WELL - Higher For Longer

2023-08-20 09:00:00 ET

Summary

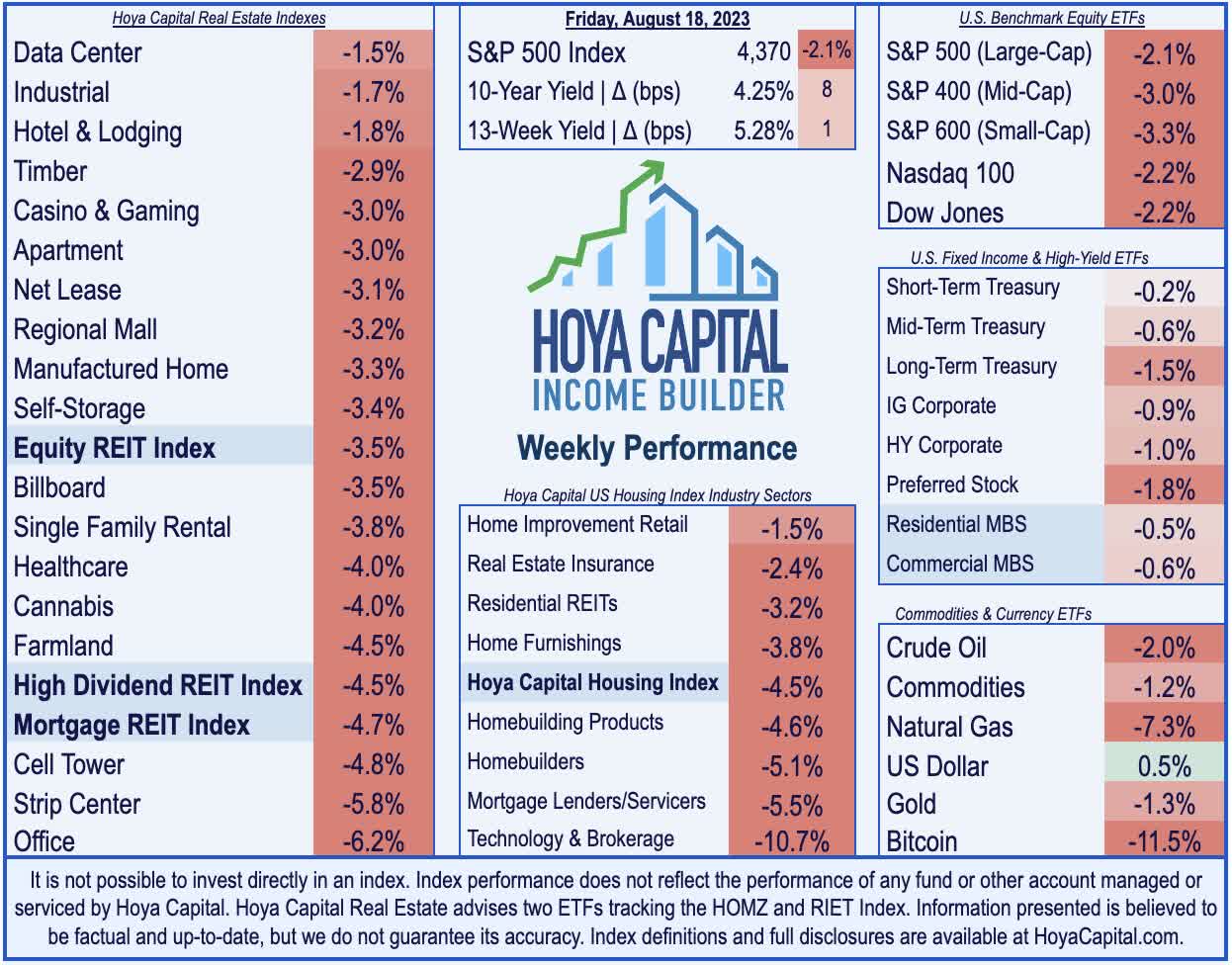

- U.S. equity markets slumped for a third-straight week on concern over the implications of a "higher-for-longer" interest rate environment as resilient economic data provided fresh support for hawkish Fed posturing.

- Closing below its 50-day moving average for the first-time in three months, the S&P 500 declined 2.1%, while the tech-heavy Nasdaq dipped 2.2% to extend its monthly slump to 7%.

- Higher rates continued to pressure yield-sensitive segments, in particular, as real estate equities and homebuilders have been among the hardest-hit sectors so this month following strong performance earlier this summer.

- A key look into the health and sentiment of the U.S. consumer, retail sales data this week showed surprising strength in July, contrasting with other recent indicators and corporate commentary hinting at a late-summer slowdown in consumer and business economic activity.

- Embattled hospital owner Medical Properties Trust - which has been in the cross-hairs of short-sellers since mid-2022 - dipped more than 14% this week after the Wall Street Journal reported that a California state regulator put on hold a deal to save one of its largest tenants.

Real Estate Weekly Outlook

U.S. equity markets slumped for a third-straight week on concern over the implications of a "higher for longer" interest rate environment as resilient economic data provided fresh support for hawkish Fed posturing. Optimism over an economic "soft landing" has faded in recent weeks as a rebound in global energy prices and signs of continued resilience in consumer spending has fueled a modest reacceleration in real-time inflationary pressures, and prompted a handful of the more hawkish Fed officials to again vocalize their belief that further tightening is necessary to quell inflation.

{kind=link}

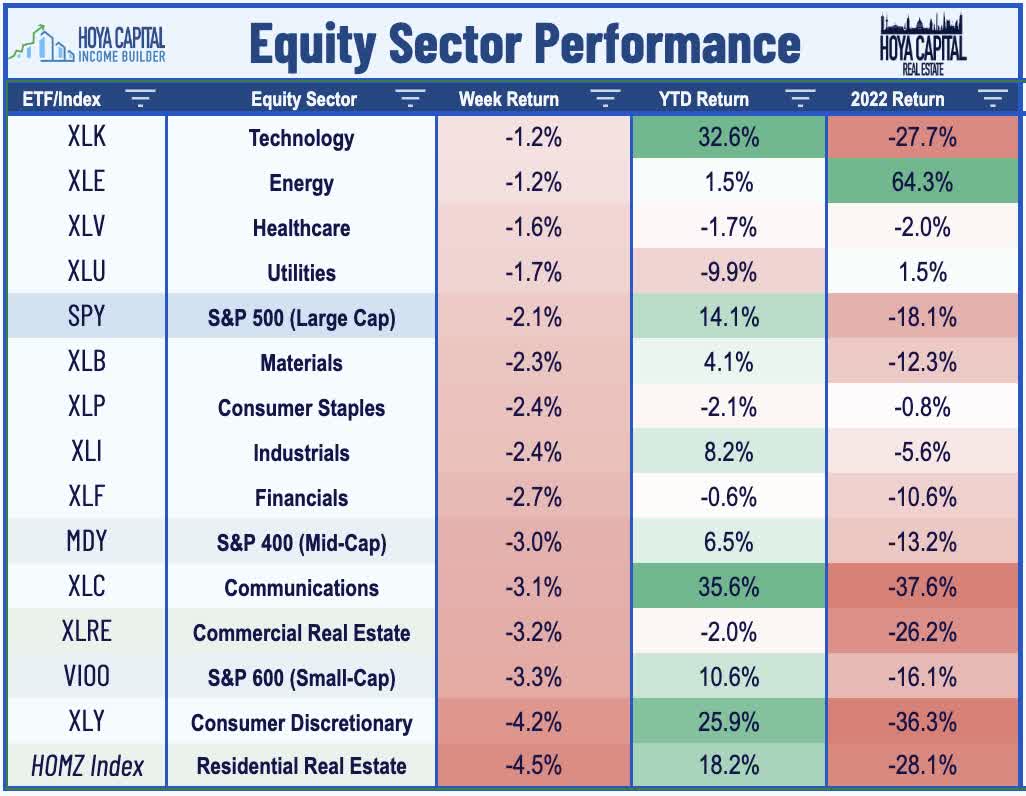

Closing below its 50-day moving average for the first time in three months, the S&P 500 ( SPY ) declined 2.1% this week, while the tech-heavy Nasdaq 100 ( QQQ ) dipped 2.2% to extend its three-week skid to over 7%. Selling pressure was even stiffer for smaller companies, with the Mid-Cap 400 ( MDY ) and Small-Cap 600 ( VIOO ) each sliding by more than 3%. Higher rates continued to pressure yield-sensitive segments, in particular, as real estate equities and homebuilders have been among the hardest-hit sectors so far this month following strong performance earlier this summer. The Equity REIT Index ( VNQ ) dipped 3.5% on the week, with all 18 property sectors in negative territory, while the Mortgage REIT Index ( REM ) slipped 4.7%. Homebuilders , meanwhile, dipped over 5% as 30-Year Mortgage rates climbed to fresh fifteen year-highs.

