PTY - HIO: Unleveraged Fund With A Leveraged Performance

Summary

- Western Asset High Income Opportunity Fund is a fixed income CEF.

- The fund focuses on U.S. high yield and has a middle of the road credit build, with no excessive risk taken via CCC credits.

- The fund however displays a return profile very similar to the top HY CEF cohort, namely CIK and PTY.

- The vehicle is trading at a discount to NAV of close to -12%.

- This article covers CEFs.

Thesis

Western Asset High Income Opportunity Fund ( HIO ) is a fixed income CEF. The fund has been around since the early '90s and focuses on high yield credit. What is particular about this fund is the lack of leverage, a cornerstone of fixed income CEFs. The vehicle seeks current income, with capital appreciation as a secondary objective.

What is very particular for this fixed income CEF is its lack of leverage. Basically most CEFs in the fixed income space use leverage to juice up their returns. Leverage is what makes their high dividends possible. Not for HIO. HIO does not take excessive credit risk either, displaying a balanced credit rating build that focuses on B and BB names. The fund also utilizes a very small amount of ROC, so where does the money come from? The answer lies in the portfolio turnover figures for the fund, which speak towards more of a high yield trading shop rather than a buy and hold fund. A manager can actively trade credits and generate income that is passed on as dividends.

The fund's return profile is very similar to its leveraged peers in the space, namely the Credit Suisse Asset Management Income Fund ( CIK ), or the PIMCO Corporate & Income Opportunity Fund ( PTY ). So even if HIO has a 0% leverage ratio, its return profile is not that of an unleveraged fund. 2022 has been the perfect example of a year when true unleveraged vehicles (think the unleveraged high yield ETF JNK here) have outperformed HY CEFs by having lower negative performances. Leverage magnifies returns, both on the upside as well as on the downside. Conversely, HIO has had a total return in 2022 that falls in the same cohort as CIK and PTY. HIO might be an unleveraged fund by name, but it has a leveraged vehicle performance.

Analytics

AUM: $0.36 billion

Discount to NAV: -12%

Z-Stat: -0.1

Yield: 9%

St Dev (5Y): 9.5

Sharpe Ratio (5Y): 0.08

Leverage Ratio: 0%

Performance

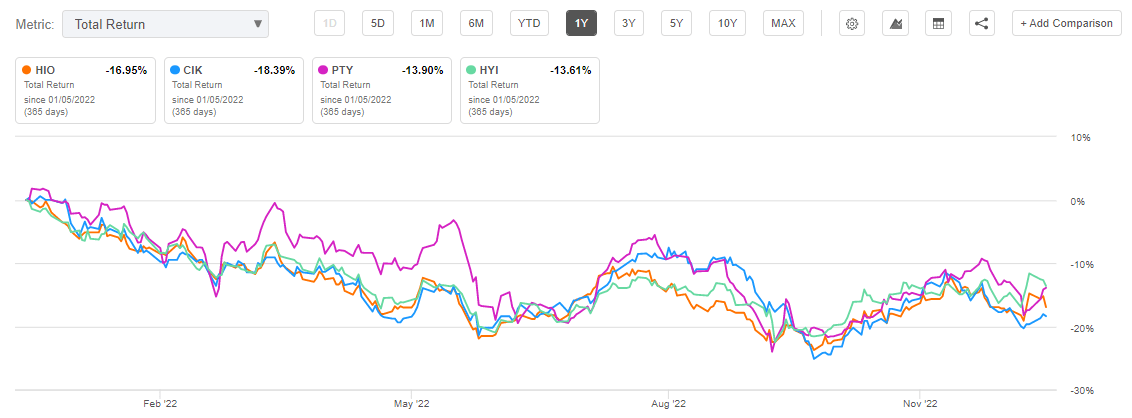

The fund was down around -17% last year on a total return basis:

{kind=link}

We can see the CEF having a similar performance with other peers in the space such as the Credit Suisse Asset Management Income Fund, or the PIMCO Corporate & Income Opportunity Fund. But these peers are leveraged, a lot actually! Both CIK and PTY have leverage ratios above 30%.

