HEES - Herc Holdings Inc.: Own This Infrastructure Play Bolstered By Strong Tailwinds

Summary

- Herc Holdings is a profitable, inflation resistant business that is supported by strong tailwinds.

- Being placed as one of the top three industry players gives HRI a moat over its smaller competitors.

- HRI is led by an experienced management team that has proven that they know how to execute and have been executing well, increasing top and bottom line.

- HRI is a buy for investors looking for more growth than the most established equipment rental operators can offer.

Thesis

Herc Holdings ( HRI ) is a profitable and inflation resistant business that is supported by strong tailwinds. Being placed as one of the top three industry players gives HRI a moat over its smaller competitors. HRI is led by an experienced management team that has proven that they know how to execute and have been executing well. It has recently started to pay a dividend at 1.85% yield that can attract a new profile of investors. HRI is a buy for investors looking for more growth than the most established equipment rental operators can offer.

Bullish Reasons

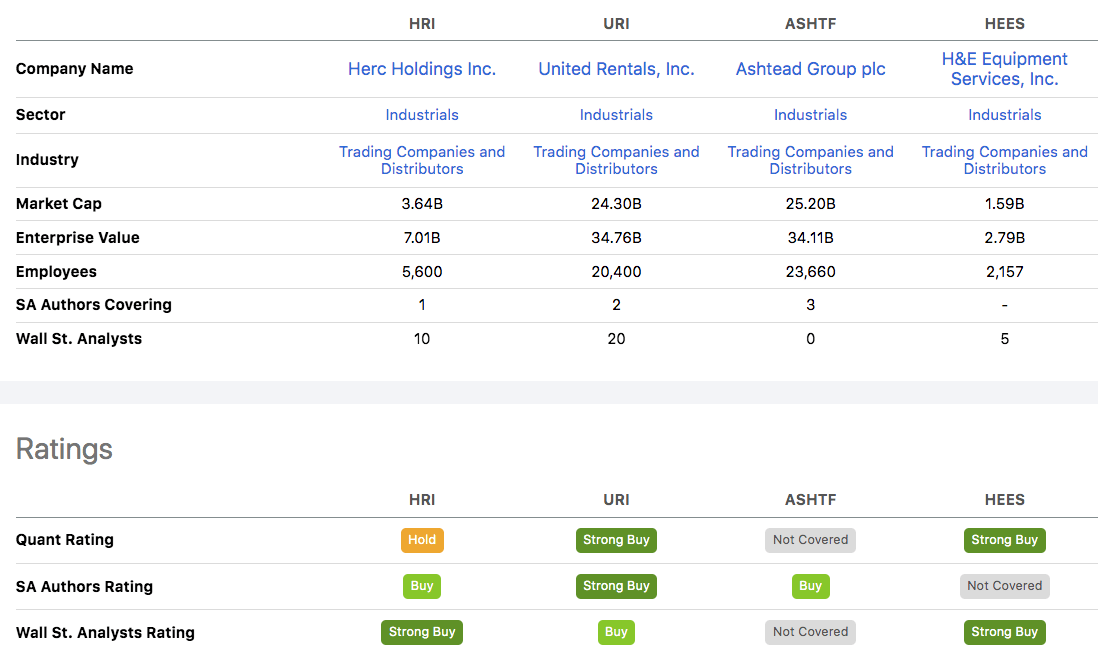

There are many bullish reasons to own equipment rental businesses like HRI, United Rentals ( URI ), Sunbelt/Ashtead ( ASHTF ) and H&E Equipment (HEES).

{kind=link}

Seeking Alpha Peer Comparison

In this article, I will cover the tailwinds that are supporting this industry, the risks that HRI faces, and how it is mitigating these to still come out strong against its competitors, and provide my valuation of the business.

Before that, let's get something out of the way first, which is a declining housing market will drag down HRI's business . A declining housing market is well-documented. I have covered that extensively in my article of Mueller Industries ( MLI ). A decline in the housing market is however largely a non-issue for HRI as its core business is not in residential construction, but is in the non-residential construction business.

In the most recent earnings conference call, CFO Mark Irion said,

The housing market, residential market really doesn't swing our business very much at all... It is really a smaller piece of our business. We're very balanced with industrial government, commercial contractors, larger projects.

With that out of the way, let's start discussing the tailwinds.

