HRIBF - Horiba: Wonderful Japanese Company At A Very Attractive Price

2024-01-12 11:27:00 ET

Summary

- Horiba is likely undervalued due to it being under followed, and offers a rare combination of a quality business at an attractive price.

- The company has high market share in specialized devices in various industries, including automotive, process & environmental, medical, semiconductor, and scientific.

- While there are risks in the automotive segment due to the rise of electric vehicles, Horiba is investing in new products for testing and evaluation of new mobility technologies.

In general the "Life Sciences Tools and Services" industry is one populated with high quality companies possessing strong competitive moats. There are several reasons for this, including high customer switching costs, as biotech and pharma companies don't want to risk their experiments and certifications because they switched to a different brand of equipment. Another reason is that these are advanced devices that require significant R&D and are well protected by patents and trade secrets. Customers are willing to pay more for brands that give them the peace of mind that lab equipment is not going to jeopardize their operations or research.

One example we have covered a few times is Agilent Technologies ( A ), most recently in this article arguing the company is currently reasonably valued and expected to return to growth soon. Together with peer Danaher ( DHR ), they have easily outperformed the S&P 500 index ( SPY ) during the past ten years, while Waters Corp ( WAT ) has delivered very similar returns. The problem with this group of companies is that they usually oscillate between being fairly valued and over valued, it is indeed a rare occasion when an investor can purchase shares in one of these companies at a significant discount.

That is why we are finding Horiba ( OTCPK:HRIBF ) so interesting, even if it is located in another country and only part of its business is focused on "Life Sciences Tools and Services". In fact, on Seeking Alpha, it is classified as part of the "Electronic Equipment and Instruments" industry, since that is the larger part of its business. Still, Horiba has a growing "Life Sciences" segment, and the other segments are performing relatively well too.

What really sets it apart is the valuation, as Horiba is trading at much lower multiples. We believe this is in large part due to the company being based in Japan, a market many investors have given up on after decades of under performance. Even Bloomberg recently described it as the "land where optimistic stock bets go to die". While Horiba has outperformed the iShares MSCI Japan ETF ( EWJ ) by a wide margin, it still has underperformed the S&P 500 index by a significant margin the past ten years.

Company Overview

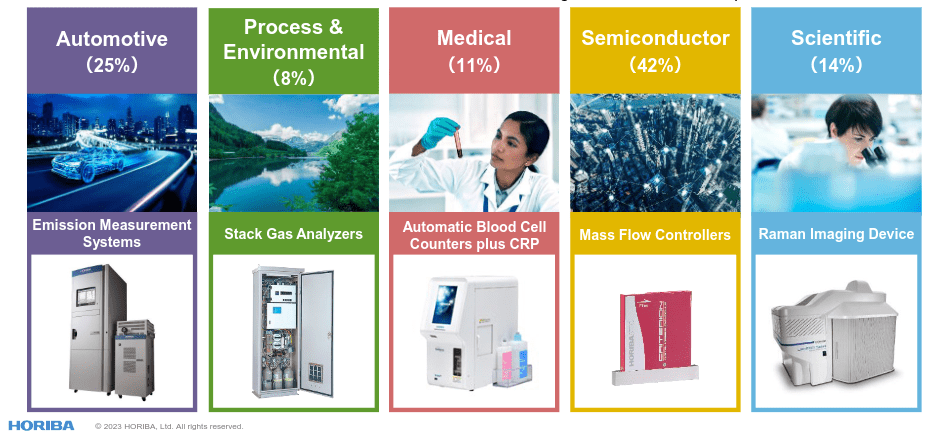

The company has five business segments, three of which are similar to the companies we discussed in the section above. The other two segments are also attractive, but tend to have some cyclicality, these being the Automotive segment, and the Semiconductor segment. The five business segments are Automotive, Process & Environmental, Medical, Semiconductor, and Scientific. The automotive segment also has a long-term risk in the electrification of transportation that we will discuss in more detail later.

{kind=link}

Horiba has very high market share for some specialized devices in some of these industries. For example, in the Automotive segment, its Emission measurement systems have approximately 80% global market share. In the Process & Environmental, its Stack gas analyzers have around 50% market share in Japan. In the Medical Diagnostic segment its Hematology analyzers have around 7% global market share. The biggest segment is Semiconductor, where the company has products like Mass flow controllers where it has an impressive ~60% global market share, and Chemical concentration monitors with an even higher share of ~80%. Finally, the Scientific segment offers products like Raman spectrometers, where the company commands a ~30% global market share, and pH meters for water quality analysis and examination systems where the company has a ~50% market share in Japan.

