MONRY - High Fashion Companies: Which One Has The Best Dividend?

2023-11-27 12:00:00 ET

Summary

- High fashion companies have high profit margins, growing revenues, and competitive advantage from successful historical brands.

- In this case, being European companies, it is important to consider the withholding tax.

- At the right price, I would buy them all, especially Hermès.

High fashion is one of the best industries to invest in in my opinion, as the leading companies in it generally have the following characteristics:

- High profit margins and Return on Capital.

- Consistently growing revenues over the long term.

- Competitive advantage dictated by successful historical brands.

Overall, they are solid companies and have performed excellently over the decades. In any case, it is often put on the back burner that these companies used to issue a dividend, which is why in this article I will focus on the latter. In addition, for each company there will be a brief analysis based on the results of the last 10 years.

The companies I will discuss are all European, so one must keep an eye on double taxation.

First company: Kering

The first company is Kering ( PPRUF ), founded in 1963 and headquartered in Paris, France. This company, with due proportion, is the direct competitor of LVMH, as its brands have experienced strong growth especially in the last 5 years. Some of the most prominent include Gucci, Saint Laurent, Bottega Veneta, Balenciaga, Alexander McQueen, DoDo, Qeelin, and Kering Eyewear.

{kind=link}

Over the past 10 years, Kering has experienced strong growth in several ways:

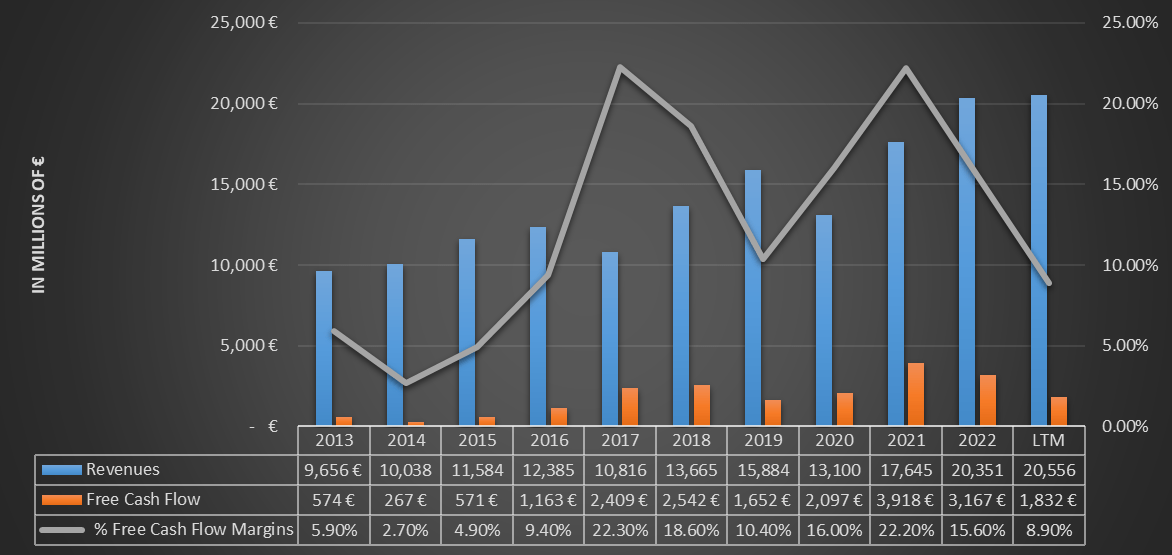

- Revenues have increased from €9.65 billion in 2013 to the current €20.55 billion, a 10-year CAGR of 7.84%.

- Free cash flow increased from €574 million to the current €1.83 billion, a 10-year CAGR of 12.30%. In any case, the LTM result was affected by a CapEx of €2.63 billion, far higher than the historical average. This figure was affected by the acquisition of 30% of the Valentino brand for €1.70 billion. If we considered the 2013-2022 CAGR, it would be 20.89%.

- The free cash flow margin has improved over the long term, and from being in the single digits today it has steadily exceeded double digits: the LTM result should be considered an exception due to the large acquisition.