Strong Mid- and Long-Term Tailwinds

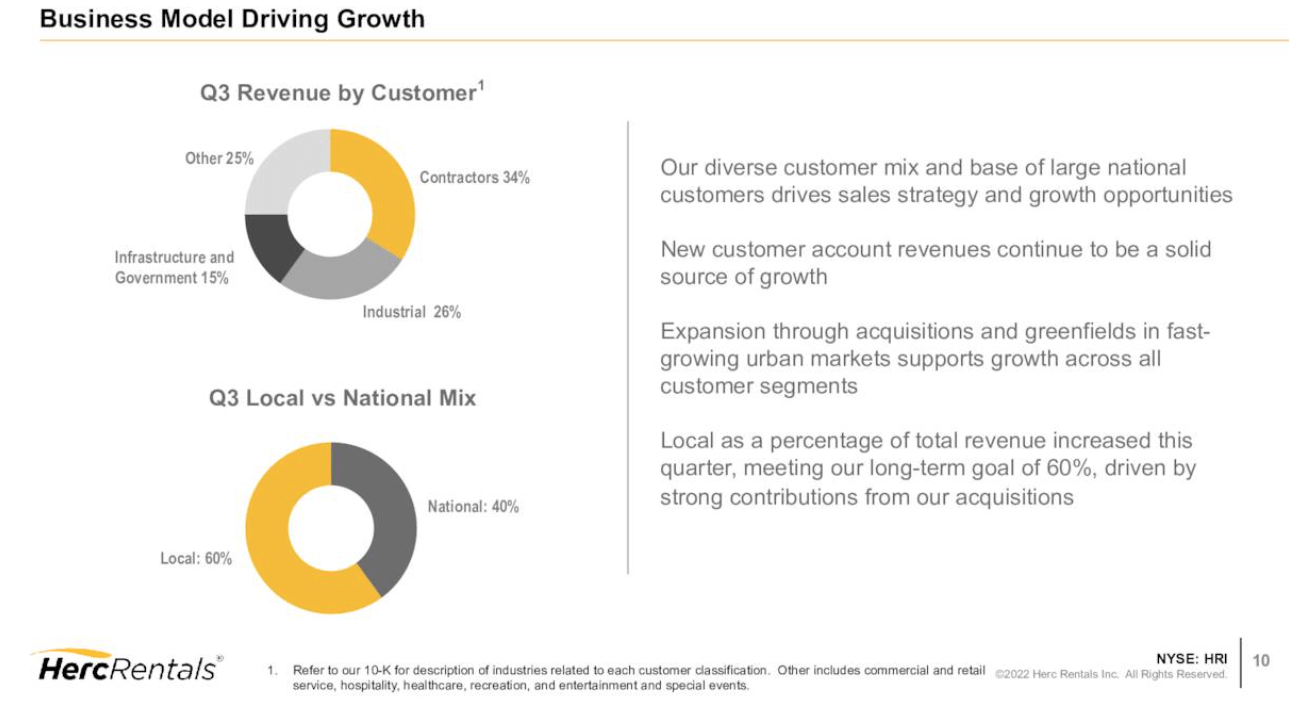

The strong tailwinds are coming from the non-residential (Contractors, and Infrastructure and Government) and industrial segments. HRI's revenues come primarily from Contractors (34%), Industrial (26%) and Infrastructure and Government (15%), making up 75% of the total revenue. Residential-related revenue forms part of the remaining 25% under "Others".