{kind=link}

Choppiness has returned to markets in recent weeks, as the Cboe Volatility Index climbed to the highest level since May. Resilient economic data - combined with recent supply/demand concerns in primary Treasury markets -lifted the benchmark 10-Year Treasury Yield to the highest-levels since 2007 this week - briefly breaching though 4.30% before settling at 4.25% - matching the 15-year closing highs set last October. The policy-sensitive 2-Year Yield has remained steadier through the recent choppiness, however, rising by four basis point this week to close at 4.93%. WTI Crude Oil prices - perhaps the most critical swing input for the near-term inflation outlook - declined 2.0% this week while Natural Gas futures plunged more than 7%. Importantly, crude oil production in the United States rose to 12.7 million bpd last week, finally marking a full recovery to pre-pandemic 2019 levels. All eleven GICS equity sectors finished lower on the week with Real Estate (XLRE) and Consumer Discretionary ( XLY ) stocks lagging on the downside.

{kind=link}

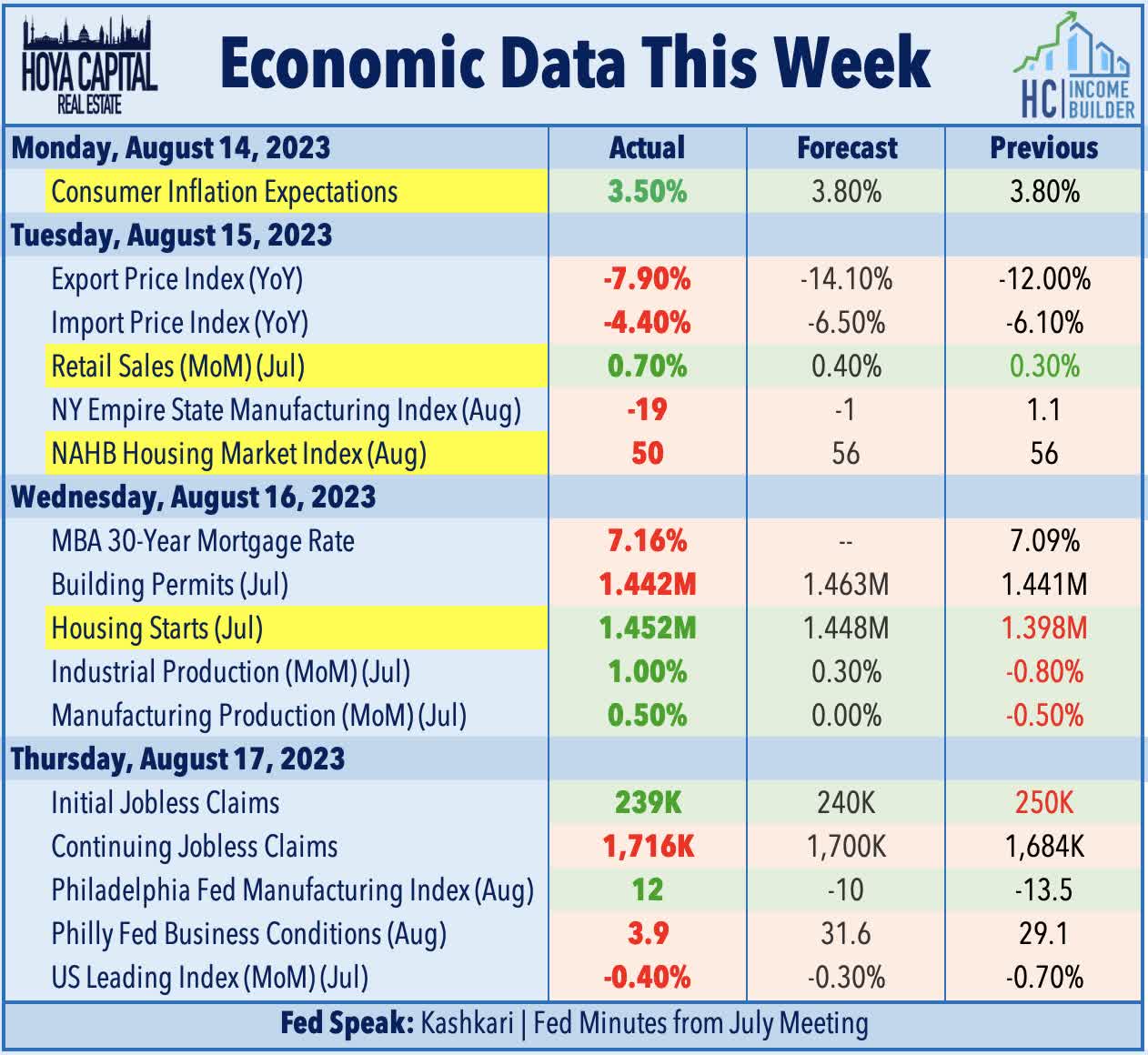

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

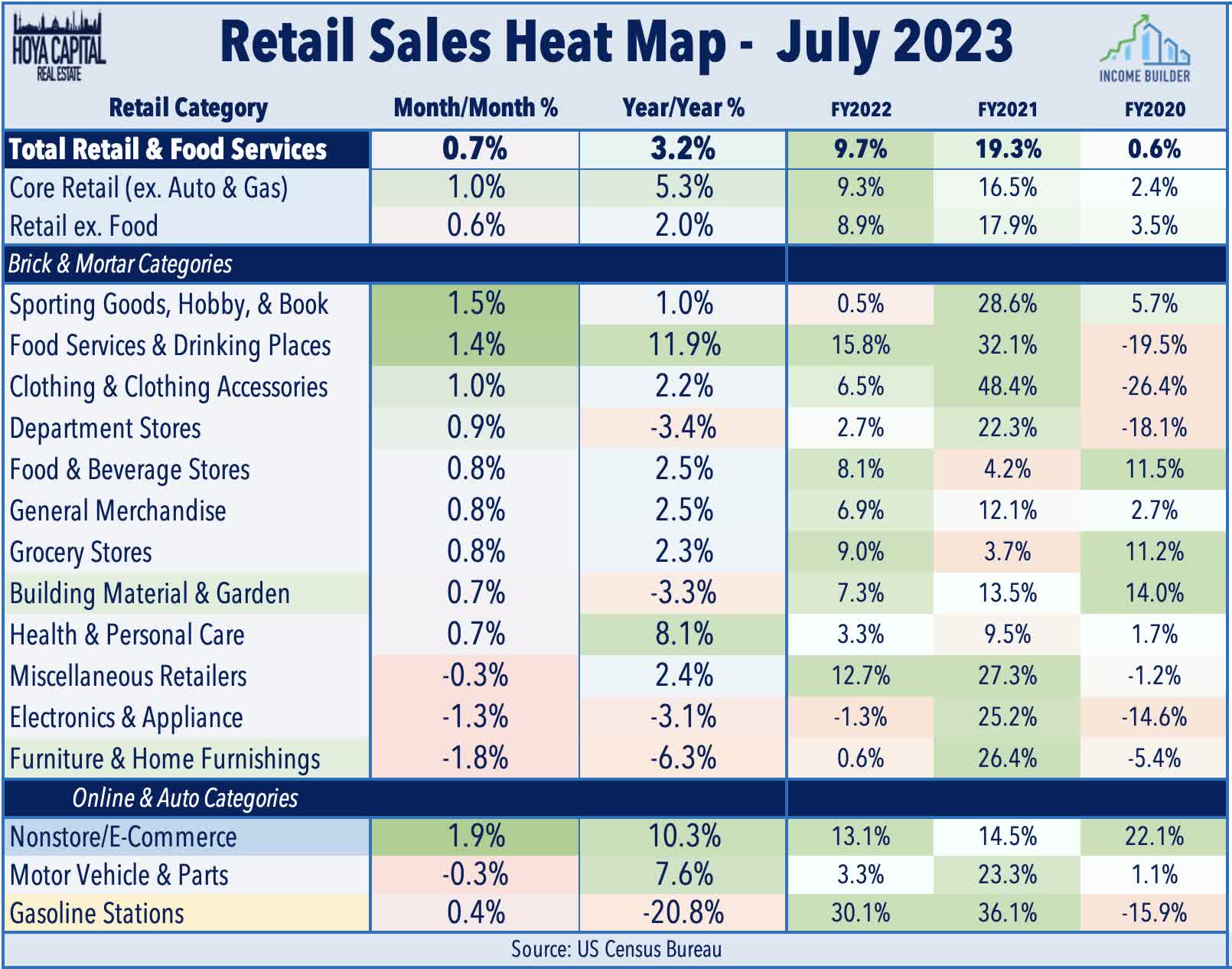

A key look into the health and sentiment of the U.S. consumer, retail sales data this week showed surprising strength in July, contrasting with other recent indicators and corporate commentary hinting at a late-summer slowdown in consumer and business economic activity. Total retail sales increased 0.7% in July compared to the prior month and 3.2% from last year - well above the 0.4% forecasted increase - while the prior two months were also revised higher. Spending strength was relatively broad-based, led by e-commerce, restaurants, department stores, and sporting goods retailers, while several housing-related categories - furniture and appliances - were generally among the laggards amid a sluggish home sales market. Excluding gas and auto, retail sales appeared even stronger with a 1.0% monthly increase, which was 5.3% above last year. As these figures aren’t adjusted for inflation, "real" retail spending is roughly flat year-over-year when adjusted with headline CPI.