{kind=link}

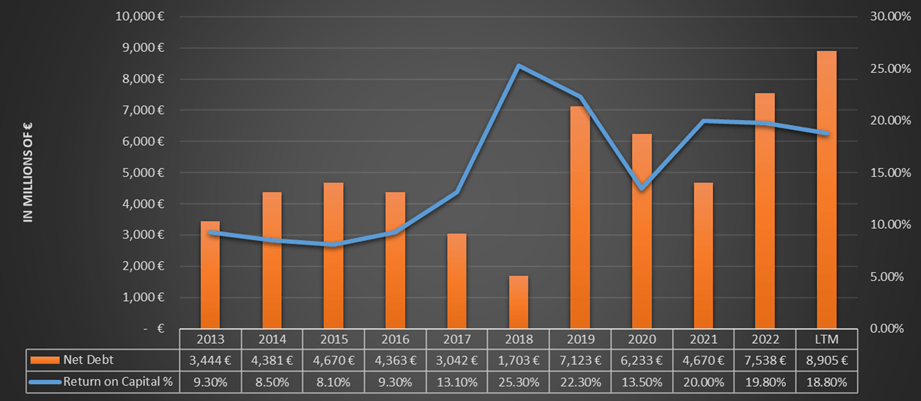

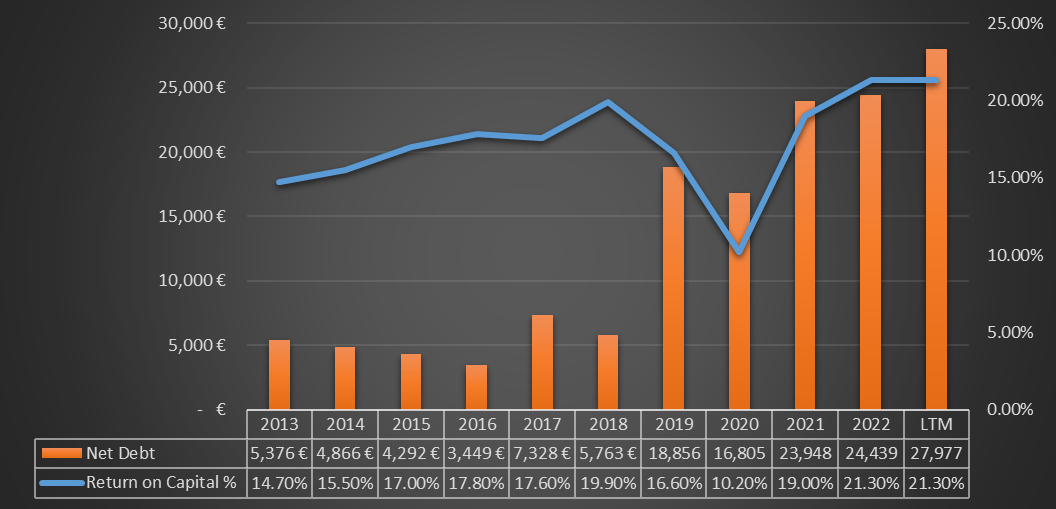

In addition, return on capital has also seen a strong improvement, and net debt, although increasing, is fully sustainable given the strong growth in free cash flow.

Overall, Kering's results have been very positive and much credit should be given to Gucci's creative director Alessandro Michele. Unfortunately for the company, he decided to resign last year and this was a major blow. His place was taken by former Valentino creative director Sabato De Sarno.

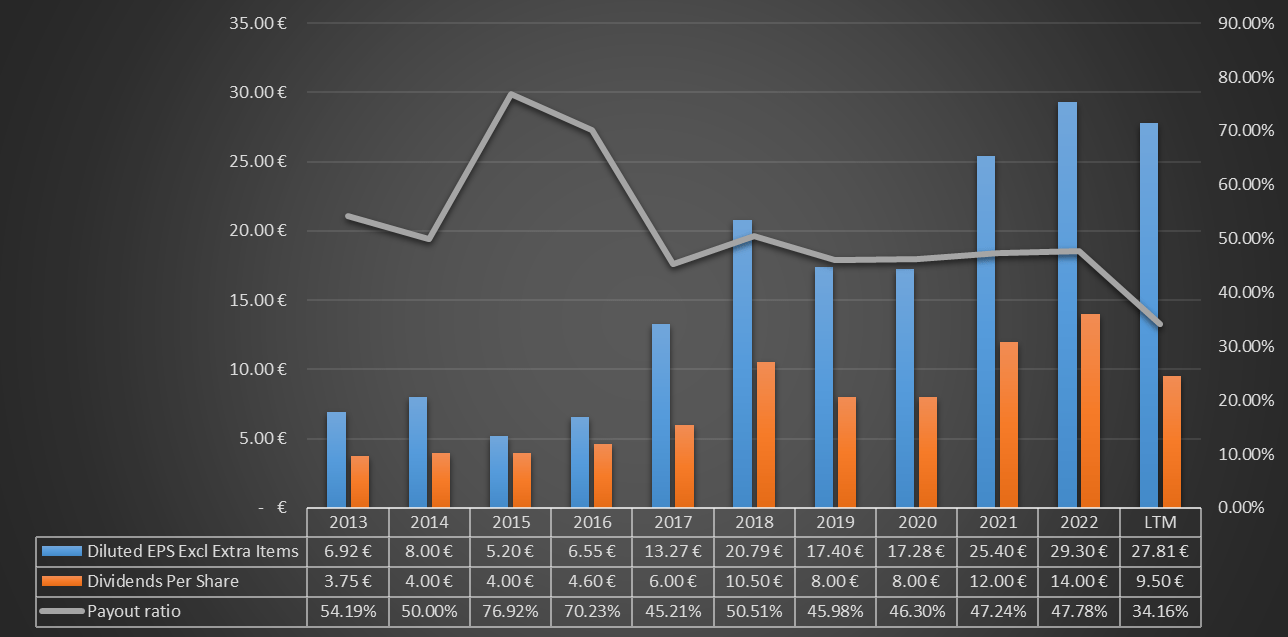

Finally, let's take a look at the dividend. Currently, the dividend yield is 3.40%.