{kind=link}

Q3 2022 Earnings Presentation Slides

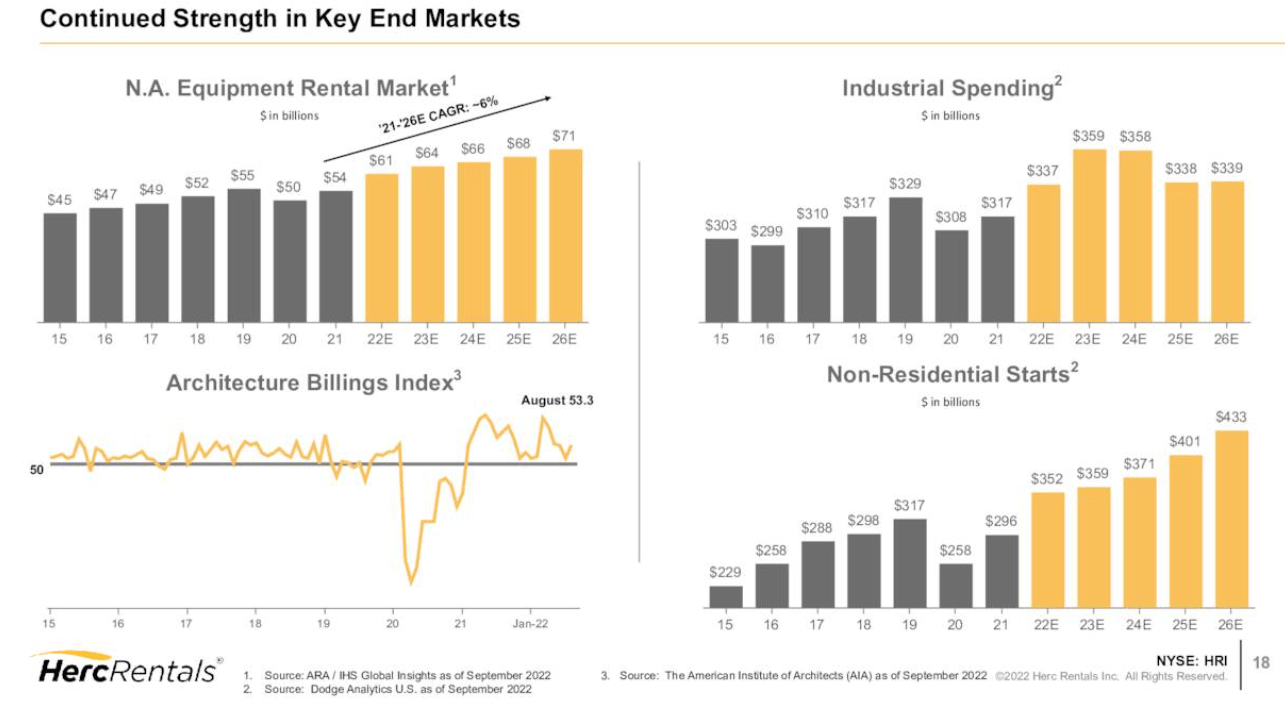

HRI's two key end markets are industrial spending and non-residential construction. Both did well in 2022, and the forecasted spending remains robust for 2023 and 2024. Combined these end markets reflect about two-thirds of HRI's customer base and both are likely to outperform other more consumer driven markets in 2023.

{kind=link}

Q3 2022 Earnings Presentation Slides

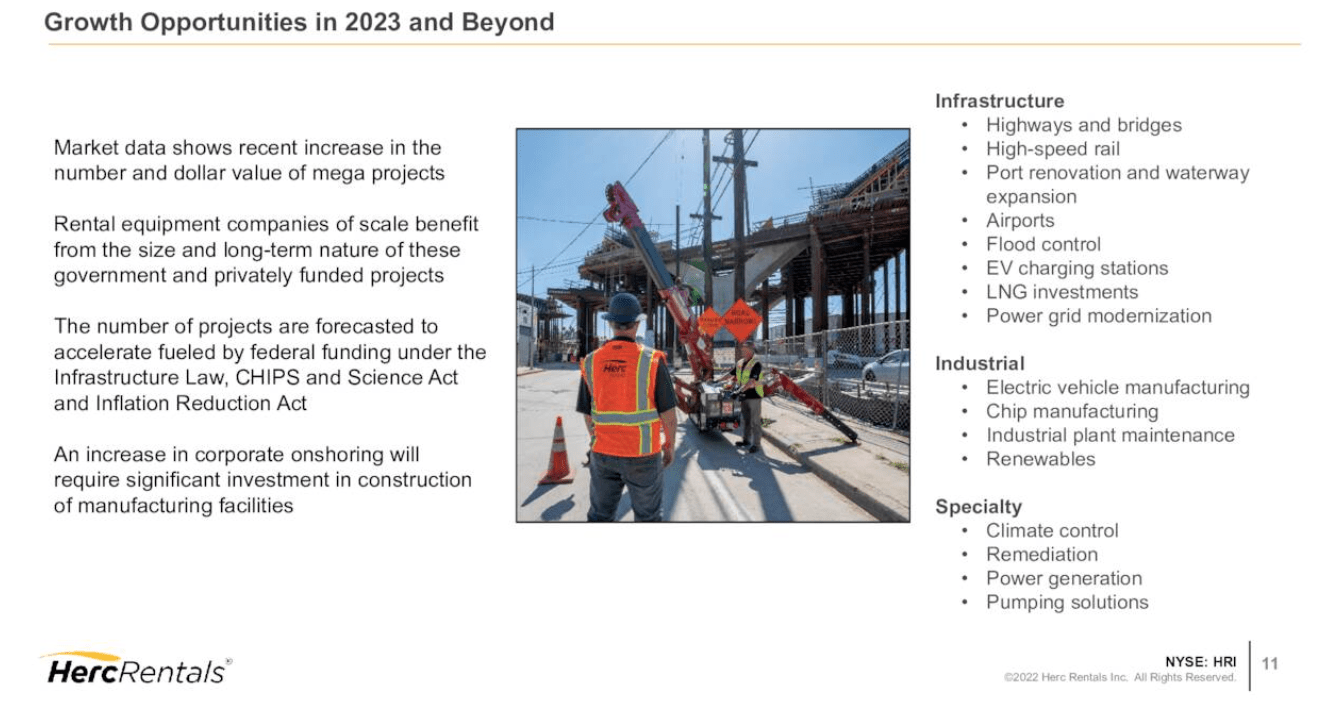

Keep in mind the $110 billion from the infrastructure bill will flow into the construction industry which includes federal spending, highways, bridges, roads, electric vehicles and electric vehicle chargers, power systems, water infrastructure, internet broadband infrastructure, and modernizing ports, airports, and waterways, all which will drive further infrastructure spending and strengthen demand for rental equipment.

Strong Long-Term Tailwinds

I mentioned infrastructure spending earlier. There is also additional demand for construction in niche areas like data centers, and electric vehicle manufacturing plants. The Sino-American tensions are well-known and with trade restrictions coming one after another, the issues between these two global competitors are not coming to a resolution anytime soon. These spell an urgent manufacturing shift from off-shoring to on-shoring. Intel ( INTC ) building foundries in the United States is one prominent example of this on-shoring movement. Another will be the increasing competition among car manufacturers to build electric vehicles, with many CEOs making bold claims to have fully electrified fleets by the end of the decade. All these and more provide solid tailwinds for increasing demand for HRI's services.

