BIP - How To Make Money Off The Brookfield Spin-Off - Part 2

Summary

- After the spinoff, Brookfield investors have to allocate between BAM and BN. BN is the old BAM but owes only 75% of asset management. BAM is an asset-light manager.

- Both stocks are currently undervalued.

- BAM is expected to deliver better returns vs BN with higher yield and growth. It may become one of the best dividend payers.

- BN is significantly undervalued on a SOTP basis and may deliver comparable returns in case of material buybacks.

This is an update to Part 1 . It includes fresh data and responses to some of your comments. The readers are expected to be familiar with the subject as the Brookfield structure is fairly complicated, but I will provide a short background section for convenience.

Background

On Dec 12, investors who owned Brookfield Asset Management ("old BAM") in their brokerage accounts received a spinoff with the same name ("new BAM"). The "old BAM," meanwhile, was renamed to Brookfield Corporation. So now, we have two Brookfield stocks of two Canadian corporations trading on both NYSE and TSE - Brookfield Corporation ( BN , TSE:BN.CA) and the new Brookfield Asset Management ( BAM , TSE:BAM-A.CA). BN is the old BAM but owns only 75% of its asset management. The new BAM is responsible for asset management and nothing else. Both companies are so intertwined that the business remains effectively unified despite the split of tickers. The new BAM stock is supposed to unlock the value of the asset management segment and put its growth on steroids.

To better understand the following, BN also has 3 public subsidiaries that exist in both partnership and corporate forms: Brookfield Infrastructure Partners ( BIP , BIPC ), Brookfield Renewables Partners ( BEP , BEPC ), and Brookfield Business Partners ( BBU , BBUC ). The fourth subsidiary, Brookfield Reinsurance Partners ( BAMR ), exists only in the partnership form.

Brookfield Corporation as SOTP

BN is a pure holding company now and we will start with a table representing it as the sum of the parts ((SOTP)).

{kind=link}

Compiling this table I used BAM's Q3 Supplementary and market quotes for Brookfield Infrastructure, Brookfield Renewables, and Brookfield Business. We will not discuss their valuations.

Carry from existing funds will belong 100% to BN. Carry from new funds will be split 2:1 between BAM and BN respectively. In some remote future, BN will receive 1/3+75%*2/3 ~ 83% of carry. Practically speaking we can ascribe all carry to BN today.

From 2017 to 2021, Brookfield (together with Oaktree since 2019) generated net realized carry of $74, $188, $396, $348, and $715 in millions respectively. Q3 LTM number was $509. Averaging over the last three years, Brookfield generates about ~$500M of net carry annually. Applying a 10x multiple, the value of carry is ~$5B and this is the number in the table. It is conveniently close to the ~$6B in accumulated (but unrealized) net carry in Q3 which should be still discounted to its present value. Am I sure about 10x multiple? Not at all, but the input of carry is so small today that the crudeness of calculations hardly matters.

I used Brookfield data for corporate assets, other investments (including important Brookfield Residential), and working capital. Based on Bruce Flatt's comments and the value of the Oaktree investment, I expect $3-4B in cash and assets have been transferred to the new BAM.

There might be some small mistakes in these numbers but it makes sense to switch to more important line items - real estate, insurance, and asset management.

Brookfield Property Group (BPG)

BPG, the former BPY , consists of 3 segments: core office, core retail, and LP investments representing Brookfield contributions into its private funds.

BPG/BPY was formed through a spin-off from the mothership in 2013 and started growing by acquiring companies in which it owned partial stakes such as Brookfield Office Properties ( BPO ) and Canary Wharf in London. Everything was going smoothly but even at this time, it was trading consistently below its IFRS book value. For example, my records show that in 2015 it was trading at more than a 20% discount from its book value. But the worst was yet to come.

One of the companies partially owned by BPY was General Growth Properties ( GGP ) which BPY, after some adventures, acquired in full in 2018. It was a contrarian bet as GGP owned malls, and the term "death of malls" was already coined.

The market was not charmed. In early 2020, before the pandemic, I posted on Brookfield subs and registered a ~40% discount from the BPY book value. If we trust the market to value BIP and BEP, we should respect BPY market valuations as well.

For many reasons, investors kept disliking BPY and in 2021, Brookfield had to take it back private. The pandemic may have further negatively affected BPG/BPY value and that is why I used a 25-50% discount from the IFRS book value in the table.

Accounting also suggests some caution. IFRS (contrary to conservative GAAP) requires periodic revaluation of properties attempting to present their fair values. This can be done rather reliably with comps for some standard properties. For complex properties of BPG's portfolio, comps are hardly applicable. Instead, Brookfield projects rental cash flows and determines the properties' fair values using discount rates and terminal cap rates. To illustrate the process, here is a table from the Q3 BPY filing (BPY's preferreds are trading publicly and the company has to issue quarterly reports):

{kind=link}

How confident can one be of the terminal rate in 10 years being precisely 5.3%? How confident can one be of the discount rate to remain precisely at 7.0% during 2022 despite the general rate increase?

