soon and generate $5 and more in earnings per share.

Business Transformation Continuing

Aside from raising the guidance for fiscal 2023, management also gave several hints during the last earnings call that the transformation and merger of the consumer business is underway and successful so far. Henkel is ahead of its own plan and will generate more than 80% of the targeted Phase I savings of around €250 million already at the end of this year.

Henkel Q3/23 Roadshow Presentation

{kind=link}

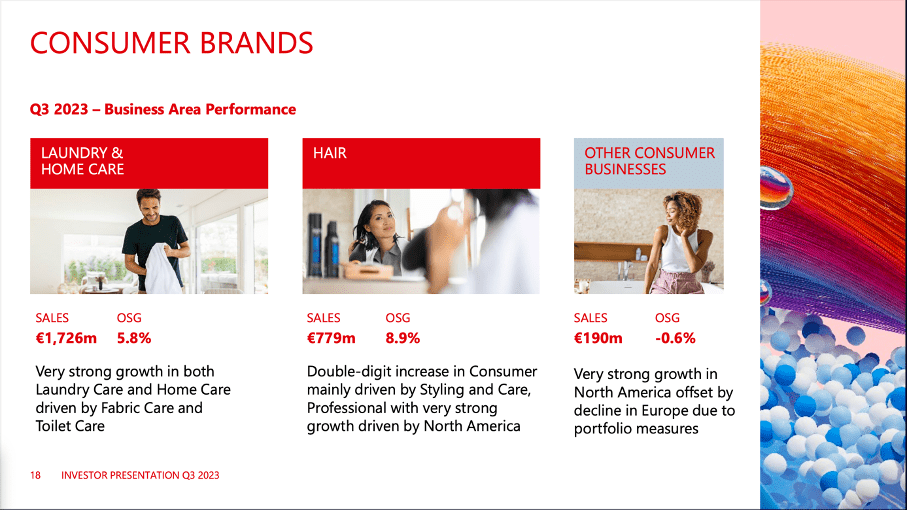

Especially the Hair business, where Henkel started the transformation a bit earlier than in the Laundry & Home Care business is already showing positive results. And in the third quarter, the segment reported 8.9% organic sales growth, which was driven by Styling and Care.

Henkel Q3/23 Roadshow Presentation

{kind=link}

But the Laundry & Home Care business also reported great results. In North America, Henkel now saw the seventh consecutive quarter of organic sales growth. Additionally, Henkel is gaining market share in the important fabric cleaning category. Year-to-date, Henkel gained 30 basis points overall (with ' All standing out and gaining about 50 basis point). Overall, Laundry & Home Care reported 5.8% organic sales growth in the third quarter, and it seems like Henkel is quite optimistic about its Consumer Brands business and raised outlook to 5%-6% growth (compared to 3%-5% in the previous guidance).

And management also pointed out that the transformation is not over:

However, this journey is by no means already at its end. We will continue to work on shaping a winning portfolio, investing into the brand equity and innovations and working on our supply chain in the upcoming quarters. We are highly confident that this will lead us to an even more profitable and faster growing business going forward and that we are well on track in bringing this business back to mid-teens margin levels in the next years. You can expect a more detailed status update on this Consumer Brands merger with our full year call in March 2024.

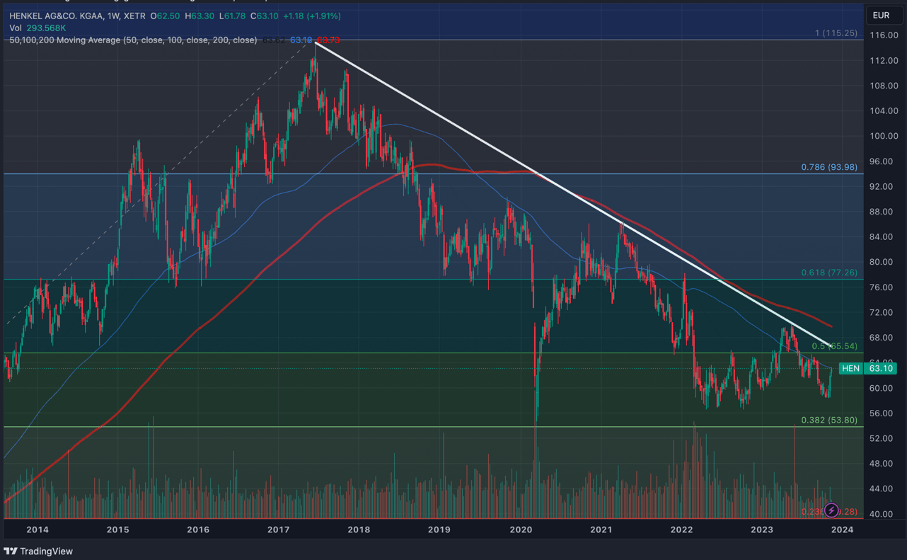

Support Level Holding

And I would also see it as a good sign that the support level around €60 is holding so far and Henkel bounced off that support level for several times in the past. Of course, we never know what will happen and we should not rule out the stock breaking through the support level. But I assume the support level between €55 and €60 consisting of several lows (from the years 2020, 2022 and 2023) will hold. Additionally, we have the 38% Fibonacci retracement of the last major upward wave (between 2009 and 2017) at €54.

Weekly Chart Henkel (TradingView)

{kind=link}

We also should not assume that the stock will just go higher in the coming months as we have resistance levels on the way up. Aside from the white declining trendline, Henkel also must overcome the 50-week and 200-week moving average before we see higher stock prices.

Intrinsic Value Calculation

I calculated an intrinsic value for Henkel several times in the last few years and my conclusion was always that Henkel is undervalued. And we will calculate an intrinsic value once again, but the conclusion is quite similar. As basis we take 419.4 million outstanding shares (combination of preferred and ordinary shares ) and a 10% discount rate. And for fiscal 2023 we assume €1,000 million in free cash flow (although I am optimistic it could be even higher). For the next two years I assume we come back to previous free cash flow levels and in 2024 Henkel will generate $1.5 billion in free cash flow and €2.0 billion in fiscal 2025. For the following years till perpetuity, we assume 5% growth, which seems like a reasonable growth assumption. Calculating with these assumptions leads to an intrinsic value of €83.95 for Henkel (and the ordinary share - the one I would buy - is trading for €63 right now).

Using a discount cash flow calculation is great as we take into account many different scenarios and assumptions and reach a very precise intrinsic value. On the other hand, we must make several assumptions for the coming years - and without a crystal ball it is rather difficult to estimate a precise free cash flow for 2032 or 2038. Therefore, I try to keep it simple and often calculate with the same growth rate for most years - knowing very well how unlikely it is for Henkel to grow 5% annually every year. It might grow 10% in one year and only 1% in the next year, but on average 5% seem like a realistic assumption. Between 1985 and 2022, Henkel grew earnings per share with a CAGR of 7.13% and 2022 was certainly not the best year to use in such a calculation (when calculating a CAGR between 1985 and 2017 we get 10.61%).

Bottom Line

All in all, Henkel is still not reporting impressive results, but we can be confident that the company is on a good path for solid performance in the years to come. The combination of Henkel being undervalued, the stock being close to a strong support level between €55 and €60 as well as the business transformation going well, is making me rather bullish about Henkel and I assume higher stock prices in the years to come.

For further details see:

Henkel: Raising Guidance And Transformation Progressing