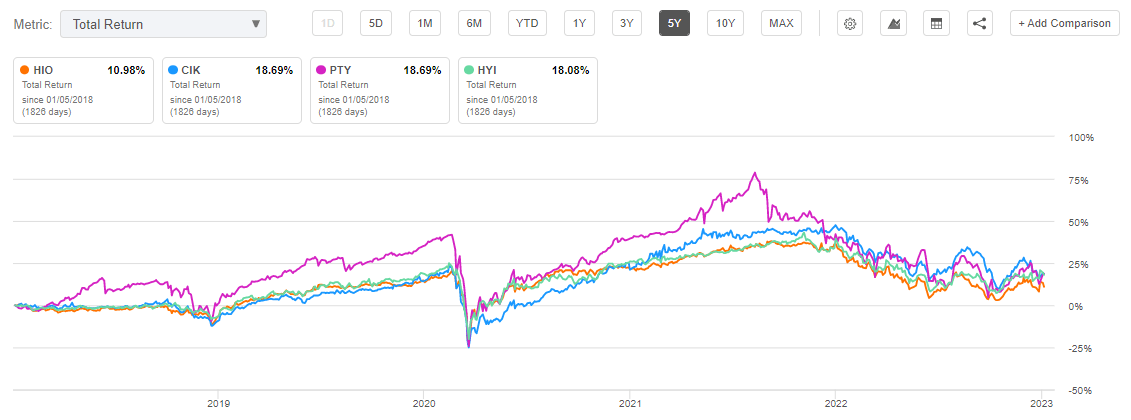

If we look at a longer time-frame, we see a similar performance:

{kind=link}

PTY and CIK outperformed during the zero rate environment that characterized 2020 and 2021, but have come back to earth since.

So we ask ourselves here - how is it possible for HIO to generate these types of results without leverage? Unleveraged high yield funds are nowhere near these sort of total returns. Just have a look at one of the most popular names in the space, namely SPDR Bloomberg High Yield Bond ETF ( JNK ). JNK's analytics and returns are nowhere near HIO's. The answer lies in the portfolio turnover performance for the CEF:

Turnover (Fund Fact Sheet)

This is a massive turnover figure, and it tells us HIO is not a buy-and-hold vehicle. HIO is more of a high-yield hedge fund lite type of vehicle. The portfolio managers trade very frequently, and in fact are able to generate returns via market activities rather than only by picking good credits, layering in leverage and waiting. So by investing in HIO, you are also taking a view on their trading acumen.

Holdings

The vehicle holds a middle of the road high yield portfolio:

Rating Profile (Fund Website)

There is no excessive credit risk here by pumping up the CCC bucket. Just an average high yield allocation.

The sectoral allocation is fairly standard as well:

HIO Sectors (Fund Fact Sheet)

We like the fact that the fund has Energy as one of its top sectors since that section of the market has made many strides in the past years to fix balance sheets, pay down debt and generate free cash flow.

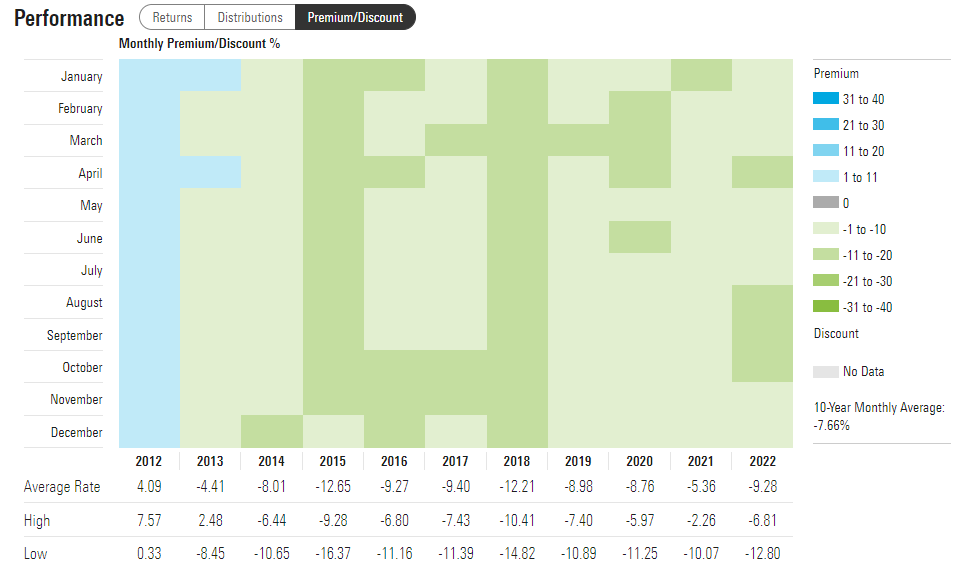

Premium / Discount to NAV

The fund usually trades at a discount to net asset value:

Premium / Discount to NAV (Morningstar)

{kind=link}

We can see that in the past decade the vehicle spent its time mostly below the value of its assets. The average rate for the discount is somewhere close to 8%.

