CUKPF - Hotel REITs: Dividends Are Back

Summary

- Despite lingering recession concerns and recent travel disruptions, Hotel REITs have been among the better-performing sectors over the past year, buoyed by steady post-pandemic operating improvement fueling long-awaited dividend resumptions.

- Several years of pent-up leisure demand helped to offset a sluggish business and group travel recovery. Hotel revenues eclipsed record highs in 2022, but with wide dispersion between markets and segments.

- The final months of 2022 saw a mild softening in demand- worsened by holiday travel nightmares- but recent high-frequency data and REIT updates show surprisingly solid momentum in early 2023.

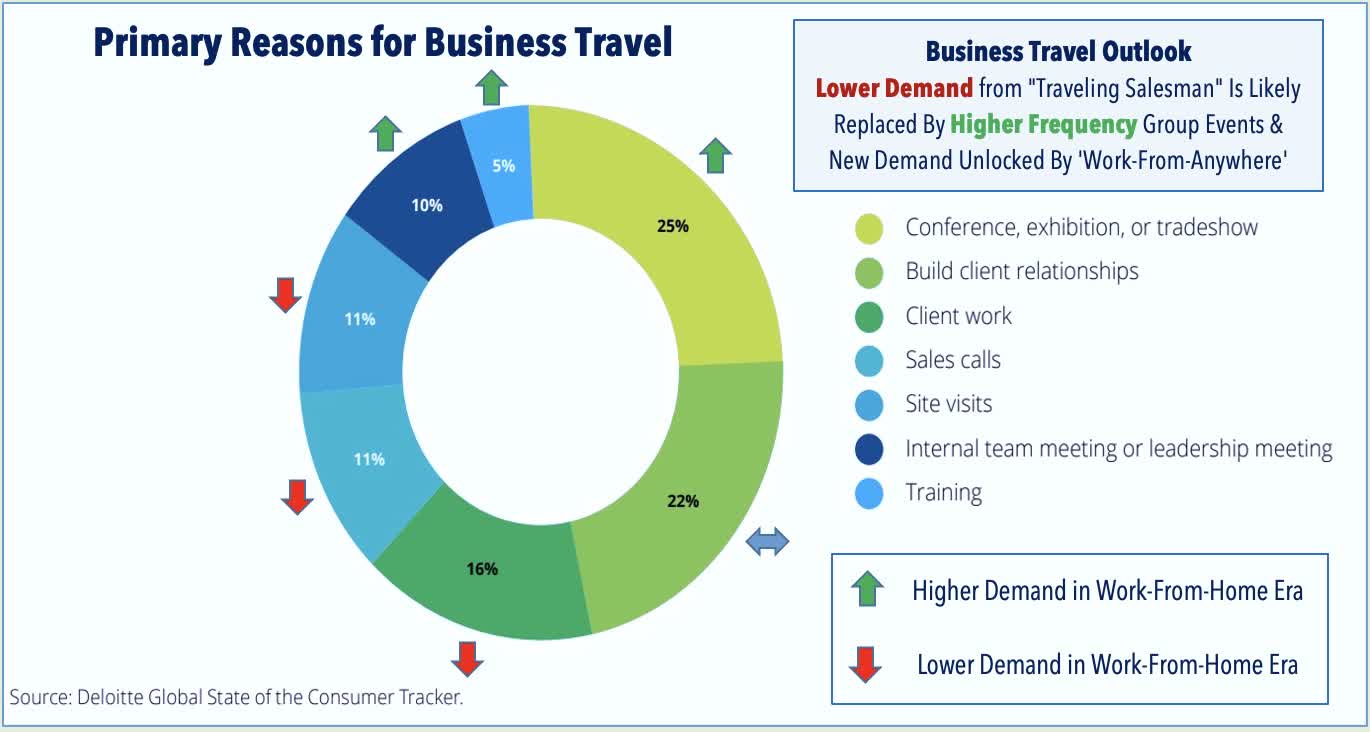

- Remote work is changing the complexion of business demand. The "traveling salesman" visits are being replaced by more frequent group events while "work-from-anywhere" hybrid work-leisure trips are skewing demand towards more "destination" segments.

- We see the best value in the higher-margin limited-service segment and in select full-service names with a heavy "destination" market focus, but also see compelling value in high-yielding preferred stocks.

REIT Rankings: Hotels

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on January 22nd.

{kind=link}

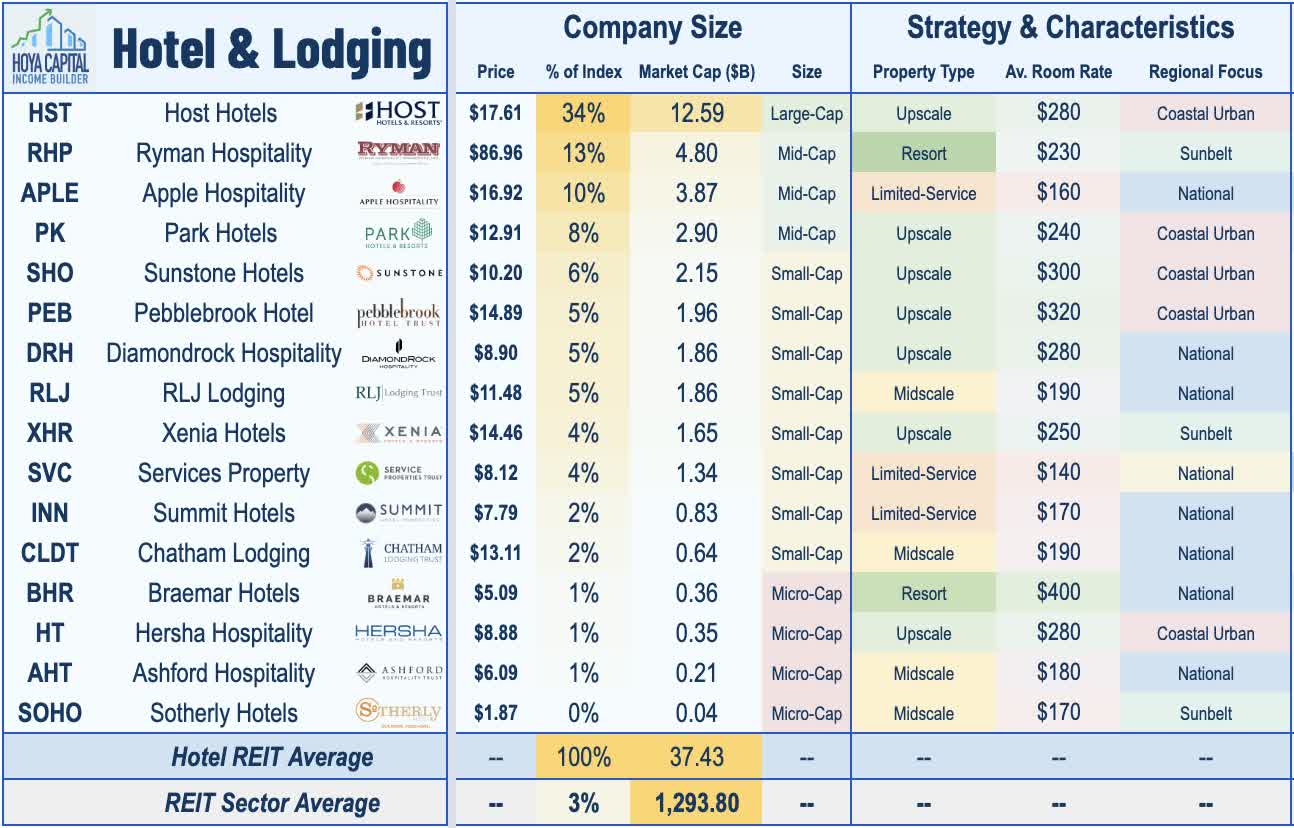

Hotel REITs - alongside the broader U.S. hospitality industry - have delivered surprisingly solid operating performance over the past six months in the face of numerous headwinds, allowing these REITs to shore up their balance sheets and restore dividend distributions after a harrowing pandemic plunge that pushed the sector to the absolute brink. Total hotel revenues in the U.S. eclipsed record highs in 2022 - but with a notably wide dispersion in performance between markets and segments - as several years of pent-up leisure demand helped to overcome a sluggish business and group travel recovery. Within the Hoya Capital Hotel REIT Index , we track the sixteen largest hotel REITs, which account for roughly $40 billion in market value.

