HI - Hillenbrand: Near-Term Headwinds And High Net Leverage

2023-11-23 21:21:16 ET

Summary

- Hillenbrand, Inc. is facing near-term revenue headwinds due to lower backlog and order bookings in its APS and MTS segments.

- The company's margin outlook is mixed, with cost management initiatives being offset by the negative impact of lower-margin FPM acquisition and volume deleveraging.

- The company's near-term outlook is challenging, with a decline in organic revenue growth and high net leverage, leading to a neutral rating on the stock despite lower than historical valuation.

Investment Thesis

Hillenbrand, Inc.'s ( HI ) revenue faces near-term revenue headwinds from lower backlog and order bookings in both the Advanced Process Solutions ((APS)) and Molding Technology Solutions ((MTS)) segments. The current macroeconomic uncertainty and a high-interest rate environment are resulting in an increase in the decision timing of the company's customers, particularly within the large projects which is impacting orders and sales for its APS business. In its MTS business, a soft order environment for its capital equipment business including a decline in orders for injection molding equipment is expected to adversely impact the company’s revenue in the coming quarters. In addition, the company is unlikely to pursue M&As in the near term given its high net leverage of 3.2x.

The near-term margin outlook is challenging with the negative impact of lower margin Schenck's Food and Performance Materials ((FPM)) acquisition and volume deleverage. The company’s valuation is at a discount versus the historical averages. However, I believe it's best to wait on the sidelines till order trends improve and net leverage reaches the targeted levels. Hence, I have a neutral rating on the stock.

