HENOF - Henkel: Upside Potential Remains

2023-07-18 08:20:25 ET

Summary

- Henkel reported double-digit top line growth in the recent past, but operating income as well as earnings per share are declining.

- Nevertheless, Henkel can grow its top line along with the overall market and has the potential to improve its margins again.

- We also discuss the question if Henkel has pricing and if the company has a wide economic moat around the business.

- In my opinion, Henkel stock is still undervalued and a solid long-term investment.

Henkel AG & Co. KGaA ( OTCPK:HENKY ) is continuing to struggle, and the stock is still in a bear market with declining stock prices since 2017. When looking at the performance in USD, the total return since my last article was published in February 2023 was 12%, which is a solid performance and was in line with the S&P 500 ( SPY ). However, when looking at the performance in Euro – and Henkel is a German company – the stock price is more or less the same as it was in February 2023 (of course, Henkel paid its annual dividend in the meantime).

Despite the mediocre performance in the last six years, Henkel has not made new lows since 2020 and it seems like the stock could have reached its bottom with a strong support level around €55 to €60 (of course, we should never make the mistake and rule out the risk for lower stock prices). In the following article I will provide an update on Henkel and reiterate my “Buy” rating as I still think Henkel is a solid long-term investment trading for an attractive price.

Results

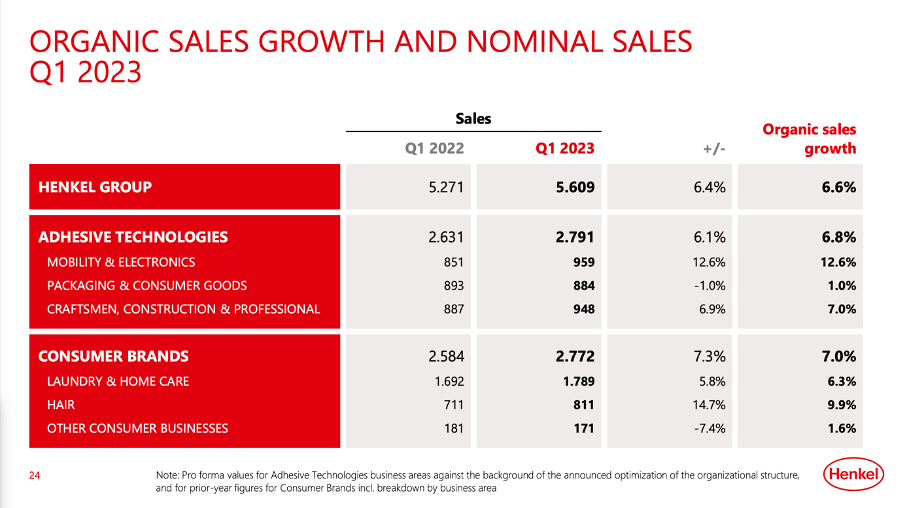

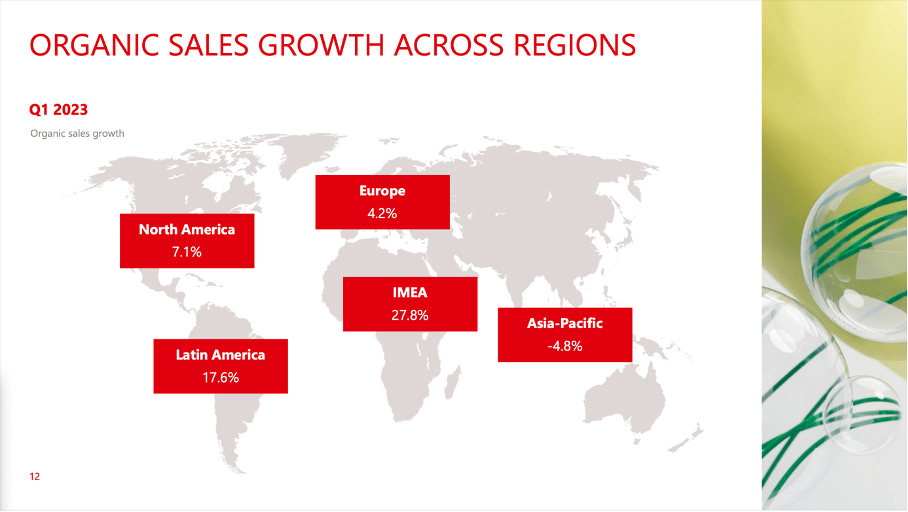

We can start by looking at the quarterly results, Henkel reported in May 2023. Group sales increased from €5,271 million in Q1/22 to €5,609 million in Q1/23 – resulting in a nominal growth of 6.4% and organic growth of 6.6%. Henkel is now reporting in only two business segments – instead of three business segments before. And Adhesive Technologies increased sales from €2,631 million in the same quarter last year to €2,791 million this quarter, while Consumer Brands increased sales from €2,584 million in the same quarter last year to €2,772 million this quarter. When looking at organic growth in more detail, volume declined 5.4% YoY while price increased 12.0%.