{kind=link}

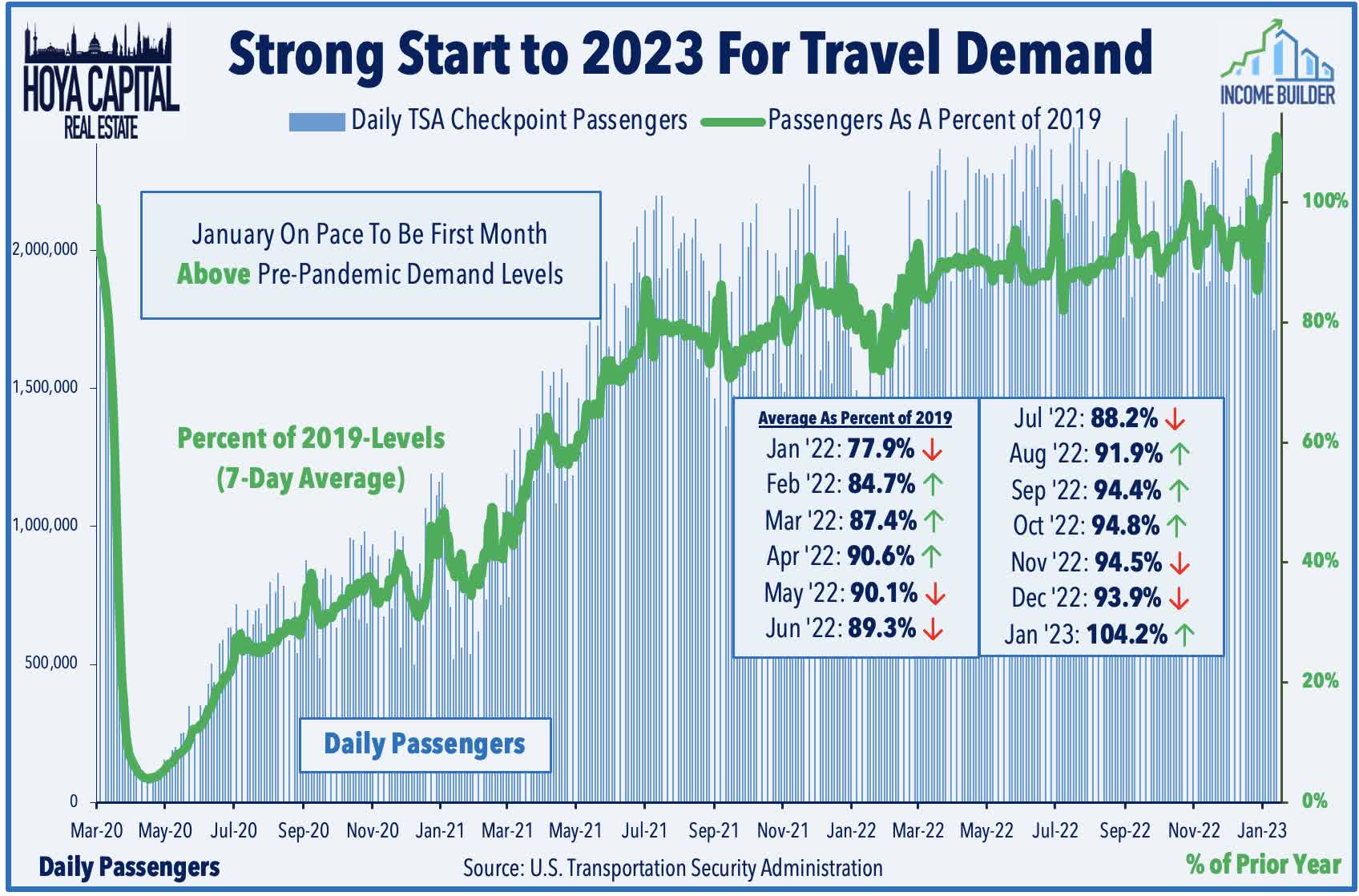

Few industries were harder hit by the global pandemic than leisure and hospitality, which faced historic declines in occupancy rates and revenues as travel restrictions and health concerns kept consumers at home. As illustrated through TSA Checkpoint travel volume data - a key high-frequency indicator that we've tracked throughout the pandemic - travel demand in the U.S. has steadily recovered since bottoming in mid-2020, pushing through periodic interruptions from new COVID variants, major weather events, surging fuel prices, vaccine mandates for international travel, and broader economic headwinds. Travel demand recovered to within 10% of pre-pandemic levels in the back half of 2022 as several years of pent-up leisure demand helped to offset a sluggish business and group travel recovery - and pushed above 100% for the first time in early January.

{kind=link}

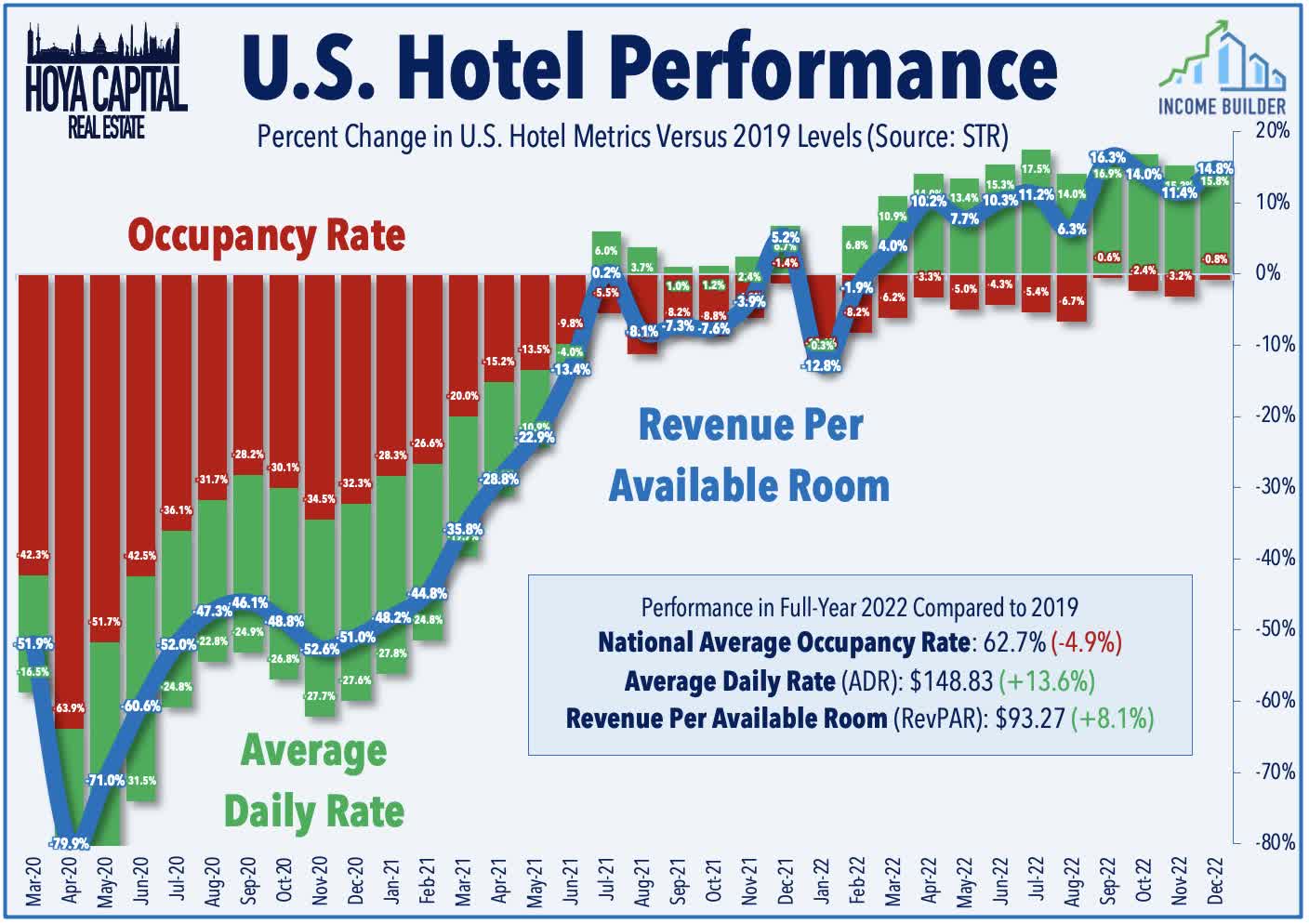

While total passenger throughput - and hotel occupancy - remained slightly below pre-pandemic levels throughout 2022, the U.S. hotel industry nonetheless enjoyed an impressive year of operating performance, recording the highest Average Daily Rate ("ADR") and Revenue Per Available Room (RevPAR) for any year on record, according to 2022 data from STR . Critically, hotel operators enjoyed significant pricing power throughout the year, pushing average daily room rates to levels that were 10-20% above pre-pandemic rates, which more than offset the modest drag from lower occupancy rates. STR notes that RevPAR averaged $93.27 for the year - up 8.1% from 2019 - as a 13.6% relative increase in ADR offset a 4.9% drag from occupancy.

