HHC - Howard Hughes: It's Attractive But Also Tricky

2023-07-11 13:40:52 ET

Summary

- I discuss the potential investment value of The Howard Hughes Corporation, a B+ rated real estate developer based in Texas.

- I previously recommended a "hold" position on the company, which proved to be the correct choice.

- I believe that the company could become a good investment if it reaches a certain price point.

Dear readers/followers,

You may recall an article from a few months back about The Howard Hughes Corporation ( HHC ). I Established my thesis for this B+ rated real estate developer who is actually a favorite of many rich investors out there that I follow. In the end, I had a hard time going anything but "HOLD" - which actually turned out to be exactly the correct choice between now and then.

Seeking Alpha Howard Hughes ROR (Seeking Alpha)

However, let's look at what we have going forward - because the company does become attractive at a certain price point, and if that point is reached, you will see me invest in HHC.

Howard Hughes Corporation - I say "Yes", at the right price

The company is a component of the Russel 1000 and a real estate developer out of Texas. Its founding came about 13 years ago, and its headquarters is in The Woodlands, Texas.

Since my last article about HHC back in February, we've gotten the 1Q23 results. The company's portfolio highlights remain relatively at the same level. It operates a highly attractive, almost-7M square feet office portfolio, 2.6M sqft of Retail, and over 5,500 units of multi-family units, as well as 1,367 units of self-storage. That's a big portfolio to manage - and it's not over yet.

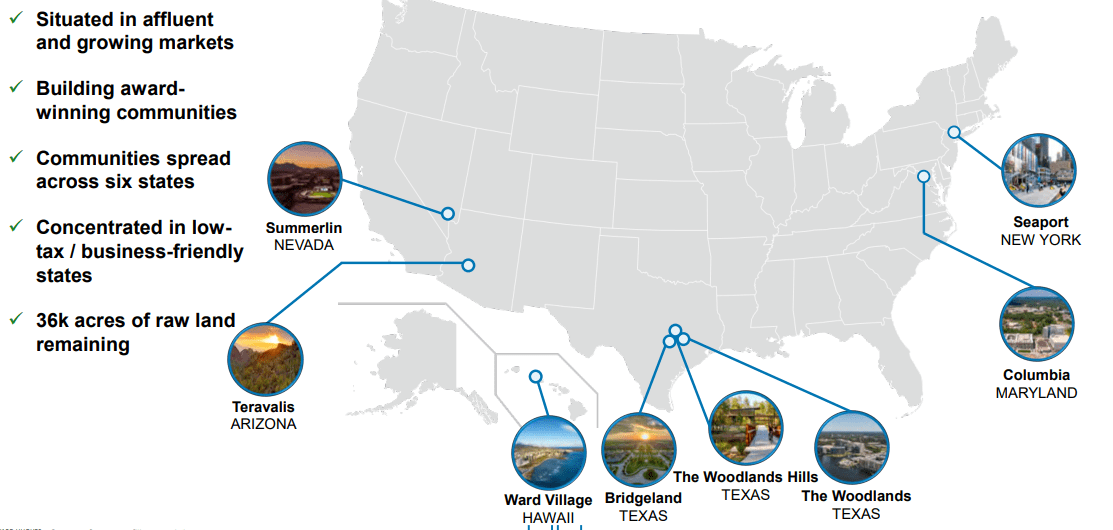

The company also has 36,000+ acres of land and a total of 8 managed communities. HHC's RoE is excellent, averaging 21% as well as a historical YoC of 9%.

The company has a proven track record of developing high-quality and appealing places to live, and the company's idea is to work its self-funding business cycle, using proceeds from land and condo sales as well as overall NOI to fund new development. It's already in a stage, where based on its current portfolio, the company generates significant amounts of recurring income based on its business model. Its geographical exposures are as follows:

{kind=link}

So, as you can see - no California or Oregon/Washington exposure, the areas that are typically now considered to be a "higher" risk given the macro trends we're seeing in these areas.

The company is a sort of complete-solution provider for communities, including public and private school system collaborations, a variety of housing options, development of shopping and dining, office space, safety like hospitals, police and fire stations as well as houses of worship, delivering for a variety of religious backgrounds.

I believe it's fair to say that the company's business model is fairly unique. I do believe others may adopt part of it, but I've yet to find a company that really "does" the same as The Howard Hughes Corporation.