{kind=link}

Henkel May 2023 Roadshow Presentation

Similar to many other European companies, Henkel is only reporting a few selected numbers and metrics in Q1 and Q3 and therefore we can also look at the company’s annual results for fiscal 2022. Sales in 2022 increased 11.6% year-over-year from €20,066 million in fiscal 2021 to €22,397 million in fiscal 2022. But while the top line increased with a solid pace, operating profit declined from €2,213 million in fiscal 2021 to €1,810 million in fiscal 2022 – resulting in 18.2% year-over-year decline. And earnings per share declined even 22.0% YoY from €3.78 in 2021 to €2.95 in 2022. Adjusted earnings per share were €3.90 in fiscal 2022 but still declined 14.4% YoY from €4.56 in the previous year.

{kind=link}

Henkel Annual Report 2022

Guidance - Fiscal 2023

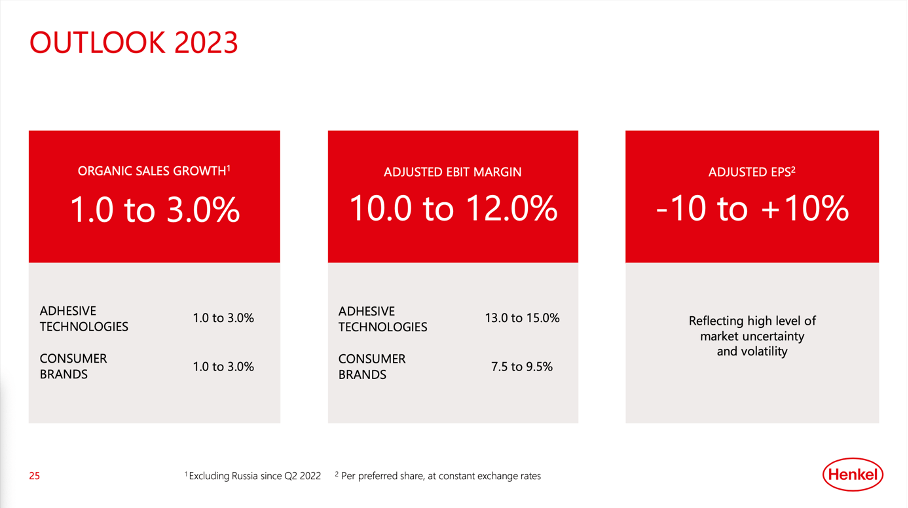

When looking at the guidance for fiscal 2023, Henkel is expecting organic sales growth to be in a range between 1.0% and 3.0%. Adjusted EBIT margin is expected to be between 10% and 12% compared to 10.4% in fiscal 2022. And finally, adjusted earnings per share are expected to be in a range between a 10% decline on the low end and a 10% increase of the high end.

{kind=link}

Henkel May 2023 Roadshow Presentation

And during the last earnings call , management was rather optimistic about rather reaching the top end of its guidance range:

Today, we confirmed our full year guidance. But of course, given the strong top line momentum in the first quarter, we also have a higher confidence today to reach the upper half of the organic sales growth guidance range.

Long-term Growth

And although Henkel has been struggling in the last few years and the guidance for fiscal 2023 is once again not what it should be, we can remain long-term optimistic. According to many different studies, Henkel’s business will not see high growth rates, but solid low-to-mid single digit growth for sales seems likely as the underlying market is expected to do the same. When looking at the laundry care market, studies are expecting growth rates of 3.9% for the decade to 4.9% growth till 2030 . For the hair care market, growth rates are expected to be between 3.7% and 5.4% according to different studies. Likewise, growth rates ( around 5% ) are expected for the adhesive market.

