AQNU - HPS: Take Profits And Cut Exposure To Potential Near-Term Losses

2024-01-09 10:15:32 ET

Summary

- The John Hancock Preferred Income Fund III offers a high level of current income, making it attractive for income-focused investors.

- The fund has seen strong performance, outperforming the preferred stock index and delivering a 4.15% price increase since August 25.

- However, there are concerns about the sustainability of the fund's gains, as the market's expectation of interest rate cuts by the Federal Reserve may not materialize. Investors are advised to take profits before a potential price correction.

- The fund failed to cover its distributions during the most recent full-year period and is destroying its net asset value by holding the payout stable.

- The fund is trading at a much higher-than-average premium, making right now a good time to take some profits.

The John Hancock Preferred Income Fund III ( HPS ) is a closed-end fund that specializes in providing its investors with a very high level of current income. The provision in income is something that has become a popular strategy among retirees and others who are dependent on the investments in their portfolio to cover their investments over the past decade of incredibly low interest rates. While it is now possible to earn a reasonable yield by investing in money market funds or even certain bank savings accounts and certificates of deposits, almost nobody expects today’s rates to be a permanent fixture of the economy. Indeed, it seems very unlikely that the debt-laden economy of most Western nations can sustain even 5% interest rates for very long. As such, investors are still looking for more long-term solutions to obtain the income that they need to meet their requirements. The John Hancock Preferred Income Fund III yields 9.22% at the current price, so it is certainly a very reasonable solution for income-focused investors. Indeed, that yield is in line with many junk bond funds, and it is substantially higher than the 6.76% current yield of the iShares Preferred and Income Securities ETF ( PFF ) so it appears that the fund is beating its asset class by a respectable margin.

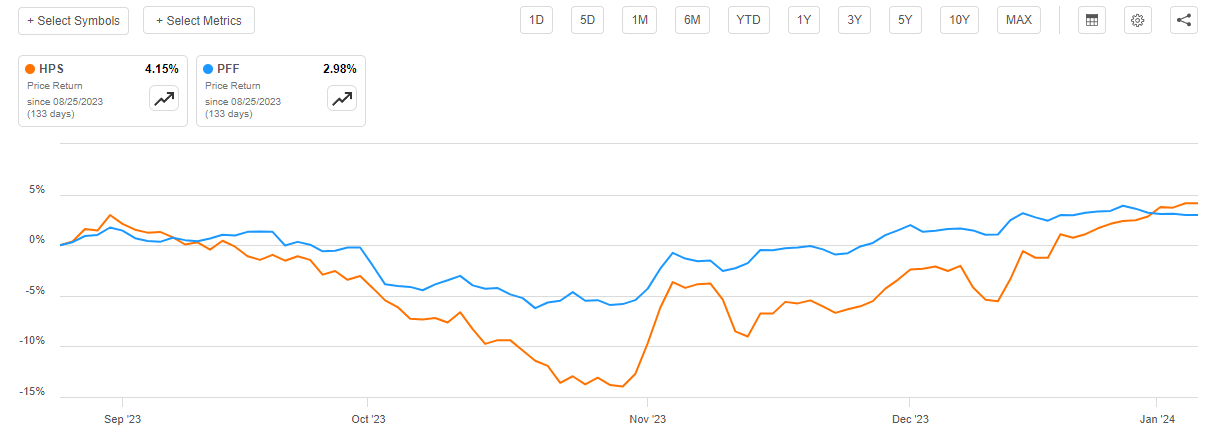

As regular readers can likely remember, we last discussed the John Hancock Preferred Income Fund III on August 25, 2023. The overall market environment at that time was very different from the one that we have today. After all, at that time, investors were beginning to accept that the Federal Reserve was serious about its “higher for longer” mantra and were generally repricing assets to account for the fact that interest rates were unlikely to decline in the near term. We have the exact opposite scenario today, as the market generally expects that the Federal Reserve will be cutting the federal funds rate by 1.25% to 1.50% by December. As a result, it has bid up fixed-income securities such as the preferred stock held by this fund. That has caused the fund’s share price to deliver a reasonably strong performance since the last time that we discussed it. As we can see here, shares of the John Hancock Preferred Income Fund III have appreciated by 4.15% since August 25. That is much better than the 2.98% price increase in the preferred stock index fund:

{kind=link}

Unfortunately, there are many reasons to believe that the fund will not be able to sustain the gains that it has delivered in recent months. In particular, the probability that the Federal Reserve will actually cut interest rates to the degree that the market expects in order to make the current price make sense is very low. This is particularly true because 2024 is an election year and the nation’s central bank will want to avoid accusations that it is making a political move. The economy is also nowhere near weak enough to justify cutting interest rates in order to avoid a recession. We will discuss these in greater detail later in this article.

In light of the factors that were just mentioned, investors would probably be best off taking their recent profits in the fund before it suffers from a price correction as fixed-income prices start to slide due to the failure of the nation’s central bank to satisfy the current expectations of the market.

About The Fund

According to the fund’s website , the John Hancock Preferred Income Fund III has the stated objective of providing its investors with a very high level of current income. The fund also has the objective of preserving its capital.

John Hancock Investments

These objectives make a lot of sense for a preferred stock fund. After all, preferred stock acts very much like bonds in terms of its characteristics. An investor purchases the preferred stock at its par value when it is first issued and then receives a regular stream of dividends from it. The difference between preferred stock and bonds comes from the fact that most preferred stock does not have a maturity date. There are some issues that do have maturity dates though, but in such cases, the maturity date is usually many years in the future. As such, there is no date when the investor receives the par value of the security back from the issuing company, although some issues can be redeemed at the issuer’s option after a certain date. Preferred stock dividends do not usually change based on the profitability of the issuing company though, so they usually trade around their par value depending on how the dividend compares to the market interest rate. The yield of preferred securities is usually fairly high, so investors do not typically lose money if they hold the security for long enough, regardless of interest rate movements. As such, the capital preservation objective makes a certain degree of sense. The current income objective also makes sense because these securities primarily deliver their investment return through direct payments to the investor as opposed to capital gains that accompany the growth and prosperity of the issuing company.