{kind=link}

Q3 2022 Earnings Presentation Slides

And even before the Infrastructure Bill came to being and the rising global tension increased the pace of the shift to on-shoring manufacturing, there has already been a decades-old transition to an asset-light business model that benefits equipment rental companies like HRI and URI. To reduce the cost of starting a construction business, for instance, instead of buying all the expensive equipment like cranes and bulldozers, companies can opt to rent this equipment. This is another long-term tailwind that bodes well for HRI.

Strong Short-Term Tailwind

The supply chain issues of 2021 and 2022 have resulted in a shortage of equipment that can be delivered from OEMs to their clients. This leads to increasing demand for the equipment-for-rent business.

Stability In Revenue

HRI a recurring revenue component called the National Association Program. It has yearly contracts with large companies and these contribute 40% of the total revenue.

Q3 2022 Earnings Presentation Slides

This 40% figure actually came down from a previous 60% and that is deliberate on management's part, who want to keep growing the revenue contribution from the national piece while targeting more of a local mix because the latter provides higher margins than the national accounts. This, according to management, also affords HRI a faster turnover where it could accelerate and penetrate the local markets and not totally be reliant on the national account base.

Effective Execution

The abovementioned bullish tailwinds mean nothing if management cannot execute. Apparently, the management at HRI has been able to do so, despite being spun off from Hertz ( HTZ ) in 2016 with almost $2 billion in debt, and having to face several macro-event level crises in its short history, namely the pandemic and the housing market slowdown that is affecting the construction industry for the residential market.

At the helm of Herc Rentals is CEO Larry Silber. He has great reviews on Glassdoor. His right-hand man, COO Aaron Birnbaum, has been with Herc Rentals and its predecessor business for more than 30 years, so he has in-depth experience in the workings of the business and an understanding of what works for different business cycles. These alone are insufficient to say much. Results speak louder.

{kind=link}

Glassdoor

Under the present leadership, the company has posted good results. From 2016 to 2021, revenue went up by 33.3% (from $1555 million to $2073 million), net operating cash flow improved by 71.8% (from $433 million to $744 million), diluted earnings per share increased by 837% (from -$0.70 to $7.37), and free cash flow per share increased by 7850% (from -$2.92 to $3.36).

The company posted strong operating results in the most recent quarter. Equipment rental revenue increased by 36% over 2021, driven by strong performance in the core business. The company continues to grow market share from the higher margin specialty businesses (Pro Solutions) and through the contribution from 16 acquisitions to date and expanded 24 new greenfield locations. Total revenues grew 35% despite lower sales from the sale of used equipment. Adjusted EBITDA grew 40% over the prior year. Adjusted EBITDA margin went up 160 basis points to 46.3% in the third quarter of 2022. Management was so confident that going into Q4 2022 it raised the full-year guidance for adjusted EBITDA from the previous $1.19 billion to $1.24 billion range, to $1.22-$1.25 billion, a 36% to 40% increase over the 2021 results.

Risks And Mitigations

All this impressive growth came despite the challenges faced by the company. In this segment, I will discuss some of the key risks and threats facing HRI, and how it is mitigating these.

The main risk will be competition and that can come from several directions.

Threat From OEM Raising Prices And Competition From OEM's Rental Business

HRI can face issues in two ways. The first is OEMs that offer their own equipment rental (for instance Caterpillar and Deere offer their own equipment for rental). It is not difficult to see a scenario where these OEM businesses raise the prices of the sale of equipment-to-equipment rental companies like HRI and URI as a competitive move to reduce their margins.

At the same time, HRI may find it difficult to pass the rising costs to their customers because the rental business is a competitive, cut-throat one. One of the business risks mentioned by HRI in its 2021 annual report is precisely this.

Competition in the equipment rental industry is intense, often taking the form of aggressive price competition. Other competitive factors include customer loyalty, changes in market penetration, the introduction of new equipment, services and technology by competitors, changes in marketing, product diversity and quality and the ability to supply equipment and services to customers in a timely, predictable manner.

HRI may be caught in the middle of this if OEMs ever increase the prices of their equipment too much. However, there is always a silver lining. On the plus side, if OEMs ever do that to improve the revenue from their rental business, that will also mean a higher cost of procurement for construction companies who consider owning their own assets but decide not to, and these companies will turn to equipment rental companies. Therefore, I think this threat from OEM is not too serious as it will mean they will be cannibalizing sales from their core business to improve sales from the rental business (note: revenue from Caterpillar's rental segment is so small that it did not break it out but subsumed that under a generic "All other segments" on page 36 of 2021 10K).

Threat From Inflation

Inflation is more than a headline threat. Many businesses have reported lower revenues and profits due to inflationary pressures. HRI is not immune to it but it is able to mitigate those, passing on costs to its customers.