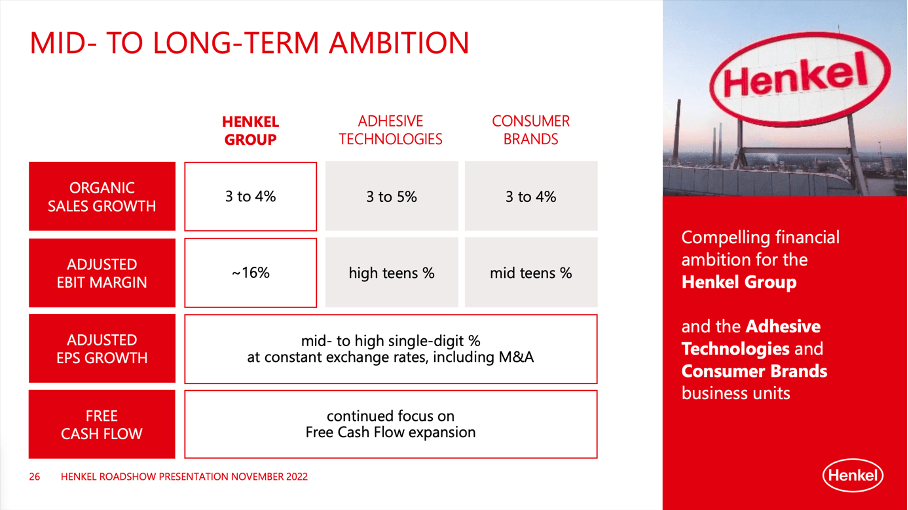

And at least in the November 2022 Roadshow presentation, Henkel still had included its mid-to-long term ambitions and the company is expecting organic sales growth to be between 3% and 4% and adjusted earnings per share are expected to grow in the mid-to-high single digits.

{kind=link}

Henkel November 2022 Roadshow Presentation

Overall, Henkel can pull several levers to grow in the years to come:

- Growing sales and a growing top line will contribute to bottom line growth and as demonstrated above, Henkel can probably grow in the low-to-mid single digits by just keeping its market share and growing in line with the overall market.

- Henkel might be able to improve its margins again over time. The goal is to reach an adjusted EBIT margin of 16% again and this would have a significant effect on the bottom line.

- And finally, Henkel could use share buybacks once again after it recently repurchased about €1 billion worth of shares (we will get to this). And with moderate debt on the balance sheet, Henkel could buy back shares again.

Pricing Power and Economic Moat

During the last earnings call, an analyst asked about Henkel’s pricing power and if Henkel is not pushing pricing to far (which could backfire and increase the risk of customers switching to cheaper competitors):

So the first one is on competitiveness in Consumer Brands because your pricing has been 3 consecutive quarters in the low to mid-teen territory. You seem to signal this morning, there is more pricing to be implemented over the coming months.

(…)

So my question here is, are you not pushing pricing too far? And as a result, could we see a scenario whereby pricing will have to be adjusted downwards later this year?

And it seems understandable to raise that question: How high is Henkel’s pricing power and how strong is the economic moat around the business? Price increases of 12.0% year-over-year (for the first quarter of fiscal 2023) are clearly above inflation. CEO Carsten Knobel responded:

Let's start with the situation when you talked about the competitiveness in our HCB business. I think we have been discussing quite a while how strong a business is in terms of being -- in terms of solid, in terms of brands and portfolio, also in the context of being able to bring price increases through.

I think we have been showing that, I would say, very clearly in 2022, that we have been able to bring prices to respective amount through, we see it in Q1 of this year that in HCB we have double-digit pricing in that context.

And yes, as you are saying, we are also seeing additional pricing activities which we will and -- which are foreseen to be implemented in the next couple of weeks/months.

And if Henkel would pull off the price increases without losing customers, it would be a strong sign for the company’s pricing power. On the other hand, Henkel also reported declining volume and customers purchasing less products. This could just mean that demand from the same customers is lower, but it could also mean that some customers won’t purchase from Henkel anymore. Management indicated during the earnings call that it was rather weak demand – in this case for the Adhesive Technologies segment:

Volumes were below prior year, but the decline of minus 4.6% was comparable to what we have seen in Q4 last year, which already was impacted by the rather weak market in China which also affected us in the first quarter.

We also must differentiate between the two business segments. In Adhesive Technologies, Henkel certainly has a wide moat around its business and most likely has pricing power – but especially due to the high switching costs. In its Customer Brands business, the moat is probably not so strong and based on the brand names of the different Henkel products. If Henkel will continue to raise prices aggressively, customers might switch to the cheaper products of a competitor.

