HCHDF - Hochschild Mining: Limited Margin Of Safety At Current Levels

2023-12-19 12:43:25 ET

Summary

- Hochschild Mining's Q3 production declined by 14% compared to the previous year, with lower production across all assets.

- The company's costs and margins haven't been anything to write home about either, with all-in sustaining costs soaring, and guidance increased to $1,535/oz at the midpoint.

- In this update, we'll look at the Q3 results, recent developments, and whether the stock looks worthy of investment at current levels.

Just over four months ago, I wrote on Hochschild Mining (HCHDF), noting that while the stock was becoming much more attractively valued, it was still a high-risk, high-reward bet given that we didn't have certainty yet on its flagship asset, Inmaculada. Since then, Hochschild Mining ("Hochschild") has received its MEIA covering a larger area (~260 hectares), is on track to first production within four months at Mara Rosa, and has a new management team in place after what's been a disappointing few years of missed guidance for the company. In this update we'll look at the Q3 results, recent developments, and whether the stock looks worthy of investment at current levels.

Hochschild Operations - Company Website

{kind=link}

Q3 Production

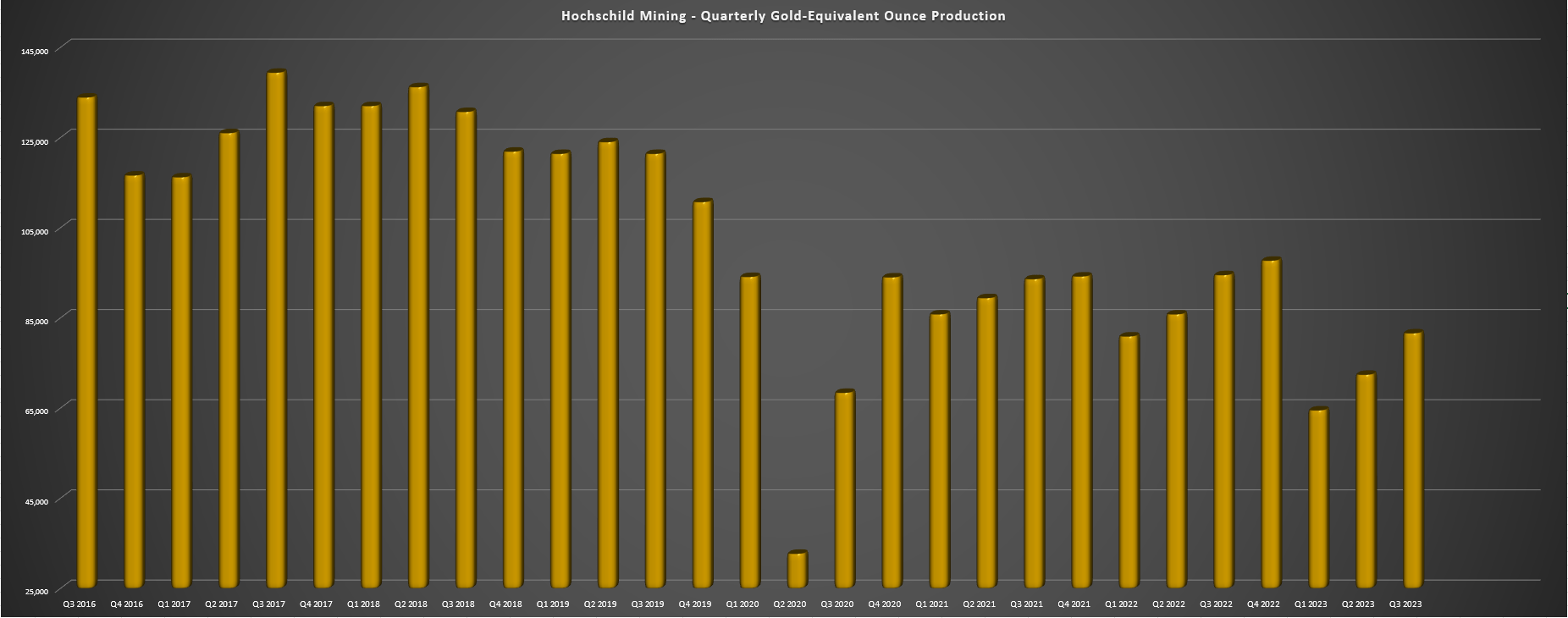

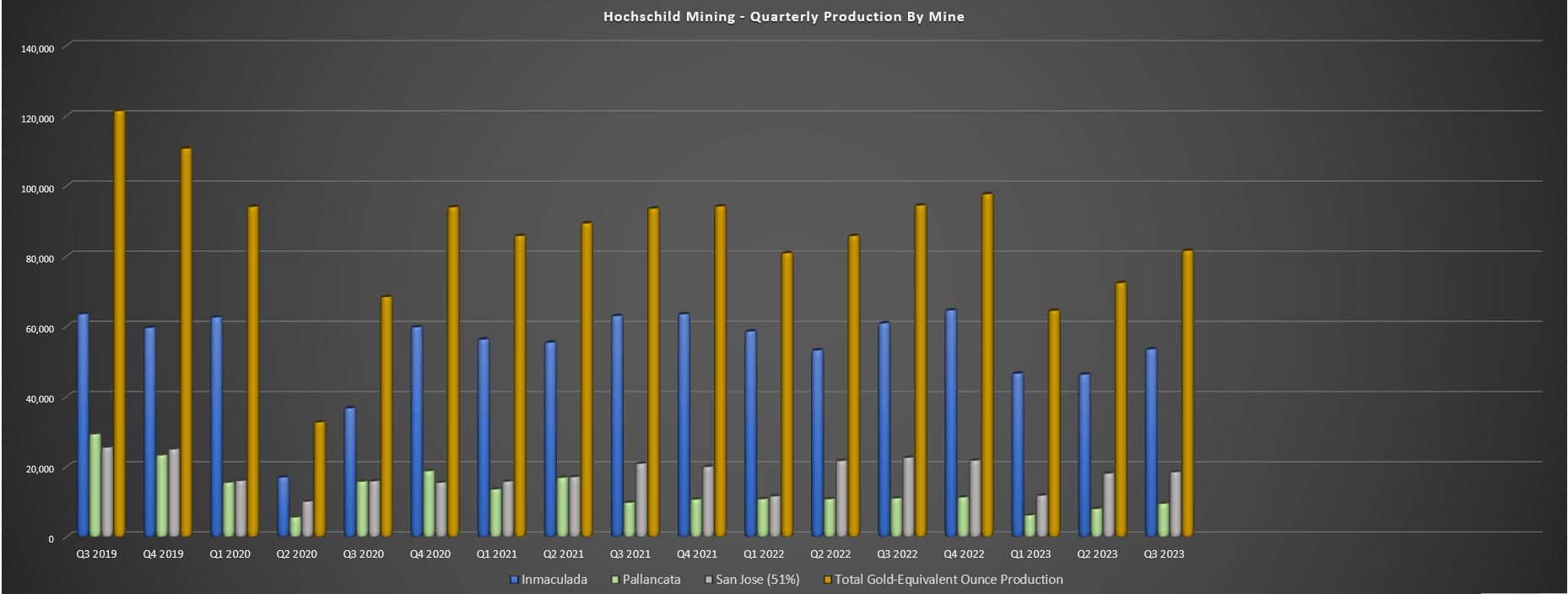

Hochschild Mining released its Q3 results in late October, reporting quarterly production of ~81,600 gold-equivalent ounces [GEOs]. This represented a ~14% decline from the year-ago period, with lower production across the board. As the chart below highlights, the most significant drop in production volume came from Pallancata (~53,500 GEOs vs. ~60,900 GEOs), while San Jose's attributable production slipped from ~22,600 GEOs to ~18,500 GEOs, and Pallancata's production also fell on the back of lower gold and silver production to just ~9,500 GEOs. Unfortunately, the year-over-year production declines will continue into Q4, with Pallancata set to head into care & maintenance, and lapping ~97,700 GEOs compared to the year-ago period.

Hochschild - Quarterly GEO Production - Company Filings, Author's Chart Hochschild - Quarterly GEO Production by Mine - Company Filings, Author's Chart