Based on the transcript from Q1 2022 , the CFO was confident that they were able to raise rates every quarter in 2022.

In addition, the industry seems to have gotten price momentum back, and we intend to continue leading the industry on price. Our track record of executing on price in all sorts of operating environment is clear. The momentum and our rate is clear, and we expect to increase rates year-over-year and sequentially each quarter for the remainder of 2022.

For instance, it raised rates by more than 6% in the 3rd quarter which helped offset inflationary pressures. HRI could also manage rising fuel costs through increased revenue recovery and equipment delivery and equipment refueling charges in the quarter. There are clearly several levers for HRI to pull to raise rates to combat inflation.

Lack Of A Moat. Or Does It?

A third threat will be the perceived lack of a moat. It will be hard for HRI to differentiate itself from its largest competitors. HRI is not an OEM with an R&D department introducing new features in their equipment. Everyone else in the same equipment rental business will buy the same machines from OEMs. This is what Morningstar analyst Dawit Woldemariam said in his 21 October 2022 note to investors.

We think Herc will continue to be a top-three player in the equipment rental industry. As one of the industry leaders, the company provides customers better equipment availability and reliability than smaller players. However, many of the equipment brands found in Herc’s product catalog can also be found at other competitors , such as United Rentals, Sunbelt Rentals (owned by Ashtead), and thousands of other rental companies across North America.

From URI's investor presentation slide, it is clear that HRI is a distant third from the top two other competitors, United Rentals and Sunbelt.

URI Investor Presentation Slides Q3 2022

I will agree with the Morningstar analyst to an extent that HRI has no moat over the largest industry leaders. Being third place is not so bad. In my opinion, HRI's scale as the third-placed player in a fragmented industry gives it a moat over its smaller competitors. The highly fragmented nature of this industry offers plenty of opportunities for M&A for HRI, and the growth opportunities that come with that. The growth strategy by merger and acquisition is easier for third-place HRI than it is for the larger competitors. For instance, URI, being the largest player dominating 15% of the market, is also most subjected to the law of large numbers; growth be it via increasing fleet size or through M&A becomes harder at that scale due to increasing costs. That has yet to happen to HRI .

As you can see below, HRI's year-on-year revenue growth exceeds that of market leaders URI and ASHTF, and also against the smaller HEES, and HRI is expected to grow revenue in 2023 at 22.32% (FactSet analysts forecast 21.32% revenue growth and 19.19% adjusted earnings growth in 2023) which is higher than all these peers.

{kind=link}

Seeking Alpha Peer Comparison

Note: Second-placed Sunbelt is a subsidiary of Ashtead Group PLC and is traded as OTC under the ticker ASHTF. It is traded on the London Stock Exchange under the ticker AHT .

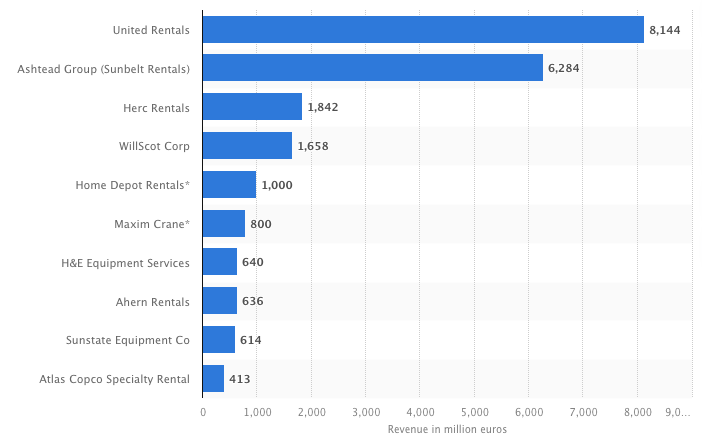

From the Statista graph below, HRI brings in more than three times the combined revenue of the 8th to 10th competitors. With its much larger revenue and market share than the smaller competitors, it is not difficult for HRI to do surgical nip and tuck acquisitions to increase its reach into niche areas and to increase the customer base for it to cross-sell its services.

{kind=link}

Statista 2021 Top 10 Equipment Rental Companies

It is my personal view that HRI is in the sweet spot in terms of size. It is not so large that it can no longer grow fast like URI and ASHTF, yet it is large enough to have an edge over smaller competitors with better pricing and a wider range of services. For instance, HRI provides services such as Pro Contractor and Pro Solutions. Pro Contractor offers clients different types of smaller equipment that the professional contractor might have around in his business—some HVAC equipment, dehumidification equipment, drying equipment, Hilti hammer equipment, Tennant floor sweepers - that may not have been traditionally rented, but are now being rented as more and more companies move to an asset-light model to reduce start-up and operating costs that come with owning and maintaining their own equipment. Pro Solutions helps customers tailor solutions that meet their needs by designing, configuring, and even engineering a solution to their project, and then bringing all the necessary support material in addition to just the equipment to make that project complete. Compared to the smaller H&E Equipment Rentals, HRI already has an edge as HEES does not offer such services.

