HOFT - Hooker Furnishings: Poor Quarterly Results And High Valuation Make It Unattractive

2023-09-28 12:28:07 ET

Summary

- HOFT has reported negative sales growth and declining operating margins in Q2 FY24.

- The company's net income has also significantly decreased compared to the previous year.

- Technical analysis suggests a bearish price action, and the company's high valuation and unfavorable market conditions further indicate potential struggles in the future.

Hooker Furnishings ( HOFT ) manufactures and imports residential household and contract furniture. HOFT has been struggling due to the housing market slowdown and demand softness, and the Q2 FY24 clearly shows it. HOFT recently announced its Q2 FY24 results with negative sales growth, and its operating margin was under pressure. I don’t think it would be worth staying invested in this company as it might continue struggling in the second half of FY24. In addition, its valuation, technical chart, and future outlook look unfavorable. Hence, I assign a sell rating on HOFT.

Financial Analysis

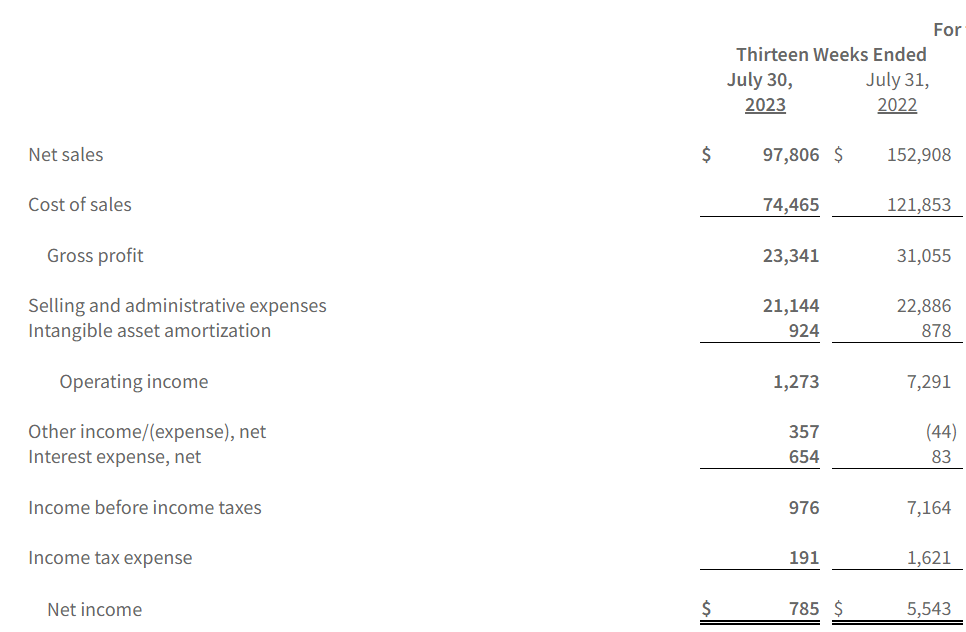

HOFT recently posted its Q2 FY24 results . The net sales for Q2 FY24 were $97 million, a decline of 36% compared to Q2 FY23. All three segments underperformed, which led to a decline in sales. The Hooker Branded, Home Meridian, and Domestic Upholstery segments sales declined by 34.3%, 51%, and 19.4% in Q2 FY24 compared to Q2 FY23. All the segments were affected by softer home furnishings demand and reduced unit volume. Its operating income margin for Q2 FY24 was 1.3%, which was 4.7% in Q2 FY23. I believe the operating margin was adversely affected by increased discounting and labor expenses.

{kind=link}

Its net income in Q2 FY24 was less than a million, which was $5.5 million in Q2 FY23. Honestly, there isn't much to say here. The numbers look terrible, and the company struggled in every area. The margins were under pressure, profitability declined, and the sales were down significantly. Looking at the market conditions, I don't see them recovering in the second half of FY24. The company's success is very much dependent on the housing market, and the current situation is unfavorable. The housing market is facing a slowdown, and the mortgage rates are the highest in 20 years. Moreover, its retail clients are clearing off their excess inventory. Therefore, I think the demand for its products might stay low through FY24. Hence, looking at the softness in demand and unfavorable market conditions, I think the company might continue to struggle in the second half of FY24. Hence, I would advise investors to be very careful, as disappointing results in the upcoming quarters might adversely affect its share price.