{kind=link}

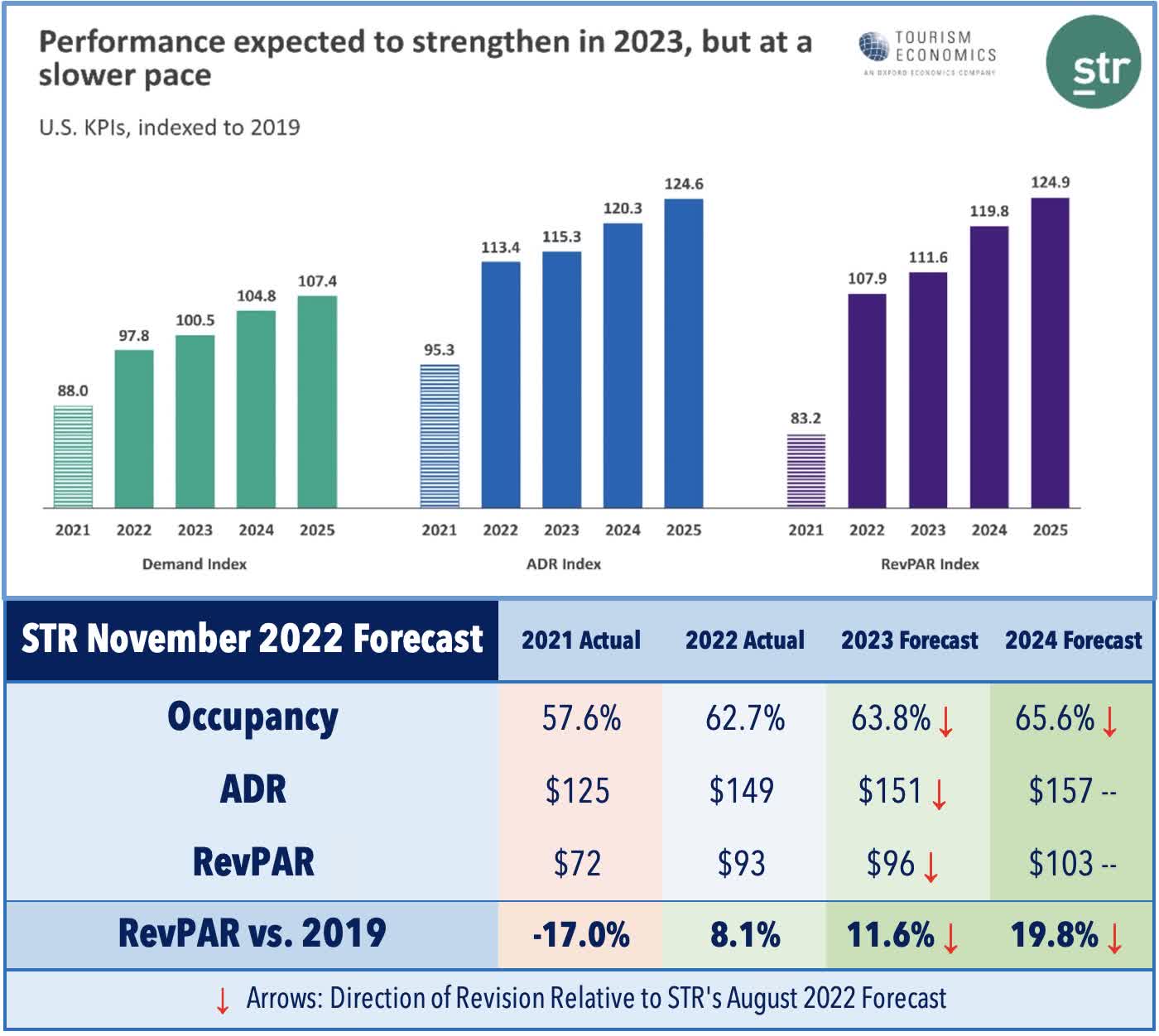

STR provided a relatively upbeat outlook for 2023 in their latest forecast in November, predicting a further recovery in hotel revenues despite a mild recession as a "base case" scenario. STR forecasts that RevPAR will improve another 3% above 2022-levels driven by a 100 basis improvement in occupancy and a 1% increase in ADR. STR noted that "group business travel has been much more aligned with pre-pandemic patterns... [while] leisure travel has maintained its strength." Importantly, STR sees a continued improvement in bottom-line performance metrics in 2023 as hotels continue to operate with lower employment levels and reduced services compared with pre-pandemic levels. Hotel profitability hovered at just 60% of 2019-levels at the start of 2022 but climbed above 2019-levels beginning in June 2022.

{kind=link}

CBRE ( CBRE ) provided a similarly constructive outlook in their latest report last month with a baseline forecast calling for RevPAR growth of 5.8% in 2023 driven by a 4.2% increase in ADR and a roughly 100 basis point improvement in occupancy. CBRE highlighted the ongoing dispersion in performance between markets and segments, noting that lower-priced hotels and secondary markets significantly outperformed the urban "gateway" markets early in the recovery, but the surge in room rates in the upscale segment this summer closed some of the RevPAR differentials. The Top-10 performing markets in 2022 were all in the Southeast or Southwest regions led by Miami, St. Petersburg, Tampa, and Virginia Beach while the Bottom-10 markets were in Northeast or Northwest urban destinations with San Jose, San Francisco, Oakland, Seattle, D.C., and Chicago among the most significant laggards.

{kind=link}

With pent-up leisure demand carrying the recovery over the past year, further progress rests largely with the other two major demand segments - group and business travel - which remain in the nascent stages of recovery. We've become more optimistic about the future of business travel, understanding that while remote work is certainly changing the complexion of business demand, it's not necessarily for the worse. As post-pandemic hybrid work environments become increasingly formalized, we foresee many "traveling salesman" visits being replaced by more frequent group events - industry conferences and quarterly/annual in-person "team meetings." Additionally, incremental demand is unlocked from the flexibility of "work-from-anywhere" dynamics, facilitating hybrid work-leisure trips. We foresee that these two dynamics combine to skew longer-term hotel demand away from "office-dense" coastal cities and towards more "destination" segments.

{kind=link}

Hotel REIT Fundamentals

As discussed in our REIT Earnings Recap , these trends of substantial and lingering dispersions between markets and segments have been on full display across hotel REIT earnings results since early in the pandemic. After lagging early in the recovery, the coastal urban upscale segment - including Host ( HST ), Pebblebrook ( PEB ), and Hersha ( HT ) - enjoyed significant pricing power during the peak summer leisure travel season resulting in 20% average ADR growth in the third quarter, which more-than-offset a double-digit drag from reduced occupancy rates and pushed RevPAR above pre-pandemic levels for these REITs.

{kind=link}

The midscale and limited-service segments, by comparison, saw occupancy rates recover to 100% pre-pandemic levels by late in the third-quarter led by Apple Hospitality ( APLE ) and Chatham ( CLDT ), but this lower-tier segment wasn't able to push room rates as hard as their upscale peers. In total, upscale-focused hotel REITs delivered RevPAR that was 0.6% above 2019-levels in Q3 while midscale-focused and limited service REITs delivered RevPAR that was 0.6% below pre-pandemic RevPAR in the quarter. Profitability metrics remained far better in the limited-service "rooms-focused" segment, however, with EBITDA margins near 40% for these names compared to the low-30% range for their full-service peers - consistent with the pre-pandemic trends.