{kind=link}

EPS grew over the long term and increased more than dividend per share: the latter, recorded a 10-year CAGR of 9.74%. As EPS has grown more, the payout ratio has gradually declined to only 34.16%. So, the dividend is widely sustainable.

If we considered the same CAGR of dividend per share over the next 10 years, buying Kering today, the dividend yield on cost in 2033 would be 5.94%. In short, a good result for a company that is likely to dominate for decades to come thanks to its brands. Over the past 10 years, the price return has been 163% despite the stock being 50% far from its all-time high.

Second company: LVMH Moët Hennessy - Louis Vuitton

The second company is the world's most famous in its industry, LVMH ( LVMHF ). The successful brands that this company presents are innumerable and not only cover high fashion, but the luxury industry in general. I will list just a few because there are really too many: Dom Pérignon, Moët & Chandon, Hennessy, Belvedere, Louis Vuitton, FENDI, Celine, Christian Dior, Emilio Pucci, Givenchy, Kenzo, Marc Jacobs, Tiffany & Co, Bulgari e Royal Van Lent.

{kind=link}

The income results over the past 10 years have undoubtedly been positive:

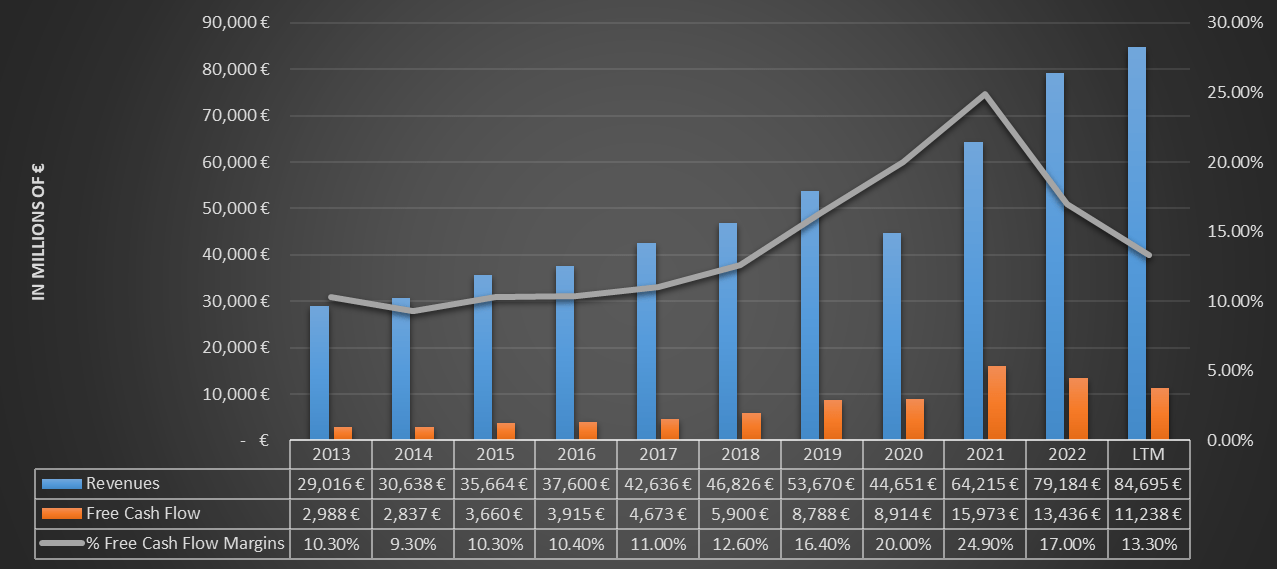

- The 10-year revenue CAGR was 11.30%, an important achievement since LVMH was already a huge group in 2013.

- Free cash flow suffered a setback in the last year due to an increase in inventory. After strong demand in the second half of 2020 and 2021, there has been a decline from late 2022 to the present. In fact, LTM inventory is up by €1.09 billion from 2022 and by as much as €3.69 billion from 2021. Regardless, it represents a momentary slowdown and the free cash flow margin still remains above double digits. The 10-year CAGR of free cash flow was 14.16%.