High Debt

The final risk I see will be its financial situation. Not only does HRI have a substantial amount of debt to pay, but it has also been experiencing several quarters of negative free cash flow.

Let's talk about the debt situation.

{kind=link}

2021 Annual Report

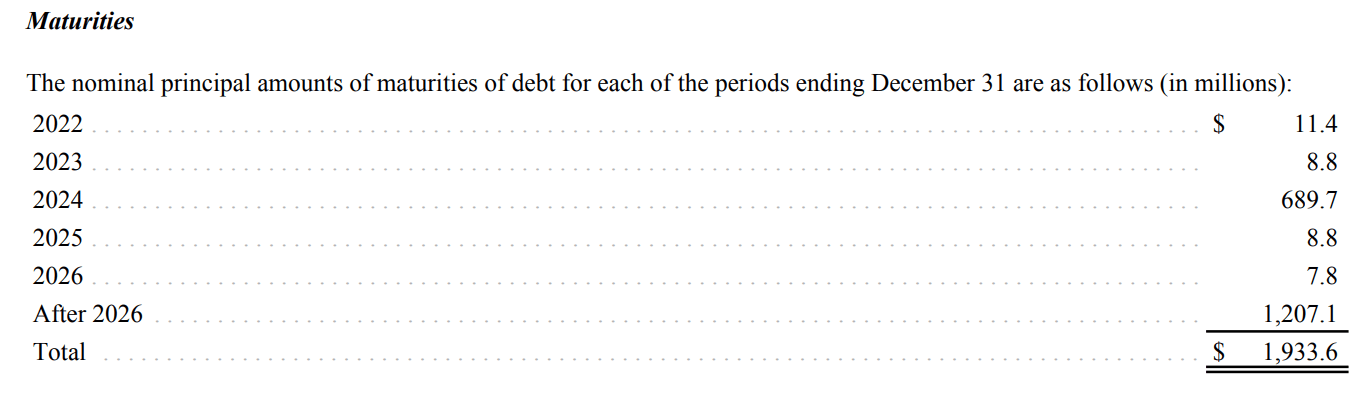

As of December 2021, HRI has $1.93 billion of long-term debt. That long-term debt of $1.93 billion at the end of 2021 has increased to $2.76 billion by Q3 2022.

{kind=link}

Q3 2022 Earnings Presentation Slides

On a positive note, the principal amounts of maturities of debt are very manageable for the years 2022, 2023, 2025, and 2026. Looking back at HRI's ability to generate operating cash flow of $744 million in operating cash flow in 2021, the company is expected to exceed that in 2022 (it already achieved $623 million in operating income for the first nine months of 2022) the $689.7 million of debt to repay in 2024 seems very achievable from an operating cash flow perspective.

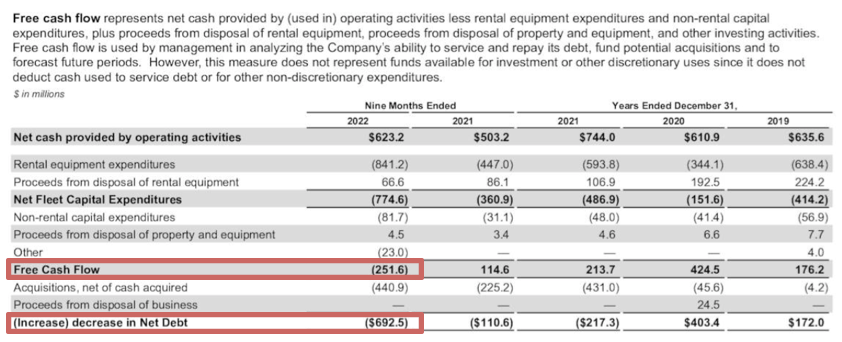

Other than the increasing long-term debt, another cause for concern is the negative free cash flow situation. The company also recorded negative free cash flow for the nine months ending in 2022.

{kind=link}

Q3 2022 Earnings Presentation Slides

Free cash flow is important as it is used by management to analyze the company's ability to service and repay its debt and fund potential acquisitions being in negative free cash flow is a definite worry for me.

Of course, it is not unusual for companies in this industry attempting to grow to be in a negative free cash flow situation. The same was happening to the behemoth in this space, United Rentals. From 1999 to 2014, the company was in a negative free cash flow position for 11 years out of that 16-year period, during which revenue increased 2.5 times from $2234 million in 1999 to $5685 million in 2014. Likewise for second-place Ashtead/Sunbelt. From 2000 to 2016, it was in a negative free cash flow situation for 11 years in that span of 17 years, during which revenue increased 7.8 times from $486 million in 2000 to $3820 in 2016.

In HRI's case, it has increased revenue from $1555 million in 2016 to $2073 million in 2021. There is definitely room for more growth, but that will also mean investors should not be surprised when HRI reports negative free cash flow. Once the company reaches a certain scale like URI and Ashtead/Sunbelt, I believe HRI will be operating at a consistently positive free cash flow level similar to the number one and two in the industry.