{kind=link}

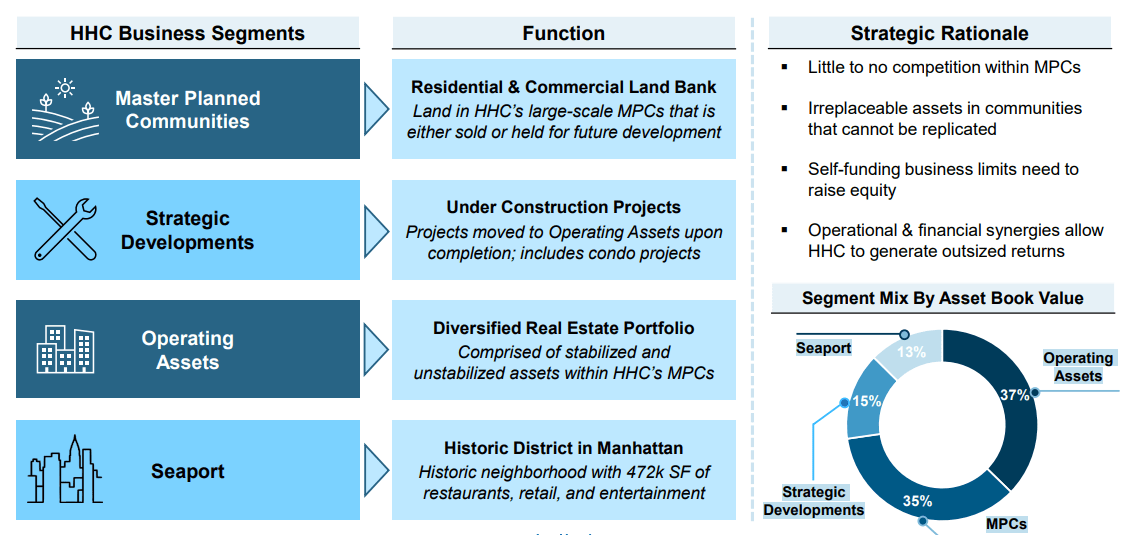

What you see above is the company's 1Q23 business model update, with a mix of MPCs, developments, a diversified real estate portfolio, and the Seaport business segment, which is around 15% of book value.

What I would consider a massive advantage is actually the competition, or lack thereof, in the company's main business segment. The company's claim that it does not need to raise equity (or a limited need) also checks out if we look historically compared to others, and the synergies within this company are significant, to be sure.