Emission Headwinds and Tailwinds

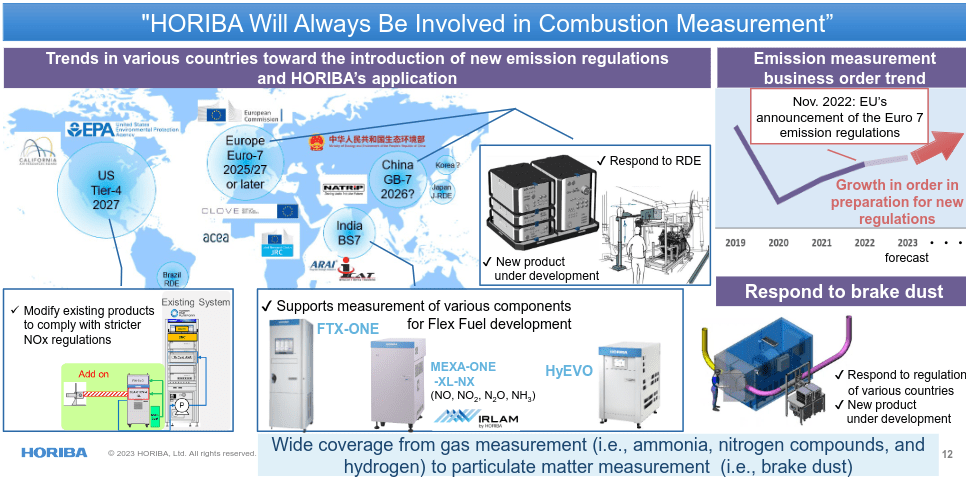

We believe the least attractive business for the company is the Automotive segment, as EVs will continue to increase their market share. This is important, as this segment represents roughly a quarter of the company's revenue.

Still, we believe the segment could actually grow before it starts declining, and might even make a successful transition into the new era. The medium-term tailwinds include increased regulations on car emissions, which means vehicle manufacturers will have to invest in more emission measurements equipment. To address this fear, the company even includes a slide in its investor presentation explaining the long-term outlook. At the same time, the company is already working on future products to support testing of next generation mobility technologies, as seen in the paragraph below from their annual report.

We are also actively developing our Engineering Consultancy & Testing (ECT) business, which supports development of next-generation mobility technologies for applications such as electrified vehicles, autonomous driving, functional safety, and cybersecurity.

{kind=link}

M&A

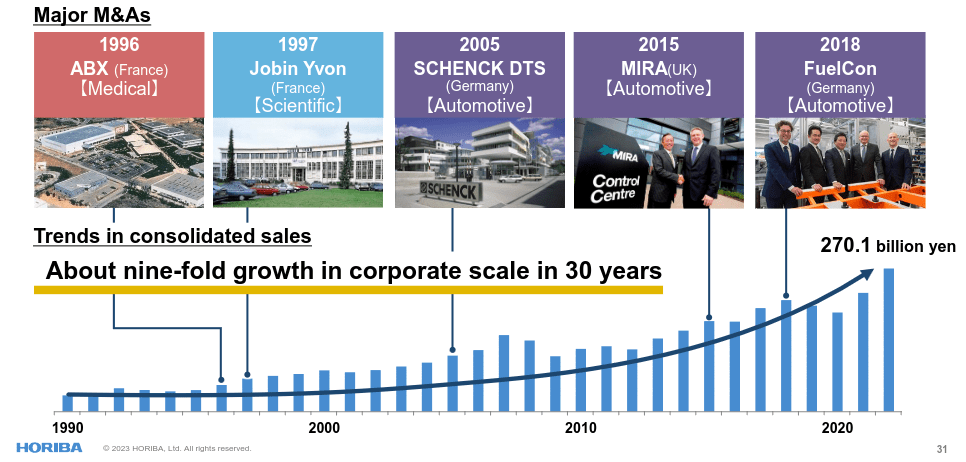

Horiba has a policy of retaining around 70% of profits to reinvest in organic and inorganic growth opportunities. It has made several important acquisitions over time, which have created the company that it is today. The most important ones have been of European companies, which have added nice diversification to its Japanese operations.

{kind=link}

Financials

Horiba has attractive profit margins, and has been showing operating leverage as revenues increase, with its operating and net profit margins in general trending up over the last ten years.

Despite having a very conservative balance sheet, the company has been able to deliver attractive returns on equity, which have also been trending up in recent years, but with some cyclicality as well.

Growth

It is easier to see the company's cyclicality looking at its trailing twelve months revenue chart for the last ten years. We can clearly see periods of rapid expansion, and other periods where growth stalls or even slightly declines.

The average quarterly year-over-year growth has been a relatively modest 4.4%, but it would probably have been a little bit higher if the Japanese Yen ( FXY ), other Asian currencies, and the Euro ( FXE ) had not depreciated so much against the dollar these past ten years. The company only gets about 16% of its revenue from the 'Americas' region.