{kind=link}

{kind=link}

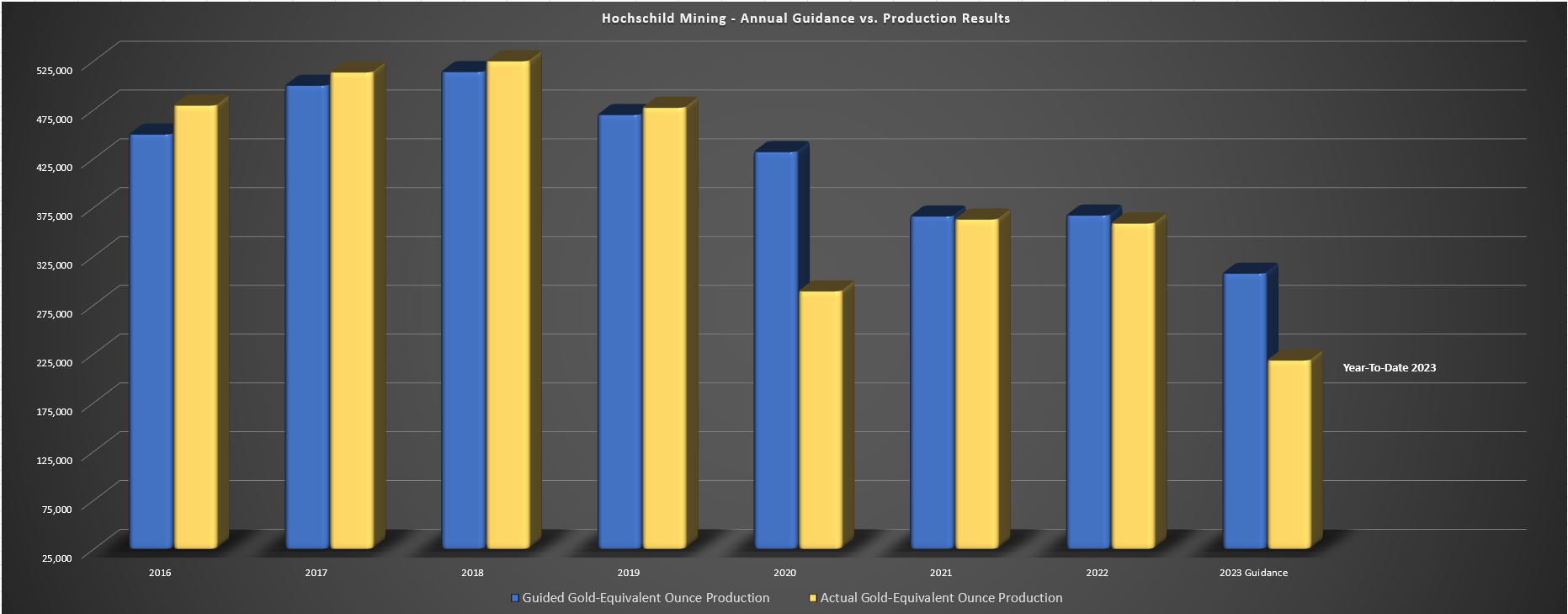

Looking at the company's annual guidance, the production midpoint was initially set at ~307,000 GEOs (since downgraded to ~296,000 GEOs at the midpoint), and Hochschild's year-to-date production of ~218,500 GEOs is sitting at just 71% of this guidance. Hence, this will mark the fourth year of missed production guidance relative to the midpoint for the company, a disappointing trend after several years of consecutive beats pre-pandemic. In fairness to the company, the lower production this year can be attributed to the delayed receipt of the Inmaculada MEIA, which negatively affected mine development. However, a more conservative guide would have been appropriate given that its largest asset had permitting uncertainty.

Hochschild - Initial Production Guidance vs. Actual & YTD 2023 Results - Company Filings, Author's Chart

{kind=link}

Costs & Margins

Moving over to costs and margins, there wasn't much to write home about here, with company-wide all-in sustaining costs [AISC] soaring to $1,572/oz in H1 2023, and Pallancata's AISC jumping nearly 20% from $1,074/oz to $1,272/oz. The higher costs at Pallancata can be attributed to lower production volumes (lower throughput, which was offset by higher grades). At Pallancata, costs remained elevated at $31.70 per silver-equivalent ounce, down from $32.30/oz, but still well above the company's average realized silver price of $23.60/oz. Finally, San Jose's costs have continued to creep higher, coming in at $21.50/oz (H1 2022: $21.20/oz), leaving little room for free cash flow generation despite pushing significantly more tonnes through the plant and the benefit of currency devaluation in Argentina.