{kind=link}

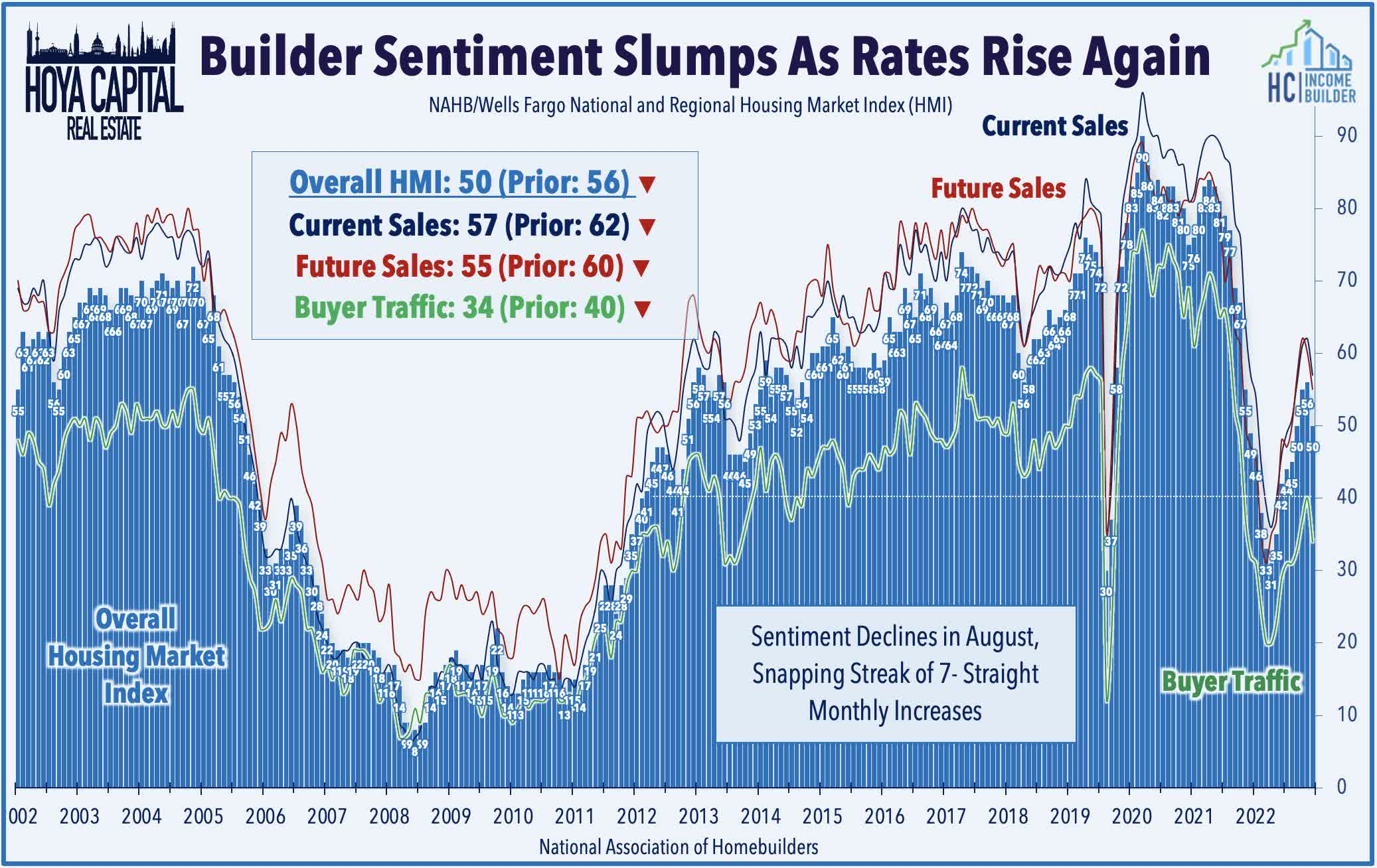

Housing market data this week was mixed however, as the NAHB Homebuilder Sentiment - a leading indicator of housing market activity - fell rather sharply in August, snapping a streak of seven-straight monthly increases. The dip in sentiment was attributed to the recent leg higher in mortgage rates, which are now solidly over 7% - hitting 7.37% by the end of the week according to Mortgage News Daily. The composite Homebuilder Sentiment Index fell to 50 in August from 56 in July, with all three sub-components posting declines of at least 4 points. Housing Starts data, meanwhile, was modestly stronger-than-expected, reflecting some of optimism from earlier this summer, but Building Permits data was sluggish, posting a year-over-year decline of 13% - the twelfth straight month of negative year-over-year growth. Despite the disappointing data, homebuilders were buoyed by the disclosure of new investments by Warren Buffet’s Berkshire Hathaway in a trio of the largest U.S. homebuilders - Lennar (LEN), D.R. Horton (DHI) , and NVR (NVR).