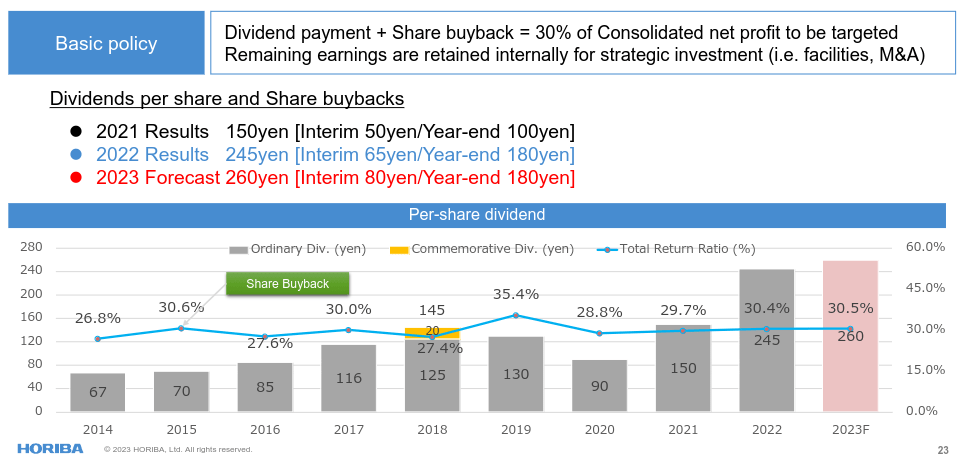

Dividend

The company has a decent dividend yield of ~2.3%, with the company paying an interim dividend and a year-end dividend. Its policy is to return 30% of earnings to shareholders when considering dividends and buy backs combined.

This means there is some variability, and some times the dividend will decrease if there is a dip in earnings. Still, it has grown nicely from 67 Yen per share in 2014 to 260 Yen for 2023. This means the dividend has been growing at ~16% CAGR, and given the low payout ratio, it has room to keep growing in the future.

{kind=link}

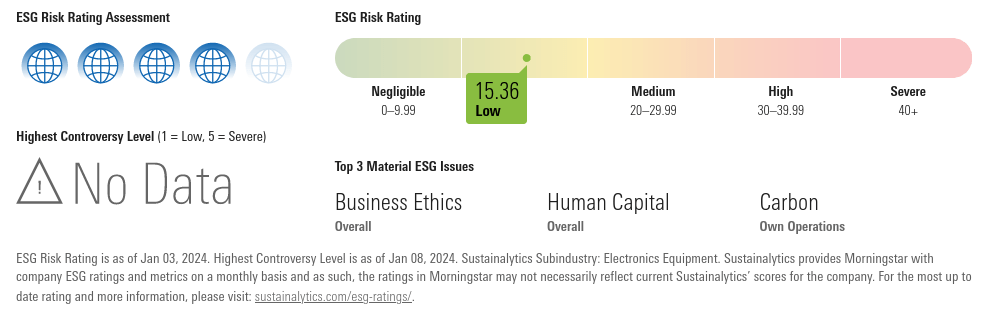

ESG

One area where we believe the company can do a better job is improving its ESG score. According to CDP , it has a 'C' grade related to its Climate Change mitigation efforts, and also a 'C' grade with respect to its Water Use.

| Company |

| Evaluation Type |

| Score |

| HORIBA, Ltd. |

| Climate Change 2022 |

| C |

| HORIBA, Ltd. |

| Water Security 2022 |

| C |

Morningstar's Sustainalytics give the company a 4/5 grade, and it shows no major controversies for the company.

{kind=link}

Balance Sheet

It is an understatement to say that Horiba has a strong balance sheet. It actually has a net cash position that is over 10% of the market cap. With its strong profitability and free cash flow generation, high earnings retention, and massive liquidity, the company is in an excellent position to take advantage should attractive M&A opportunities present themselves in the future.

Unsurprisingly, the company has an excellent credit rating. It has an “A” rating from Rating and Investment Information, Inc. and “A+” from Japan Credit Rating Agency, Ltd.

Valuation

On most valuation metrics the company is trading at a massive discount to the sector median. For example, the price/earnings ratio of ~12x is less than half the ~27x sector median. Similarly, the company is trading at less than half the sector median for EV/EBITDA, P/B, EV/EBIT, etc.

At current prices the company offers an earnings yield of ~8%, if the valuation multiples remain unchanged, and it grows earnings at a low GDP-like growth rate of 2-3%, it can easily offer shareholders double-digit total returns.

SeekingAlpha

Risks

The biggest risk we see for the company is that in the long-term it might lose revenue in the emissions equipment business, as companies transition to EVs. Still, this is likely to play over a long period of time, and Horiba is already investing in new products tailored for testing and evaluation of new mobility technologies.

The significant cash and short-term investments the company holds, its geographic and business diversification, and free cash flow generation capacity significantly reduce risks.

Conclusion

Horiba is a high-quality company that is not very well known by investors outside of Japan. This might be one of the reasons it is trading at a significant discount to valuation multiples in its sector. There is probably a country discount as well, and some investors might be a little worried about the Automotive segment. The Semiconductor segment also tends to experience high cyclicality. Still, we believe the company is being significantly under valued by investors, and it offers a rare combination of a quality business at a very attractive price. As such, we are rating Horiba as a 'Strong Buy'.

For further details see:

Horiba: Wonderful Japanese Company At A Very Attractive Price