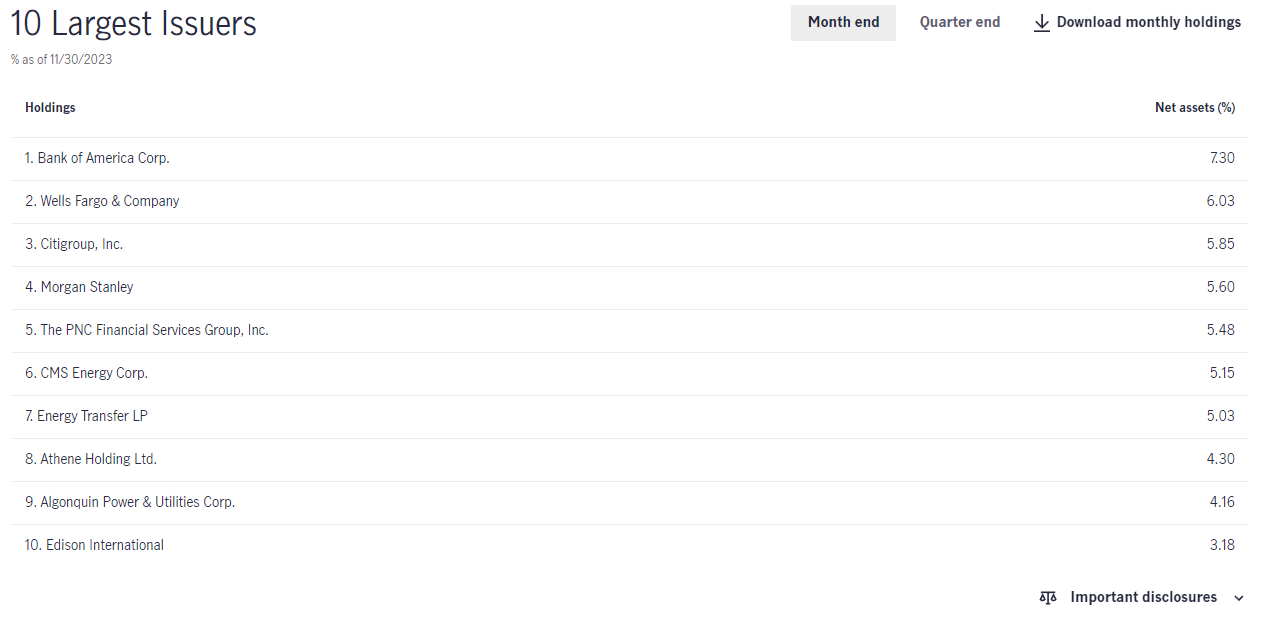

In my previous article on this fund, I showed that the John Hancock Preferred Income Fund III is heavily exposed to the banking sector. This continues to be the case today, which we can clearly see by looking at the largest holdings in the fund. Here they are:

{kind=link}

We do see a few changes here from the last time that we looked at this fund. In particular, NiSource ( NI ) has been removed from the fund’s largest holdings list. In its place, we have Edison International ( EIX ), which is a major utility company that serves Southern California. We also see a number of weighting changes, such as various banking institutions having a much more dominant position among the top five positions in this fund. The last time that we discussed the fund, Algonquin Power & Utilities ( AQN ) was the second-largest position in the fund. The fact that banks are accounting for such a large portion of the fund’s largest positions could be concerning to those investors who remember the events of March 2023. At that time, Silicon Valley Bank, Signature Bank, and First Republic Bank failed in a series of some of the largest banking collapses in the history of the United States. The banking sector is still under a considerable amount of stress today, with the nation’s banking sector sitting on somewhere around $650 billion in unrealized losses from their bond and loan portfolios. The Federal Reserve’s emergency bank lending facility seems to have prevented any further bank collapses though, and there has not been any especially bad news out of that sector for three quarters now. As such, the situation has probably calmed down enough that risk-averse investors do not need to worry too much about having bank preferred issues in their portfolios. Investors who may be concerned about the sector may wish to limit their exposure by only holding a small position in a fund like this one and focusing their attention elsewhere, however.

As I mentioned in my previous article on this fund:

The first thing that we notice here is that all of the companies in the fund’s largest positions list are either utilities or banks. This is not uncommon for a preferred stock fund because banks and utilities are the largest issuers of preferred stock in the market. As a result, almost any preferred stock fund will be very heavily weighted towards these two types of companies. With that said though, usually the overwhelming majority of companies in the top ten list are banks. This is due to international banking regulations that require banks to hold a certain percentage of their assets in the form of Tier One capital. Tier One capital refers to that proportion of a bank’s assets that are not simultaneously a liability to somebody else (such as a depositor). When regulators require that a bank increase its Tier One capital, its only options are to issue either common or preferred stock. The bank will often choose to issue the preferred stock in order to avoid diluting the common stockholders. A utility does not have these regulations to follow but they become heavy issuers of preferred stock due to the cost of their infrastructure. It is extremely expensive to build a network of utility-scale infrastructure over a wide geographic area. The utility company will often finance the construction of this infrastructure with debt, but the company will usually want to avoid taking on too much debt and becoming overleveraged. Thus, it will often issue preferred stock to partially cover the expenses so that it can avoid too much debt or common stock dilution.

Curiously, the fund’s website does not provide the fund’s current sector allocations. The fact sheet does not provide this information either. CEF Connect states that 4.41% of the fund’s assets are invested utilities, but that is very hard to believe as CMS Energy ( CMS ) by itself is listed at 5.15% of the fund’s portfolio on the website. The top ten positions list also mentions a few other utilities that have noticeable ratings. Thus, it seems almost certain that the figure provided by CEF Connect is incorrect. It would be nice to have this information in order to determine how much exposure the fund actually has to each of these sectors. After all, that information is very important to anyone who is seeking to properly diversify their portfolios across sectors.