Technical Analysis

{kind=link}

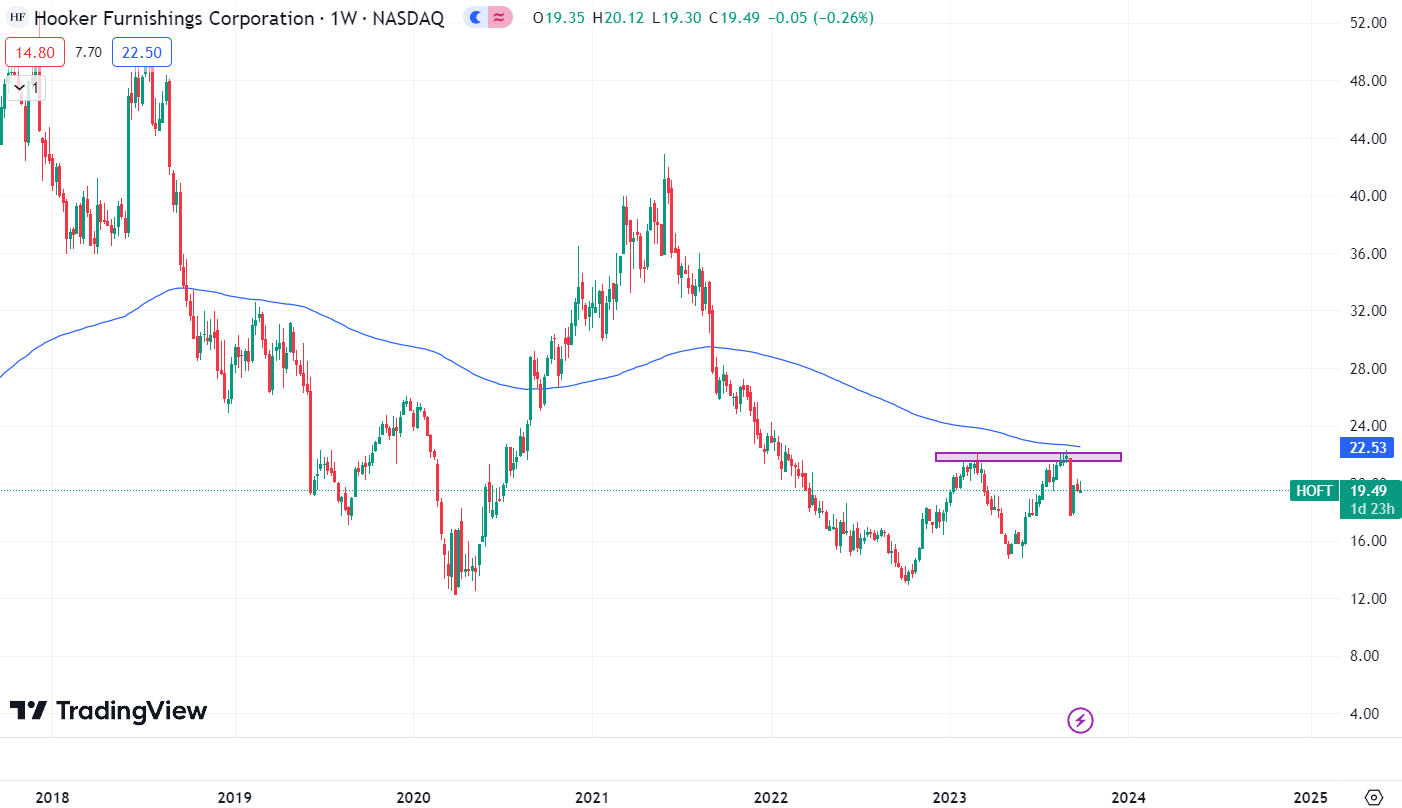

HOFT is trading at $19.5. At one point, the stock was trading at the $52.7 level, but now it is trading around $19.5. Its price action over the last couple of years has been horrible, and the recent price action also doesn’t look too good. Recently, the stock price faced a rejection from its 200 ema, which shows weakness. In addition, the stock price reversed from the resistance zone of $22 last time the price touched the $22 level in February 2023, and it fell about 30%. So, the price action here is quite bearish, and I see a downfall of about 20% from the current level. Hence, I would suggest ignoring this stock due to bearish price action.

Should One Invest In HOFT?

First, look at HOFT’s valuation . It is trading at a P/E [FWD] ratio of 23.29x, which is higher than its five-year average of 12.11x and the sector median of 13.91x. HOFT has an EV / EBIT [FWD] ratio of 18.46x, which is higher than the sector ratio of 12.86x. After seeing its growth rate, I don’t think it deserves to trade at a higher valuation, and the future outlook is also not positive, so I think the future growth may not be able to support the high valuations and if we compare it to some of its peers like Lovesac ( LOVE ) and Flexsteel ( FLXS ), they are trading at a lower valuation, and LOVE and FLXS have a P/E [FWD] ratio of 8.99x and 11.3x. However, the whole industry is struggling due to macroeconomic headwinds like the slow housing market, so I would not suggest investing in any of these companies. Talking about HOFT with a high valuation, demand softness, housing market slowdown, declining operating margin, and revenue growth, I think staying invested in the company wouldn’t be wise. As I think it might continue to underperform in the second half of FY24, and its share price might be adversely affected due to the underperformance. The technical chart is already showing weakness and early signs of correction. Hence, considering all the factors, I assign a sell rating on HOFT.

Risk

Their top five customers accounted for over 22% of their fiscal 2023 consolidated sales, while one customer accounted for about 6% of their total sales. Twenty percent of their total accounts receivable are concentrated in their top five clients. Their financial condition and liquidity would be immediately and materially affected if these receivables were uncollectible. The sales, financial status, and liquidity may all suffer if one or more of these clients leave. The loss of numerous key clients due to corporate mergers, product placement losses, failures, or other reasons could negatively impact sales, the financial situation, and liquidity, and the lost business may be difficult or impossible to replace as a result.

Bottom Line

HOFT has been struggling due to the housing market slowdown and demand softness for its products, and the quarterly results showcased how much the company has been struggling with its operating margins and how profitability is declining. I expect them to continue to struggle in the second half of FY24. So, I don’t think it would be worth staying invested in the company as I don’t see them providing any returns in the near future. In addition, the current valuation is quite high. Hence, I assign a sell rating on HOFT.

For further details see:

Hooker Furnishings: Poor Quarterly Results And High Valuation Make It Unattractive