Revenue Analysis and Outlook

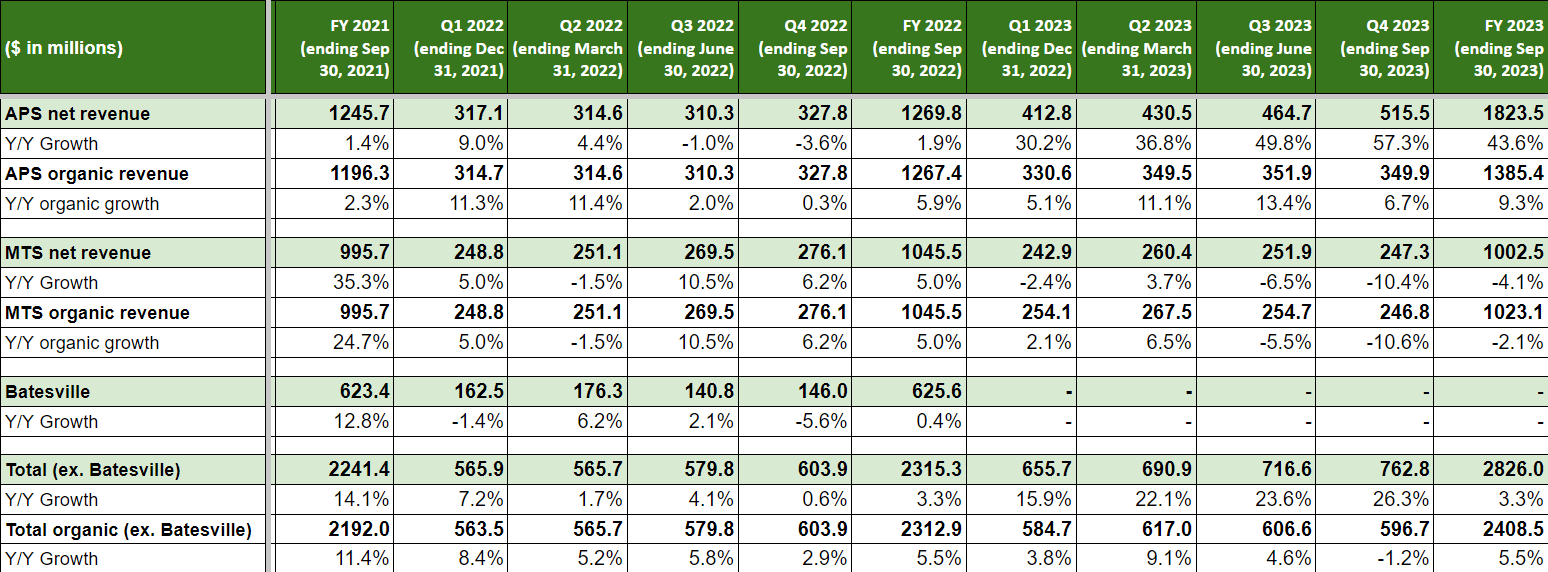

After seeing good growth in revenue in the last couple of years, the company’s organic revenue growth turned negative last quarter. I previously covered the stock in August when I raised concerns about rising macroeconomic uncertainty and declining backlog impacting the company’s organic revenue. In the fourth quarter of 2023, the company reported a 26.3% Y/Y increase in net revenues to $762.8 million primarily attributed to the favorable impact of acquisitions, including a $43 million contribution from the Schenck Process Food and Performance Materials acquisition, which was completed on September 1, 2023. However, on an organic basis, revenues declined 1.2% Y/Y as higher pricing and increased volume in the Advanced Process Solutions segment was more than offset by lower volume in the Molding Technology Solutions segment.

In the Advanced Process Solutions segment, net revenues grew 57.3% Y/Y mainly due to the favorable impact of acquisitions including the Schenck Process Food and Performance Materials acquisition (completed in September 2023), Peerless Food equipment acquisition (completed in December 2022) and LINXIS Group SAS acquisition (completed in October 2022). Organic revenues rose 6.7% Y/Y driven by favorable pricing and higher aftermarket parts and service revenues.

On the other hand, the Molding Technology Solutions segment’s net revenue declined 10.4% Y/Y and 10.6% Y/Y organically due to a decline in hot runner and injection molding equipment sales.

{kind=link}

HI’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, the company’s near-term outlook is challenging.

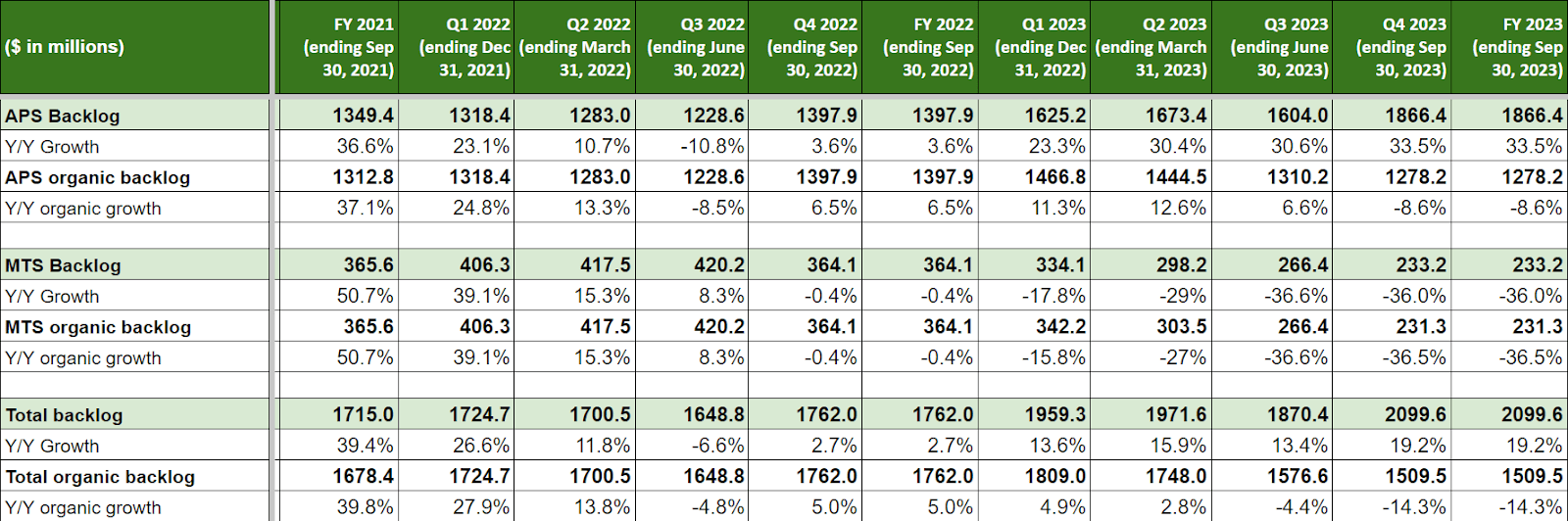

If we look at the company’s organic backlog, it was down 14.3% Y/Y at the end of FY23 with the APS segment organic backlog down 8.6% Y/Y and the MTS segment backlog down 36.5% Y/Y.