The Sell Thesis

As mentioned in the introduction to this article, the market has been very excited about the prospect of a monetary policy pivot by the Federal Reserve this year. This excitement has been building over the past few months, and it is the biggest reason for the stock and bond market rallies that began in mid-October. The federal funds futures market currently expects that the effective federal funds rate will decrease by 1.384% by the end of 2024:

{kind=link}

This is a bit less than the market expected a week ago, before the release of the minutes by the Federal Open Market Committee, but it still represents five to six 25-basis point cuts in the federal funds rate over the next eight meetings of the Federal Open Market Committee. As the market does not expect a rate cut in January, the committee can only fail to reduce rates at one or maybe two of the remaining meetings in 2024. That does not seem particularly likely to occur unless the economy is in an incredibly severe recession. Recent jobs data and gross domestic product growth figures do not support the idea that the economy is about to enter a recession, despite the fact that right now most of the gross domestic product growth is caused by Federal Government spending (the Federal budget deficit is actually higher than economic growth). Policymakers in Washington do not like the economy to enter into a recession during a presidential election year, so it seems likely that they will do everything possible to keep the economy strong enough to make interest rate cuts unneeded. Thus, the Federal Reserve will face accusations of trying to influence the election by cutting rates more than needed. It typically tries to avoid such situations. There has only been one time in history when the Federal Reserve has cut by 125 to 150 basis points if there was no recession, so it seems highly unlikely that it will do it in 2024. That means that the market is expecting a much bigger interest rate decline than is likely to occur.

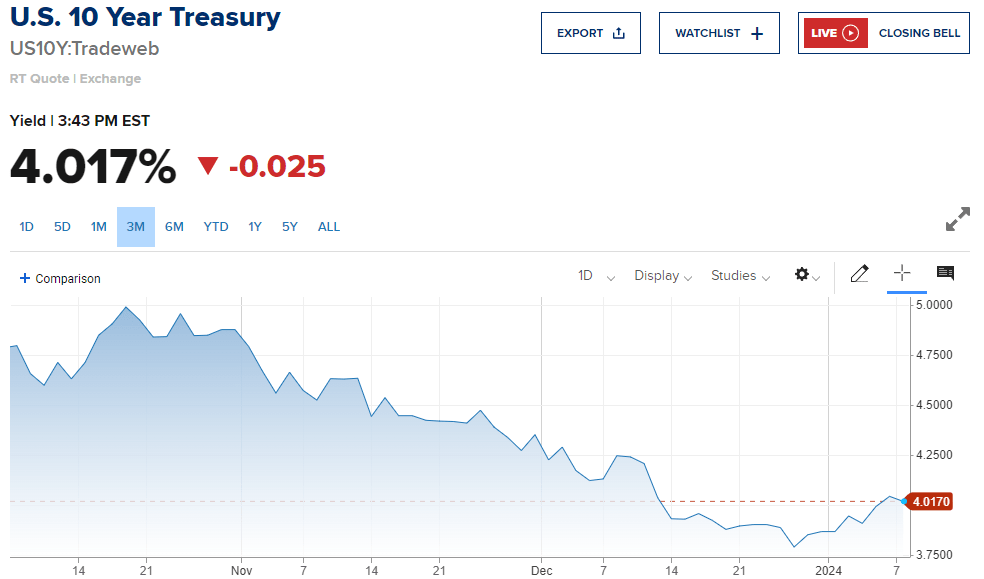

The market has bid up the price of most fixed-income securities in anticipation of the federal funds rate cut that is unlikely to occur. For example, take a look at the yield of the ten-year U.S. Treasury note over the past three months:

{kind=link}

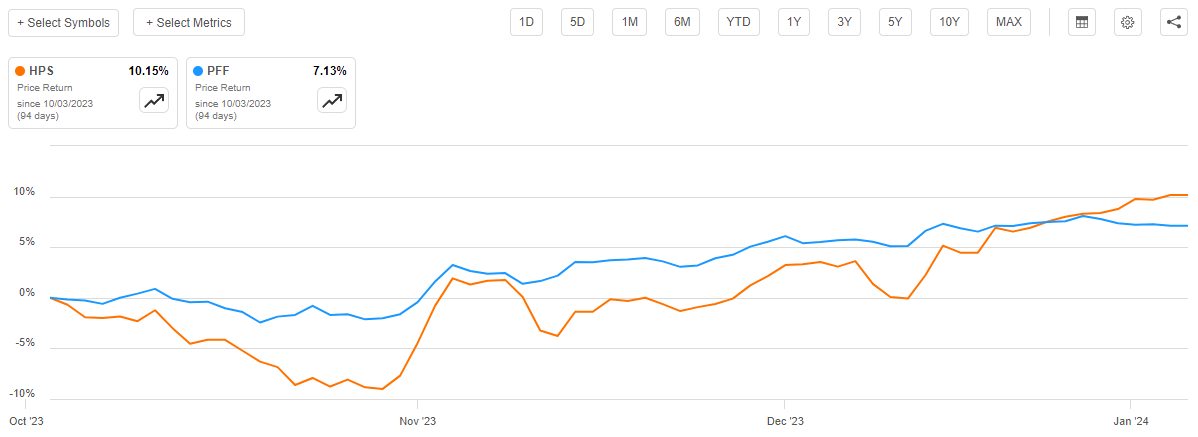

The price of the bond moves inversely to the yield, so this roughly 100-basis point decline in yield has caused the price of the bond to increase. The same thing occurred in the price of preferred stock, such as the preferred stock that is held by the John Hancock Preferred Income Fund III. As we can see here, the fund’s share price is up 10.15% since the first trading day in October:

{kind=link}

We can see that the fund has outperformed the preferred stock index over the period, which is exactly what we would expect considering that this is a leveraged preferred stock fund. The important thing for right now though is that this fund has clearly gotten caught up in the market exuberance. Fortunately, the fund’s net asset value per share is up 9.99% over the same period, so this is not a case of the fund’s shares substantially outperforming its underlying portfolio. We have seen that with a few other funds, such as the BlackRock Limited Duration Income Trust ( BLW ) that I discussed over the weekend.

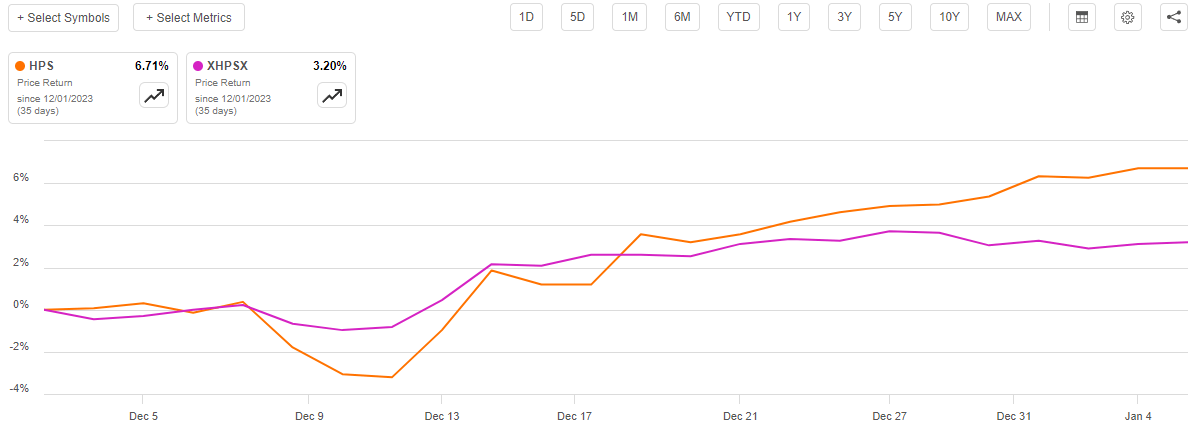

As a result of this capital appreciation, it seems likely that this fund will give up some of its gains in the very near future. We are starting to see this already in the net asset value. As we can see here, the fund’s share price is up 6.71% since the start of December but the fund’s net asset value is only up 3.20% over the same period:

{kind=link}

We can see that the fund’s net asset value has generally been declining over the past week or so, but the share price has not. This adds further confirmation that the fund is starting to look overpriced given the likely forward trajectory of the fixed-income market. Investors would be best off taking some of their recent gains off of the table before the share price corrects.