The fund trades on risk-on / risk-off signals, with the discount narrowing when the market trades in the green:

We saw this type of behavior in August and again in November. At some point towards the end of 2023, we will see a narrowing of the discount once more.

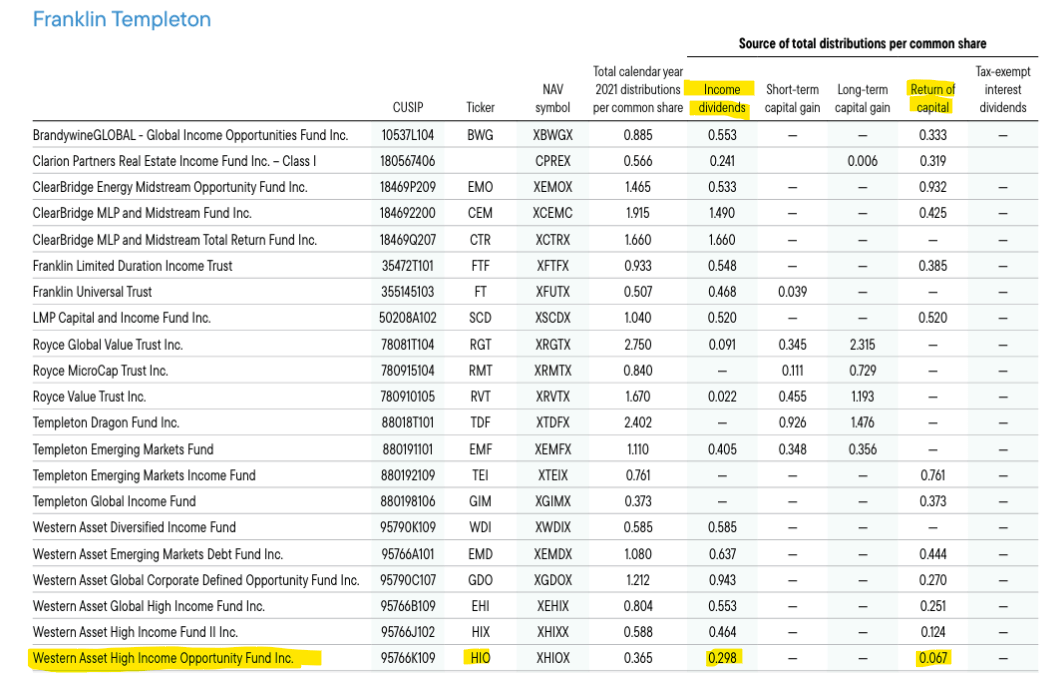

Distributions

The fund usually disburses what it makes, with a very low utilization of ROC:

{kind=link}

That is a net positive for the fund since ROC is very NAV destructive.

Conclusion

HIO is a U.S. high yield fixed income closed end fund. The fund has a middle of the road credit build, with no excessive risk taken via CCC credits and a balanced sectoral approach (no sector breaches a 17% threshold). The fund's return profile, however, is very similar to the top HY CEF cohort, namely CIK and PTY. We believe HIO achieves these results with a very active portfolio turnover / trading strategy. The fund is not a vehicle that purely buys and holds credits, but more of a trading shop. When owning this name, you are also underwriting to a certain extent the manager's trading acumen. The vehicle is trading at a discount to NAV of close to -12%, and has seen this metric have a high correlation to the market wide risk-on/risk-off sentiment. The fund's monthly dividend is fairly well covered, and the CEF has made use of small amounts of ROC in the past. Despite its lack of leverage, do expect a performance and volatility here that are in line with the classic 30% leveraged U.S. HY CEF.

For further details see:

HIO: Unleveraged Fund With A Leveraged Performance