{kind=link}

Return on capital is stable above 20% and net debt remains sustainable despite the sharp increase. Relating it to free cash flow margin, in 2013 it was 1.79 times, today 2.48 times. There has been a deterioration, but nothing of concern.

Finally, we come to the dividend. The current dividend yield is 1.70%, which is low but has good growth prospects.

{kind=link}

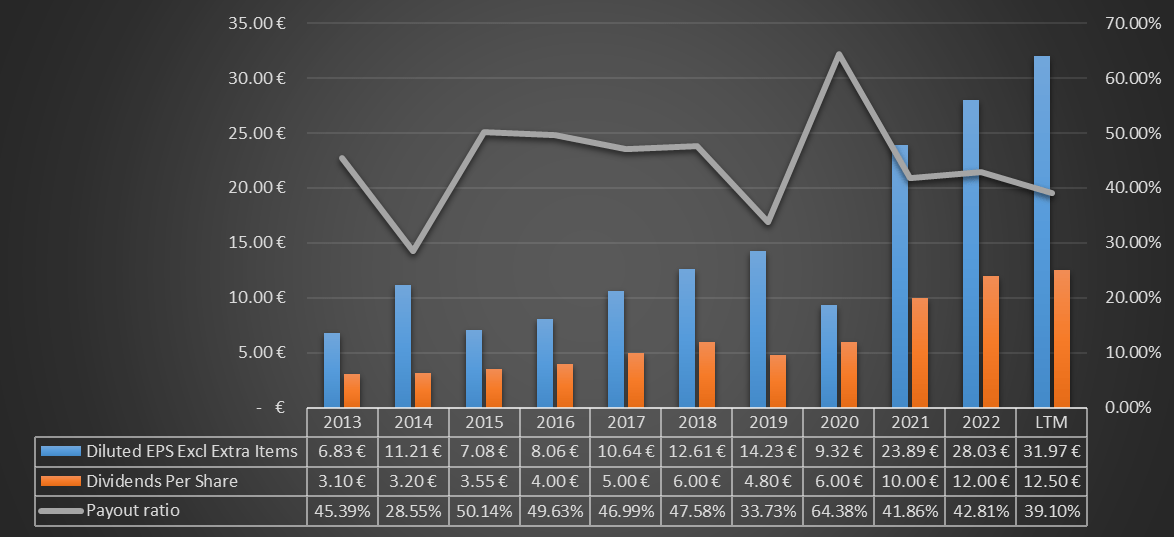

Over the past 10 years, EPS has increased at a CAGR of 16.68%, and dividend per share at a CAGR of 14.96%: two excellent achievements. The payout ratio today is only 39.10%, which denotes a sustainable dividend. Assuming the same growth rate in the future, buying LVMH today, the dividend yield on cost will be 7.08% in 2033.

At this point we can already start making the first comparisons, in fact LVMH's dividend has proven more interesting than Kering's over the past 10 years. In addition to growing faster, it has also exhibited some stability in issuance, showing slight weakness only during the pandemic. Moreover, there has also been a better performance in terms of price return: +438.20% over the past 10 years.

Third company: Hermès International

The third company I want to talk about is Hermès ( HESAY ).

In my opinion, this company is unrivaled in the fashion world and is the epitome of luxury. Its distinguishing feature is the exclusivity of its brand: while almost all of us can buy a Louis Vuitton or Gucci bag by saving for months, few can buy a Birkin .

While all companies try to open as many stores as possible, Hermès instead operates against the trend in order to preserve the brand's exclusivity: in 2011 there were 328 stores worldwide ; today there are only 300. At first glance you might think it is a silly choice to decrease stores, but the revenues say otherwise: in 2011 there were €3.75 billion, today €12.82 billion.

In this case, the quote from former CEO Patrick Thomas fits like a glove:

The luxury industry is built on a paradox: the more desirable the brand becomes, the more it sells but the more it sells, the less desirable it becomes.