Leverage

As is the case with most closed-end funds, the John Hancock Preferred Income Fund III employs leverage as a method of boosting its effective yield and total return beyond that of any of the assets in the portfolio. I explained how this works in various articles on other closed-end funds:

Basically, the fund borrows money and then uses that borrowed money to purchase preferred stocks or similar income-producing securities. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that leverage is a less effective strategy today with interest rates at 6% than it was a few years ago when interest rates were basically zero.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally prefer a closed-end fund’s leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the John Hancock Preferred Income Fund III has leveraged assets comprising 38.27% of its portfolio. This is obviously considerably higher than the one-third of assets level that we would ordinarily prefer a closed-end fund to possess. However, as I have discussed in various previous articles, fixed-income funds are typically able to sustain a higher level of leverage than an equity fund due to the fact that its assets are somewhat less volatile. In the end, it is volatility that causes the biggest problem when leverage is used, just like volatility can cause problems for an individual who purchases stocks with margin. The fund’s leverage is not substantially higher than the leverage that is employed by some other fixed-income funds, so it is probably acceptable right now.

It is important to note that the fund’s leverage will cause this fund’s share price to decline much more than the preferred stock index in a market correction. As we have already discussed, a market correction seems likely to occur at some point in the near future, so this leverage increases the need to take some profits before this happens.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the John Hancock Preferred Income Fund is to provide its investors with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio that consists primarily of preferred stock issued by banks and utility companies. These securities deliver the majority of their investment return in the form of direct payments to the shareholders and usually boast somewhat higher yields than investment-grade securities. They cannot really compare to junk bonds in terms of yield though, so this fund will not be able to generate as high a level of income as those funds that invest in those securities. This is generally priced into the shares though, and the fund might have a greater opportunity to earn profits by trading securities and exploiting price changes that occur with interest rate movements. The fund collects all of the money that it receives from these activities and pays it out to its shareholders, net of its expenses. We can expect that this will result in a respectable yield.

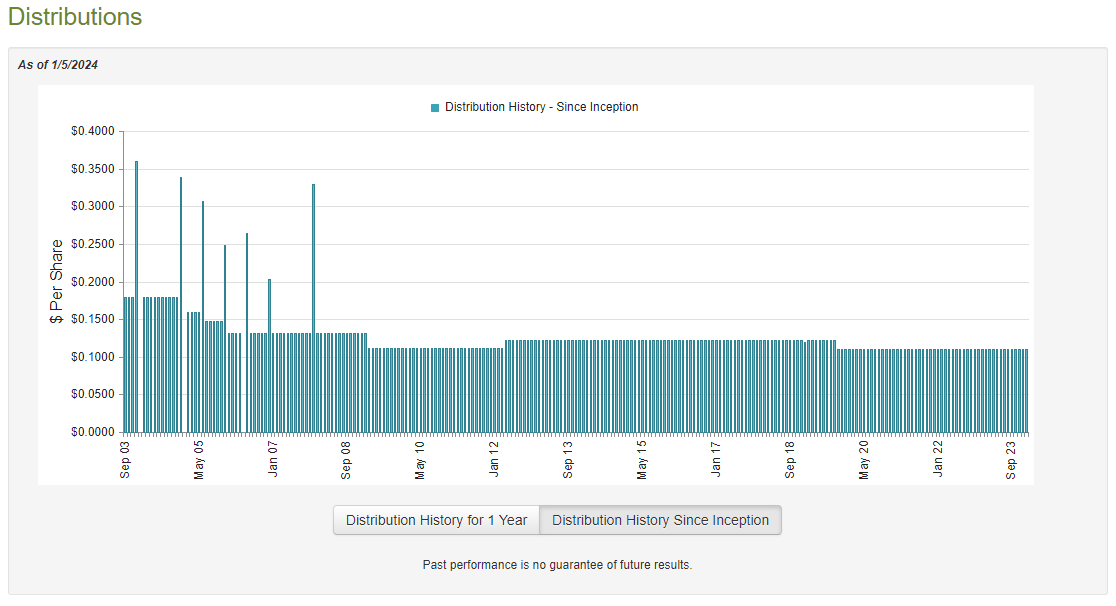

This is certainly the case, as the John Hancock Preferred Income Fund III pays a monthly distribution of $0.11 per share ($1.32 per share annually), which gives it an impressive 9.22% yield at the current price. The fund has not been perfectly consistent throughout its history with respect to its distribution, but it has generally managed to do a much better job than most other fixed-income funds. As we can see here, the fund has had a relatively stable distribution over the past ten years, with only a single distribution cut prior to the COVID-19 outbreak:

{kind=link}

This history will probably appeal to any investor who is seeking to earn a relatively safe and consistent income from the assets in their portfolios. After all, this is one of the only fixed-income funds that did not cut its distribution in response to the shift in monetary policy that occurred in 2022. In fact, it is somewhat confusing why this fund did not cut the payout as that event caused any fund that was not heavily invested in floating-rate securities to take significant losses. This fund does not invest in those securities, so we should take a look at its finances to determine why it was able to accomplish a feat that its peers could not. It is certainly possible that this fund is distributing too much money to its shareholders and destroying its net asset value.

Fortunately, we do have a fairly recent document that we can use for the purpose of our analysis. As of the time of writing, the fund’s most current financial report corresponds to the full-year period that ended on July 31, 2023. As such, this report will not include any information about the fund’s performance over the past five months. However, this is a newer report than the one that we had available to us the last time that we discussed this fund, so it is nice to have an update on the fund’s financial situation to determine the distribution sustainability. It will also give us a good idea of how well the fund was able to take advantage of the strength that was present in the bond market during the first half of 2023 due to the market’s expectations of a late-2023 pivot by the Federal Reserve. While the market proved to be wrong with its predictions, the fund might have still had the opportunity to make some trading profits.

During the full-year period, the John Hancock Preferred Income Fund III received $31,265,331 in dividends and $19,357,572 in interest from the assets in its portfolio. The fund had to pay foreign withholding taxes on some of this income, which gave it a total investment income of $50,505,961 over the full-year period. The fund paid its expenses out of this amount, which left it with $30,901,333 available for shareholders. That was, unfortunately, nowhere near enough to cover the $42,037,805 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning since we would normally prefer a fixed-income fund such as this one to fully fund its distributions out of net investment income. This fund obviously failed at that task.

However, there are other methods through which the fund can obtain the money that it needs to pay the distributions. For example, it might be able to take advantage of changes in preferred stock prices that accompany interest rate changes to earn some profits. Realized capital gains are not considered to be investment income for tax or accounting purposes, but they obviously represent money coming into a fund that can be distributed to the investors. Unfortunately, the fund failed miserably at this task over the full-year period. It reported net realized losses of $37,813,820 and had another $23,833,834 net unrealized losses. Overall, the fund’s net assets declined by $71,318,563 after accounting for all inflows and outflows during the period.

Thus, the fund clearly failed to cover its distributions over the most recent reporting period. This confirms many of our suspicions that it probably should have cut the payout following the devastation of the fixed-income market in 2022. The fact that the fund is maintaining its distribution anyway is destructive to its net asset value and will make it harder and harder to sustain the current payout in the long term. This actually supports our thesis that it is time to start reducing positions in this fund.

Valuation

As of January 5, 2024 (the most recent date for which data is currently available), the John Hancock Preferred Income Fund III has a net asset value of $13.87 per share but the shares currently trade for $14.63 each. That gives the fund’s shares a 5.48% premium on net asset value at the current price. That is substantially above the 2.09% premium that the shares have had on average over the past month, and there is no reason to purchase shares of this fund at a premium right now anyway. This actually supports the idea that we should sell the shares and wait for a better time to get back in.

Conclusion

In conclusion, the John Hancock Preferred Income Fund III has managed to acquire a strong reputation over its history which is probably due to its very strong distribution history. However, this fund appears to be overvalued no matter how we look at it. It is highly vulnerable to a near-term correction in the fixed-income market when the Federal Open Market Committee inevitably disappoints the market’s expectations of interest rates, and the shares are substantially more expensive than is justified by the value of the assets in the fund’s portfolio. When we combine this with the fact that this fund appears to be overdistributing and failing to cover its distribution, it may be time to take profits and reduce our exposure to potential losses.

For further details see:

HPS: Take Profits And Cut Exposure To Potential Near-Term Losses