{kind=link}

HI’s Historical Backlog Growth (Company Data, GS Analytics Research)

In the APS segment, the current macroeconomic uncertainty and high-interest rate environment are resulting in customers delaying decisions on several large projects. While management has guided for organic growth of between 3% and 8% Y/Y for this segment counting on resilient aftermarket sales as well as strength in the food and pharma and recycling end market to offset the impact of the slowdown in other markets, I am skeptical. Aftermarket sales constitute ~28% of the APS segment’s total sales while capital equipment is ~72% of total sales. So, it is unlikely that Aftermarket growth can offset the impact of ~8.6% Y/Y decline in capital equipment backlog. End market-wise, while food and pharma including the recently acquired FPM business are ~34% of APS segment revenue, and recycling is around 3%, I don’t think they should be able to offset the slowdown in Plastics and Chemicals which is 51% of segment revenue and this has been evident from the recent organic backlog decline. I believe management is building in some kind of improvement in their large project orders in their guidance, especially in the back half of the year but I believe a wait-and-watch approach may be prudent.

MTS is doing even worse with a backlog declining 36.5% Y/Y due to decreased orders for injection molding equipment and this should result in a Y/Y decline in revenues.

Overall, the company has guided for -3% to 3% Y/Y organic revenue growth and I am towards the lower end of the guidance range and believe if the order rate doesn't improve as the year progresses, there is a potential for downward revision in organic growth guidance.

Inorganically, the story is better with the recent acquisition of Schenck FPM business which has an annual revenue of ~$547 mn. However, after the acquisition, the company’s net leverage (net debt to EBITDA) has climbed to 3.2x and I believe the near-term focus will be on debt repayment. So, further M&As are unlikely in the near term until leverage comes down to management’s targeted 1.1x to 2.7x range.

Longer term, management is planning to increase the company’s exposure to Food and Pharma and Recycling markets. Including FPM business, these end markets currently account for ~27% of the company’s revenue and the company considers these strategic growth markets where it can post a GDP+ growth rate. However, I believe the company has to increase its sales from these markets meaningfully before investors start appreciating this opportunity. With near-term M&A activity paused due to high leverage, I don’t see much to be excited about this business in FY24 and would watch for order trends in legacy business to improve before becoming more optimistic on the company’s prospects.

Hillenbrand's changing end-market exposure (Company Presentation)

