HNW - HNW: Appealing Multi-Asset Fixed Income CEF 10% Yield

2023-08-02 18:31:07 ET

Summary

- Pioneer Diversified High Income Fund is a fixed income CEF with a multi-asset approach, including high yield bonds, leveraged loans, ILS securities, EM bonds, and ABS securities.

- The fund has a low standard deviation and is currently trading at a large discount to NAV, which is expected to normalize when the Fed lowers rates.

- The fund has a dividend yield in excess of 10%, which is fully supported.

- The vehicle has moved to a more conservative stance in the past year by lowering its leverage ratio, but still contains a portfolio which is highly credit risky when judged by its rating profile.

Thesis

Pioneer Diversified High Income Fund, Inc. ( HNW ) is a fixed income CEF. The fund has a multi-asset approach, containing high yield bonds, leveraged loans, ILS securities, EM bonds and ABS securities. The CEF is on the smaller side at only $85 mm in assets, and has a classic build via a 30% leverage ratio.

Despite its credit risky portfolio that contains a significant amount of 'B' and 'CCC' credits, the fund has a low standard deviation of only 9%, translating into the portfolio manager doing a good job at selecting credits. The fund is currently trading with an extremely large discount to NAV of -14%, which we think will move back toward average historic levels when the Fed starts lowering rates next year.

We like this fund for its portfolio build, especially the ILS bucket. Catastrophe bonds have a low correlation to capital markets credit spreads, and that is a feature which is going to persist in our view.

Analytics

- AUM: $0.09 billion

- Sharpe Ratio: 0.21 (3Y)

- Std. Deviation: 9 (3Y)

- Yield: 10%

- Premium/Discount to NAV: -14%

- Z-Stat: -1

- Leverage Ratio: 30%

- Composition: Fixed Income - Bonds / Lev Loans / ILS / ABS

- Duration: 2.7 yrs

- Expense Ratio: 1.59%

Holdings

The fund holdings is what makes this CEF interesting. The vehicle has a multi-asset portfolio that spans U.S. high yield and emerging markets bonds:

Sectors (Fund Fact Sheet)

The largest exposure in this fund is represented by U.S. high yield, followed by event-linked bonds and emerging markets.

Event-linked bonds are a niche of the capital markets, and they represent what is colloquially referred to as ' catastrophe bonds ':

Catastrophe bonds, also called cat bonds, are an example of insurance securitization, creating risk-linked securities which transfer a specific set of risks (typically catastrophe and natural disaster risks) from an issuer or sponsor (ceding company) to capital market investors.

In this way, the investors take on the risks of a catastrophe loss or named peril event occurring in return for attractive rates of investment return. Should a qualifying catastrophe or named peril event occur, the investors will lose some or all of the principal they invested and the issuer (usually an insurance or reinsurance company, but sometimes a corporate or sovereign entity) will receive that money to cover their losses.

If there is a significant hurricane in Florida, or a very large earthquake in California, these securities might get impacted. Otherwise their credit spreads are not that driven by market risk-off events. This basically means they have very low correlations to the other sleeves in this CEF. Furthermore, many insurance linked securities are also floating rate, which translates into low durations and higher cash yielding levels when rates are high.

The fund also sports significant sleeves allocated to emerging market bonds and international high yield. The fund is granular, with only one holding above 2% of the portfolio:

Top Holdings (Fund Fact Sheet)

Granularity is important for these type of funds, especially in today's environment, where there is the possibility of higher default rates down the road, which can lead to actual impairments. A high level of granularity ensures no single name is able to bring the fund down.

The one large risk factor looming for this CEF is its lower quality collateral:

Ratings Matrix (Fund Fact Sheet)

We can see from the ratings table above that the name is extremely overweight 'B' and 'CCC' collateral, also sporting a large 'Not Rated' bucket. Poorly rated credits have a higher probability of default , and when a potential recession is around the corner that matters. The U.S 'High Yield' sector has high dividends for a reason - it is riskier than investment grade credit. The riskier the credit, the higher the dividend yield (all else equal).