{kind=link}

Equity REIT Week In Review

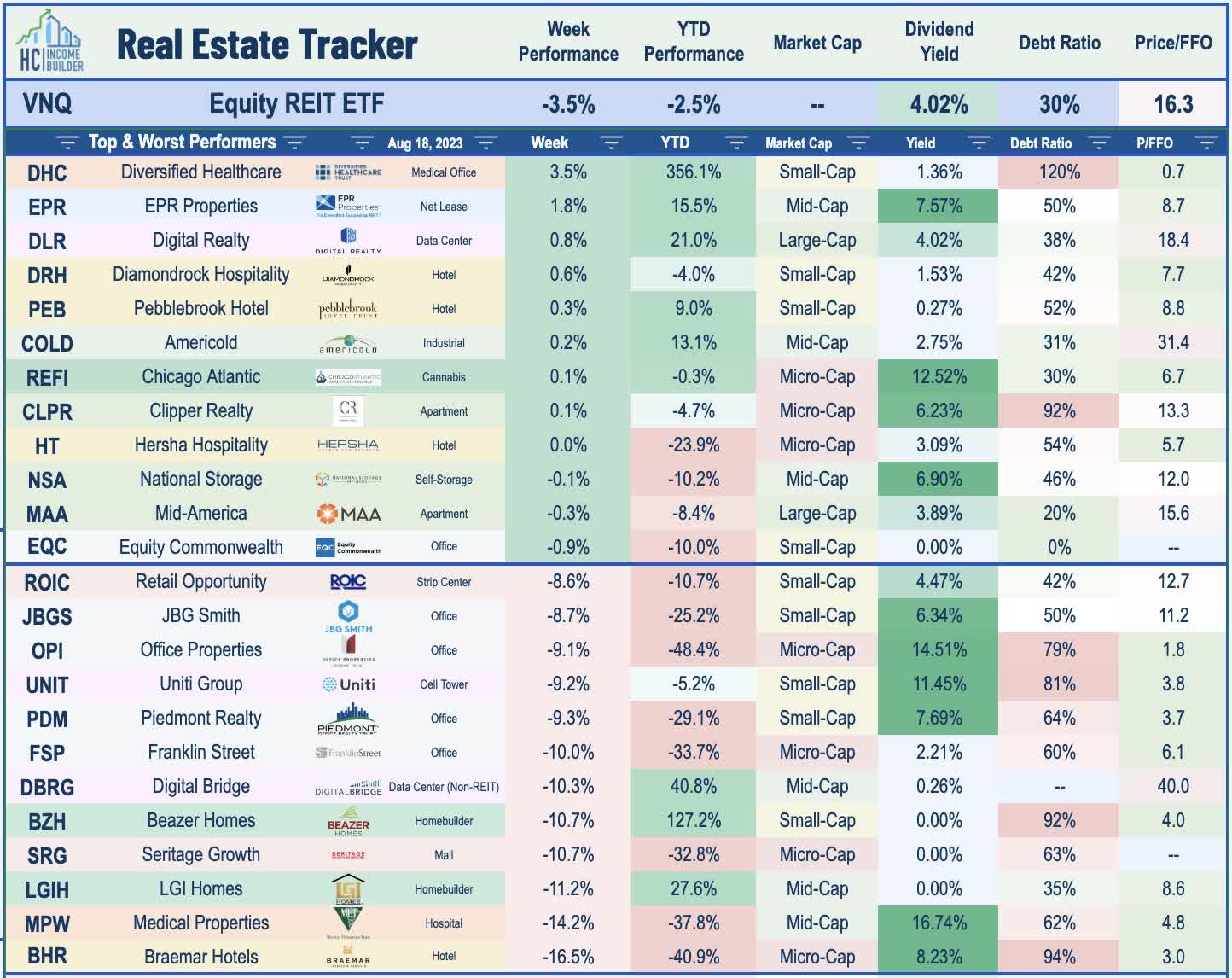

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Healthcare : Embattled hospital owner Medical Properties Trust ( MPW ) - which has been in the cross-hairs of short-sellers since mid-2022 - dipped more than 14% this week after the Wall Street Journal reported that a California state regulator put on hold a deal to save one of its largest tenants - Prospect Medical - which had previously stopped paying rent to MPW. The WSJ had previously published critical stories regarding MPW and, more broadly, the involvement of private capital in hospital system. Prospect is one of several healthcare operator tenants that have been slammed by industry-wide headwinds in recent quarters as government relief funds waned while profit margins were hit by soaring labor expenses. The timing and disclosure of the hold were the key focus of this latest issue, as the hold order was filed on July 20th, but MPW did not disclose the order in its earnings report or its 10-Q filing on August 8th. After the report, MPW fired back with a press release in which the firm called the regulatory hold "immaterial" and was a "standard, expected, and non-controversial part of the approval process" and it continues to expect the transaction to ultimately reach approval. MPW announced last quarter that, as part of the deal, it would receive equity in Prospect in lieu of cash payment for $573 million of rent. The WSJ report came just hours after MPW disclosed positive tenant-related news, announcing that it sold $105 million of its interest in Steward Health's credit facility, another troubled major tenant that MPW has required financial support from MPW.

{kind=link}

Healthcare : Sticking in the healthcare space, lab space operator Alexandria Real Estate ( ARE ) declined about 6% this week after it disclosed in a filing that its President and Chief Financial Officer, Dean Shigenaga, submitted his resignation from all of his positions with the Company and its subsidiaries for "important personal family health reasons," effective September 15, 2023. It is expected that he will continue to assist the Company with transitional matters and ongoing as a strategic consultant. The Board elected Marc Binda as Chief Financial Officer and Treasurer, effective September 15, who has served as Executive Vice President – Finance and Treasurer since June 2019. ARE has stumbled more than 20% this year amid a weakening in lab space fundamentals from a combination of sluggish demand and elevated supply growth. CBRE reported last month that the vacancy rates in the top 13 markets jumped to 9.0% in Q2 - up from 5.0% a year ago - resulting from 3.4 million square feet of new lab space being delivered in Q2, representing a roughly 2% expansion in total industry-wide square footage.

{kind=link}

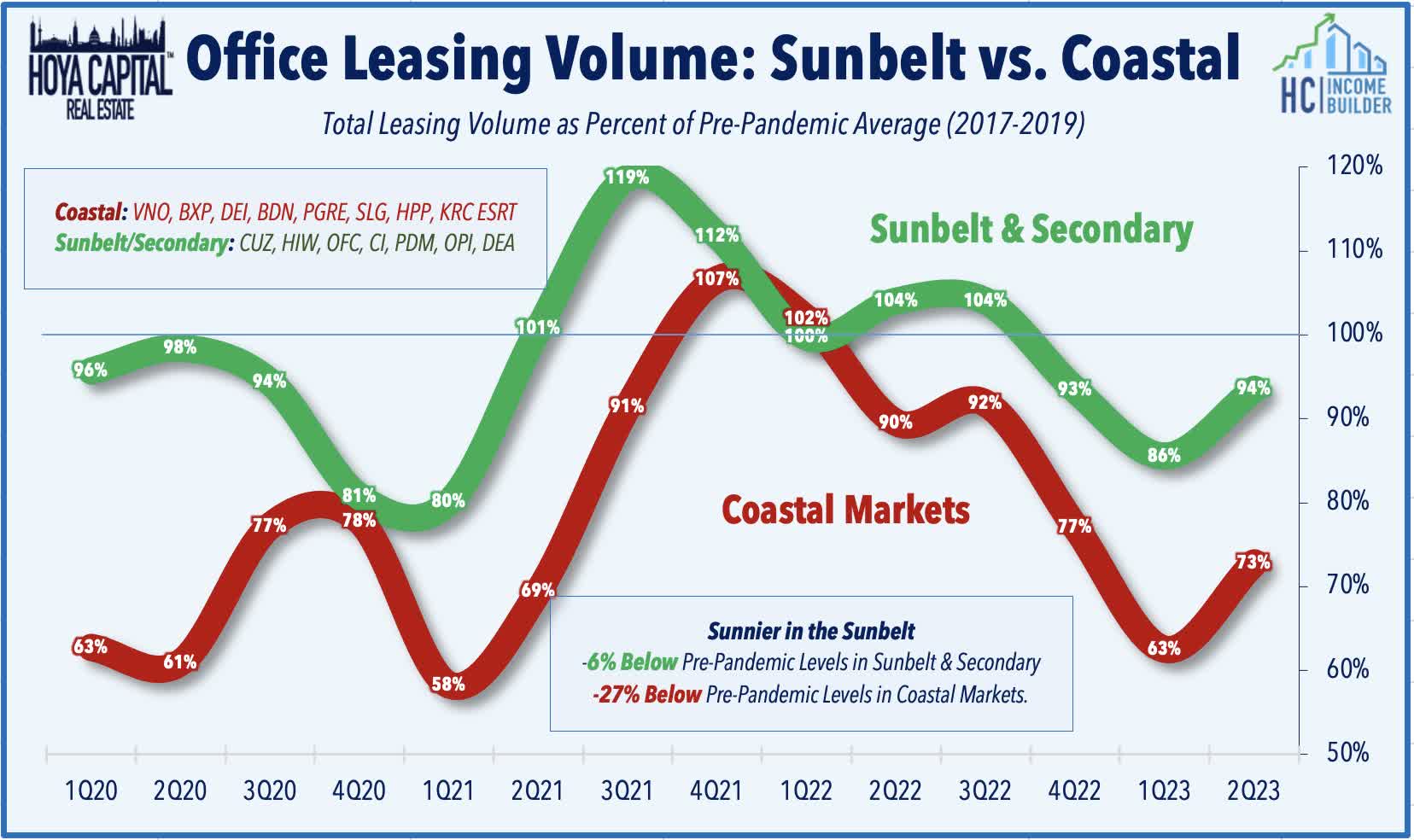

Office : After leading the gains throughout earnings season, office REITs were under pressure this week on renewed financing concerns in a potential "higher for longer" environment. Vornado Realty ( VNO ) dipped 7% following a Bloomberg report that it is weighing a partial or full sale of its redeveloped Farley Building in New York City - one of its top-performing assets that is leased to Meta Platforms under a 15-year lease - as it seeks to shore up its balance sheet and potentially refinance other high-cost capital. Bloomberg reported that other option for the NYC-focused office REIT may include putting a mortgage on the unencumbered asset, which has no property-level debt. As noted in our Earnings Recap , Office REITs posted the strongest stock performance this earnings season after results were "less bad" than feared, and alongside indications that the "return to the office" has picked up steam as labor markets loosen. The sharp regional bifurcation persists, however, as coastal-focused REITs reported leasing volume that remained about 25% below pre-pandemic levels in Q2, but Sunbelt and Secondary market-focused REITs reported total leasing volume that was just 6% below typical pre-pandemic levels.

