HENOF - Henkel: Waiting For Profitability To Recover

2023-09-06 00:15:14 ET

Summary

- Shares of Henkel are a hold as I look for profits to recover with the company trading at 21.6x TTM P/E and free cash flow yields around 4.3%.

- Henkel's organic revenue grew by 4.9% in the first half of the year, driven by growth in both the Consumer Brands and Adhesives Business.

- Operating profit increased by 7.6%, and adjusted EPS grew by 14.4%.

- Henkel's profitability has declined in recent years, but first half year 2023 results are starting to look promising.

Shares of Henkel ( OTCPK:HENKY ) have my attention again in an expensive market with the consumer staple and adhesive company trading around 21.6x TTM P/E with a dividend yield of 2.91%. Since I last wrote about Henkel back in December 2020, the company has underperformed the market significantly with a total return of negative 21.6% compared to the S&P 500's return of 22.2%. This has been largely due to declining profitability at the company as this article will discuss and as the trend gets longer, I become more cautious about when, and if, it will come back up to historic averages.

Revenue continues to grow nicely but profitability at Henkel has been weak in recent years and I would like to see this trend reverse before investing any new money in the company. In the first half of the year, EBIT margin increased 80 basis point to 11.50% supported by the higher prices, by savings from the creation of the integrated Consumer Brands business unit and by portfolio optimization measures. These are good signs at the half-year mark and I will be watching for full year results to continue this margin expansion back towards historic norms.

Latest Half-Year Results

Organic revenue grew by 4.9% in the first half of the year to around €10.9 billion (nominal 0.1%) with growth in both the Consumer Brands business and the Adhesives Business. Foreign exchange effects had a negative impact on sales of 2.5% and acquisitions/divestments reduced sales by 2.2%. Adhesive Technologies recorded very strong organic sales growth of 4.7%, driven by the Mobility & Electronics and Craftsmen, Construction & Professional business areas. Consumer Brands achieved very strong organic sales growth of 5.7%, driven by the Laundry & Home Care and Hair business areas.

Operating profit grew to €1,254 million (+7.6%) helped by EBIT margin increasing 80 basis point to 11.50% supported by the higher prices, by savings from the creation of the integrated Consumer Brands business unit and by portfolio optimization measures. All of this led to adjusted EPS increasing to €2.13 for double-digit growth of 14.4% at constant exchange rates.

Management raised guidance for full year organic sales growth of 2.5% - 4.5% (previously 1.0% to 3.0%), EBIT margin of 11% - 12.5%, and EPS to increase in the range between 5% - 20%. So far, the results for the first half of the year outpace these results so management is looking conservative amid a weakening economy.

Henkel had announced the exit of its Russian operations following the Russian attack on Ukraine last year and on April 20, 2023, they announced the signing of an agreement to sell their business activities in Russia to a consortium of local financial investors. The transaction has been closed, and the sale price amounts to 54 billion rubles (around €600 million).

Quick Intro To The Company

Since being founded in 1876 as a laundry detergent manufacturer, Henkel has grown into a global powerhouse spanning Laundry & Home Care, Beauty Care, and Adhesive Technologies. While investors in the U.S. may not be familiar with the name Henkel, they might be surprised that they are familiar with some of the company's brands such as Schwarzkopf hair products, Dial soaps, or Persil and Purex laundry detergents. As of the 2022 fiscal year , only 27% of sales still come from Europe with a growing percentage coming from North America (27%) and emerging markets (42%).

Henkel's more industrial-focused Adhesive Technologies segment is by far the largest segment generating sales of 50% of their sales as of 2022. Interestingly, this adhesive segment was founded out of necessity in 1923 when the glue supply used in the packaging of its consumer products was interrupted, forcing the company to create its own supply using its chemical manufacturing knowledge. In my opinion, the company knows what it does well and that is chemicals manufacturing whether it be the production and sale of soaps, detergents, or adhesives.

Henkel Sales by Segment and Geography (from Henkel 2022 annual report)

Shrinking Profitability

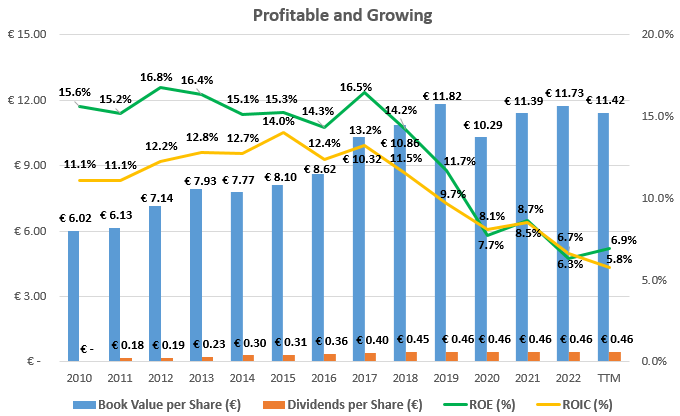

Over the past decade, Henkel has achieved average return on equity ((ROE)) and return on invested capital (ROIC) of 12.9% and 10.7% respectively. This level of profitability is above my rule of thumb of 9% ROIC but below my 15% rule of thumb for ROE due to the low financial leverage being utilized at Henkel. I would not mind seeing the company use more debt in the capital structure to leverage ROE.