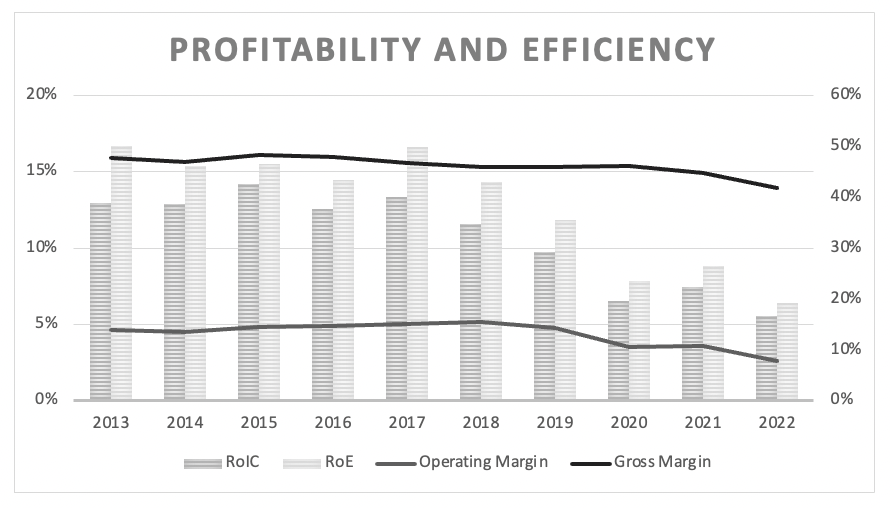

And when looking at the last ten years we clearly see margins declining over time. Not only operating margin is declining in the last few years, but also gross margin and this is a clear sign for missing pricing power. In 2015, gross margin was still 48.2% and then declined to 41.8% in 2022. We should also not exaggerate this fact as the decline is not dramatic, but it is not a great sign either.

{kind=link}

Henkel: Margins and return on invested capital (Author' s work)

And when talking about pricing power and looking at the double-digit price increases Henkel reported in the last quarter, we should not ignore that high price increases in some regions are also stemming from hyper-inflation – countries like Turkey or Argentina are coming to mind. However, these countries are contributing only a small part to overall sales.

{kind=link}

Henkel May 2023 Roadshow Presentation

Dividend and Share Buyback Program

Henkel once again paid an annual dividend of €1.85 for its preferred share and €1.83 for the ordinary share – the same dividend the company paid in the last few years. When looking at the payout ratio, it is not perfect but also no reason for concern. When using earnings per share, the payout ratio is 63%, when using the adjusted earnings per share we get a payout ratio of 47%. And the current dividend is resulting in a dividend yield of 2.9% right now, which is solid but certainly no reason to invest in Henkel right now.

{kind=link}

Henkel Investor Relations

At the end of March 2023, Henkel also completed its first share buyback program . The company bought back shares worth about €1 billion. As Henkel is having a market capitalization around €30 billion right now this will add about 3.3% growth to the bottom line.

Intrinsic Value Calculation

Of course, when taking fiscal 2022 EPS of €2.95, Henkel is trading for 21 times earnings right now – which does not seem like an extreme bargain. When using adjusted earnings per share, Henkel is trading for 16 times earnings. We should always keep in mind that Henkel was struggling in the last few years and could not really grow – this is begging the question if Henkel deserves a high valuation multiple.

Nevertheless, I would stick to the intrinsic value calculation of my last article. In February 2023, I calculated an intrinsic value by using several different assumptions leading to four different numbers what Henkel should be worth. Most realistic in my opinion is an intrinsic value around €90 and still resulting in almost 50% upside potential for the stock.

Of course, these assumptions could also be seen as too optimistic as I calculated with growth rates between 5% and 6% in the different scenarios and a free cash flow of €1,500 to €2,000 as basis. And neither are we seeing such growth rates nor was the free cash flow in fiscal 2022 anywhere close to these numbers. Free cash flow in fiscal 2022 was €653 million, in fiscal 2021 it was €1,478 million. But long-term I am optimistic these growth assumptions and assumptions for free cash flow are realistic.

Conclusion

In my opinion, Henkel remains a long-term buy and I would also expect the business to perform rather well in the short-to-medium-term. We are talking about a rather recession-resilient business and therefore Henkel will most likely perform solid even in a challenging environment: While the Adhesive Technology segment might suffer more during a recession, the Consumer Brands products will most likely still be purchased even during an economic downturn.

And while I see the stock price well supported in the range between €55 and €60 (data for the ordinary share), this does not mean we cannot expect another steep decline as investors’ sentiment can be decoupled from the fundamental performance of a business.

For further details see:

Henkel: Upside Potential Remains