{kind=link}

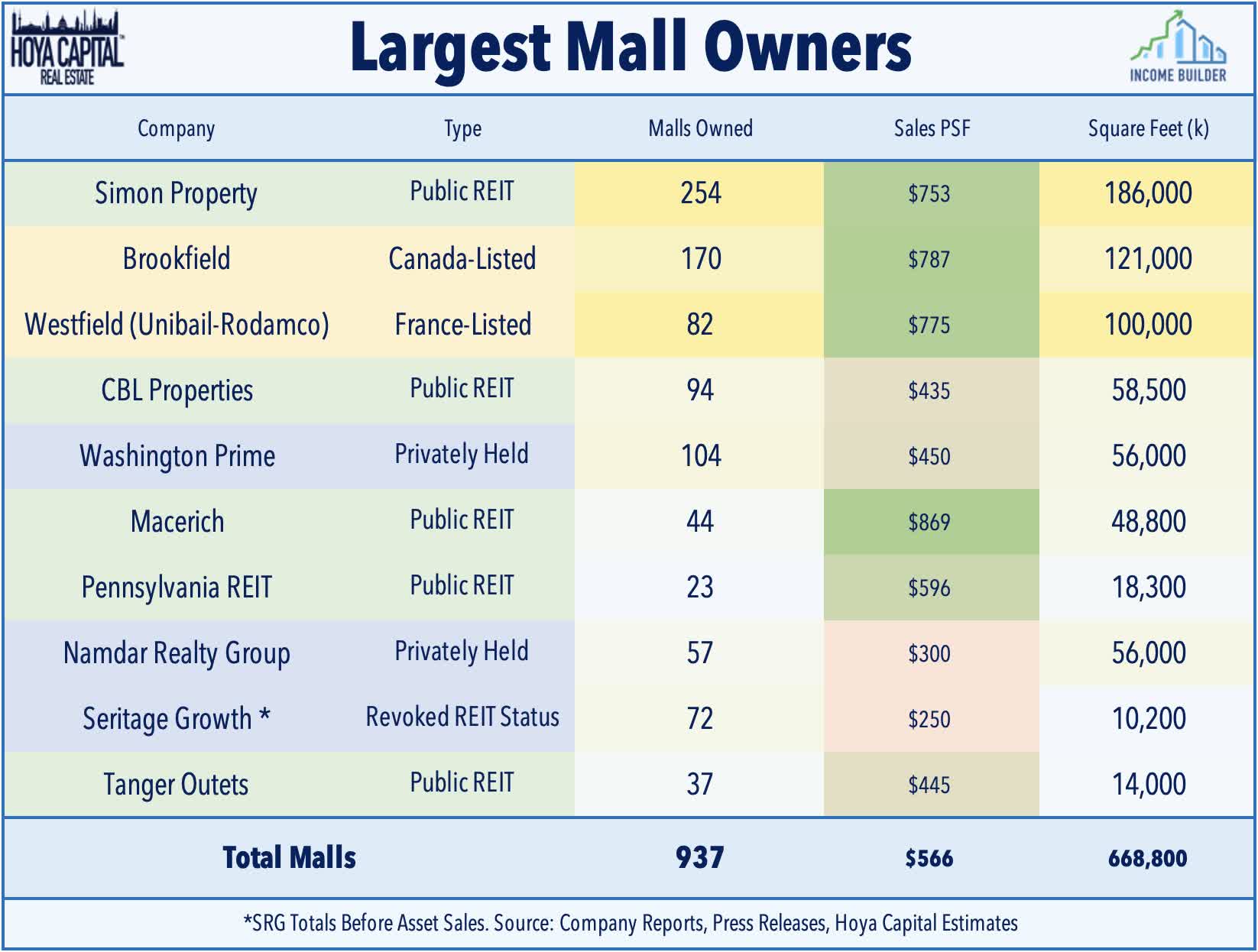

Mall : Seritage Growth ( SRG ) - the spin-off from Sears that began a strategic liquidation of its portfolio in March 2022 - dipped more than 10% this week after reporting second-quarter results and providing an update on its sales progress and current holdings, which included the recognition of a $104.5M impairment on its development property in Aventura, Florida. SRG noted that it has now sold a total of 127 properties for $1.4 billion in gross proceeds and paid down $960M on its term loan. Most closely-watched within SRG's results is the pricing on its recent asset sales. SRG noted that, since the start of Q2, it has either sold or has an accepted offer on six malls worth $124M at a 7.3% average cap rate, which compares favorably to the 8.0% reported cap rate from the sales in the prior quarter. Total sales for the quarter - which includes non-stabilized and joint venture interests - totaled $295.4M. SRG noted that its remaining portfolio includes 3 stabilized assets, 5 partially stabilized assets, 7 joint-venture assets, and 18 non-income producing parcels. After paying off $250M during the quarter and $70M subsequent to quarter-end, the company's current loan balance stands at $480M.

{kind=link}

Apartment : Continuing with the theme of capital-raising through asset sales, sunbelt-focused apartment REIT NexPoint Residential Trust ( NXRT ) - which was slammed after reporting downbeat results earlier this month - was among the leaders this week after it announced that it reached agreements to sell two Texas properties - Old Farm in Houston and Silverbrook in Dallas - to separate buyers, with an expected closing in early Q4 2023. NXRT had been seeking to sell these properties since early 2023 when it noted plans to exit the Houston market and pay off its most expensive variable rate debt capital. NXRT expects the dispositions of these assets to generate approximately roughly $68M in proceeds at a combined cap rate of 4.96%. After completing these sales, NXRT expects to pay off the entire $57 million outstanding balance on its corporate credit facility and reduce its variable rate debt exposure to just 3% from 12%, addressing perhaps the most significant source of concern for the small-cap REIT, which has been among the most highly-levered residential REITs.

{kind=link}

After publishing Winners of REIT Earnings Season last week, we published Part 2 of our Earnings Recap this week: Losers of REIT Earnings Season . While there were upside standouts and some solid reports within these lagging property sectors, the losers of REIT earnings season included: Self-Storage, Hotel, Healthcare, and Specialty REITs. Many of the "misses" emanated from the direct and secondary effects of the higher interest rate environment, underscoring the continued challenges facing more-highly-levered private real estate portfolios. More concerning was the handful of downward revisions driven by sudden demand softness cited by the most pro-cyclical property sectors: hotel and billboard REITs, indicating that more corporations are in cost-cutting mode. Consumer softness was also seen via an uptick in unpaid mid-tier apartment rents and sluggish storage demand. The Sunbelt vs. Coastal bifurcation hasn't completely dissipated, but market-level performance is becoming more localized. West Coast weakness was a common thread across most property sectors, but NYC was a notable upside standout.