{kind=link}

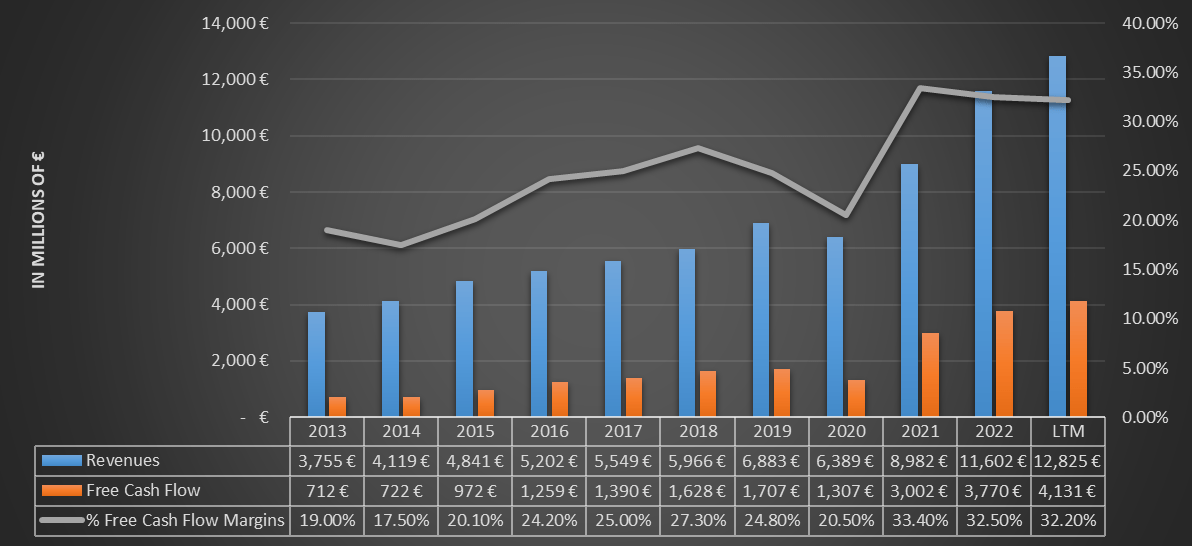

The results achieved over the past 10 years have been sensational:

- The 10-year revenue CAGR was 13.06%, more than Kering and LVMH.

- The 10-year free cash flow CAGR was 19.22%, more than Kering and LVMH.

- The free cash flow margin is well and steadily above 30%, an achievement that no one in this industry can match: such a margin we can expect from a big-tech company. But there is more.