Hochschild Mining - AISC by Mine (Annual & H1 2023) - Company Filings, Author's Chart

{kind=link}

Looking at annual costs, the trend has been no better. As the chart below shows, all-in sustaining costs have soared over 50% from 2018 levels compared to the updated guidance midpoint of $1,535/oz in 2023, wiping out most of the benefit from a higher gold price. And although the lower-cost Mara Rosa Project will come online in 2024 and help to pull down company-wide costs, the benefits won't be realized immediately from a margin standpoint. This is because Inmaculada's costs will remain elevated due to $45 million in deferred capex, and I would expect minimal free cash flow generation next year with a relatively high capex budget of ~$180 million at the high end in 2024 even with Mara Rosa construction complete.

Hochschild Mining - Annual AISC & FY2023 Guidance - Company Filings, Author's Chart

{kind=link}

Recent Developments

So, what's the good news?

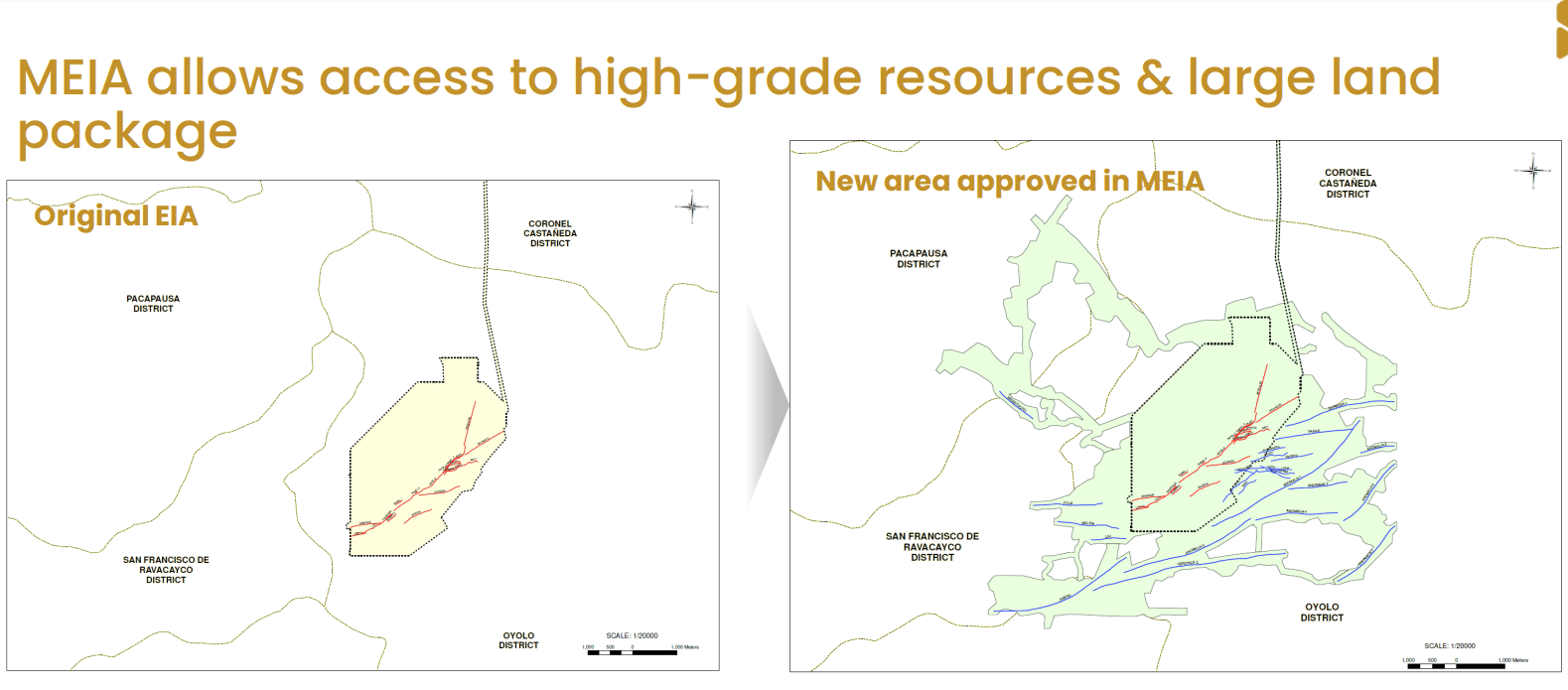

Beginning with Inmaculada, the MEIA is finally in hand after several delays that affected Hochschild's share-price performance, and it covers a larger area of 262 hectares, providing access to high-grade resources that previously weren't able to be extracted, and giving investors visibility into future production with it granted for an additional 20 years. This is certainly a positive development given that this is the company's flagship asset, and while costs will come in above $1,600/oz next year, we should see a significant improvement in costs in 2025 once higher capex rolls off that has been pushed into 2024.