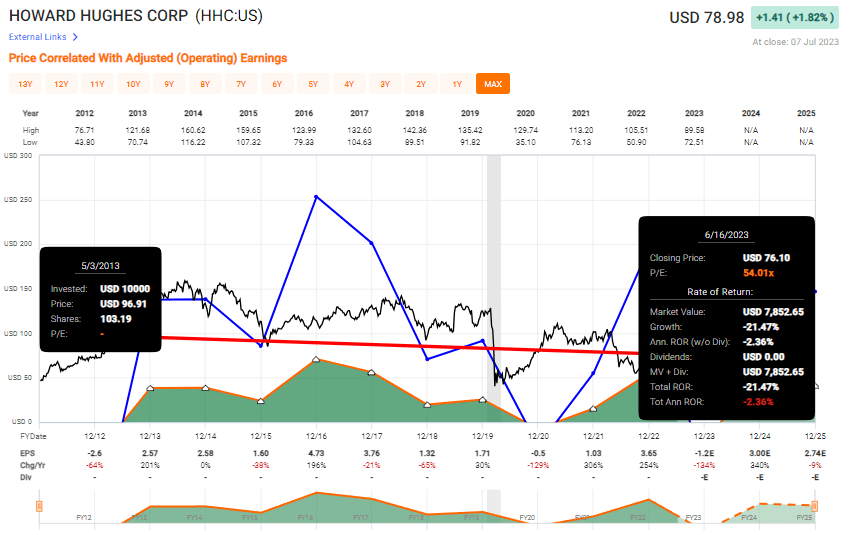

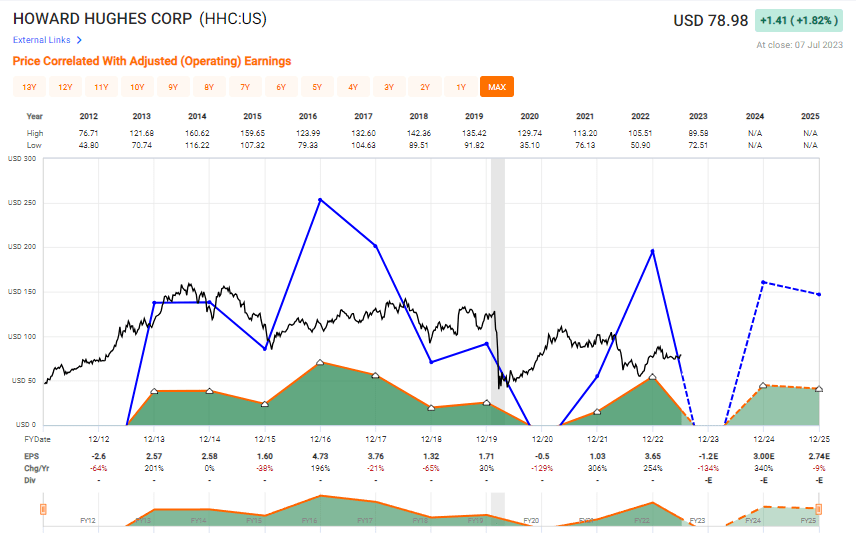

The problem arises when we look at returns. That's where the arguments for investing in HHC really fall apart. The company has been on the market for over a decade at this point. Even if you invested at the onset in mid-2012, the company's total RoR is a meager 4.77% per year, or 70.92% in about 12-13 years. That's well below the S&P500 and most indices - and you also wouldn't have seen any sort of dividend in the interim, because the company pays none. The main problem is that if you bought at any time after 2012-2013, and before the COVID-19 crash, your returns have a very good chance of being significantly in the negative - again, due to the fact that there are no yields to be had here.

{kind=link}

And I did not even pick an especially high valuation to compare to here. It's very easy to find capital destruction of more than 50% in terms of loss in this business.

All of the company's truly excellent arguments start falling apart if I in the space of 10 years and more cannot reliably see a way to make money on my investment, or at least see a high possibility of loss.

Evaluating the appeal of this company is extremely tricky because it lacks usable FFO/AFFO or income metrics. It showcases earnings, but those earnings go down up and down from year to year, down 129% in 2020, up 306% in '21, and down 107% again in 2023E. For most of the last 10 years, it's had negative FFO and AFFO. The troubles that the company has been through, including a serious consideration to sell off the entire company, are more described in my previous article found here.

The company has a very real, theoretical, and actual, appeal as an investment. The problem is that without any sort of yield or payouts, I and other investors can't really even speculate a time as to when we will see returns for this investment. Management has repeatedly come out with lofty price targets for its shares, but I don't view this as especially relevant - the market decides prices, and HHC also needs to accept that we as investors will compare the HHC ticker with alternatives - alternatives that give us money for "waiting".

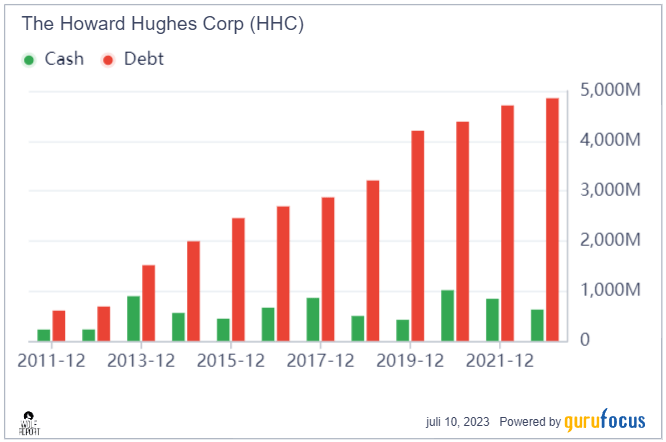

I can't argue with any of the positives that the company offers. It does rank as the best-selling MPC, landscape designer, and community planner, especially down in the southern states (though this outsized exposure to say, Houston, also represents one of its risks). Its business model clearly works - though I can clearly state that HHC is in no way a market leader in terms of profitability. It is average, no more than that. The company may not issue equity, but it has increased its debt load over the past few years.

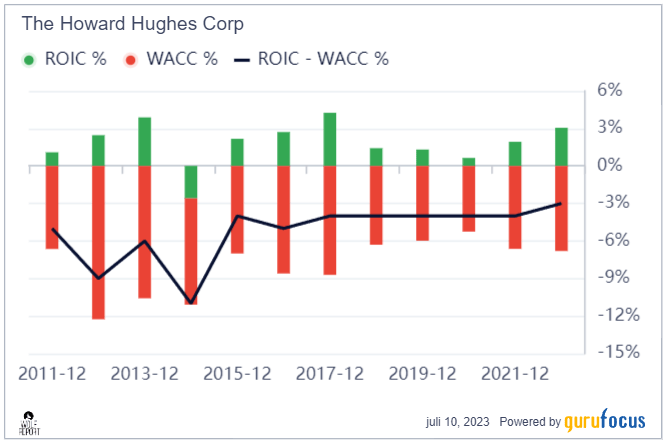

{kind=link}

While the ROIC net of WACC isn't the end-all-be-all of anything, there is nothing anyone can say to convince me that this is a positive or conviction-inducing track record on the part of a company.