Certainly, this valuation method is approximate by its nature and we would like to test it using real-world transactions. The situation with actual sales varies across the segments. LP is supposed to be the riskiest but Brookfield sells properties in this segment regularly exiting private funds. We know that Brookfield's real estate funds are successful and the company records big disposition gains on its net income account supporting IFRS valuations. In the Office segment, Brookfield sells properties (or interests in them) occasionally and almost always at slight premiums to their IFRS values. This means that at least some properties are valued correctly but does not prove that assets are valued conservatively in general. Finally, I am not aware of significant sales in the Retail segment and valuations in this segment remain unproven. Based on the latest BPY filing, the current value of all properties is ~$62B (with ~$20B in the Retail segment) plus another ~$19B in equity-accounted investments. Due to high leverage, a 20% inaccuracy in properties' valuations may halve BN's real estate equity. Without granular market data about properties (in particular, weaker retail properties), the discount to IFRS value, in my opinion, is warranted.

To be fair, a 50% discount is, most likely, overkill. But I would like to mark the lowest possible (within reason) valuation for BN.

Insurance solutions

The book value of BAM's insurance business - Brookfield Reinsurance ( BAMR ) - is ~$4B (as a reminder: BAMR stock price is linked to BN and BN analysis is equally applicable to BAMR). The management values the business at exactly twice its book value. This implies 20% ROE which is achievable in the short run as Brookfield keeps reinvesting cash and short-term securities at much higher yields. I am not sure this ROE is sustainable in the long run nor can I disprove it. Apollo's Athene ( APO ) ( ATH ) has been achieving ROE of ~15% and higher for many years while modestly leveraged and having excess capital. BAMR may use higher leverage and be less conservative since BN provides an implicit backstop.

I am almost certain that the insurance business should be valued at a significant premium to its book value. However, the business is still very young and has not generated a reliable track record. This is the reason why I still use its book value on the low side.

The new BAM

We already have early trading data for the new BAM, but it is too fresh to rely upon. We know now that Q1 23 dividend for BAM will be $1.28 annualized. This is significantly higher than my predictions in Part 1. Q3 filings that appeared after my post cannot explain it. Perhaps, it is due to the strong Q4 performance that only Brookfield knows about for now.

In Part 1, I assumed that BAM would be trading on yield since the company will be paying out 90% of its earnings and based on comps, predicted a trading range within a 3-4% yield or $32-43 using the just announced dividend.

I may have found a better comp since. One can dissect alternative asset managers by two main attributes: a) asset-light or asset-heavy and b)the importance of recurring (primarily management) fees in the realized (or distributable) income. The new BAM is asset-light and recurring fees (mostly management fees) dwarf performance-based income such as carry or performance income from BBU appreciation. Out of big alternative asset managers, only Ares Management ( ARES ) shares the same attributes. Moreover, while Ares receives some performance income, its dividend policy is mostly linked to recurring FRE (fee-related income). Both Ares and Brookfield keep growing their FGAUM (fee-generating assets under management) at a similar clip of ~20%.

Here are Ares dividend yields in 2021-22 (2020 is not representative because of the pandemic):

Author

BAM has several edges compared with Ares. First, it is a better-known name. Secondly, its top management is holding the same shares that are available to retail investors (Ares management owns partnership units in addition to shares). But it is the third edge that matters.

Asset-heavy managers have an important advantage compared with their asset-light peers: they can contribute significant equity of their own to private funds achieving the so-called alignment of interests with clients. No doubt it helps in fundraising. At the same time, asset-light managers can grow faster and have better ROE. Brookfield's approach combines both advantages! BAM is asset-light but still enjoys the alignment of interests because of BN's contributions to the funds. I believe this unique feature goes to the very core of Brookfield's design.

BAM is expected to trade at least at the same yield as Ares but not necessarily right away - it takes time for a new stock to settle at its trading range. At a 3.5% yield, it corresponds to ~$37 stock price (for your reference: my comp from Part 1 ( BIPC ) is currently trading at a 3.3% yield which implies a still higher price for BAM).

BAM constitutes roughly half of BN's SOTP value. If we expect BAM to trade, say, 20% higher than today, it should pull BN ~10% higher as well.

BN vs BAM

I have received a lot of questions about it. How Brookfield shareholders are supposed to allocate between two tickers?

Based on SOTP, BN seems severely undervalued today even with BAM trading at ~$33. It is also rather clear that BN's progress will depend mostly on real estate, insurance, and asset management. Values of real estate and insurance are firmly linked to their IFRS book values.

There is a saying that "you cannot eat book value" (I think it belongs to Warren Buffett but am not sure). To a certain extent, it may describe the BN's situation.

BN's strategy is to keep selling real estate and invest in insurance. It was stated during Investor Day 2022 and is pretty obvious from our SOTP table. But I guess it will take years to achieve considerable progress here. Meanwhile, most of BN's capital will be consumed by building the insurance empire, contributing to private funds, and, perhaps, entering into some strategic combinations. This explains BN's meager dividend with a yield of less than 1%. As we know, BAM is yielding 4% now.