{kind=link}

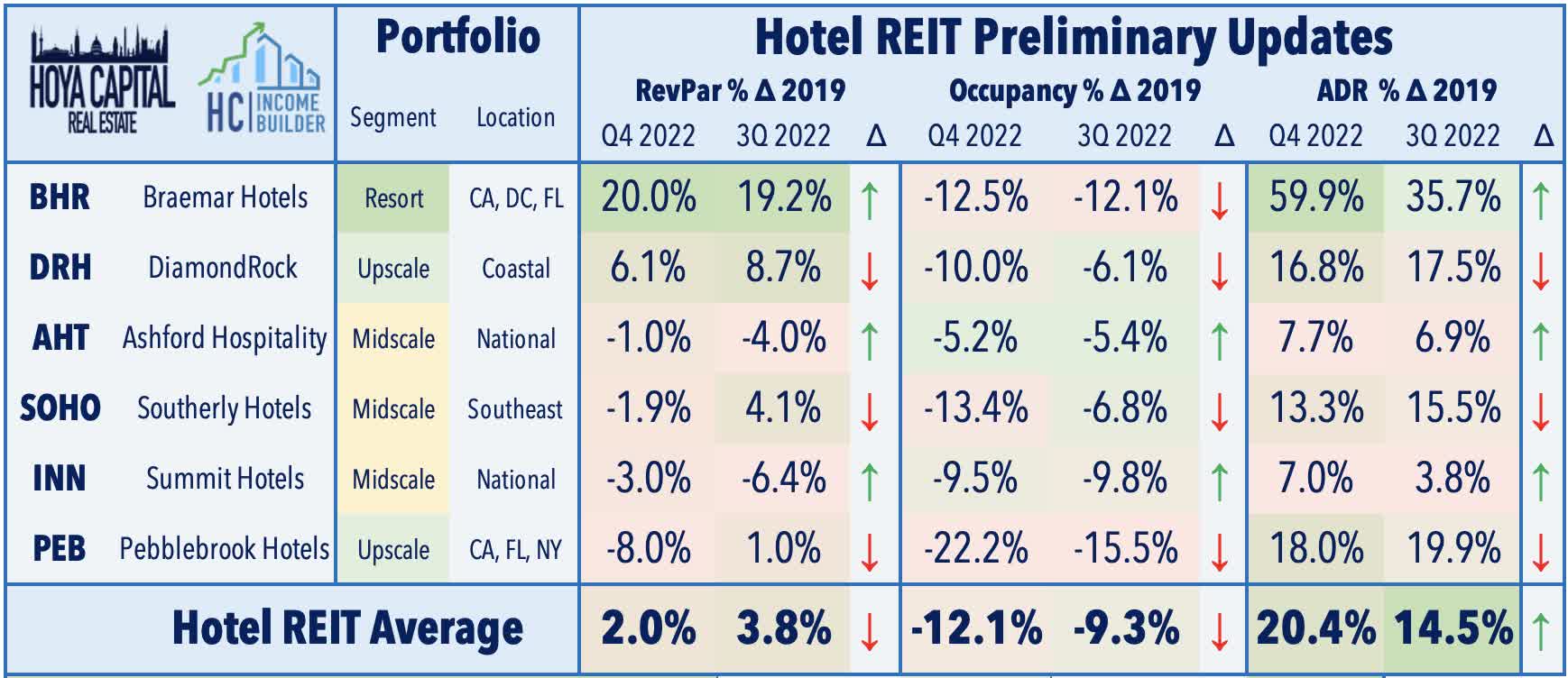

Ahead of the fourth-quarter earnings season beginning later this month, a half-dozen REITs have provided preliminary fourth-quarter metrics showing relatively solid performance in the final months of the year - but with some indications that pricing power in the upscale segment has begun to normalize. Three of the six REITs reported that their comparable RevPAR improved in Q4 compared to Q3 led by midscale-focused Sunstone ( SHO ) and Ashford ( AHT ). On the other hand, three REITs noted a sequential decline in comparable RevPAR including urban-focused DiamondRock ( DRH ) and Pebblebrook . Notably, DRH reported very strong performance in its leisure-oriented Resort portfolio - which generated comparable RevPAR growth of 18%, but its Urban portfolio remained 2% below pre-pandemic RevPAR levels.

{kind=link}

Hotel REIT Stock Price Performance

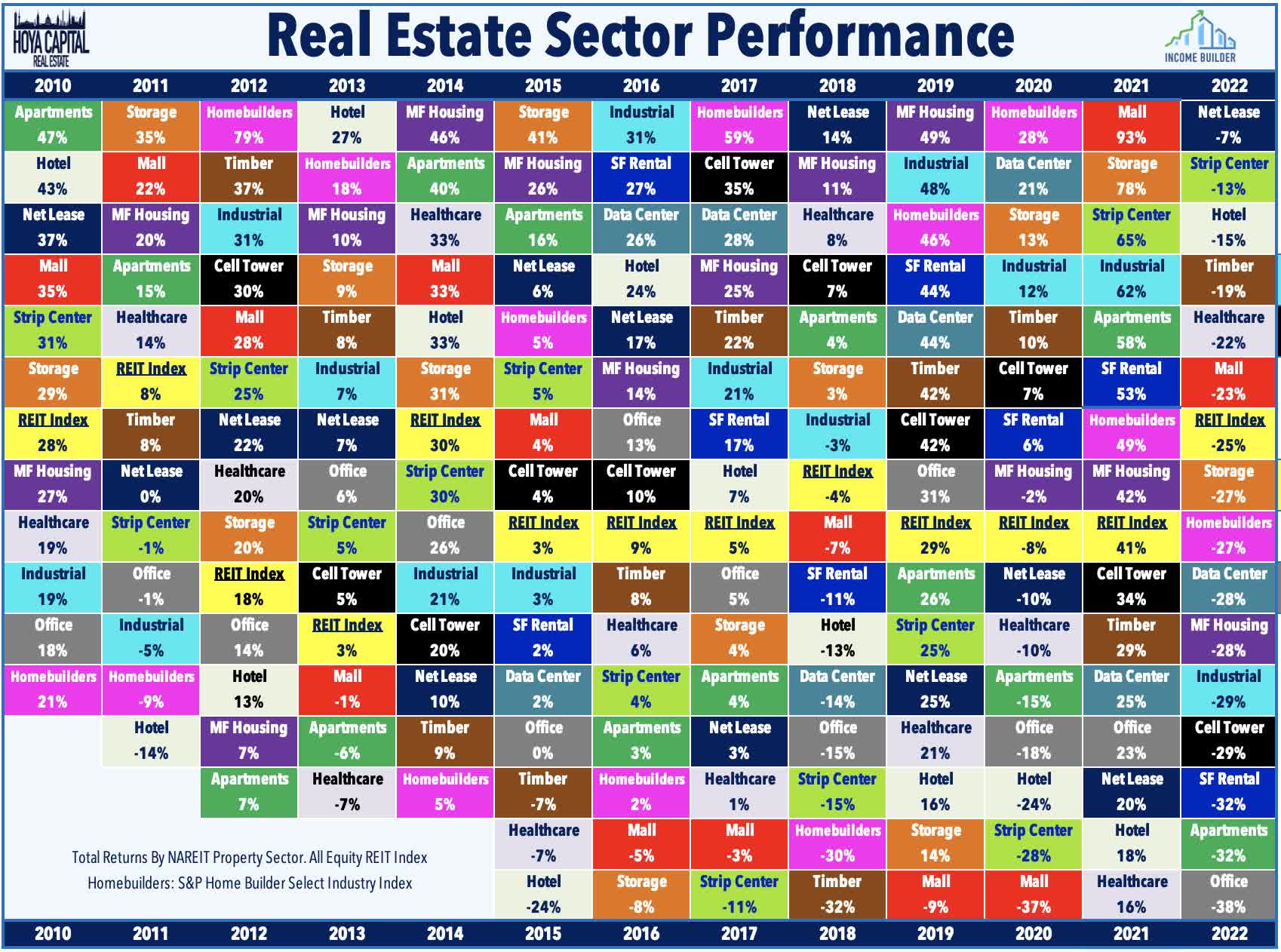

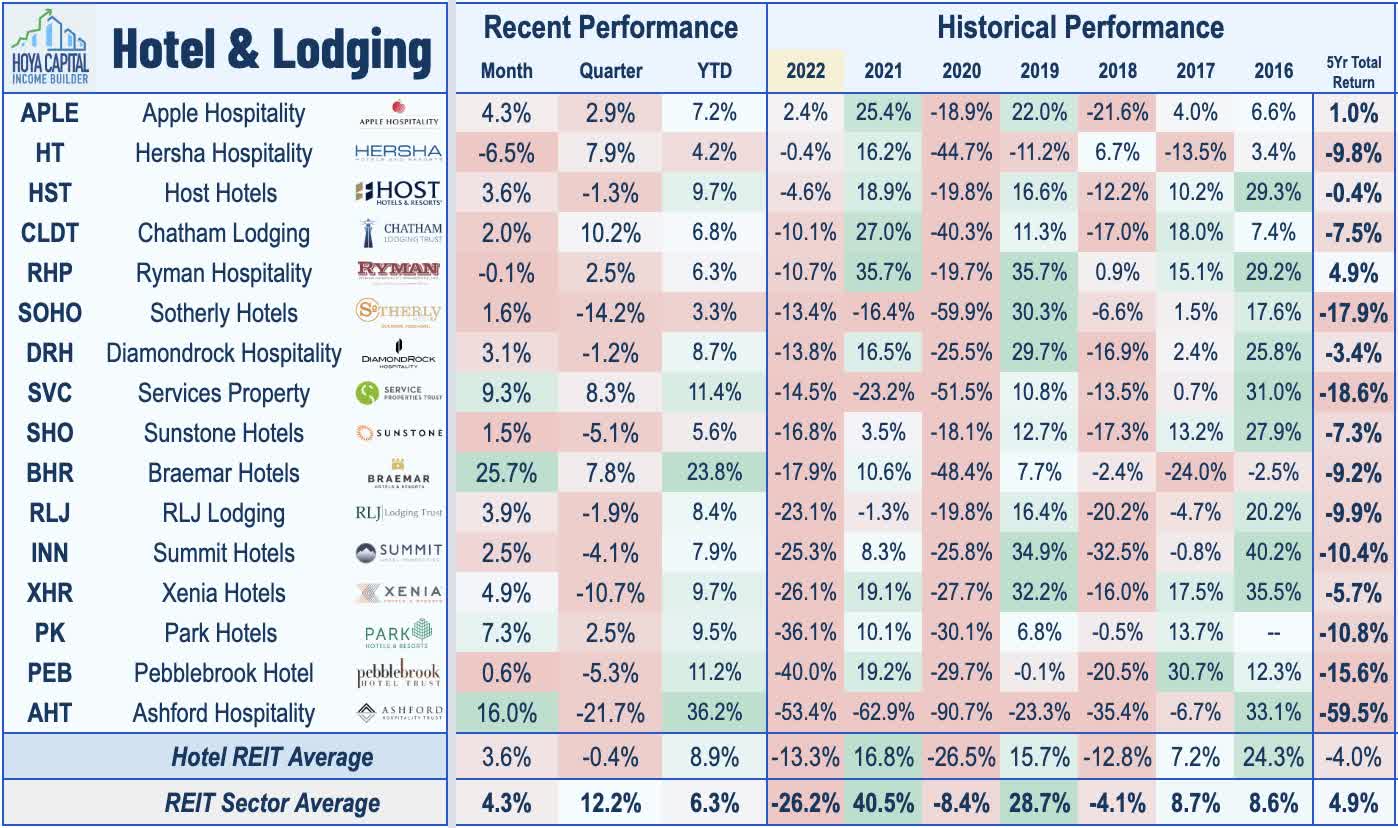

Hotel REITs finished 2022 as the third best-performing REIT sector - snapping a four-year stretch of underperformance relative to the broader Equity REIT Index - buoyed by the steady demand recovery alongside the broader growth-to-value rotation across the global equity market and optimism around the post-COVID recovery. The Hoya Capital Hotel REIT Index - a market-cap weighted performance index - finished 2022 with total returns of -15%, outperforming the -25% total return from the Vanguard Real Estate ETF ( VNQ ) and the -18% decline from the S&P 500 ETF ( SPY ).