{kind=link}

Insider buying for this company is heavy - this is the positive that we see here, but at the same time, these insiders may have different deals that allow for payouts and returns in a way that we as ordinary shareholders and investors do not see or can partake in.

The bullish side to the company is clear to me. Any market leader in a segment is in a good position to deliver potential long-term value on a forward basis.

The problem is, with HHC this has been woefully absent - and it's not for lack of trying, given that we saw Ackman going into the investment. Now, some people following the company may defend and say that HHC still needs time to turn things like Seaport around and work with its office space portfolio - but as I noted in my previous article, I think HHC is being bullish in its office portfolio valuation (and that's me covering office REITs as well as investing in them).

In the end, not even the new developments, strong liquidity, or the relatively positive 1Q23 (in that it beat, but still came in negative, and missed on revenues) can change my stance on where this company is trading or should be trading, or how it should be viewed.

HHC has failed, for the most part, for the past decade, to deliver shareholder value unless you picked it up at trough. I would be willing to invest or consider it more closely when it shows me that it can deliver stability, income, and growing value.

Let's bring this down to valuation.

Howard Hughes - valuation is still not compelling to me

The case for Howard Hughes is relatively simple both on the bullish and bearish side. The bearish side focuses on Seaport, office exposure, cash overhead expenses, and overall not the envisioned profitability that the company had in mind.

And frankly, it's very hard to make even a slightly concerted effort to put a positive spin on the company here when you can literally invest in a 5-7%-yielding REIT that can easily be argued to have a 10-20% annual, concrete upside. Even if Howard Hughes Corporation goes up, so what?

Other companies are likely to go up as well if that does happen. HHC has a correlation to RE - but so do others.

HHC needs to outperform the sector/more, not just deliver growth. And that's where the issue is - I don't see a scenario where the company can reliably do this in a way where I would consider HHC a better investment.

And the B+ rating does not help matters in the least.

It's one of those companies where investors have sometimes told me "Oh, you just don't understand the business model".

Well, I would argue - the business model that has delivered 4.7% annual RoR if you invested essentially on day one, while the market has nearly doubled that? That business model?

My argument with this investment is on the basis of valuation. I do not believe cash flows this volatile, or earnings, to be worth anything close to what some are arguing here. Whenever I see bullish investors speaking to this company and trying to downplay the importance of valuation in it being more art than science (which is not wrong), I become careful. Because while in the short-term valuations can indeed be fickle, the assertion that valuation over time does not adhere to certain principles, be they sector-based or market-based is demonstratively false if you look at any company that's been around for the past 50 years.

And this is the trend of HHC in the last ~10 years.

{kind=link}

As I said early in this article - I do not argue about the company having an attractive portfolio. I argue that the company, as of yet, has failed to turn that portfolio into a positive return for the company's investors, many of which are likely saddled with a decade, or years of sub-par or even negative returns. And when a company fails what I believe to be a basic requirement of any investment, I cannot in good conscience be positive about it unless it is significantly undervalued.

For Howard Hughes, this means I now won't pay more than $50/share for the company, after further discounting the office portion of its portfolio, which by the way is large - one of the largest even.

So, I am lowering my PT, reiterating my "HOLD" rating and going to the following thesis on The Howard Hughes Corporation.

Thesis

- Howard Hughes is an interesting, MPC and office-based RE developer/company, but with a history of generating sub-par returns for over a decade. I do not see any potential clear catalysts for delivering value to its shareholders in the near term. For that reason, I'm fairly negative on the business.

- I would "BUY" this one at a severe discount to the company's own calculated NAV, coming to around $50/share, happy to hold until appreciation, all things being equal, and nothing changing.

- However, at anything beyond that, I'm at a "HOLD", and I would view this business as a clear "trim" target. This is the thesis I update in July of 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

With a B+ rating, I can't call it qualitative, but it's fundamentally safe and well-run, being in Ackman's pocket (to some extent). However, it only fulfills one out of five criteria, making the company a very clear "HOLD". Remember that as smaller investors, trying to think like billionaires comes with risk - and that is also part of the reason why I would stay out here.

For further details see:

Howard Hughes: It's Attractive, But Also Tricky