The worrying part of the above slide is the decline in profitability since 2018. Looking at their margins across the board over the years, I can see this is due to cost of goods sold increasing 3.1% from the 2018 period and selling, general and administrative expenses increasing 2.9% which drove net income margins down 5.5% to be 6.1% in the TTM period compared to 11.6% back in 2018.

Historical Profitability and Growth at Henkel (compiled by author from company financials)

{kind=link}

In 2022, profitability decreases were seen in Laundry and Home Care where adjusted EBIT margin fell from 13.7% to 8.6% and the Beauty segment where EBIT margin fell from 9.5% to 7.8%. The companies largest Adhesive segment also saw EBIT margin fall from 16.2% from 13.6%. I would like to see this trend reverse before putting any new money to work as the recent war in Ukraine cannot explain the now 5 years of profitability struggles.

On the growth side, book value per share has grown from €6.02 in 2010 to €0.46 in the latest quarter, which, when combined with the dividends paid out from equity, has averaged growth of 9.3% annually. In terms of revenue per share, they have grown from €8.69 in 2010 to €13.08 in the TTM period for an average annual growth rate of 3.2%. This is not a great growth rate but shows the company holding its ground against inflation.

Returning Cash To Shareholders

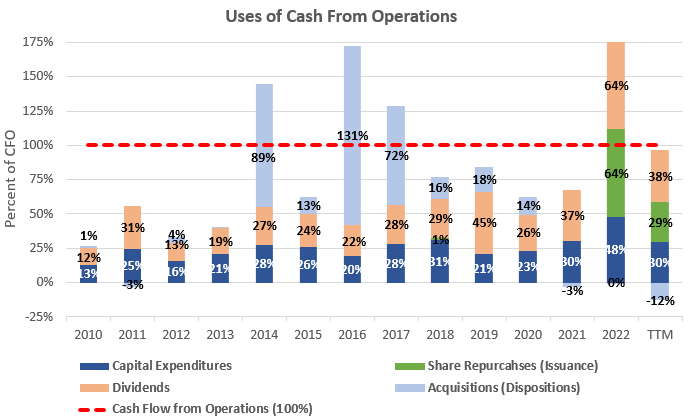

Henkel does a good job of returning cash flow to shareholders through the form of dividends and share repurchases. With capital expenditures and acquisitions only taking up on average 24% and 26%, respectively, of cash flow from operations since 2010, this leaves approximately 50% to be returned to investors through the form of dividends and share repurchases. With average cash flow from operations of $2,407 million over the past five years, this 50% would imply free cash flow available to shareholders of $1,205 million for only a 4.3% free cash flow yield at the current $28.4 billion market capitalization.

Cash Flow Analysis (compiled by author from company financials)

{kind=link}

Strong Financial Position

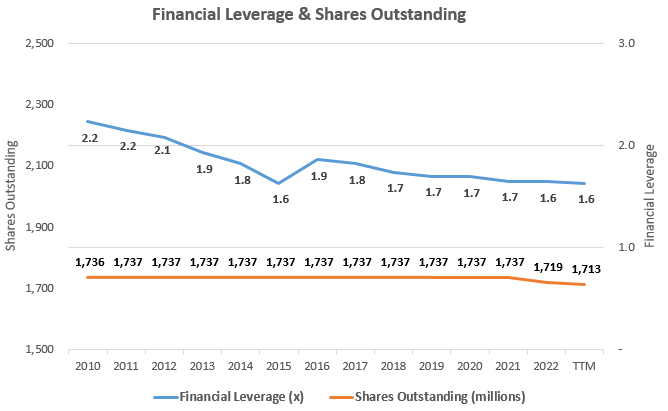

Debt levels at Henkel are quite reasonable with a current financial leverage ratio of only 1.63x in the most recent quarter and operating profits providing a conservative interest coverage level of 17.1x. As mentioned earlier, I would not mind seeing the company use more debt in the capital structure to leverage ROE.

While the company's capital allocation policy has not contained any share repurchase programs before the past two years which I like to see, Henkel has not been issuing shares in order to pursue expensive acquisitions either. In my opinion, this shows management and the board of directors is inclined to behave responsibly and not pursue grand acquisitions that would potentially dilute shareholders or raise debt significantly. I am excited by the share repurchases in the latest couple years and hope that they continue.

Financial Leverage & Shares Outstanding (compiled by author from company financials)

{kind=link}

Takeaway for Investors

Shares of Henkel have my attention again with a historical free cash flow yield around 4.3% and trading at 21.6x TTM P/E. The company is conservatively financially leveraged for a part consumer staple company and could be leveraging ROE higher in my opinion. Before putting any new money to work with Henkel, I would mainly like to see profitability continue to recover and hold over half-year increases seen so far, but I will continue to collect the dividend yield of 2.91% in the meantime.

For further details see:

Henkel: Waiting For Profitability To Recover