{kind=link}

Lifted by solid high-frequency demand data and decent preliminary earnings updates, Hotel REITs are among the better-performing sectors through the first three weeks of 2023 as well with average returns of nearly 9% - outpacing the 6% gain on the broader REIT Index. Since the start of the pandemic, we've observed a clear "flight to quality" performance pattern across the hotel REIT sector with outperformance from REITs owning the strongest balance sheet including Apple Hospitality and Host Hotels . We've also seen outperformance among REITs focused on the midscale and limited-service segment and those that have taken proactive steps to shore up their balance sheets through portfolio sales and debt refinancing.

{kind=link}

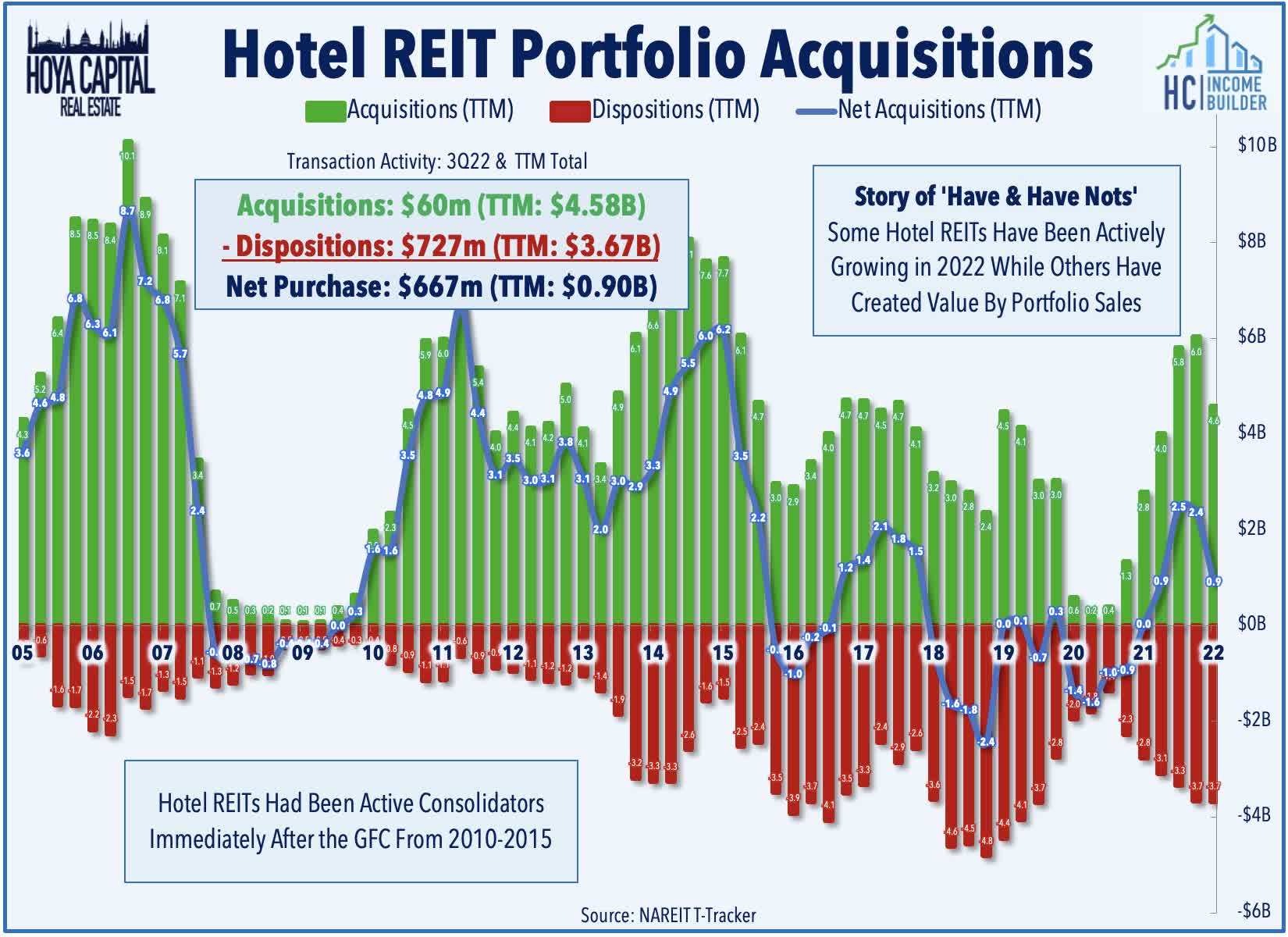

Several hotel REITs have created significant shareholder value by selling assets into the private markets at premium valuations and using the proceeds to shore up their balance sheets. Hersha Hospitality was among the best performers in 2022 after selling nearly a dozen properties across several transactions including a $125m sale of Hotel Milo Santa Barbara and Pan Pacific Seattle for $455k per key and a $505M sale of seven properties for $360K/key. The company has used the proceeds to pay down debt and noted that the deals are " confirmation of the public-to-private market valuation gap." A handful of other REITs were active sellers in the back-half of 2022 including a $100M portfolio sale from Xenia Hotels ( XHR ), over $300M in sales from Park Hotels ( PK ) and a roughly $50M sale from Sotherly Hotels ( SOHO ), - deals that look quite well-timed in hindsight.

{kind=link}

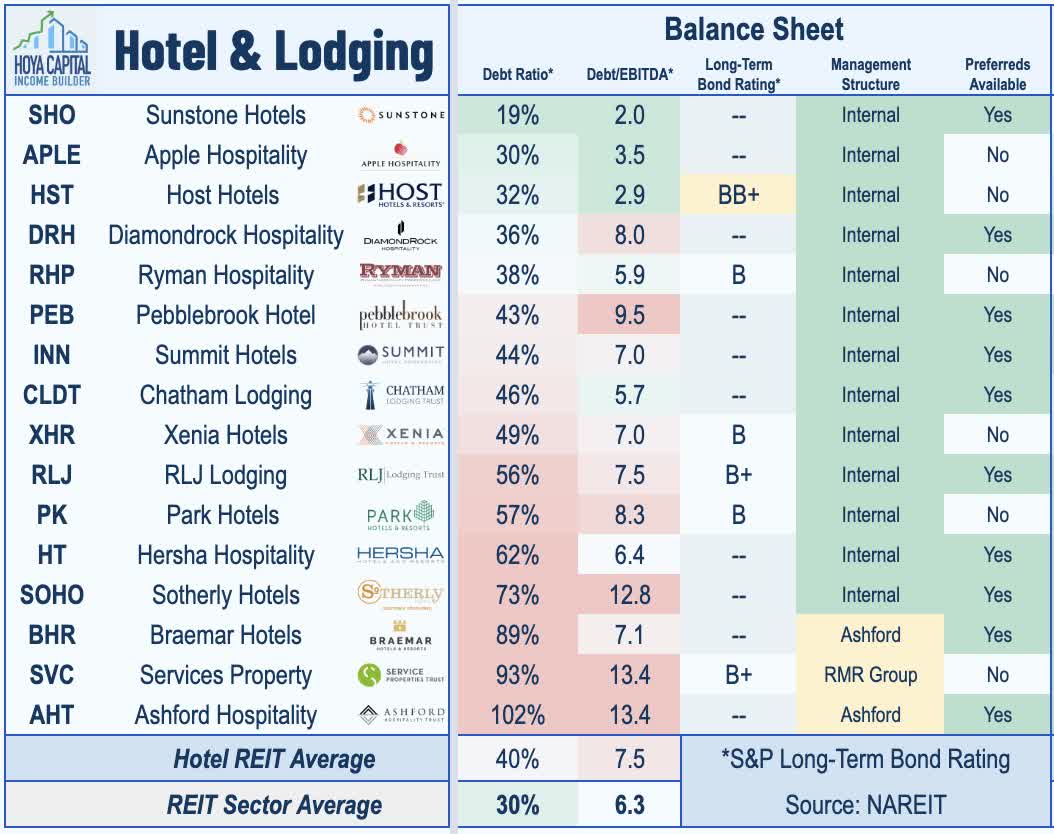

Hotel REIT balance sheets have improved considerably over the past several quarters with more than half of the REIT sector now operating with Debt Ratios below the 50% threshold - reductions driven by these asset sales, improved operating performance, and higher retention rates. We've observed the 50%-level utilized as a threshold in resuming nominal dividend distributions while the 30-40% Debt Ratio range is where we've observed a more meaningful restoration in dividends with Apple and Host serving as the leading examples. Several REITs are still far from out-of-the-woods, however, including the trio of highly-levered REITs with Debt Ratios above 80% - Ashford , Braemar ( BHR ), and Service Properties ( SVC ) - which simply cannot afford any further setbacks in the recovery.