Margin Analysis and Outlook

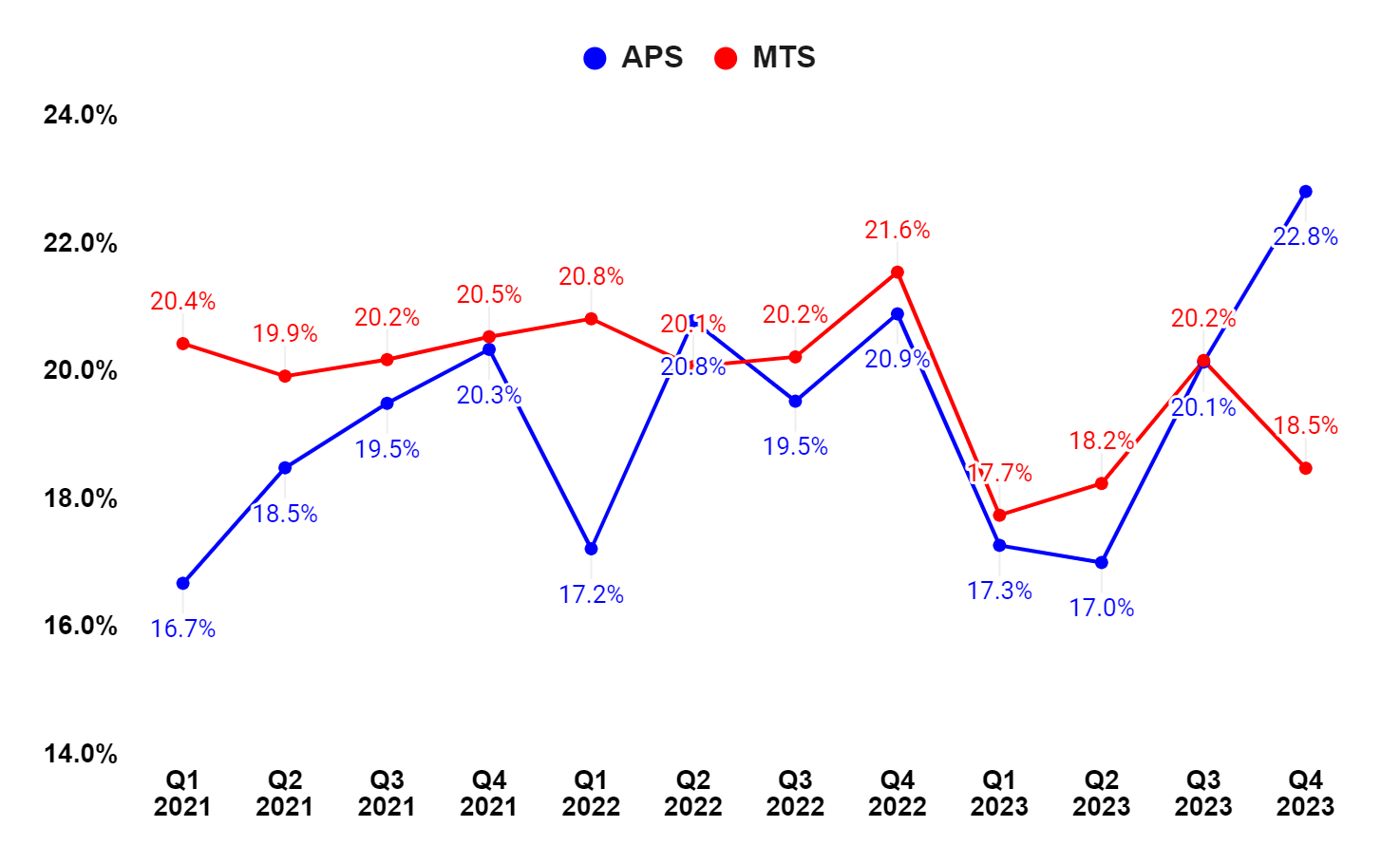

In Q4 2023, Hillenbrand's margins benefitted from favorable pricing, productivity improvements, and lower variable compensation. These positive factors helped more than offset the adverse impact of inflationary costs and lower volume in the Molding Technology Solutions segment. This resulted in an adjusted EBITDA margin increase of 90 bps Y/Y to 19.3%. The Advanced Process Solutions segment led the margin growth, which grew adjusted EBITDA margin by 190 bps Y/Y. Meanwhile, the Molding Technology Solutions segment’s adjusted EBITDA margin declined 310 bps Y/Y as lower volume, cost inflation, and unfavorable product mix outweighed the benefits from productivity improvements, lower variable compensation, and favorable pricing.

{kind=link}

HI’s Segment Wise Adjusted EBITDA margin (Company Data, GS Analytics Research)

Looking forward, in the near term, APS segment margins should be negatively impacted by FPM acquisition as FPM has a lower margin than APS business. In the MTS business, the company is focused on productivity and managing costs but I believe volume deleverage from a significant decline in sales should offset their impact to a good extent.

However, in the medium to long term, as the company realizes synergy benefits from integrating the FPM business and volumes eventually recover, there should be some improvement in the margins. So, the margin outlook is mixed.

Valuation and Conclusion

The company is currently trading at 11.97x FY24 consensus EPS estimates of $3.22 which is a discount versus the company’s average forward P/E of 12.84x over the last 5 years.

The company’s organic revenue should be negatively impacted in the near term due to a lower backlog, a slowdown in the Plastics and Chemicals end market of the APS segment, and a soft order environment for injection molding equipment in the MTS segment. There should be a pause in near-term M&A activity as well due to high leverage. The near-term margin outlook is also unfavorable with the adverse impact of lower-margin FPM acquisition and volume deleveraging from lower sales offsetting the benefits from productivity and cost savings. While the company may hold some promise in the long-term given its focus on increasing exposure toward food and pharma and recycling end markets, I believe it's prudent to wait on the sidelines till order trends improve and net leverage comes down to the targeted levels. Hence, I have a neutral rating on the stock.

For further details see:

Hillenbrand: Near-Term Headwinds And High Net Leverage