HI - Hillenbrand: There Is Upside But Time Is Needed

2023-09-07 09:57:04 ET

Summary

- Recent economic data suggests a slowdown in the US labor market and moderate inflation, leading to hopes that the interest rate hike cycle may be over.

- Hillenbrand, an industrial stock, is worth considering as it has undergone a transformation phase with divestitures and acquisitions in higher growth markets.

- While Hillenbrand's recent financial results have been mixed, its acquisitions in the food and recycling sectors position it for long-term growth opportunities.

Economic data released in recent days has signaled a moderate pace of inflation and a slight slowdown in the US labor market, renewing hopes that the interest rate hike cycle may be over.

While it is likely to give another boost to the broader stock market, I am particularly interested in investment opportunities in industrial stocks, as they can benefit from the end of the monetary tightening cycle promoted by the Fed and other central banks.

One company I believe is worth taking a look at is Hillenbrand (HI), an overlooked machinery stock that has been under a transformation phase, with the divestiture of the death care business and acquisitions in higher growth end markets, such as food and recycling. While this is an ongoing strategic shift, the stock's current undervaluation offers an attractive long-term opportunity for patient investors.

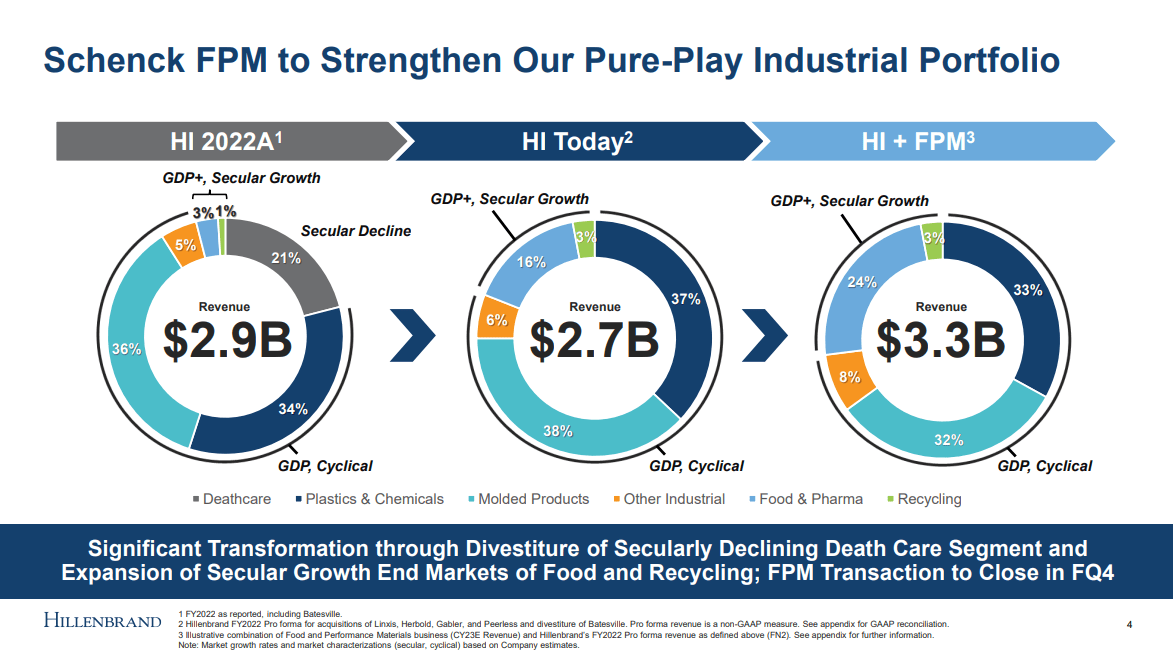

Reshaping the Portfolio

With the divestiture of Batesville, completed in Feb. 2023, Hillenbrand exited the declining death care business that represented nearly 20% of revenue for the company. Meanwhile, the company has added important capabilities over the course of the last 12 months or so by acquiring companies in the food and recycling sectors that are generating growth for the company since then.

The most recent deal was the acquisition of Schenck Process Food and Performance Materials ("FPM") business, completed on Sept. 1st, for nearly $730m million. With this transaction, Hillenbrand expects that roughly 30% of the company's total revenue will come from higher growth, less cyclical end markets like food, pharma and recycling. The figure below shows how these changes can be a game changer for the company in terms of end market exposure and growth potential over time.

Hillenbrand Q3 2023 Earnings Presentation

{kind=link}

With these acquisitions, Hillenbrand has now a comprehensive portfolio in the food processing industry, including mixing, ingredient automation and portioning solutions to attend applications such as baked goods, pet foods and alternative proteins, which are markets expected to growth above the nominal GDP over the coming years, driven by factors such as the increasing pet ownership and higher demand for plant-based meat.

In the recycling business, on the other hand, the acquisition of Herbold in 2022 added capabilities in plastics recycling, a fast-growing segment boosted by increasing environmental awareness and government regulation.

Mixed Year to Date Results So Far

While these deals should be seen as quite positive for the company with regards to its growth profile in the long run, most recent financial results have showed the overall performance has been mixed, as the weakness in the Molding Technology Solution ("MTS") segment weighed on the consolidated results.