{kind=link}

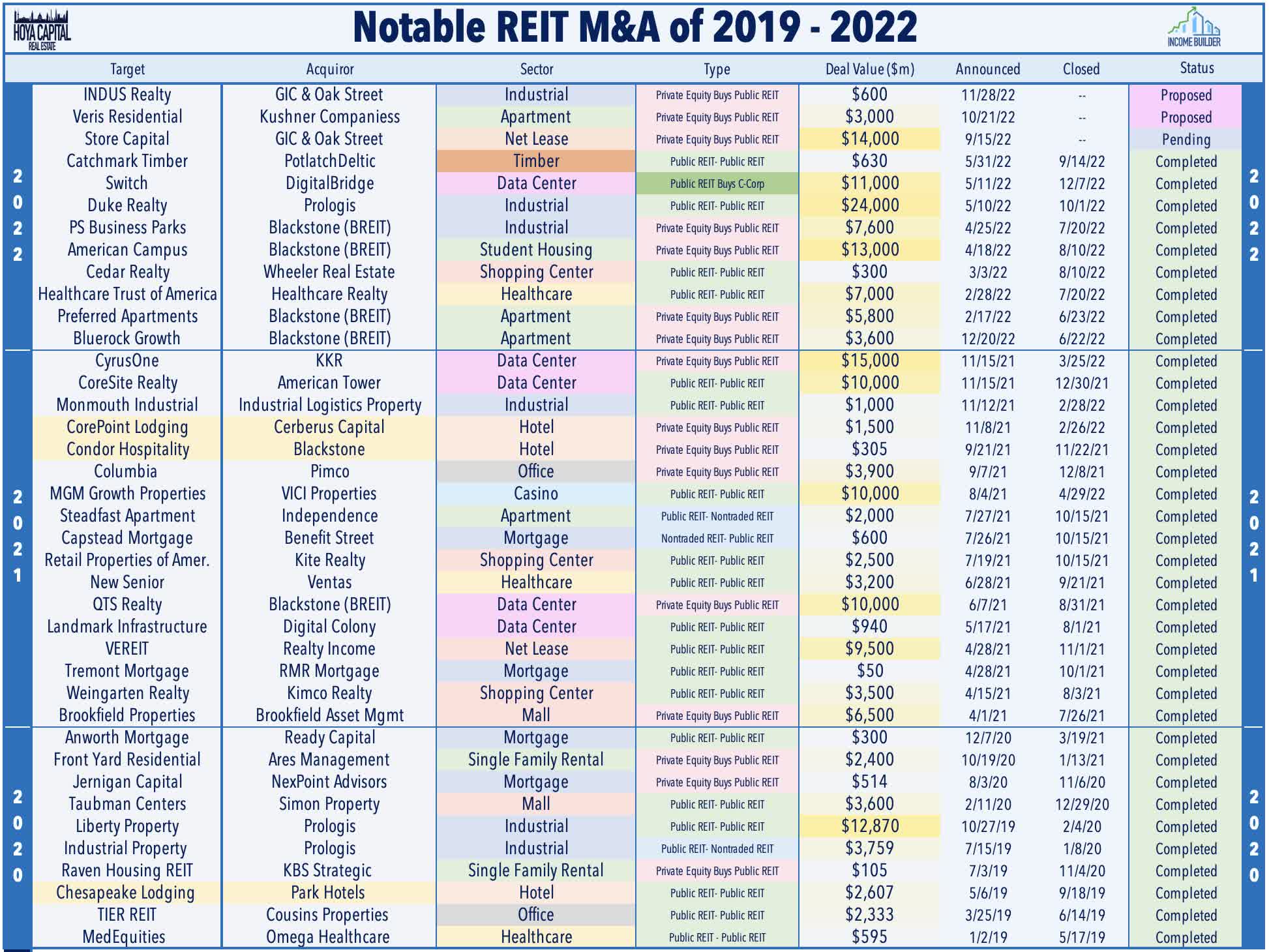

While several hotel REITs were active with portfolio-level transactions in 2022, the larger-scale M&A deals have been few and far between of late following a surge of activity in 2021. In 2021, CorePoint Lodging surged more than 125% after it agreed to be acquired by a group led by Cerberus Capital. Condor Hospitality meanwhile, also soared more than 100% last year after selling its entire portfolio to Blackstone ( BX ) in a $305M deal. These deals were the only major REIT-involved M&A since mid-2019 when Park Hotels acquired Chesapeake Lodging in a $3B deal.

{kind=link}

Deeper Dive: Hotel REIT Economics

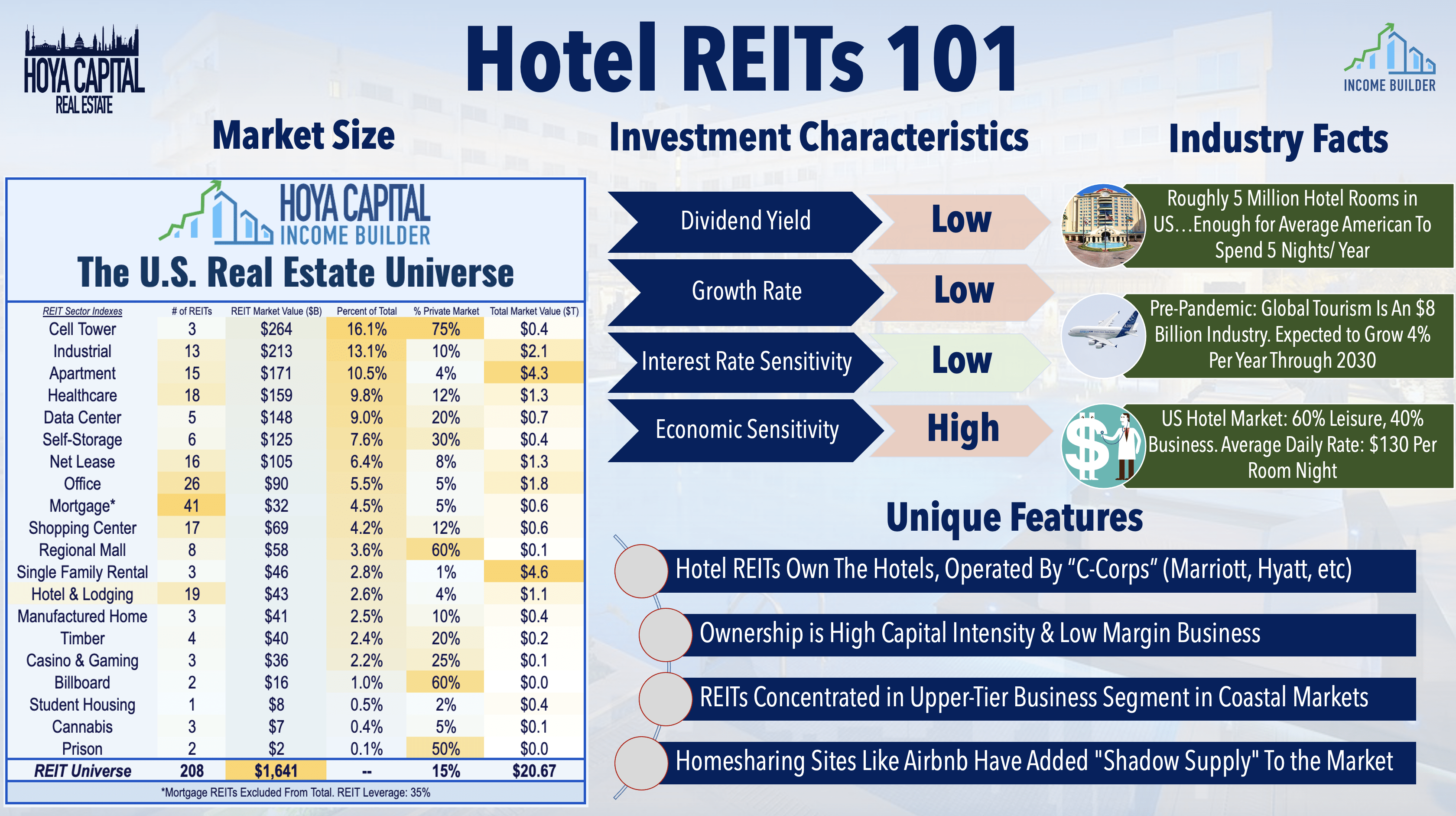

Taking a step back, hotel ownership is a tough, capital-intensive business even in the best of times. Generally, the companies that are ubiquitous with the hotel business Marriott ( MAR ), Hilton ( HLT ), Hyatt ( H ), Choice Hotels ( CHH ), and Extended Stay ( STAY ) - don't actually own hotels but instead simply manage the hotel for the property owners. These hotel operators are typically structured as C-corporations and tend to operate with an "asset-light" operating model with higher margins and lower leverage. While REITs are effectively partnering with these hotel operators, the relationship with another emerging player - Airbnb ( ABNB ) - isn't quite as friendly.