Analyst Brian Sponheimer from Gabelli Funds expressed the same concern.

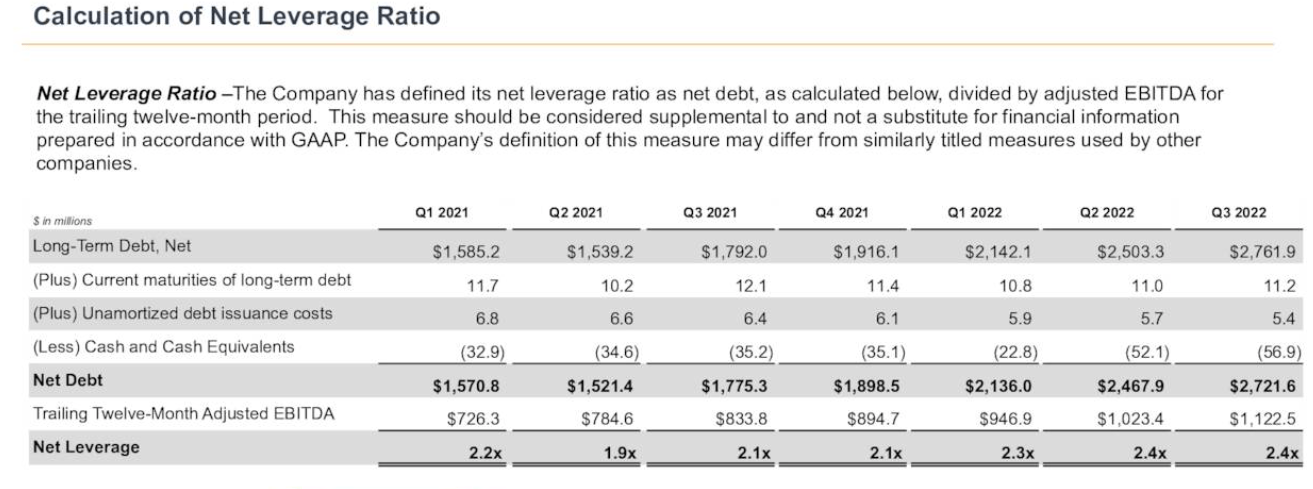

We've seen others in this industry see it two to three times levels being a little too heavy, you're at 2.4 now and buying back stock into what is still going to be a fairly heavy CapEx cycle here.

Management is aware of this and has pledged to maintain leverage between 2x and 3x. CFO Mark Irion commented in response,

...we're comfortable in that 2x to 3x zone. The balance sheet's pretty much bulletproof. There's not a lot of risk to that... We are at peak leverage in the quarter just given the working capital drain in terms of funding the CapEx. So that does decrease slightly going into Q4. So, we will manage it at the lower end of the range, but unlikely to be dropping it below two in the current environment just given our growth trajectory and the amount of money we're investing in the business.

I think investors considering HRI need to factor these aspects of increasing debt, negative free cash flow, and increasing leverage in their risk calculation.

Valuation

There are a few ways we can value HRI.

A comparison of the key valuation metrics like P/E, P/S, and P/B with the largest peers indicates that HRI is cheaper than them.

{kind=link}

Seeking Alpha Peer Comparison

A comparison of the same metrics P/E, P/S, and P/B also shows that HRI is not overpriced by any means.

Stock Rover Research

A comparison with its own 5-year history reveals some mixed results. It shows that HRI is cheaper on a P/E basis but is trading at a higher P/S and P/B than its past 5-year average, even though these values are still much lower than the Index's.