{kind=link}

Mortgage REIT Week In Review

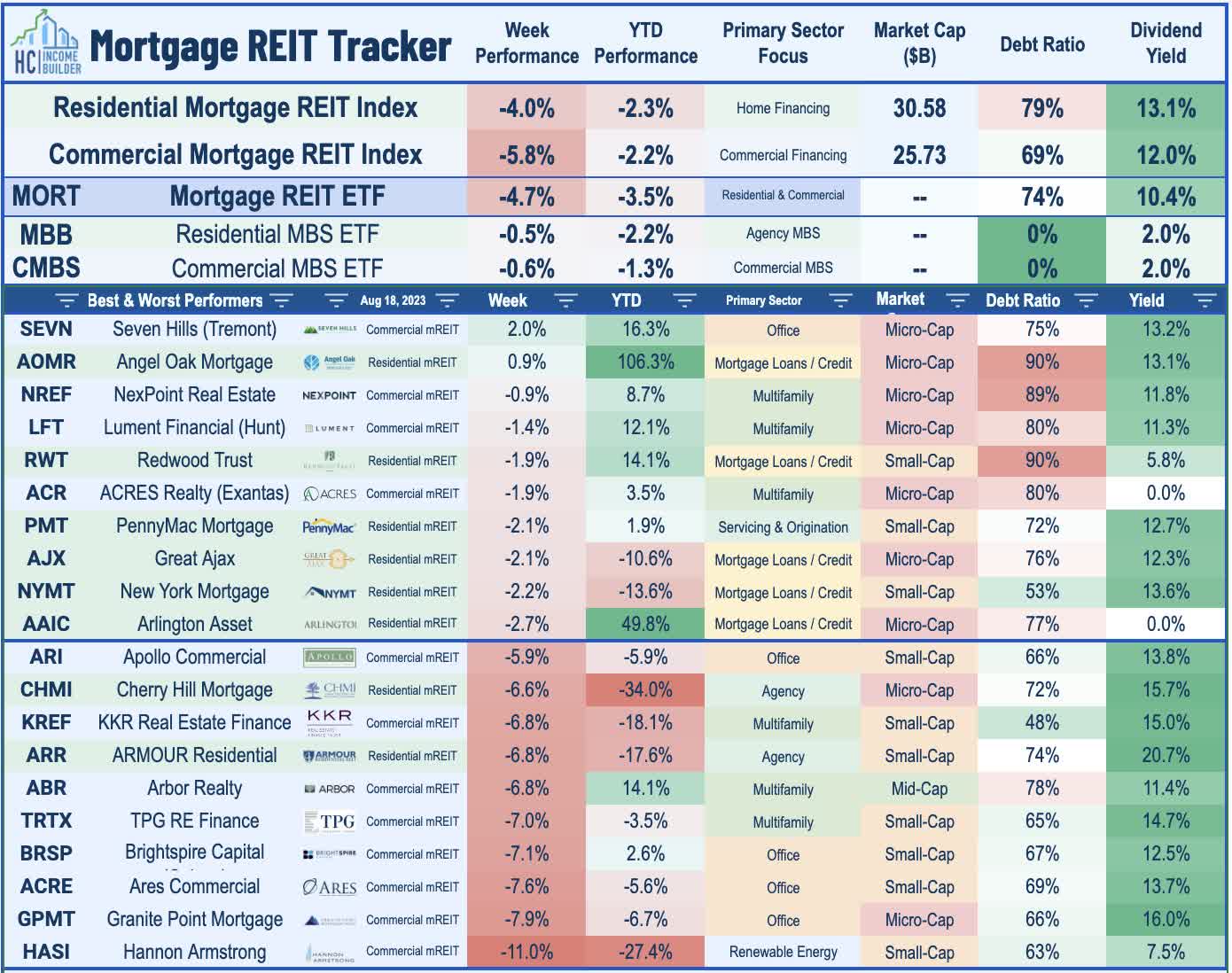

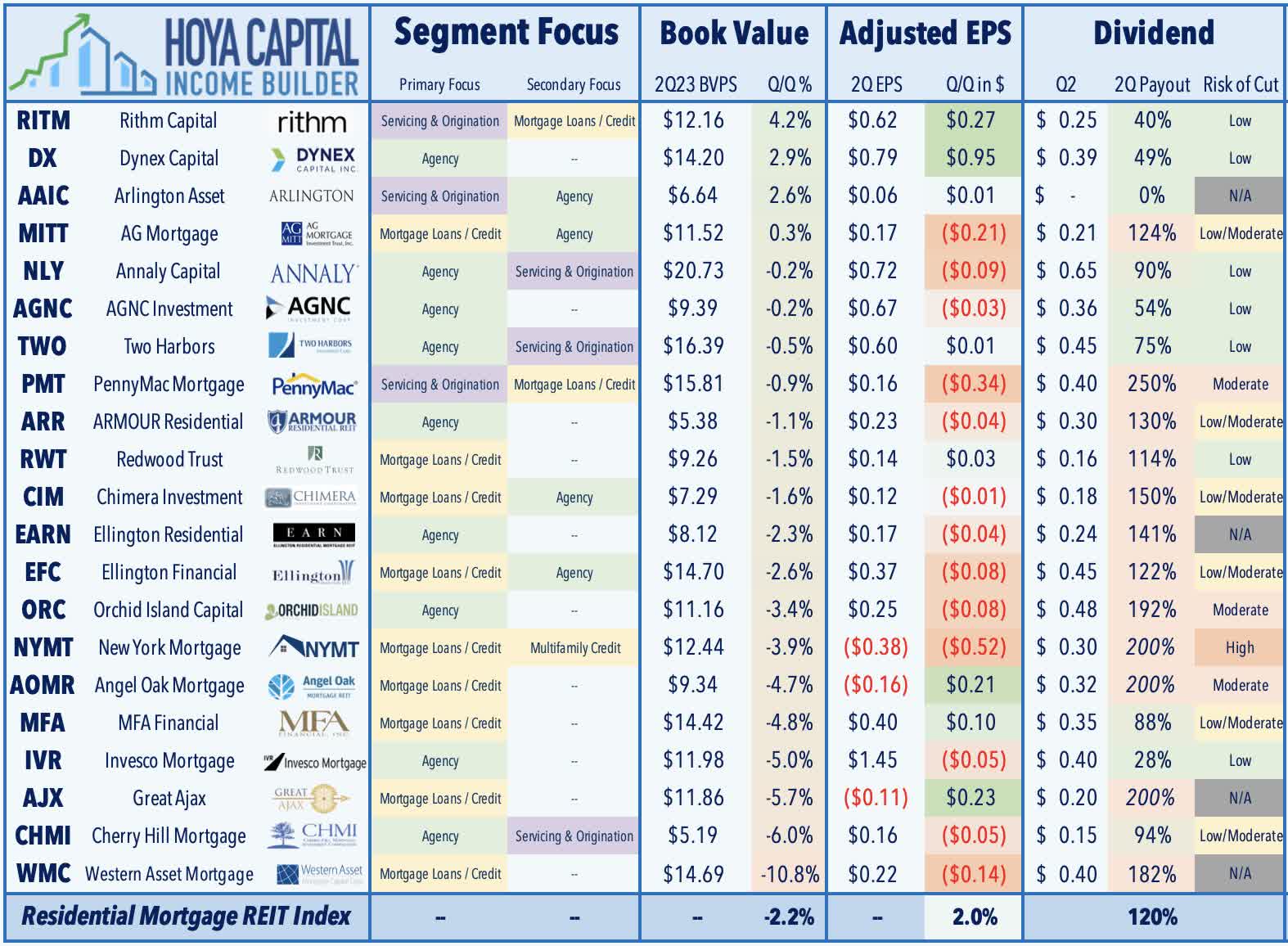

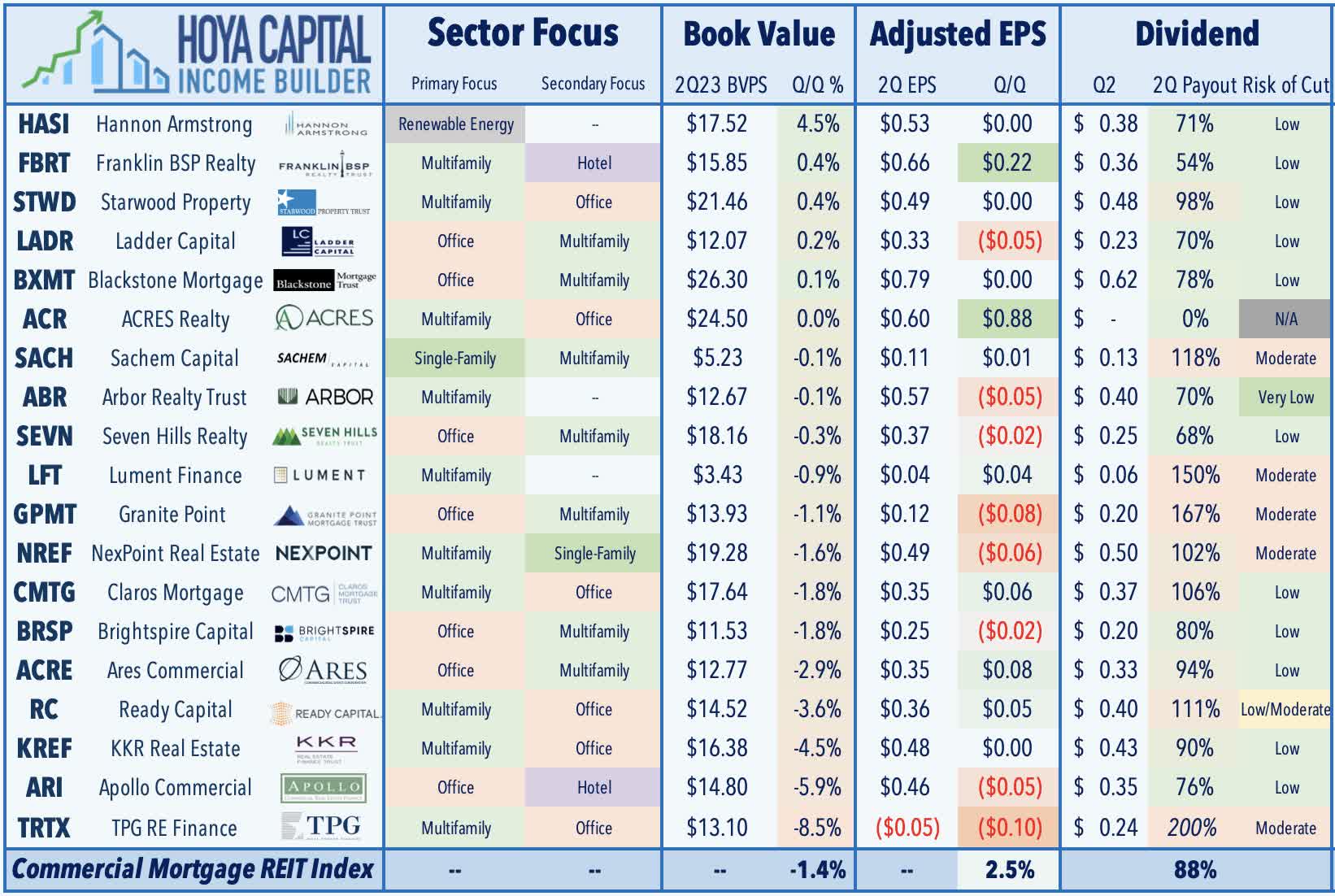

Mortgage REITs finished slightly lower this week, with the iShares Mortgage Real Estate Capped ETF ( REM ) slipping 1.2%, as earnings season wrapped up with results from nearly a dozen mREITs. On the downside this week, Hannon Armstrong ( HASI ) - a commercial mortgage REIT focused on solar and renewable energy projects - slid 11% to its lowest levels since April 2020 after Citi initiated the company with a Street-low price target, citing caution related to its dependence on equity capital raising. Last week, HASI raised $350M through a private offering of 3.75% exchangeable five-year senior notes due 2028. Office-focused lenders were among the laggards this week as well including Granite Point ( GPMT ), Ares Commercial ( ACRE ), and BrightSpire Capital ( BRSP ).

{kind=link}

Small-cap Arlington Asset ( AAIC ) - which agreed to be acquired by fellow mREIT Ellington Financial in late-May - was among the better-performers after it wrapped-up residential mREIT earnings season with a decent report, noting that its distributable EPS increased a penny to $0.06 while its Book Value Per Share increased to $6.64 - up 2.6% from the prior quarter. On average, the 21 residential mREITs reported an average BVPS decline of 2.2% in Q2, but recorded a 2.0% increase in their distributable earnings, which combined with the handful of dividend cuts during the quarter, resulting in a reduction in the average payout ratio from roughly 130% to 120%. The average residential mortgage REIT pays a dividend yield of 13.1%.

{kind=link}

Small-cap Sachem Capital ( SACH ) finished lower by 4% after it concluded commercial mREIT earnings season with reporting in-line results, noting that its distributable EPS also rose by a penny to $0.11, while its BVPS was flat in Q2. On average, the 19 commercial mREITs reported an average BVPS decline of 1.4%, while the average commercial mREIT reported a 2.5% increase in comparable EPS, which trimmed the average payout to 88% from 90%. The average commercial mREIT pays a dividend yield of 11.9%.