{kind=link}

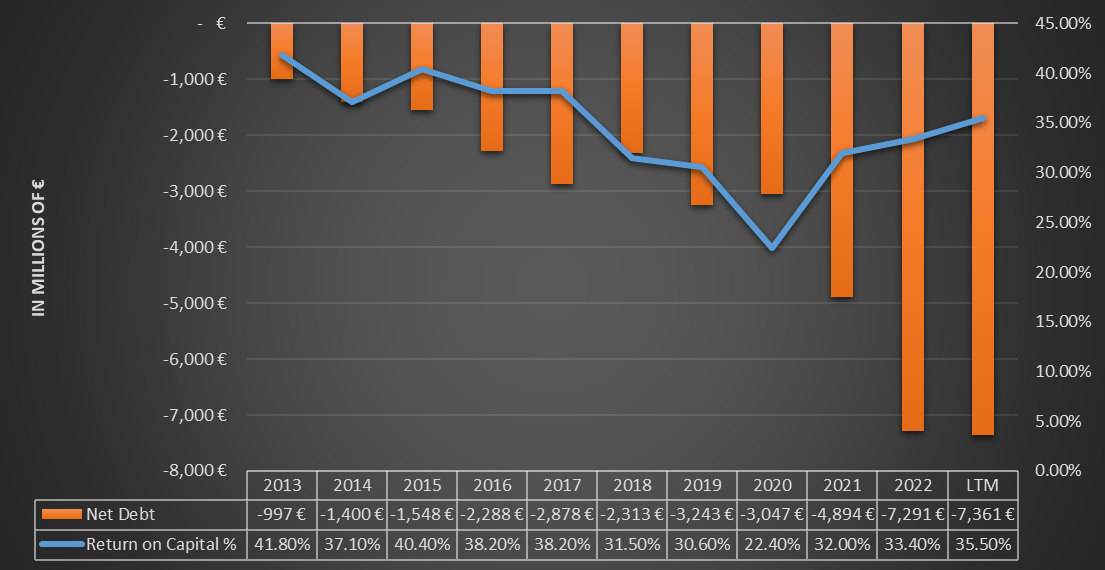

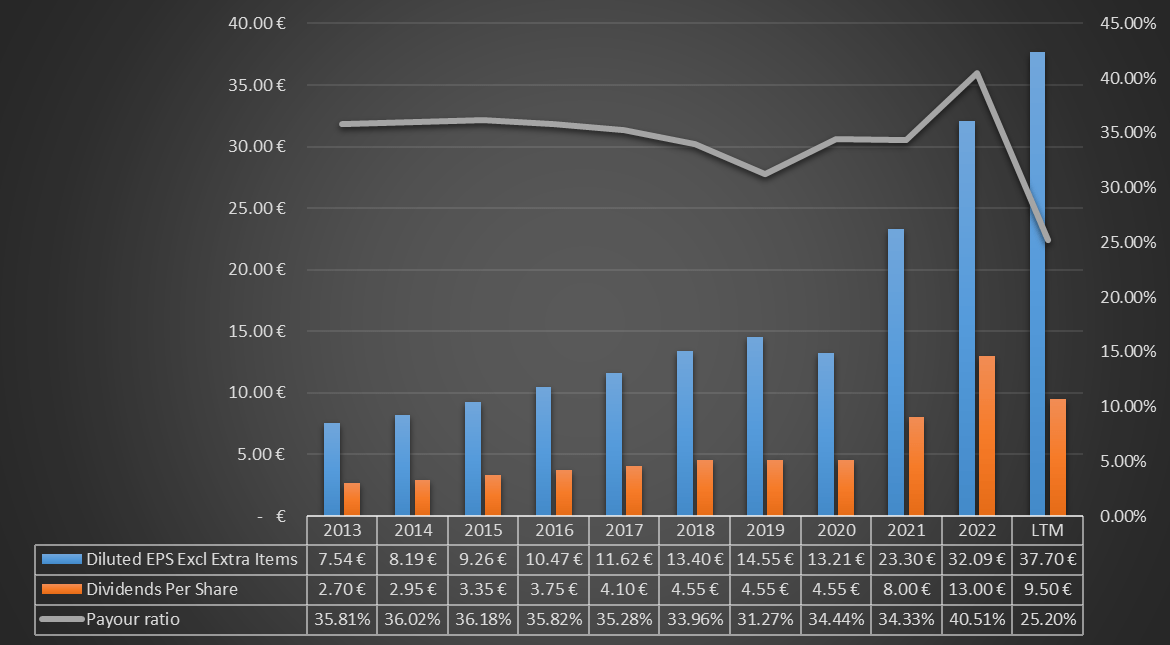

The return on capital is excellent and Hermès has no debt, or rather, it has negative net debt that is growing more and more. The company is able to generate so much cash that it could pay off all its debt in one day if it wanted to. In short, we are talking about an outstanding company overall. The only downside is that given its low dividend it may not appeal to many investors.

The dividend yield is only 0.70% because of the price per share near the all-time high. Also, since the return on capital is 35.50%, management has more incentive to reinvest capital within the business rather than issuing it externally.

{kind=link}

However, while low, the dividend is not to be overlooked. Its sustainability is beyond question since the payout ratio is only 25.20% and the 10-year CAGR was quite high, 13.40%. Buying Hermès today, assuming the same growth in the future, would imply a dividend yield on cost of 1.70% in 2033. A rather disappointing result and one that points to management's greater inclination toward capital gain rather than dividend yield. In fact, the price per share has risen 647.50% over the past 10 years.

There is no question about the company, but as far as the dividend is concerned, it is more appropriate to buy Hermès at a lower price than it is now. For example, in June 2022 it was trading at €1000 per share. Buying it at that price, with the same assumptions as before, the dividend yield on cost rises to 3.34%.

Fourth company: Moncler

After three French companies, here is an Italian one: Moncler ( MONRF ).

Actually, Moncler was originally French having been created in 1952 in Monestier-de-Clermont; however, in 2003, almost bankrupt, it was bought by Remo Ruffini and moved to Milan. Since that acquisition, the Moncler brand has made a comeback thanks to his work and he is still the CEO after 20 years.

{kind=link}

Except for 2020, Moncler's revenues increased year after year and recorded a 10-year CAGR of 17.11%, higher even than that of Hermès. Obviously, this figure was aided by Moncler's small size, an ant in front of the giant Hermès. However, this should not downplay the performance achieved under Remo Ruffini's leadership.

Here again, the increase in inventory has reduced free cash flow, but the long-term growth is still evident. Moreover, the free cash flow margin remains steadily above 20%, better than Kering and LVMH.

{kind=link}

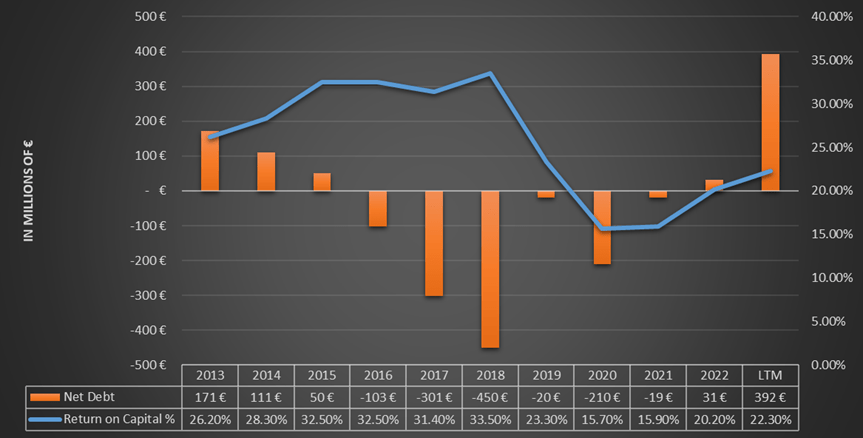

Regarding net debt, there has been a major increase in recent months as a result of various investments in the supply chain to increase production. Efforts are being made to improve the performance of the only two brands on hand, Moncler and Stone Island . Anyway, debt remains under control and the return on capital is stably above 20%.