{kind=link}

In recent years, hotel operators have been negatively impacted by a growing "shadow supply" of transient rooms offered through short-term home rental firms such as Airbnb. While we're skeptical of Airbnb's valuation - 2x the market capitalization of the entire hotel REIT sector combined - we are believers in the growing utilization of short-term home rentals. While short-term rentals represent less than 10% of available room nights on an average night, supply growth tends to swell considerably in response to high demand. Studies from STR and the BLS have found that short-term home rentals affect urban hotels most acutely, representing a source of "liquid supply" that compromises pricing power on critical compression nights.

{kind=link}

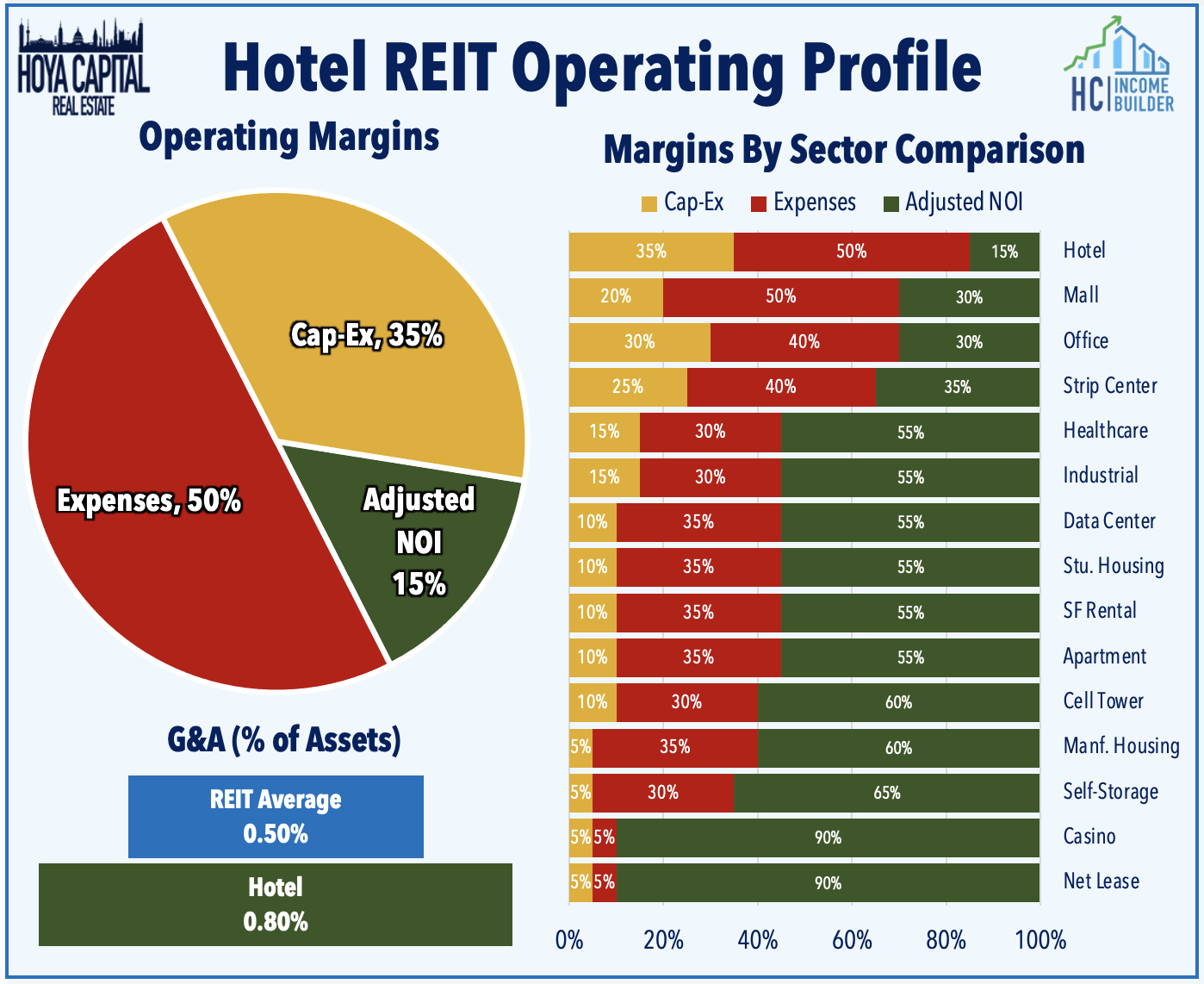

In contrast to these hotel operators, hotel REITs operate under a relatively asset-heavy model and operate at considerably lower margins. We estimate that during "normal" times, hotel REITs operate at adjusted NOI margins of just 10-20%, the lowest in the REIT sector. Because of this operating profile, they assume a high degree of operating leverage and are highly sensitive to marginal changes in supply and demand conditions. Hotel REITs tend to be less nimble and have slower growth rates than C-corp hotel operators, but have historically paid a sizable dividend yield to investors.

{kind=link}

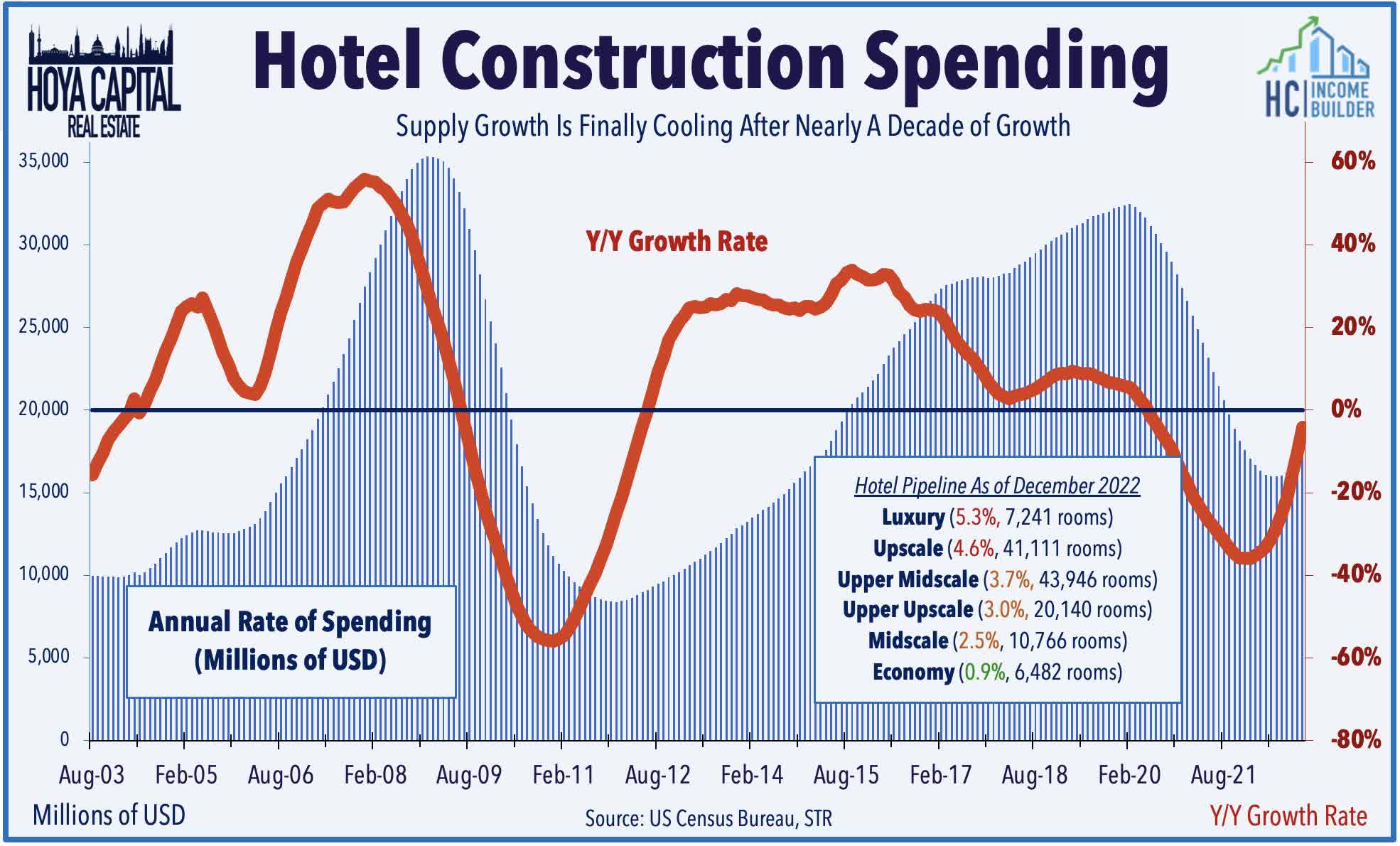

Perhaps the only silver lining of the pandemic, the hotel development pipeline is finally showing signs of cooling after a half-decade of above-trend growth, and if the past recession is any indication, developers will be slow to resume activity even after the dust settles. Over the past several years, supply growth was most acute in the middle- and upper-quality segments, the segments most commonly owned by hotel REITs. On the other hand, supply growth has been nearly non-existent in the limited-service and economy segments, which have been two of the outperforming categories over the past several years.