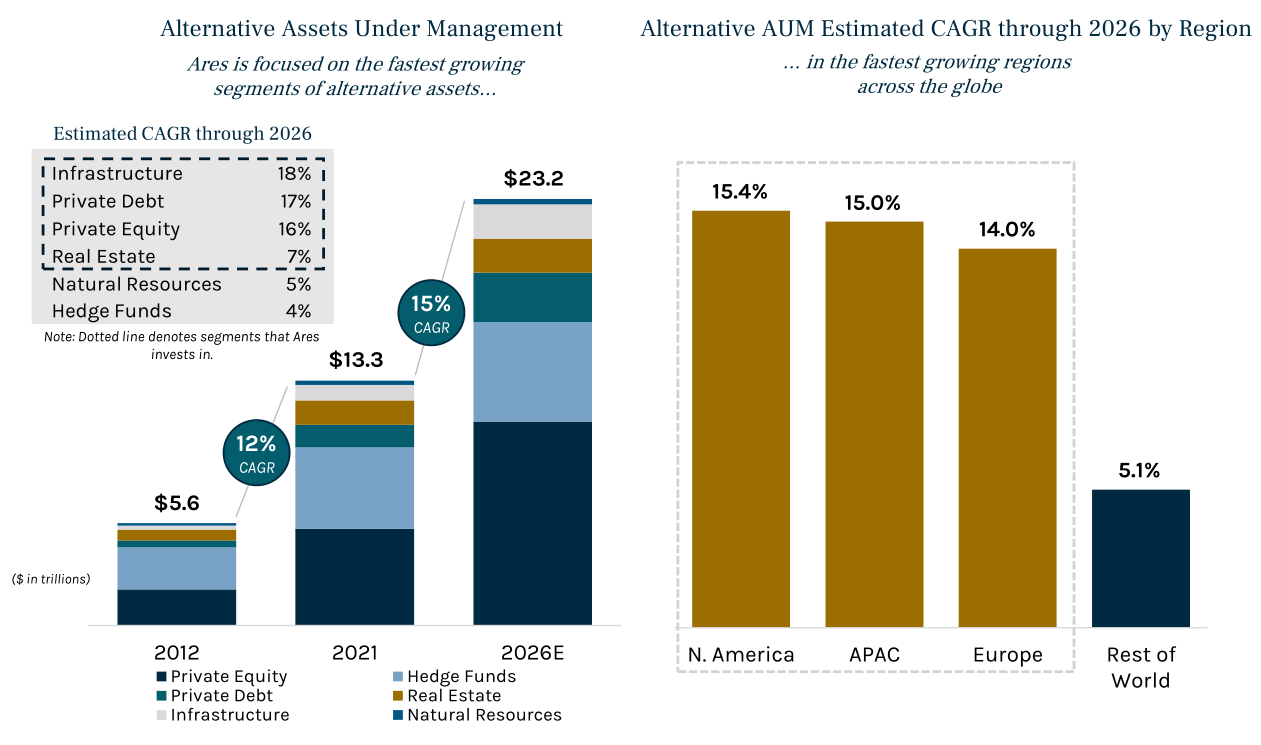

At the same time, BAM will be also growing faster than BN primarily by growing FGAUM and FRE. Asset management will remain the fastest-growing segment (if you do not believe in this, there is very little reason to hold alternative asset managers at all). How long can this growth continue? I do not have a precise answer but it seems highly probable that processes like decarbonization, digitization, and population aging will take decades to mature causing disproportionate growth in FGAUM for big alternative managers. Bruce Flatt mentioned that decarbonization alone (where Brookfield is a clear leader) will need $100 trillion. The success of big alternative asset managers hinges on a single number: the growth rate of alternative assets. I am not ready to discuss this topic in detail here but would like to share a slide from a recent Ares presentation:

{kind=link}

I would also like to mention that in his recent presentation ( available on SA ) Bruce Flatt indicated that the high growth of BAM's FRE (i.e. 15-20%) is already locked for the next several years.

Future returns from stock are a sum of a dividend yield, growth, and multiples expansion/contraction. BAM has a clear edge versus BN in both yield and growth. BN is more undervalued compared to BAM and should benefit more from multiples expansion. But this process may be slower and less certain.

BN can dramatically accelerate multiples expansion through buybacks. This is something BAM is not capable of. Historically, old Brookfield was reluctant to buy back its shares materially but it might change. One favorable factor here is the very recent upgrade of BN's credit rating by Moody's - it is now A3. Correspondingly, the company has just announced the issuance of CAD 1 billion of medium-term notes.

In my opinion, BAM is likely to deliver better returns than BN. If BN initiates significant buybacks, the returns may be comparable. Both companies are expected to trade higher than today.

Conclusion

Stating my opinion, I think I have to disclose my actions as well. Before the spin-off, I bought BAM on a when-issued basis and have further increased my BAM position at the cost of BN. However, I intend to maintain a significant BN stake for a simple reason: I believe that Brookfield management will keep holding a lot of BN stock and execute necessary actions, including buybacks, for its growth.

For further details see:

How To Make Money Off The Brookfield Spin-Off - Part 2