Recently Approved MEIA Inmaculada - Company Website

{kind=link}

The second positive development is that Mara Rosa's construction is at 98% and nearing the finish line, with the company reiterating its plans for an H1 2024 first gold pour. The company noted that pre-stripping has begun with ~1.45 million tonnes of ore moved to date, and that all main project equipment is on site, de-risking the H1 2024 start-up plans. For those unfamiliar, Mara Rosa may be relatively small as far as gold projects go at ~90,000 ounces per annum, but it's a lower-cost asset with sub $1,200/oz AISC over its life of mine even adjusting for inflationary pressures and it should help to offset higher costs at San Jose where grades have been in steady decline.

2024 Guidance - Company Website

{kind=link}

As noted by Hochschild in its early release of 2024 guidance, it will be a higher cost year once again for Inmaculada and San Jose, but Mara Rosa will deliver ~88,000 ounces at sub $1,150/oz AISC, helping to keep company-wide costs under $1,600/oz. And as noted, while 2024 will be a very high cost year because of significant sustaining capital spend, we will see improved costs in 2025 and 2026. In addition, while I was less inclined to believe guidance provided by Hochschild in 2023 because of its track record of consistently missing, there is a new team at the helm, with the former CEO stepping down and being replaced by Eduardo Landin, who served as COO of Hochschild from March 2013 to his appointment to CEO. Meanwhile, Rodrigo Nunes has been appointed as COO from Director of Technical Services previously, and prior to that VP of Mining for Optimize Group, an engineering company based out of Canada.

To summarize, the positives have certainly outweighed the negatives and Hochschild is on a path to improving margins with higher production levels post-2024. That said, the key will be to extend mine life at San Jose and the timely receipt of permits at Royropata if the company hopes to maintain a 350,000+ GEO production profile post-2026. Let's look at the valuation and see how it stacks up after the stock's recent outperformance.

Valuation

Based on ~515 million shares and a share price of US$1.34, Hochschild trades at a market cap of ~$690 million and an enterprise value of ~$950 million, a significant departure from its previous market cap of ~$1.8 billion at its 2020 highs. And while the stock might appear significantly undervalued given that it's over 60% from its highs with a new gold project in hand, a lot has changed since 2020, and certainly from a cost standpoint. In fact, while we've seen limited upside in gold/silver prices vs. their 2020 highs, Hochschild's all-in sustaining costs have soared from ~$1,030/oz in H1 2020 to guidance of $1,535/oz at the mid-point this year. Hence, the share price has slid in line with the margin compression we've seen, never mind the fact that there's been a greater appetite for Tier-1 jurisdiction producers given the negative surprises we've seen in less favorable jurisdictions, with First Quantum's (FQVLF) recent negative surprise at Cobre Panama being one example.