{kind=link}

Hotel REIT Dividend Yields

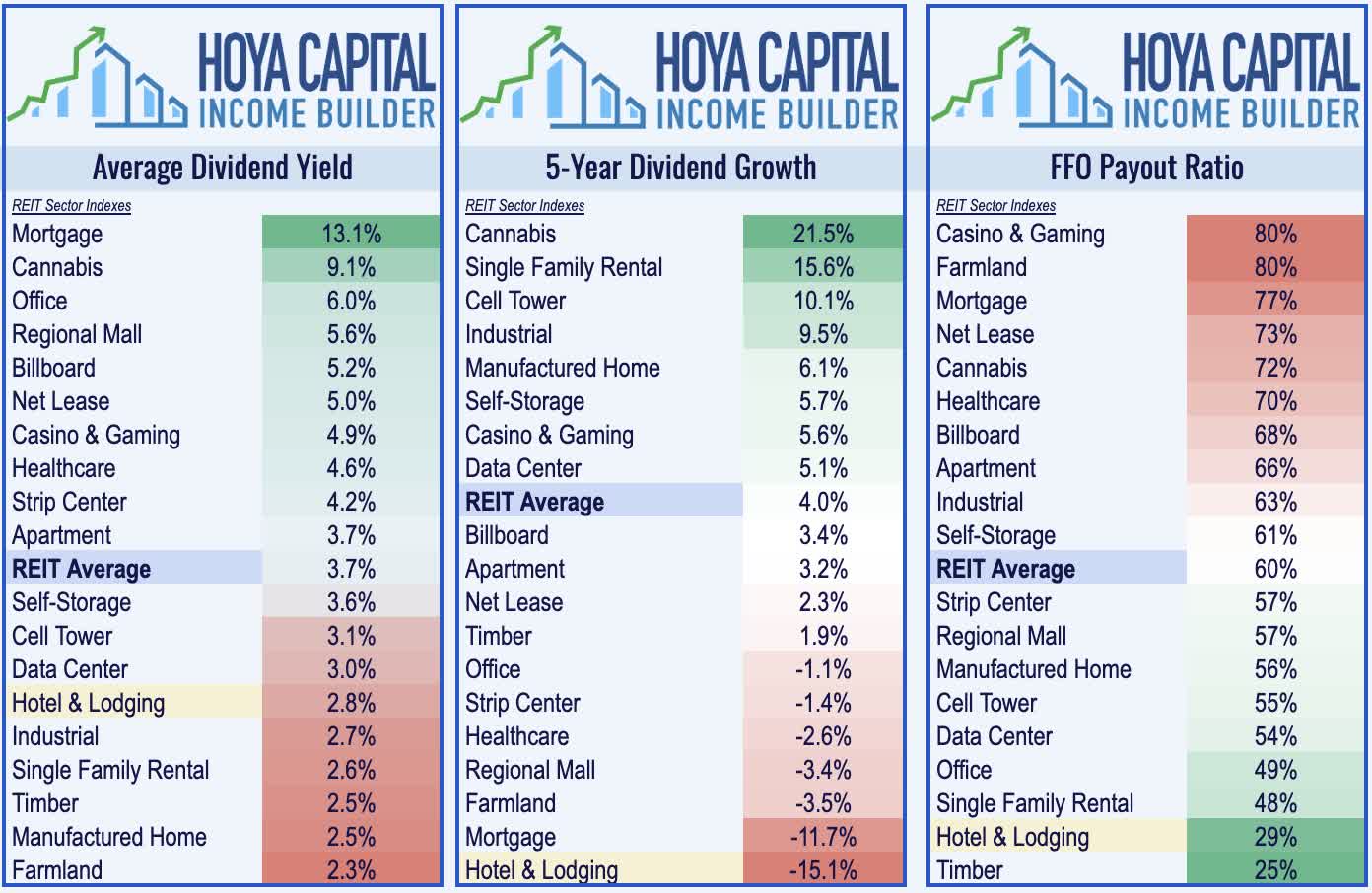

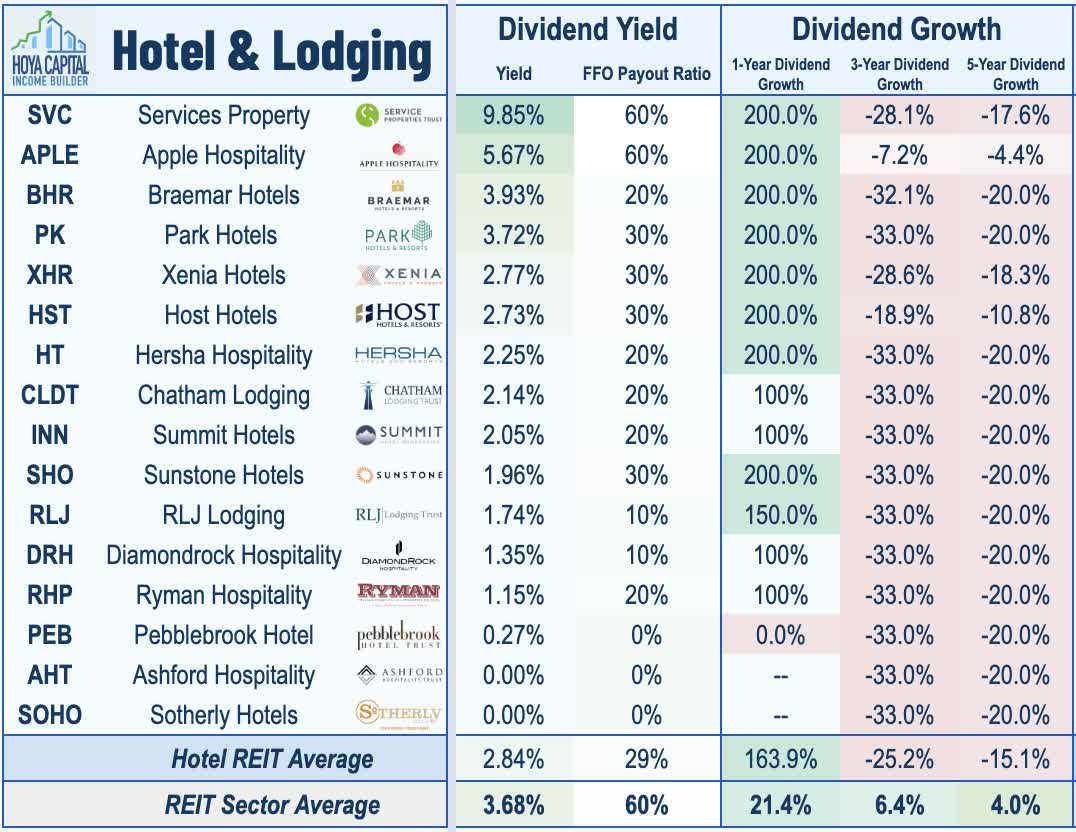

It's tough to pay dividends if hotels are sitting half-empty. Once one of the highest-yielding REIT sectors, all 18 hotel REITs slashed their dividends in 2020 - accounting for a sizable percentage of the total REIT dividend cuts during the pandemic. While hotel REITs were among the most active in raising their dividends in 2022, despite the first wave of dividend resumptions this year, hotel REITs remain near the basement of the dividend yield tables. Hotel REITs pay an average dividend yield of 2.8%, below the 3.7% yield on the market-cap-weighted average and significantly below the 9% yield on the tier-weighted Hoya Capital High Dividend Yield Index .

{kind=link}

As predicted early in the pandemic, hotel REITs were indeed among the last property sector to restore dividend distributions. Apple Hospitality was the first hotel REIT to materially restore its dividend in early 2022 followed by Host Hotels several months later. A wave of hotel REIT dividend resumptions followed in the subsequent three quarters and we've now seen 13 of the 16 hotel REITs either reinstate or raised their common dividends this year while four hotel REITs also paid supplemental special dividends in late 2022. Service Properties now pays the highest dividend yield in the sector at nearly 10% after restoring its quarterly dividend at $0.20/share in October. Braemar Hotels , Park Hotels , and Xenia Hotels also meaningfully restored their quarterly payouts in late 2022 and each now pays respectable dividend yields of at least 2.8%.

{kind=link}

Ten of the sixteen hotel REITs also have exchange-listed preferred securities and while normally preferreds are a "safe haven" for investors during drawdowns, that wasn't necessarily the case for several of the hardest-hit REITs. At the peak last year, a half-dozen hotel REITs had suspended their preferred distributions, but all except one - Sotherly Hotels - have since resumed and fully caught up on their preferred dividends. SOHO announced this week that it will resume its preferred distributions and noted that it intends to pay the accrued dividends through "periodic announcement of special dividends, as warranted by market conditions and profitability."

{kind=link}

Takeaway: Value in Limited-Service & Preferreds

With pent-up leisure demand carrying the recovery over the past year, further progress rests largely with the other two major demand segments - group and business travel. We've become more optimistic about the future of business travel, understanding that while remote work is certainly changing the complexion of business demand, it's not necessarily for the worse. The "traveling salesman" visits are being replaced by more frequent group events while "work-from-anywhere" hybrid work-leisure trips are skewing demand towards more "destination" segments. Within the Hotel REIT sector, we continue to favor the higher-margin limited-service segment but are also beginning to see value in select full-service names with a Sunbelt focus along with compelling higher-yielding opportunities in hotel REIT preferred stocks.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Hotel REITs: Dividends Are Back