{kind=link}

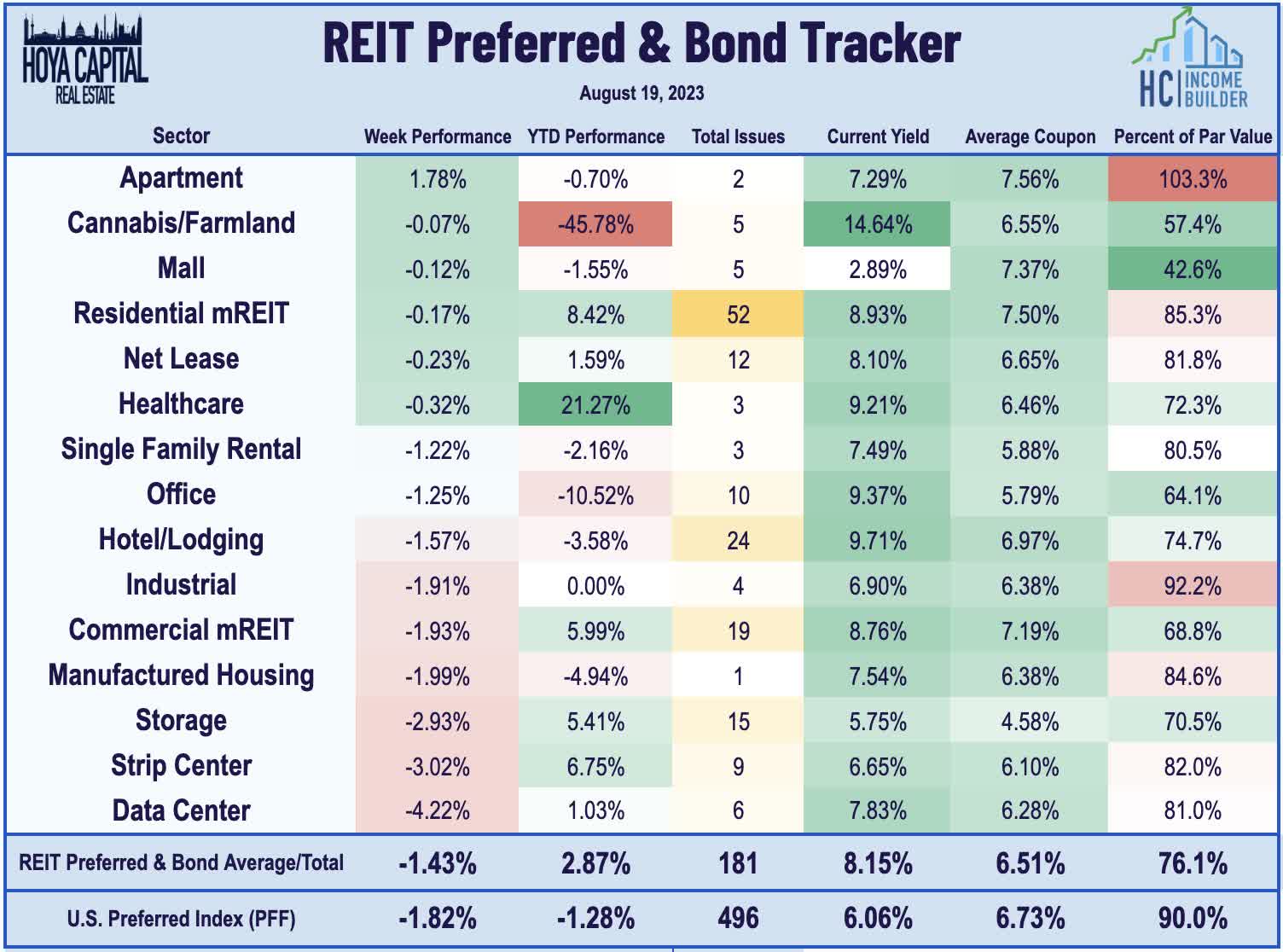

REIT Capital Raising & REIT Preferreds

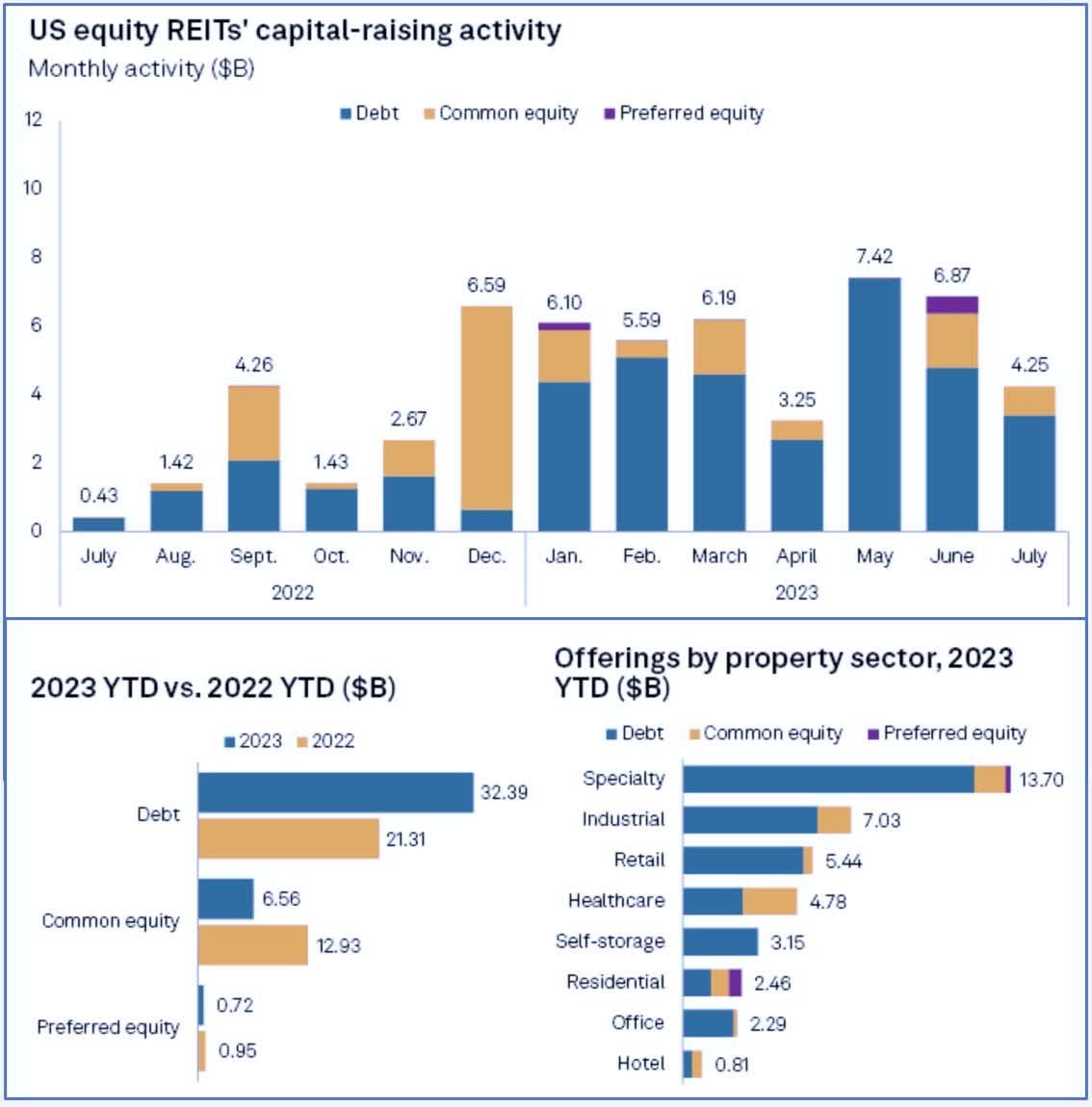

S&P reported this week that REIT capital raising activity slowed in July after a relatively strong two months of activity in May and June. REITs collectively raised $4.25 billion in new capital, bringing the year-to-date total to $39.7 billion which is 12.7% higher than the capital raised during the same period in 2022. The majority of the capital raised in July - and for the year - came through debt offerings, which have accounted for 82% of the total capital raised this year - well above the historical average of around 50%. The single largest common equity offerings year to date came via Welltower's (WELL) at-the-market offering program, which has raised $2.2B through July. American Tower (AMT) has raised the most capital year to date at $5.5B, followed by industrial REIT Prologis at $5.4B. REITs were quiet on the capital-raising front this week with the exception of skilled nursing REIT, Omega Healthcare (OHI), which announced a new two-year $400M term at an all-in fixed rate of 5.565%.

{kind=link}

Credit ratings agencies were busy this week, however, with a handful of upgrades, downgrades, and affirmations. On the upside, S&P raised Xenia Hotels' (XHR) issuer credit rating to “B+” from “B” and its senior unsecured debt to “BB-“ from “B+” with a stable outlook. Fitch Ratings affirmed their rating of Invitation Homes (INVH) at “BBB” and revised the outlook to positive from stable. Fitch also affirmed Essential Properties (EPRT) and Four Corners (FCPT) at “BBB” with a stable outlook while S&P affirmed Public Storage at "A" with a stable outlook. S&P also affirmed OUT 