Premium/Discount to NAV

The fund exposes a beta to interest rate levels from a fund discount perspective:

As interest rates got slashed following the Covid meltdown the CEF moved to a slight premium to net asset value. As the Fed started raising rates in 2022, the fund saw its premium move to a discount, a discount which clocks in at -13% today.

That is a very large figure that we expect will be partially reverted in 2024 when we think rates will eventually start coming down. A more normalized state of affairs for this fund is around an -8% discount to NAV, so there is a bit of a gain to be had here from that potential normalization, but pencil that in for next year.

Performance

The fund has had a robust performance in the past year:

When excluding its discount widening, HNW has performed in line with much better-viewed peers from PIMCO and New America. Long term though the fund does underwhelm:

We can see how on a 10-year lookback PDI does an outstanding job of creating value for shareholders, while HYB follows suit. So from that angle HNW is not a true buy and hold, but more of a cyclical play.

The fund manager was able to navigate the tricky 2022 waters via a high allocation to floating rate assets which kept duration low for the name. That is how we explain the low standard deviation for this fund as well.

Reducing Leverage via its Credit Facility

The CEF employs leverage via a credit facility:

The Trust employs leverage through a credit agreement. As of April 30, 2023, 30.3% of the Fund’s total managed assets were financed by leverage (or borrowed funds), compared with 32.7% of the Fund’s total managed assets financed by leverage at the start of the 12-month period on May 1, 2022. During the 12- month period, the Fund decreased the absolute amount of funds borrowed by a total of $12 million to $43 million as of April 30, Pioneer Diversified High Income Fund, Inc. |Annual Report | 4/30/23 9 2023. The percentage of the Fund’s managed assets financed by leverage decreased during the 12-month period due to the decrease in the amount of funds borrowed by the Fund. The interest rate on the Fund's leverage increased by 442 basis points from April 30, 2022 to April 30, 2023

Source: Semi-Annual Report

The fund has reduced its borrowings under the credit facility and has reduced the CEF leverage. This is a good set-up for a more volatile environment, and we have seen several CEF managers move to a more prudent stance via leverage reductions.

There are generally two ways for fixed income CEFs to obtain leverage - either via preferred share issuance or an asset backed credit facility. HNW does it via a credit facility.

Distributions

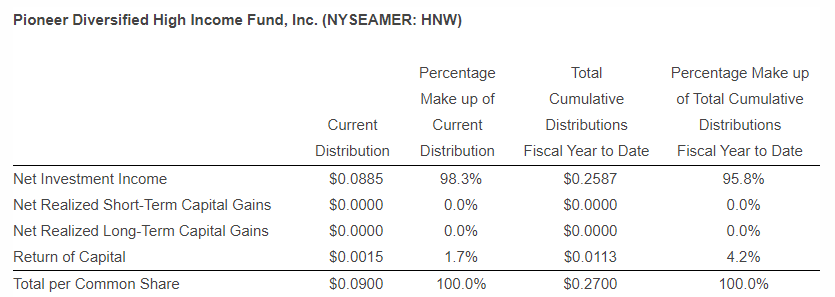

The fund is covering virtually all of its distributions as of the July 2023 Section 19 Notice :

{kind=link}

In the past there have been certain periods in time where the CEF used a significant amount of ROC, but in today's high interest rate environment the fund does not have any issues with its distribution.

Conclusion

HNW is a fixed income CEF. The fund has a multi-asset approach, containing U.S. high yield, ILS bonds and EM debt. The fund has a large floating rate asset sleeve that accounts for its short duration and the increase in net distributable cash in the past year. The fund has a 30-day SEC yield in excess of 10%, which is 96% supported via net investment income cash. We like this fund because it is trading at close to historic discount levels (currently -14%) and its holdings composition (ILS asset class has a low correlation to the other sleeves). We are a Buy here for HNW via a dollar-cost-average approach over several weeks.

For further details see:

HNW: Appealing Multi-Asset Fixed Income CEF, 10% Yield