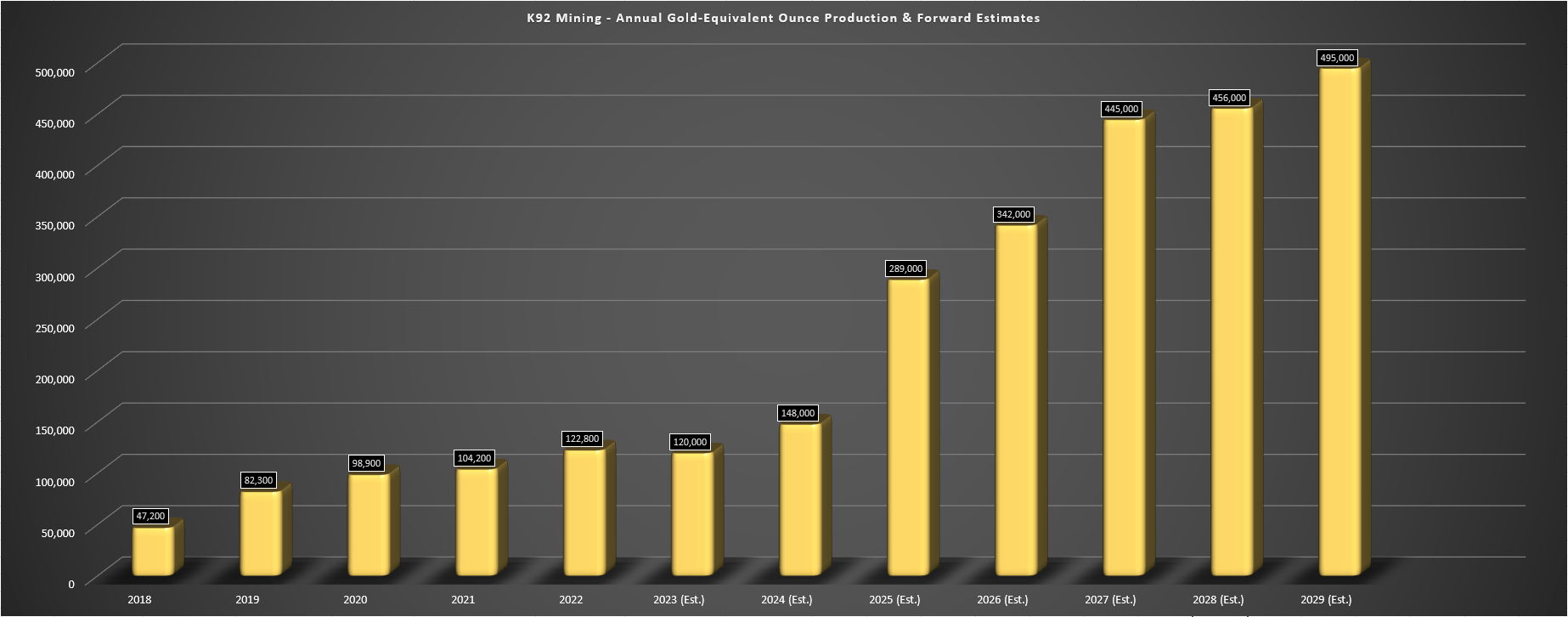

On a positive note, Hochschild's 2023 and 2024 costs will remain elevated and well above the industry average (~$1,400/oz), but we should see costs improve by 2025 back in line with the industry average, and Pallancata may be offline, but still has a future, with the new Royropata discovery next door. This should transform Hochschild into a ~360,000 GEO per annum producer in 2025 at ~$1,400/oz AISC, a significant improvement from updated guidance of ~296 GEOs at ~$1,540/oz this year. That being said, I don't see the current enterprise value of ~$950 million being much of a value disconnect for an average cost producer (2025) of this scale in Tier-2 ranked jurisdictions, especially when producers set to have larger scale with double the margins are trading at similar valuations. One example is K92 Mining (KNTNF) that's expected to produce ~340,000 GEOs in 2026 at ~$1,200/oz AISC margins using a $2,000/oz gold price assumption, translating to higher production at 100% higher margins vs. Hochschild.

K92 Mining Annual GEO Production & Estimated Production Profile - Company Filings, Author's Chart & Estimates

{kind=link}

Looking at other examples within the sector, Argonaut Gold (ARNGF) trades at an enterprise value of barely $450 million as a future 300,000-ounce producer (2026) in Tier-1 jurisdictions, which is half the enterprise value of Hochschild Mining but in better jurisdictions and with a similar cost profile. So, although Hochschild has been de-risked with the MEIA in hand and the Royropata discovery certainly helps towards Pallancata's future and turning this asset back on in 2027 potentially, I think there are far more attractive bets elsewhere in the sector, with Argonaut Gold and K92 Mining being two names that stand out as having the best reward/risk profiles over the next two years.

Summary

Hochschild Mining has recovered sharply off its 2022 lows and outperformed several of its silver peers, given that many like First Majestic ( AG ) and Endeavour Silver ( EXK ) were priced for near perfection and have diluted significantly in the period. That said, the stock's relative value is much less compelling today, and this is certainly the case when 2024 is expected to be another high-cost year, and the company has less exposure to gold price upside with 150,000 ounces of gold hedged in 2025, 2026, and 2027 at prices ranging from $2,117/oz to $2,206/oz. Finally, although Mara Rosa fills in the gap from Pallancata, the ability to extend mine life past 2026 at the higher-cost San Jose Mine is not clear, suggesting Royropata may not offer much growth if it simply offsets lost production from San Jose.

To summarize, I see far more attractive bets elsewhere in the sector, and I would view any rallies above US$1.56 before February as an opportunity to book some profits.

For further details see:

Hochschild Mining: Limited Margin Of Safety At Current Levels