Hillenbrand total revenue has been generally in line with consensus estimates this year, while last quarter fell short of expectations by 1.8%. With total revenue growth of 24%, compared to last year, mostly driven by acquisitions, the company delivered a healthy organic growth of 5%, thanks to positive pricing and strength in plastics systems segment.

The biggest contribution came from the Advanced Process Solutions ("APS") segment, with growth of 50% over a year ago, thanks not only to acquisitions, but also a solid organic growth of 14% in the segment, led by positive pricing trends and higher demand for plastic systems.

On the flip side, revenue from molding business declined 7% compared to last year, reflecting customers delays and weakness in China region, in a scenario consistent with we have seen over previous quarters.

This kind of bifurcation we have seen between Hillenbrand's two core segments in the top line is reflected in margins as well. EBITDA margin in APS segment increased 60 bps to 20.1%, led by favorable pricing, operating leverage due to higher volumes and productivity, while EBITDA margin in MTS segment remained at 20.2%, as cost management measures offset lower volumes.

The backlog remains strong across durable plastics, recycling, and food in the APS segment, despite customer delays in some large plastics, and demand across recent acquired businesses remains healthy, as evidenced by sequential revenue growth of 20% in the last quarter.

In the meantime, the demand in the molding business has not rebounded yet, with macroeconomic uncertainties in China leading to a more cautious approach from customers regarding new investment for the time being. As a result, backlog in the segment declined 37% compared to a year ago.

As we get through the back half of the year, despite the integration of FPM will raise the participation of faster growth food and pharma business to roughly 25% of Hillenbrand's total revenue from 15% at the moment, the molding business still represents nearly 35% of the consolidated revenue. That will continue to drag down top line growth over the next quarters and pressure earnings as well.

In addition, as FPM and other recent acquisitions operate with lower margins relative to Hillenbrand, the integration of them will not be as accretive as they might be at first sight in terms of bottom line.

Therefore, in the short term, the impact of these acquisitions will be somewhat limited to Hillenbrand and time is required for the company to integrate the businesses, improve efficiency and take full advantage of the combined portfolio with these new brands and technologies to drive profitable growth substantially.

Based on this scenario, I estimate top-line growth for fiscal year 2024 at low to mid-single digit, as nearly a third part of the combined revenue comes from the molding business and the time of the recovery of this business is uncertain. This top-line growth should support a moderate operating leverage gain and earnings growth at high-single digit, absent any adverse price action in the company's end markets.

An Undervalued Stock Compared to Peers

After trading near historical highs in June and July, shares of Hillenbrand have declined nearly 10% following Q3 2023 earnings posted on Aug. 2nd, in a sizeable underperformance relative to industrial sector, measured by the Industrial Select Sector SPDR ETF (XLI), that lost 2% and the S&P 500, that remained roughly flat over the same period.

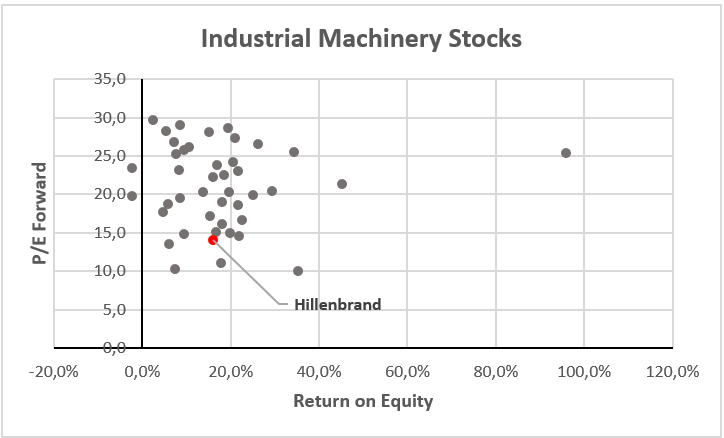

Currently, trading at a P/E forward of 14.0, shares of Hillenbrand are well below the machinery stocks' average of nearly 20.9, suggesting an upside of as high as 33% to the stock price.

In addition, some financial metrics such as ROE can provide further insights to gauge Hillenbrand's valuation relative to the peer group, taking into consideration earnings quality as well.

The chart below comparing Hillenbrand based on ROE versus P/E Forward shows the company in the mid of the pack in terms of ROE, while Hillenbrand's P/E Forward is clearly below the average, reinforcing the notion that this stock is undervalued compared to its peers.

Seeking Alpha, consolidated by the author

{kind=link}

That said, let's keep in mind that shares of Hillenbrand are still 6% above the 5-year average of 13.2. So, to me, it seems that a significant upside for Hillenbrand is unlikely before higher growth expectations are in place, as current multiples are above historical norms.

In summary, it is fair to say that Hillenbrand is arguably an undervalued stock at the current levels. However, we may not see enough catalysts to move prices up substantially in the short run. Anyway, if earnings growth of high-single digit can be materialized over the next 12 months, it is possible to see stock prices moving higher just to maintain current valuation levels.

We should be aware, however, of the ongoing challenges for the company, such as the successful integration of the acquired businesses and the lingering weakness in the molding segment, that may affect the business and financial performance over the coming months.

Longer term, as the company can move forward with this strategic shift, investors should be rewarded by holding shares of this company and the recent selloff we have seen since August may be an opportunity to add shares at lower prices.

For further details see:

Hillenbrand: There Is Upside, But Time Is Needed