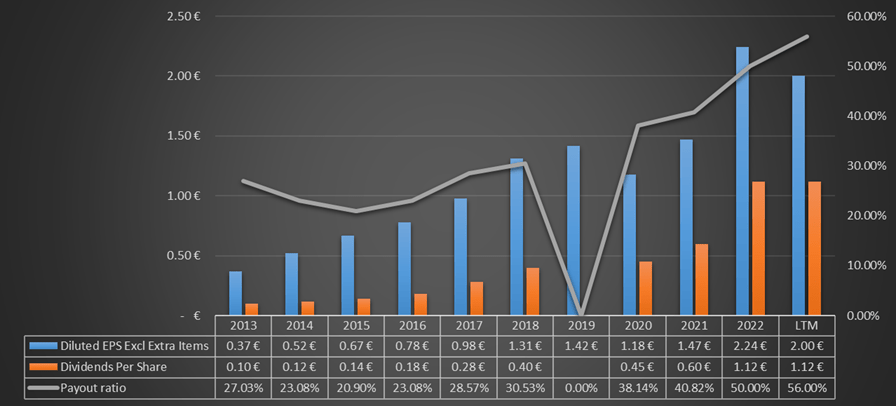

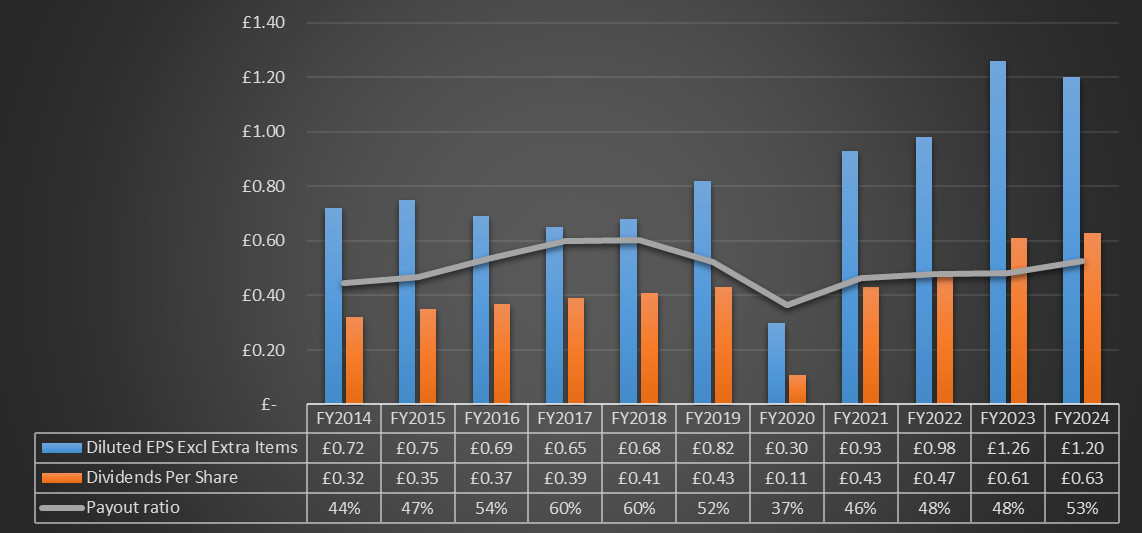

As for the dividend, the current dividend yield is 2.10%.

{kind=link}

Unlike previous companies, the payout ratio has increased over the past and reached 56%. The dividend remains largely sustainable, but it is interesting to note that EPS grew more slowly than dividend per share: the 10-year CAGR of EPS was 18.38% while that of the dividend an incredible 27.32%. There was no issuance in 2019.

Assuming the same growth in the future, buying Moncler today implies a dividend yield on cost of 24.12% in 2033. Growth will probably be lower since Moncler was a significantly smaller company in 2013 than it is today, but I would also settle for a dividend on cost of 10-12%. Since December 2013, Moncler's price per share has increased by 251.20%.

Fifth company: Burberry

The latest company comes from the United Kingdom and has more than 150 years of history, Burberry ( BURBY ). The group operates worldwide and also licenses third parties to manufacture and distribute products using the Burberry brands. Of all the companies seen so far, this is probably the most attractive to U.S. investors since the dividend is not subject to withholding tax . In the case of France and Italy it is 12.80% and 26% for individuals, respectively.