's “B+” issuer credit rating but revised its outlook to stable from positive. On the downside, Fitch downgraded SL Green (SLG) to “BB+” from “BBB-“ with a negative outlook. Back on the secondary markets, the InfraCap REIT Preferred ETF ( PFFR ) slipped 1.4% on the week, slightly outperforming the iShares Preferred ETF , which dipped 1.8%. For the year, the REIT Preferred ETF have delivered total returns of 8.0%, topping the 2.6% total returns from the broad-based iShares Preferred ETF.

{kind=link}

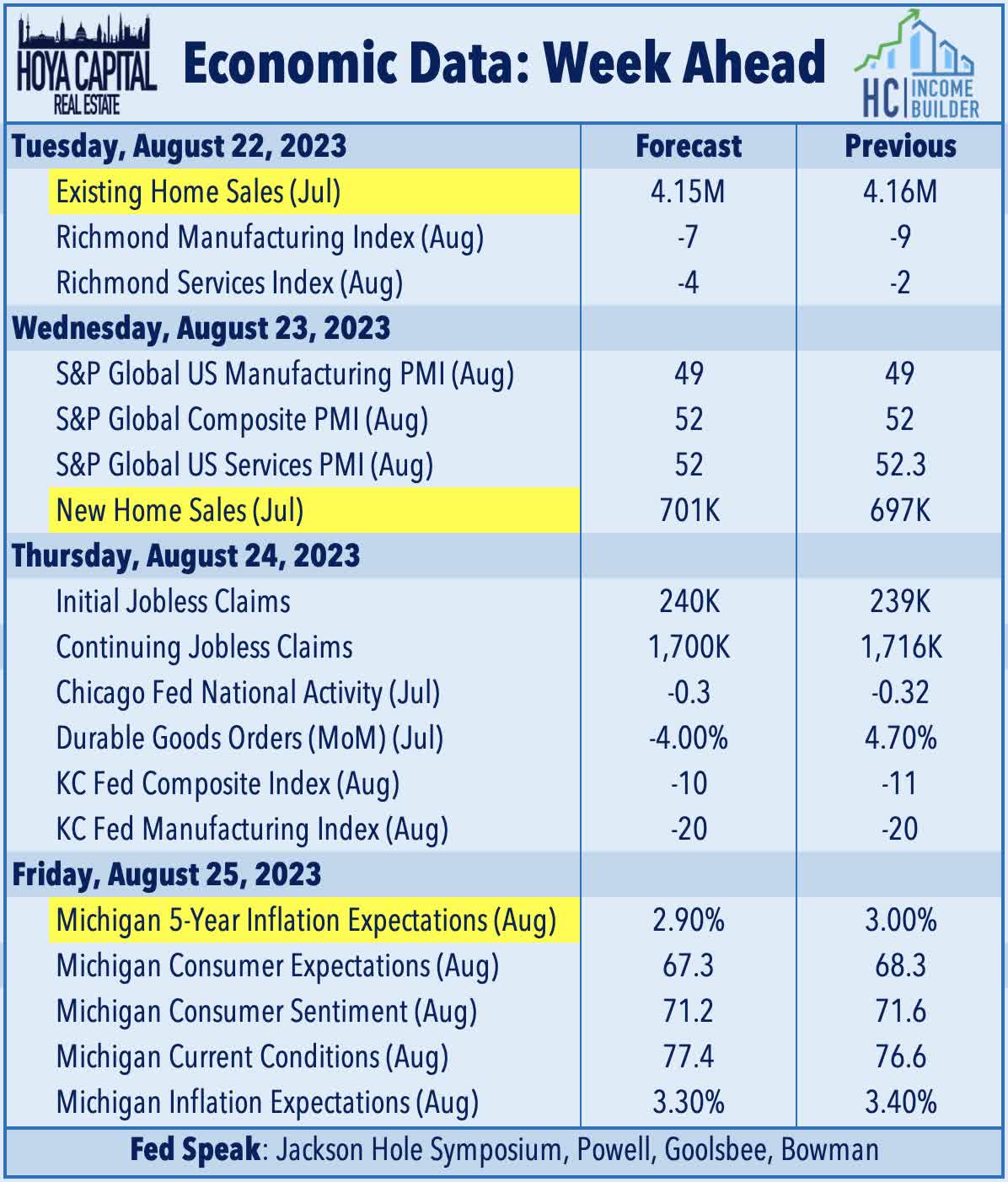

Economic Calendar In The Week Ahead

The state of the U.S. housing market remains in focus in the week ahead. We'll see Existing Home Sales data on Tuesday which is expected to show a decline in sales velocity in July to a 4.15M annualized rate - up slightly from the lows in January of 4.0 million but well below the 2021 highs of over 6.5 million. Housing inventory levels have remained near historically low levels this year due, in part, to the so-called "lock-in" effect on existing mortgages, which has kept a floor on home values and rental rates despite the stiff affordability headwinds. We'll see New Home Sales data on Wednesday, which is expected to show an annualized sales rate of 701k in July - up from the 2022 lows of around 550k but well below the peak velocity of over a million units in late 2020. The largest single-family homebuilders have, so far, been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. The most closely-watched event of the week comes on Friday morning, when Federal Reserve Chair Jerome Powell will deliver remarks at the Fed's Economic Policy Symposium in Jackson Hole.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Higher For Longer