{kind=link}

Morningstar

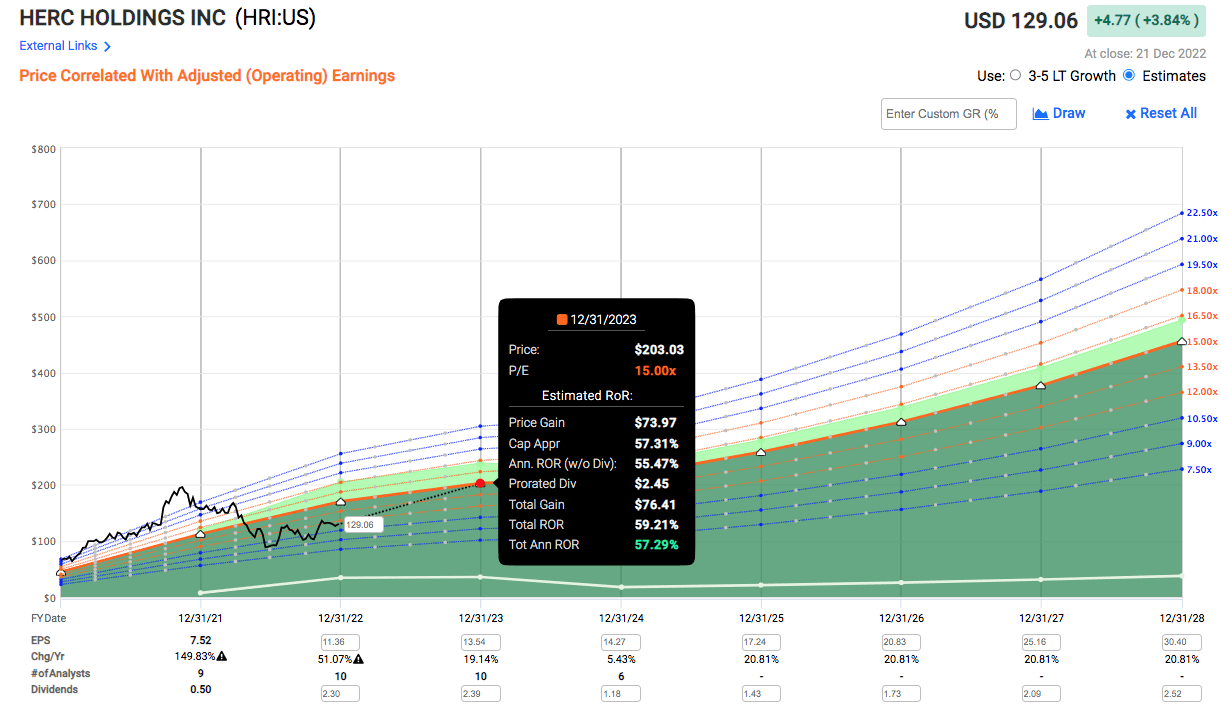

HRI's 5-year average PE is 18.83 and its current PE is 12.88. With the positive forward revenue forecasts, it is not difficult to see a premium multiple attached to it in 2023.

Assuming HRI trades up to a PE of 15, and it can achieve the adjusted operating earnings growth forecast of 19.14% in 2023, HRI offers a potential capital gain of 55.31% in 12 months.

{kind=link}

Fast Graph

Conclusion

Investing in HRI is to invest in a company that is situated in an industry that is bolstered by strong macro tailwinds. It has an inflation resistant business model. It is profitable and is led by an experienced management team that has been delivering good results.

{kind=link}

Trading View

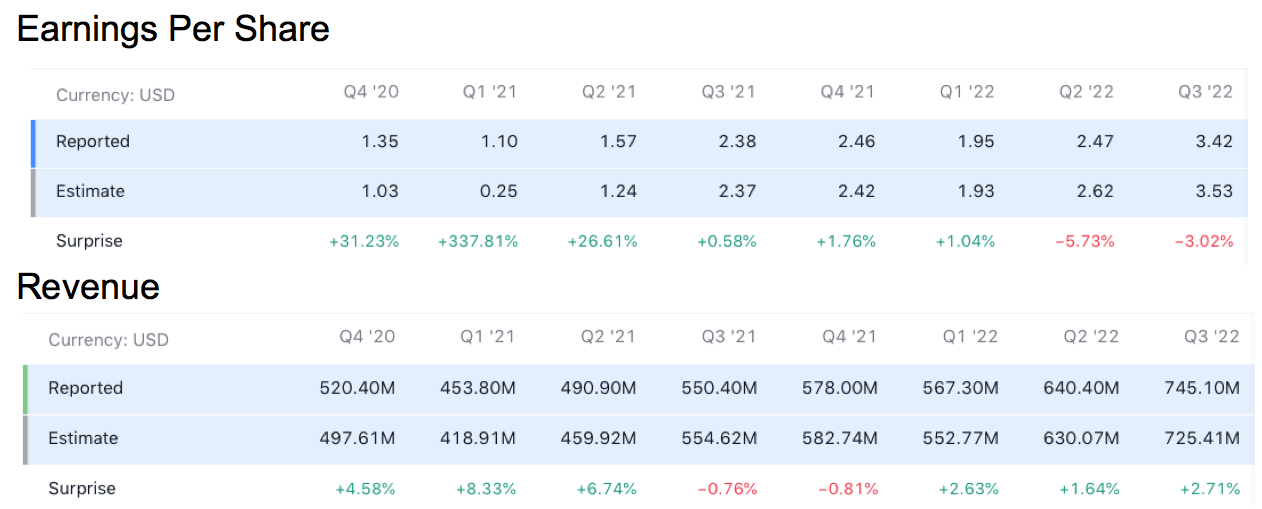

HRI has exceeded EPS and revenue expectations most of the time, and even when it misses it did so only marginally. Besides, analysts forecast that HRI will grow EPS and revenue at a rate that far exceeds the key industry peers, the industry average, as well as the S&P 500.

Stock Rover Research

HRI is at the right size to still grow faster than its larger peers while giving it a moat over its smaller competitors. It has recently started to pay a dividend at 1.85% yield that can attract income-seeking investors. At the current valuation, HRI is a buy for investors looking for higher than industry-average growth.

Editor's Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Herc Holdings Inc.: Own This Infrastructure Play Bolstered By Strong Tailwinds