{kind=link}

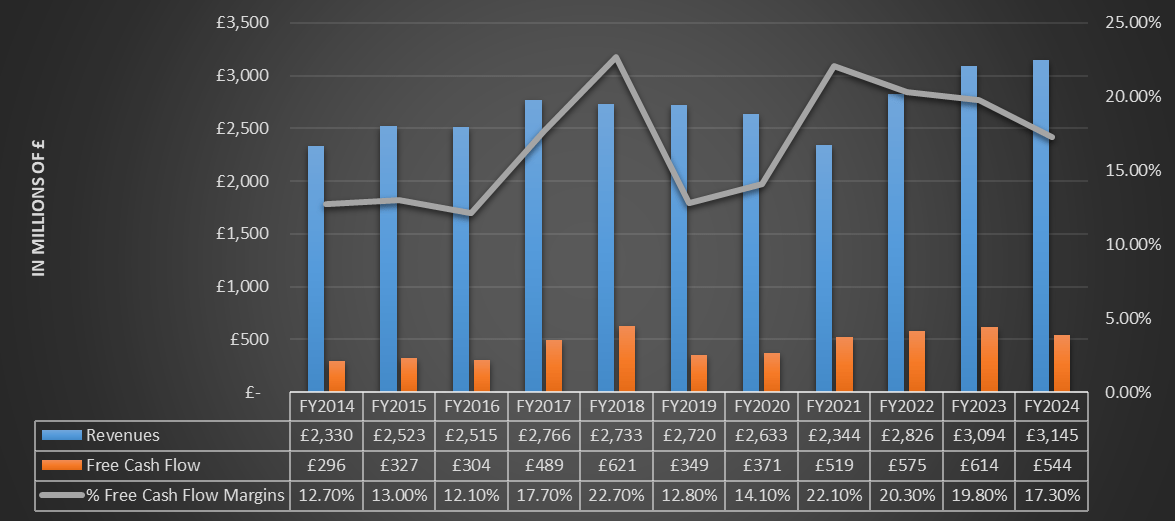

In terms of growth, Burberry is the company that is struggling the most: the 10-year CAGR of revenues was 3.04% and the CAGR of free cash flow was 6.27%. This is not exciting growth, but margins at least improved from 10 years ago. Be that as it may, at least it has shown great continuity in revenues.

{kind=link}

After having negative net debt for years today the situation has changed. Relative to free cash flow, net debt is only 1.63x larger, thus widely sustainable. Finally, the return on capital for Burberry is also stably above 20%.

Let us now look at the dividend. Burberry is currently the company with the highest dividend yield, 4%.

{kind=link}

EPS largely covers the dividend per share, however, its growth is far lower than that of other companies: the 10-year CAGR of dividends was 7%. Assuming the same growth in the future, buying Burberry now the dividend yield on cost would be 8.06% in 2033. In terms of dividend constancy, Burberry is probably the one that pays the most attention to shareholder remuneration: only during the pandemic was it preferred to cut it.

In practice, Burberry is the best option for those with a short-term view, but in the long term the low growth rate leads to a dividend yield on cost that is not that high. It is probably the most struggling company among the 5 and is 42% far from its all-time high.

Conclusion

All the companies shown in this article are in my opinion interesting and at the right price I would buy them. However, it is clear that of all of them, the one I think is the best is Hermès, both because of its competitive advantage and its earnings results. From a dividend perspective, among the 5 I would probably choose Moncler since it is the one that is growing the fastest. Also, being Italian, I would not pay any withholding tax and this is a strong advantage.

On this last aspect I take the opportunity to say that an investor's preferences can vary a lot depending on the country they are in: a French person probably prefers Kering, LVMH or Hermès, an Italian Moncler and everyone else Burberry. In short, in terms of dividend, there is no investment that will suit everyone.

Finally, I would like to point out one last aspect that I think is very interesting regarding the share ownership of the 5 companies. Burberry is the only one that has an ownership composed mainly of institutional investors, and this would explain in my view why it is so careful in remunerating shareholders through dividend. As we have seen, its consistency in issuing the dividend is better than the other companies, almost as if it were a U.S. company. The only one that comes close is Moncler, and in fact it is the second in terms of shareholding by institutional investors. French companies are dominated by noble families whose priority is company growth rather than worrying about shareholder remuneration. After all, the majority of shareholders are their own.

- Hermès International; Hermès Family owns 66.70% of the outstanding shares.

- Kering; Pinault Family owns 42.23% of the outstanding shares.

- LVMH; Arnault Family owns 48.30% of the outstanding shares.

In other words, if I were to decree the winners purely on the dividend basis, Moncler and Burberry are probably the better ones: the former for its growth rates, the latter for the consistency of its dividend. If we were to consider total return, however, so dividends plus capital gains, the French companies have a leg up. Their dividend may be fluctuating at certain times, but the century-long history of their brands is a competitive advantage that only a few have. Even if there were a new company making a handbag of the same quality as Hermès', you would still buy a Birkin .

For further details see:

High Fashion Companies: Which One Has The Best Dividend?